Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Last November, global regulators and clearing houses war-gamed the collapse of a major financial institution to see how they and their members would manage the default.

This is a classic “dull but v v v v important” issue that rarely gets the attention it should, because a lot of people understandably lose the will to live as soon as you start talking about financial plumbing.

After 2008 more and more financial transactions are centrally cleared to protect institutions from cataclysmic failures by someone on the other side. But this pools helluva lot of risk in these central counterparties (CCPs), so everyone is naturally deeply invested in making sure that even a major member default can’t bring one down.

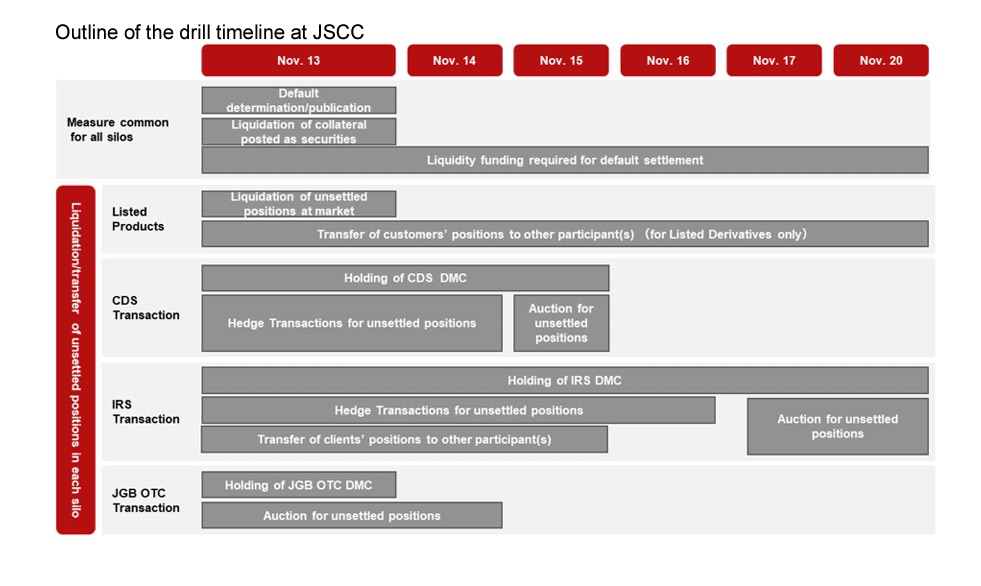

Clearing houses conduct “fire drills” all the time, but the Nov 13-20 event seems to have been the first comprehensive global exercise to see how the different CCPs would the default of a major institution dubbed ACME — A Clearing Member Everywhere.

Here’s an outline from the Japan Securities Clearing Corporation, one of over 30 that took part in last autumn’s “global fire drill” (zoomable version):

It seems everything went fine, but Optiver — a big options market-maker that took part in the fire drill — has some interesting thoughts on one weakness that was revealed: the messiness of any membership bidding for the portfolios of ACME to absorb the shock of its failure.

Optiver’s role in the fire drill was to review and price the hypothetical portfolios of defaulting members and submit bids for all or part of them. This required us to engage individually with each CCP. While in each case we were able to prepare and submit bids, we encountered a wide mixture of different requirements among the various CCPs.

When it came to bidding in the auction, here are some of the things we encountered:

— Different pricing methodologies for bidding.

— Different submission styles. We observed both manual submissions via e-mail or via a portal.

— Different acknowledgement types. Some CCPs required that participants acknowledge announcements (invitation, portfolio sharing), others didn’t.

— Different file formats. Each CCP used a different format on Excel.

— Different timelines. Some CCPs accepted extension requests from participants, others didn’t.

This non-exhaustive list reveals a potential sticking point in a real-life crisis scenario. While we recognise that a fully harmonised process may take some time, the current absence of standardisation increases operational risks. Complexity can lead to confusion, particularly when participants are forced to navigate different requirements in a very short time frame. This could impact market participants’ ability to effectively participate in the auctions, especially during stressed market conditions.

If all of the above were standardised, market participants could have devoted more time to actually pricing the portfolios instead of navigating the assorted requirements.

That sounds pretty sensible, given how quickly things can move in a real crisis. Accidents happen. So having standardised methodologies, processes and file formats across the global patchwork of clearing houses would be a boon.

Btw, in a point in favour of Bill Ackman’s belief in nominative determinism, the chair of CCP Global, the clearing industry’s trade body, is called Kevin McClear.

Q2 2024 Earnings Call Transcript")

{kind=link}