fotostorm

Co-authored by Treading Softly.

The Amazon Prime TV show Reacher has become somewhat of a cultural phenomenon within the United States. It is currently Amazon’s (AMZN) most popular and successful show. The entire premise focuses on a military veteran who’s decided to live a hobo lifestyle, traveling around the United States, and owning little more than his passport and a toothbrush. Before leaving the military, he was in charge of an investigative unit that focused on various crimes, and in his now civilian life, he frequently stumbles upon large conspiracies or other criminal organizations that he helps to take down in a vigilante-style. He frequently ends up in the wrong place at the right time to be the hero.

When it comes to the market, sometimes timing can be viewed as everything. As an income investor, I believe in spending more time in the market than trying to time the market. This means that I am willing to be a net buyer of stocks in almost every market situation because I find that the longer I spend in the market, the greater my income becomes. I don’t try to gamble on what time it is best to enter into a position.

Doing this, I recognize that there are going to be times when my entry point is less than ideal, but can still work out in the long run because of my ability to be patient while being paid. Sometimes, you might buy stock in a good company at the wrong time, and the investment might be a more volatile ride than you bargained for.

Today, I want to take a look at one investment that I think is an outstanding time to buy now, even though I bought it six months ago, and that may not have been the best time to do so.

Let’s take an honest look together.

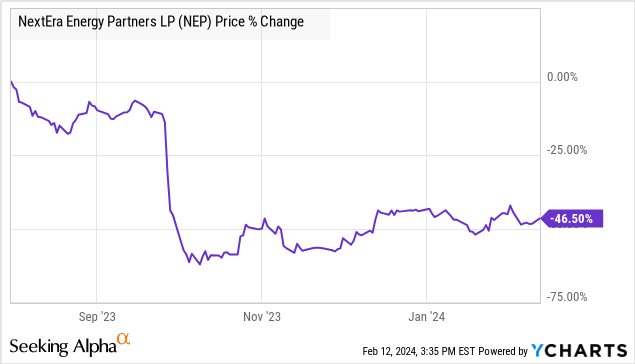

Bad Luck and Trouble

In hindsight, we bought NextEra Energy Partners, LP (NYSE:NEP) too early. It isn’t fun when you invest in a stock and 6 months later the price is half of what you paid. Especially when most of that fall occurs over a couple of days.

Yet it is a reality of investing, that sometimes you will hold a company that releases bad news that has a material impact on market sentiment. You don’t have to be a veteran investor to see where the bad news hit:

There is no sugarcoating it, that kind of fall hurts. Yet, as we recently discussed, it is the type of volatility that you can expect to happen from time to time. Naturally, it is always nice to avoid those cliffs, but it is like a boxer trying to avoid being punched. Of course, they want to avoid being hit, but the reality is that getting hit is part of the sport.

The real test of investing is how you respond when it happens to you. Can you keep a clear head, and avoid panicking? With NEP, we quickly decided to maintain a buy. The market was upset at NEP’s outlook for growth going from 12% annual growth to 6%. That is a huge decrease. Yet it is still growing. We wrote to our subscribers:

“The bottom line is that a company that can reasonably expect 5-8% dividend growth would be worth entertaining at a starting yield below 7%. With a starting yield of 11%+, it is extremely interesting. The market is right that NEP is worth something less with a growth rate of 6% as opposed to 12%, but we believe the sell-off is much more dramatic than the numbers justify.”

Of course, the market might be a bit leery of NEP’s new guidance. Certainly the price indicated that the market simply did not trust management’s ability to deliver on guidance. Since that article, NEP has now raised its distribution twice. The new distribution is $0.88, 3% higher than when NEP slashed guidance.

In addition to raising the distribution for Q4, NEP provided guidance that the fourth-quarter 2024 distribution, payable in February 2025 will be $3.73 annualized. ($0.9325/share quarterly). It is interesting to note that historically NEP has provided a range for distribution guidance. Now they are providing a precise number. We believe this is likely because management wants to regain trust.

Instead of a range, management is telling us exactly what the target is. This provides investors with something tangible to hang their hat on, and it will be a distinct hit or miss. The declared distribution will either be $0.9325 in February 2025, or management failed. There is no fudging and no in-between. While this increases the negatives if management fails to hit the target, it is a strong statement from management about the confidence in their ability to reach that target.

Importantly, this growth rate will be achieved without any new acquisitions, as management has identified 985 MW of repowering opportunities, which can be done without needing to raise equity capital.

Management hit the revised guidance for 2023 and is remaining committed to its longer-term guidance of 5-8% growth going forward. The guidance cut in 2023 was significant, and management blamed the rising cost of capital forcing them to pull in their horns. For NEP, it is crucial to be able to meet guidance and regain the trust of investors. The most significant point to draw from Q4 earnings is that management is committed to providing 6% distribution growth without raising equity.

If it can achieve that target, then NEP’s shares are extremely cheap right now. How much is an investment paying $3.52/year in distributions with 6% annual growth worth? We would argue that it is easily worth something in the $40s. It is now in NEP management’s hands to prove that it can deliver. It is a delicate balancing act for management to continue providing growth, while also dealing with its CEPF maturities and its balance sheet.

So far, management has delivered. NEP sold the Texas Pipelines and has raised enough cash to pay off two CEPFs. It has refinanced $750 million in debt at 7.25% – a higher interest rate but lower than many feared. This will remove the debt maturing in 2024.

In the words of Muhammed Ali:

“You don’t lose if you get knocked down; you lose if you stay down.”

NEP’s road isn’t an easy one, but management has a good plan, and management is executing that plan. The price of shares is down, but our income is going up.

Conclusion

NEP’s management had to eat crow and admit that their original guidance was no longer founded in reality. Because of this, investors have beaten down the stock’s price, and rightfully so. Many investors use that forward guidance for their estimates of how much they think the investment is worth and what they’re willing to pay for it now, assuming a future return. That future return is now a lot slower growth.

Management is working diligently to repair that reputation as well as right the stock towards the direction they’re going. The dividend is still growing and the outlook is still strong, but it is going to be a longer road. For many, they are going to hit the exit. For others who are walking this road along with me, we’re going to take the road less taken and be willing to hold and collect income through this environment. I suspect that this road will reward us richly in the long run, but only the future will be able to tell us that answer.

When it comes to retirement, I think many of us don’t want to live the life of Jack Reacher. We don’t want to necessarily find ourselves battling criminal conspiracies, but we want to be able to have the income to be able to enjoy watching shows like that if that’s our interest.

Having a portfolio that generates income so that you can pay for your Amazon Prime subscription, your light bill, or your car insurance is a massive benefit because every bill that your portfolio can pay is one less bill that you have to worry about figuring out how to pay in the future. For many, their dividend and income portfolio can pay all of their bills and leave excess to reinvest and enjoy hobbies. Once you’ve achieved that, you’re living what so many investors and retirees dream of living, and you found true financial security.

That’s the beauty of my Income Method. That’s the beauty of income investing.

Q2 2024 Earnings Call Transcript")