Oscar Wong/Moment via Getty Images

As the great Benjamin Graham, the father of value investing, indicated at least once, Mr. Market’s moves should be used to one’s advantage. The market can be very irrational from time to time, completely detaching from fundamentals. During times when Mr. Market is willing to pay outrageous prices for the shares you own, it might make sense to take him up on the offer. And when he is willing to sell you stocks at a steep discount to their intrinsic value, you should back up the truck to pick up as many shares as possible.

Such an event occurred on February 15th when it comes to Nano-X Imaging (NASDAQ:NNOX), a fairly early-stage company dedicated to the production of a new type of X-ray that also has a cloud component to it whereby the images taken are sent to its cloud to be securely analyzed. Shares of the company spiked on February 15th, closing up 49.4%, after news broke that tech giant NVIDIA (NVDA) bought a stake in the firm. Such a massive move higher might normally inspire confidence that is warranted. If it were a part of a strategic announcement or if it represented a sizable chunk of Nano-X Imaging’s outstanding shares, then there could be some significant implications from this maneuver. But from how the transaction occurred and because of how small it was, I view this as something of a nothing burger. It does increase the chance, marginally, of some major exit for shareholders in the company. But with fundamentals still suffering, this does not change the pessimism that I have regarding the enterprise.

This doesn’t change anything

The last article that I wrote regarding Nano-X Imaging was published in August of 2022. In that article, I talked about how shares had skyrocketed leading up to that point compared to when I wrote about it prior to that. This was based on some interesting developments that management had announced. The company had also transitioned to generating revenue, but profitability was a problem. Add on top of this some allegations of misdealings that had been out for some time, and also factor in how shares were priced, and I decided to downgrade the business to a ‘sell’. Even after the 49.4% surge on February 15th, shares have massively underperformed the market. They are still down 32.2% from the time that article was published. That compares to the 19.9% upside seen by the S&P 500 over the same window of time.

Author – SEC EDGAR Data

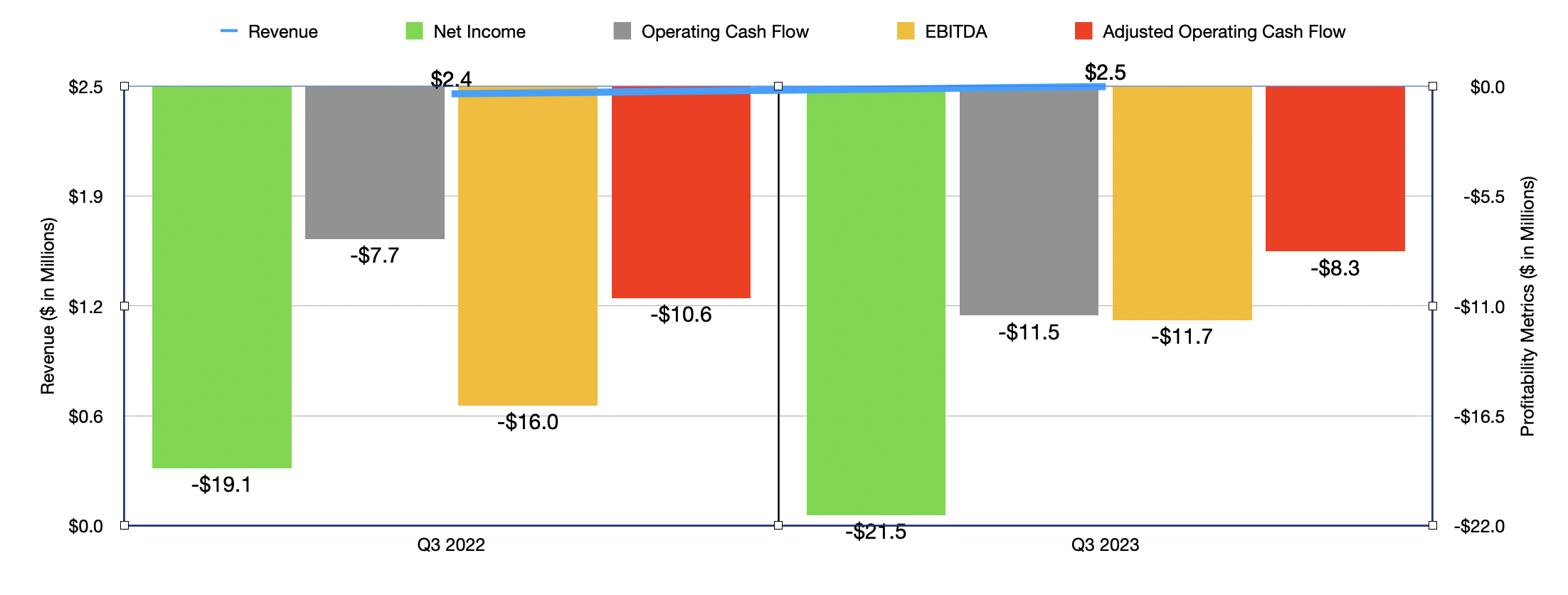

To understand why the stock continues to underperform, we really only need to look at the fundamental data for the business. If you look at the third quarter of the 2023 fiscal year, which is the most recent quarter for which data is available, revenue for the company was less than $2.5 million. That was roughly even with the $2.4 million generated one year earlier. A small amount of revenue can be fine. But it cannot be fine when profits and cash flows are materially negative. The company went from generating a net loss of $19.1 million in the third quarter of 2022 to generating a loss of $21.5 million the same time of the 2023 fiscal year. Operating cash flow went from negative $7.7 million to negative $11.5 million. To be fair, there were some areas in which the business improved. If we adjust operating cash flow for changes in working capital, it improved marginally from $10.6 million in the red to $8.3 million in the red. The same thing happened with EBITDA, going from negative $16 million to negative $11.7 million.

Author – SEC EDGAR Data

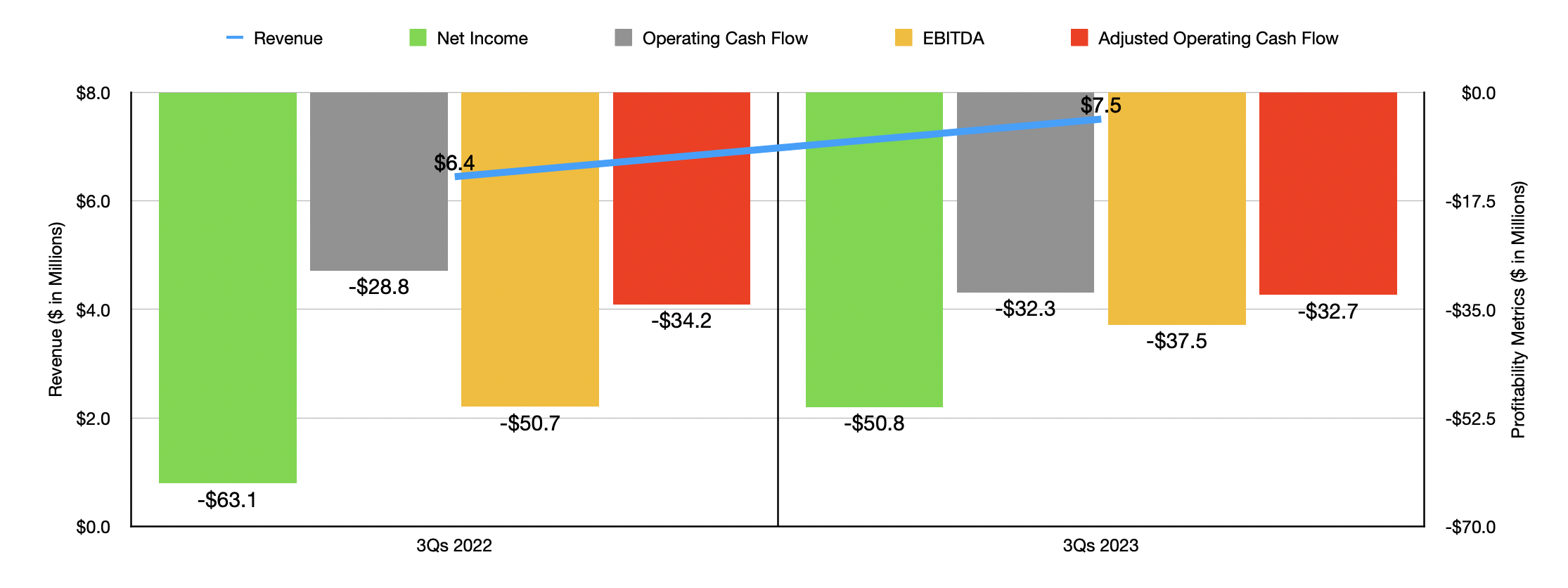

The third quarter was not a standalone issue. If you look at the chart above, you can see results for the first nine months of 2023 relative to the first nine months of 2022. Yes, revenue did increase modestly. And it’s also true that some bottom line results improved year over year. But the company is still very much in the red in these regards. In fact, if it weren’t for the fact that the company has net cash of $92 million on its books, I would be wondering about its ability to survive, especially after seeing its share price decline by so much over the past year or so.

Of course, when dealing with anything in the heavily regulated medical space, the fundamental picture of a company can change rather rapidly. Regulatory approvals and sudden material improvements in technology can result in fundamentals going from awful to fantastic in short order. And to be perfectly fair to Nano-X Imaging, it has been coming out with some interesting developments as of late. The most recent was announced on February 13th when the company announced that one of its subsidiaries that focuses on deep learning medical imaging analytics received FDA clearance for an offering called HealthFLD. This is an AI software that can be used to provide analysis of the human liver. The goal here is to help doctors detect fatty liver. That is a rather large market opportunity considering that around 24% of all adults in the US are believed to suffer from metabolic dysfunction associated steatotic liver disease.

I think it’s also important to point out that the company’s revenue picture is still very early stage. What I mean by this is that, the company only just recently started selling and deploying its imaging systems. In fact, most of its revenue to date has actually come instead from its teleradiology services and AI solutions. And this is where the angle regarding NVIDIA is interesting to many. Over the past year or so, shares of NVIDIA have skyrocketed because of the company’s ability to benefit from the AI boom. In the first nine months of its 2023 fiscal year, the company saw its revenue come in at $38.82 billion. That’s 85.5% higher than the $20.92 billion generated the same time one year earlier. Even more impressive was the fact that net profits skyrocketed from $2.95 billion to $17.48 billion. According to management, the Compute & Networking part of the company saw revenue surged by 158.9% from $11.40 billion to $29.51 billion. This was driven by a 193% increase in compute GPUs because of a surge in the global demand for training and inferencing for large language models, as well as other applications like generative AI.

You would be hard pressed to find an industry that’s larger than the medical space. But even if we just focus on the global medical imaging market that Nano-X Imaging caters to, you would see that the market opportunity is expected to grow at an annualized rate of about 5.6%, eventually hitting $52.03 billion by 2032. Getting in at the ground floor of a cutting edge technology can be very profitable and a partnership between the two firms could prove beneficial for both sides. However, I do believe the market is getting ahead of itself. I say this because there was no formal announcement of any sort of relationship between the two enterprises. There doesn’t seem to be any deal that has been explored and, in the grand scheme of things, the investment made by NVIDIA is paltry.

NVIDIA – SEC EDGAR

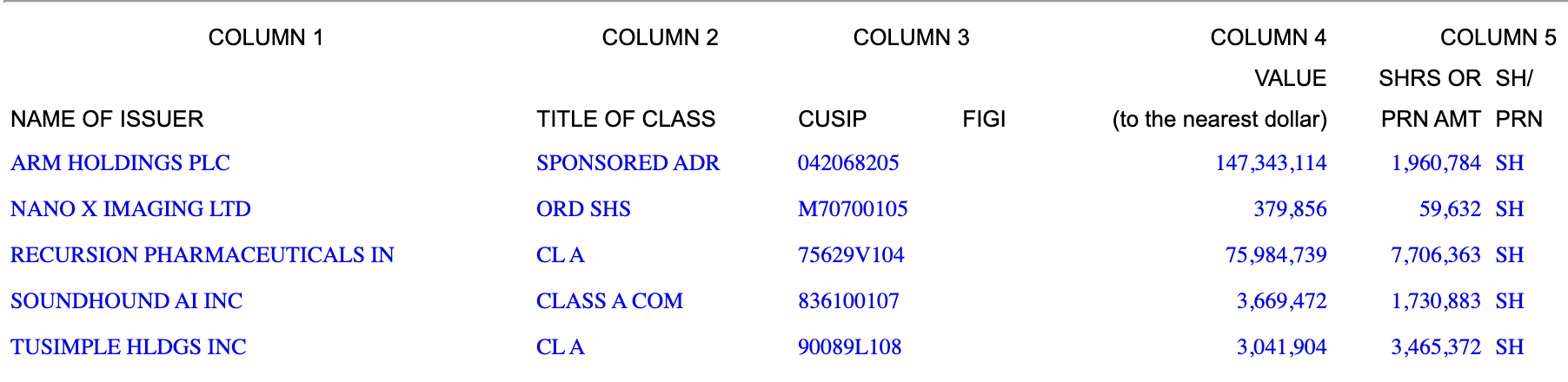

If the management team at NVIDIA we’re so inclined, they could easily snatch up Nano-X Imaging for a song. I say this because NVIDIA’s $1.83 trillion market capitalization dwarfs the $548.5 million market capitalization of Nano-X Imaging. Instead, the firm ended up acquiring 59,632 shares of Nano-X Imaging on the open market. That equates to only 1.07% of all shares outstanding of the enterprise. By comparison, the management team at NVIDIA put a great deal more capital into literally all of the other investments that it disclosed having a stake in on February 14th. At the time the documents were filed, the stake in Nano-X Imaging was worth only $379,856. Even if we go with the next smallest firm, that was an investment of over $3 million. The largest, meanwhile, involved a $147.3 million investment in Arm Holdings (ARM). In fact, when looking at the $230.4 million that NVIDIA split between five different investments, only 0.16% was allocated toward Nano-X Imaging.

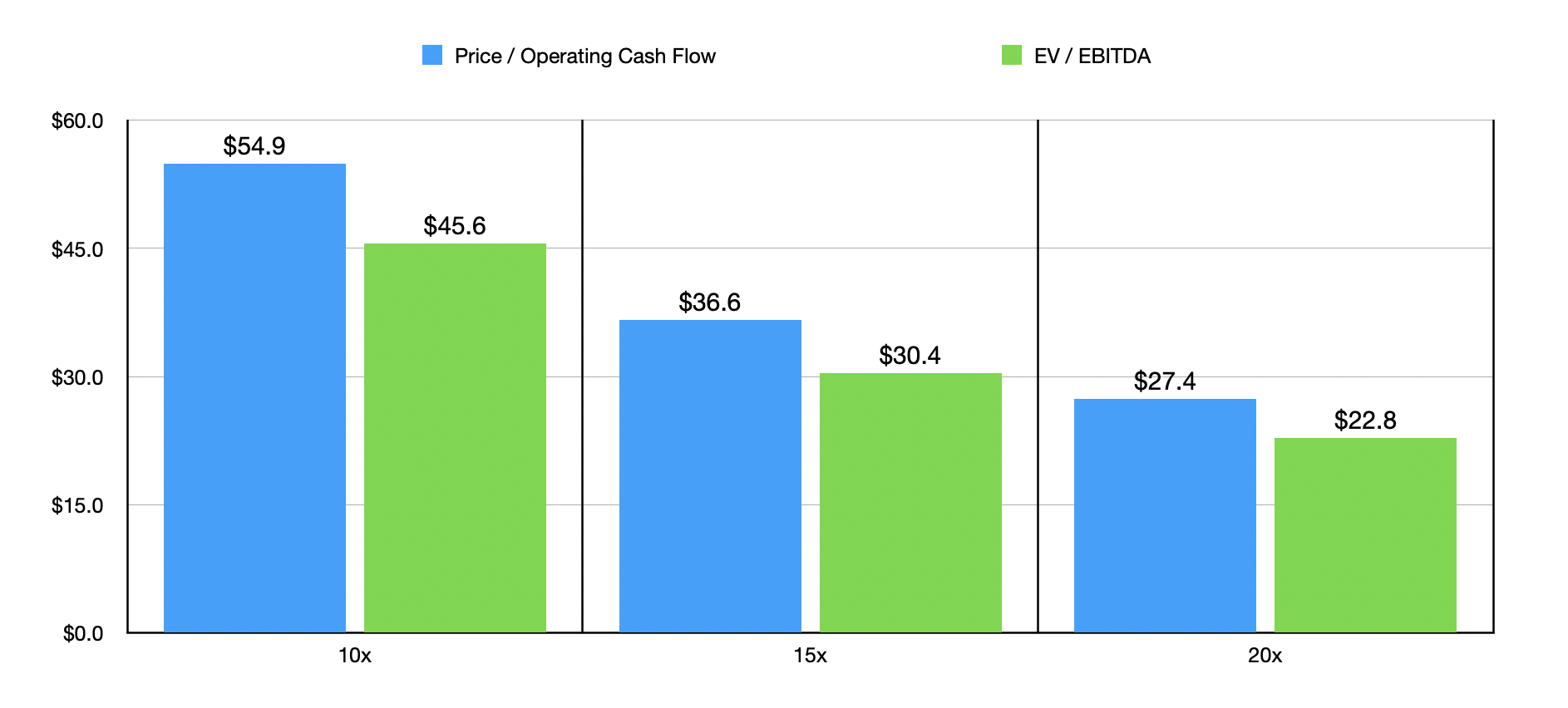

My mindset might be different if there had been some big announcement or some deal worked on between the two companies. If there had been, then I would definitely be optimistic. My mindset might also be more upbeat about the matter if the fundamental condition of Nano-X Imaging was not so poor. As you can see in the chart below, the company would need to generate at least $27.4 million of adjusted operating cash flow or $22.8 million of EBITDA to be fairly valued if we were to assume a trading multiple on a price to operating cash flow basis or on an EV to EBITDA basis of 20. And if we assume a number lower than this, those numbers increase even further. By comparison, the bottom line pain the company is experiencing is rather significant.

Author – SEC EDGAR Data

Takeaway

As things stand, I think that there is a marginal chance that Nano-X Imaging could end up with something more substantive from NVIDIA. But I don’t think it’s wise to make an investment on something so speculative and something that, frankly, is probably unlikely to occur. If fundamentals were solid for Nano-X Imaging or if we had some better insight into the adoption of its newer technology, I might view this more optimistically. But that is not the case. And when you consider the overall health of Nano-X Imaging at this time, I believe that the ‘sell’ rating still makes sense at this time.

Q2 2024 Earnings Call Transcript")