Yuichiro Chino/Moment via Getty Images

Investment Thesis

Arista Networks (NYSE:ANET) is a leading enterprise cloud network technology company that has been on a tear, returning roughly six times the S&P 500’s 110% since the pandemic lockdowns. But the relevancy of those returns really stood out since ChatGPT was launched and AI/Applied Machine Learning was finally deployed in the enterprise. Since then, Arista’s networking products have been highly sought after by enterprise companies.

The company released its Q4 and full-year FY23 results yesterday in what was widely expected to be an earnings beat by the Santa Clara, CA-based company. In my opinion, the theme of the earnings call was conservatism, but I think this was a tactic to downplay expectations of the company’s product demand. I will walk through the earnings results below and explain my rationale for buying this stock despite any pullbacks that come its way.

Arista Network’s Q4 Earnings Review

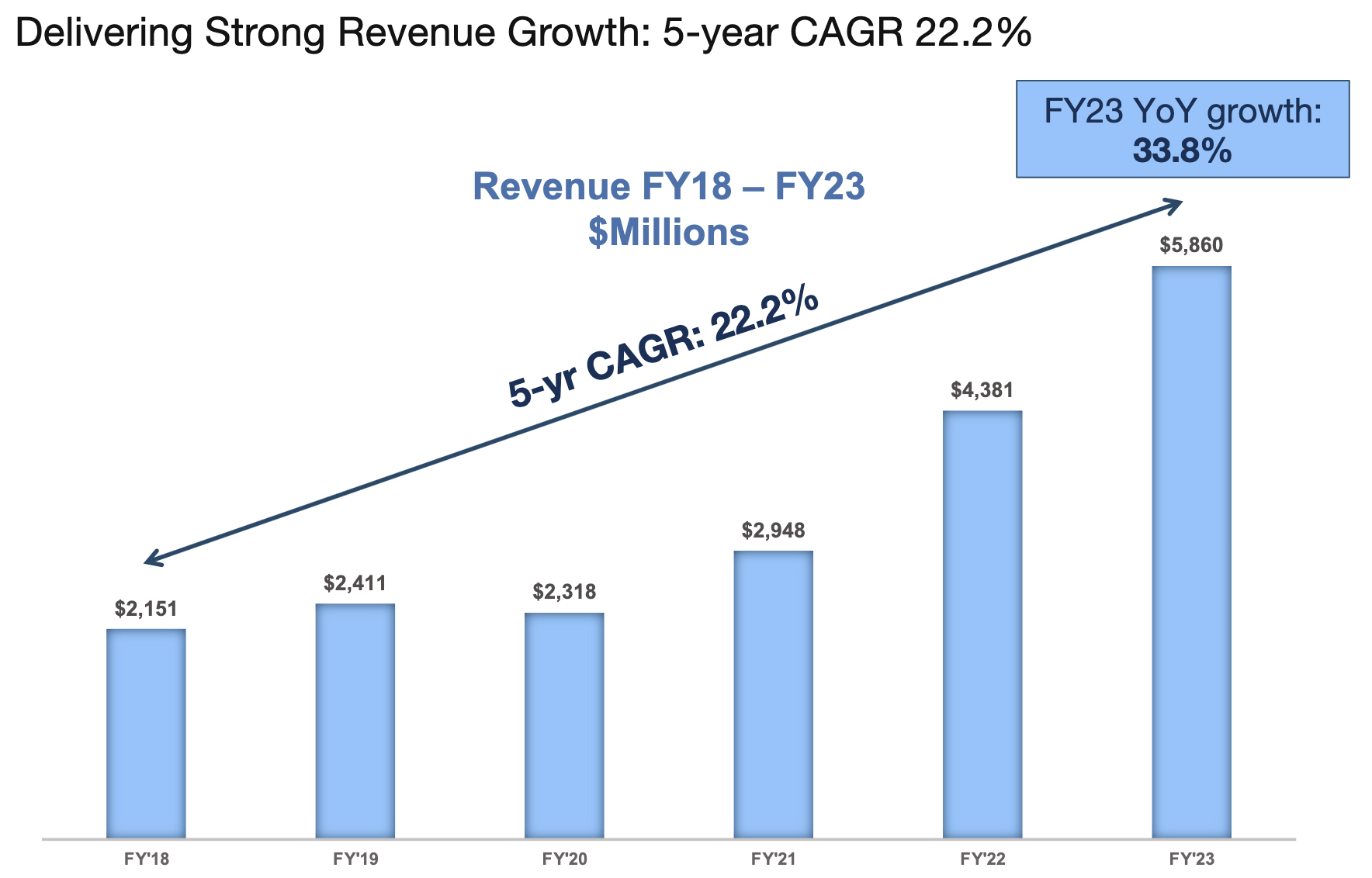

Arista finished the year strong, recording $1540 million in revenue, up 20% y/y, easily beating consensus estimates of $1530 million. During the quarter, management explained that the strength in the quarter was primarily due to the customer mix, “weighted heavily towards enterprise in Q4”, per yesterday’s earnings call. However, management quickly pointed out that this was probably a one-time strong quarterly performance. For the full year, Arista Networks recorded $5860 million worth of revenue. This was particularly impressive in my opinion, given that Arista Networks started last year projecting FY23 revenue would grow ~25% for the full year but eventually grew 33.8% y/y as can be seen below.

Arista Networks Revenue trends, Q4-FY24 investor presentation

Through FY23, the company had been launching networking products and solutions across its product lines, especially its core products, which include cloud, AI, and data center products. Management revealed that its core products had contributed ~65% of Arista’s revenue. While reviewing last year’s numbers, I found that the contribution from its core had been marginally reduced from the 68% contribution last year. At the same time, another growth initiative for the company, campus networking products and solutions, was now contributing ~19% to Arista’s revenue, as per management. As I compared this to management’s commentary last year, I found that campus networking’s contribution to the company’s overall revenue had significantly expanded from a 9% contribution to revenue last year. This is encouraging to me that the company can reach its goal of achieving $750 million in campus networking revenue by FY25.

Per its FY23 10-K, the company’s sales to its top two enterprise cloud clients, or cloud titans, Microsoft and Meta Platforms, accounted for 39% of Arista’s full-year revenue. The contribution from Arista’s cloud titan customers was down from the 42% the company saw in FY22. Although its contribution slowed from its cloud titans, I will still point out the strength of Arista’s revenue growth rates here and my belief in management’s growth initiatives. These numbers demonstrate the strength in Arista’s campus networking market that I talked about in the earlier paragraph, where contributions from the campus networking product segment expanded significantly despite contributions from its cloud titans slightly decelerating in FY23. Additionally, I also expect contributions from both Meta and Microsoft to pick up again in FY24, especially since both companies revealed plans to increase capital expenditure budgets on their recent calls. Meta Platforms revealed on their Q4 earnings call that the social media giant would be increasing capex by a whopping 23% this year. Meanwhile, Microsoft also said they would be materially increasing their capex sequentially on their earnings call. I firmly believe, these cloud titans, along with other hyperscalers, will be doubling down on building more capacity for their AI projects, and Arista will stand to immensely benefit from that.

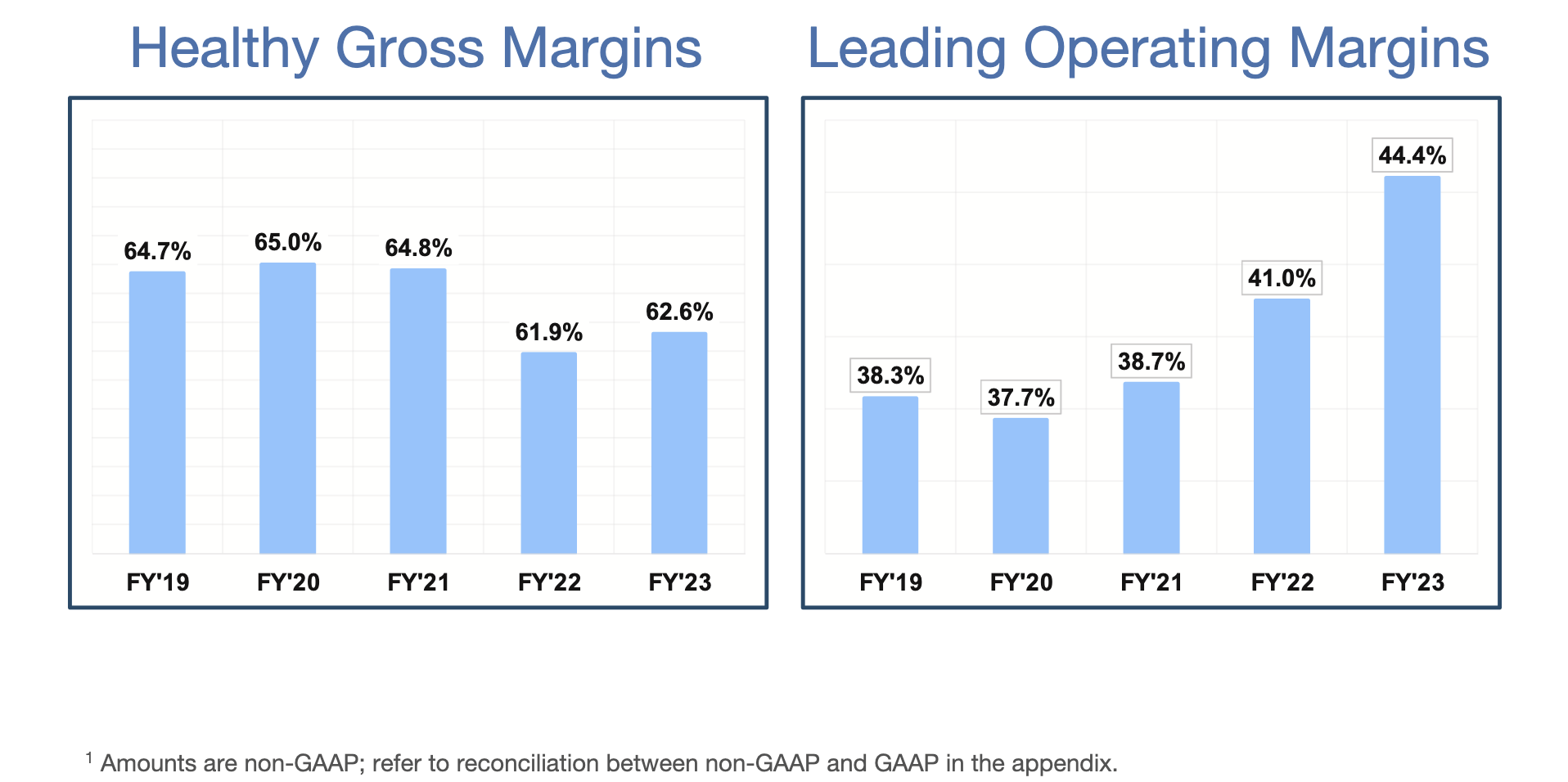

Turning to the company’s margin profile, I observed that Arista’s margins have continued to impress me. Gross margins continued to stabilize at 62.6% for FY23, and management expects the company to work towards its gross margin range of 62%-64% in FY24.

Arista Networks Margin trends, Q4-FY24 investor presentation

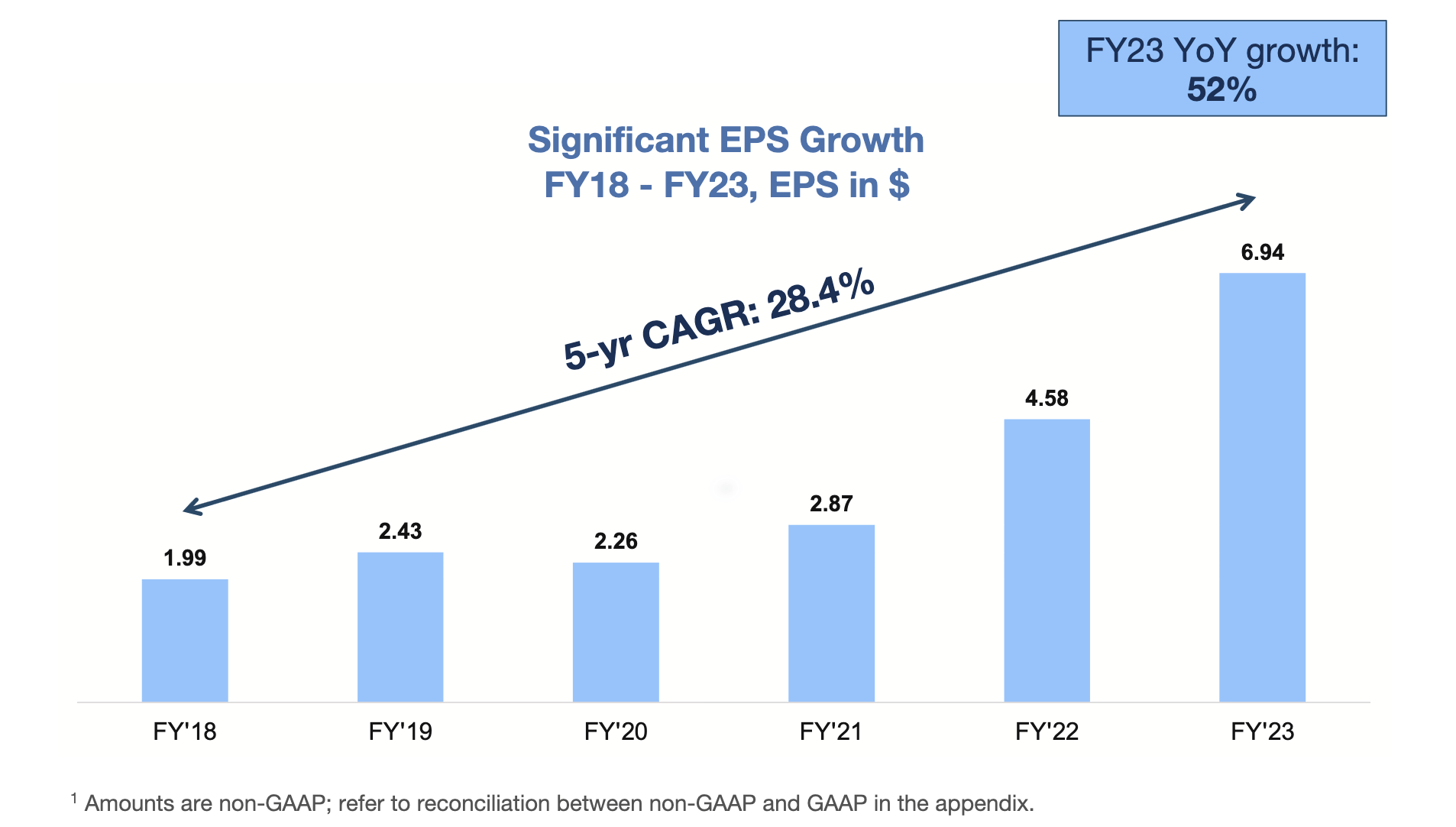

But, what impressed me were their non-GAAP operating margins, which continued their expansion trajectory in FY23 to 44.4%. Management has called for non-GAAP operating margins to normalize in FY24 to ~42%. In terms of EPS, the company recorded EPS at 6.94, up a massive 51.5% y/y and beating consensus estimates by 5.8%. The earnings beat was more pronounced in Q4, as the company recorded EPS of $2.08, beating $1.7 EPS expectations by 22%. Management attributed this Q4 beat to margins that sequentially expanded due to a higher mix of enterprise customers, as I had pointed out earlier.

Arista Networks EPS trends, Q4-FY24 investor presentation

While reviewing Arista’s balance sheet, I did notice its deferred revenue line item had moved up significantly. While current deferred revenue was up 43.5% to ~$915 million, non-current deferred revenue was up even higher at 46.3% to $591 million. Management pointed out that the company does not see deferred revenue as a metric that materially represents its performance. They did indicate that deferred revenue was higher because of some changes in the shipping schedules of their inventory. I will be keeping an eye on moving forward in the next few quarters to see if this keeps trending higher. The company continues to carry a minimal debt load on its balance sheets, with most of the load coming from prior operating lease obligations, which currently stand at $65.5 million. Cash and cash equivalents significantly expanded to $1938 million, up from $671.7 million in FY22.

Why Arista is still a Buy

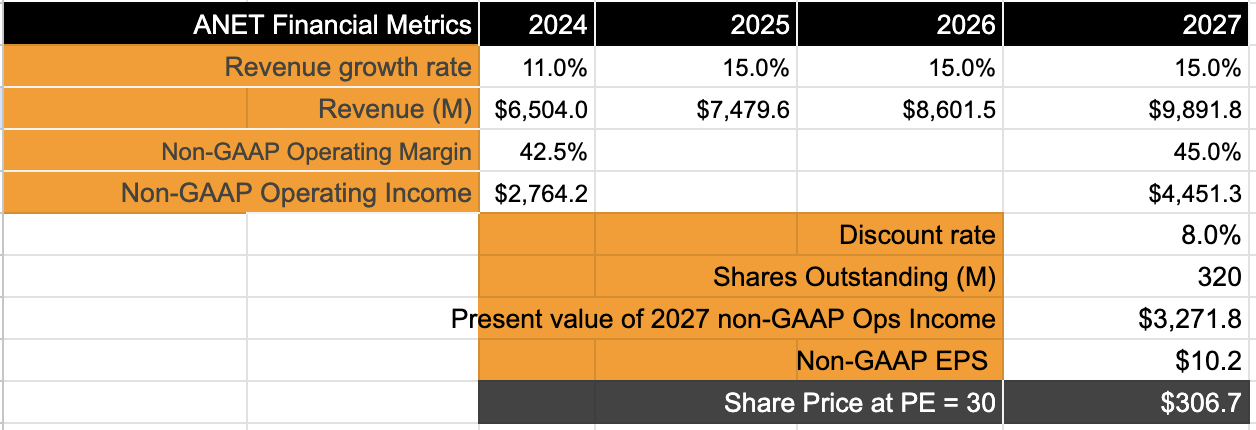

To estimate their long-term operating model, which management alluded to during the Wells Fargo TMT conference last year, The model sees Arista’s revenue growing at a CAGR of ~15% from 2022 to 2027. Management sees AI networking, data centers, and campus networking continuing to grow in that period, which is the thesis for their 15% CAGR growth rates. However, the company guided for slightly lower revenue growth rates this year, between 10% and 12%. I feel this is conservative, as management is trying to manage investor expectations. Given the capex cycles of cloud titans I noted earlier, I am confident that Arista can continue to hit its 15% growth rate easily.

On the margin front, I will assume Arista’s non-GAAP operating margin normalizes to 42.5% in FY24, slightly higher than management’s 42% projections, which I feel is very conservative. I believe margin can easily expand to 45% by FY27, which means non-GAAP operating income will grow at a CAGR of 15.4%, at par with revenue growth.

Author

I will also assume a discount rate of 8% for Arista and a diluted share volume of ~320 million shares. With the above assumptions, I believe that a forward PE of ~30 would be justified for Arista, which means there is 13%-15% upside for Arista from current levels.

Risks & Other Factors to consider

While I am optimistic about enterprise cloud spend in upgrading its datacenter networks resulting in higher capex cycles, these spending trends can reverse if there is a severe economic downturn that may force enterprises to suddenly be conservative and pull in their capex forecasts. These trends could severely impact Arista’s revenue prospects. Competition could pose another headwind to Arista as well. Most recently, Cisco (CSCO), a large incumbent in this space, moved to partner with Nvidia (NVDA) late last year. However, I do not see this impacting Arista’s market share yet. Management briefly noted the strength of their partnership with Nvidia in the Q4 earnings call.

Finally, I also wanted to call out the CFO transition that took place at the end of the year with Arista’s previous CFO, Ita Brennan, retiring. However, I do feel encouraged by the fact that Arista’s new CFO reaffirmed Arista’s targets and long-term operating model with investors on the Q4 call.

Conclusion

After reviewing the Q4 earnings report and listening to management’s commentary, I am convinced that Arista is still well on track to achieve the targets set per its long-term operating model. I see some strong growth prospects in this stock, and this is a buy on any pullback.

Q2 2024 Earnings Call Transcript")