Vepar5/iStock via Getty Images

Performance Assessment

In my last coverage of Charles Schwab (NYSE:SCHW), I had a bullish view, primarily because I expected multiple quarters of margin expansion. However, on January 14, 2024, I changed my stance to a ‘Sell’, as mentioned in a pinned comment update below the article. For the duration of my bullish view, SCHW delivered a total shareholder return of -0.27%, compared to the S&P 500’s (SPY) (SPX) +5.12%, leading to negative alpha of 5.39%. For the duration of the ‘Sell’ view since January 14, 2024, until today, SCHW has delivered a total shareholder return of -0.99% compared to the S&P 500’s +5.46%, leading to alpha of +6.45%. Altogether, this amounts to +1.06% of alpha generation.

Thesis

I am now remaining on the sidelines with a neutral view on Charles Schwab as I note the following:

- A 2024 ‘transitional year’ is unlikely to put SCHW in the alpha-leaders pack

- Key metrics still need to indicate signs of revenue profile improvement

- Discounted valuations make a ‘Sell’ less compelling

A 2024 ‘transitional year’ is unlikely to put SCHW in the alpha-leaders pack

Charles Schwab’s CEO began the conference call with the following statement in his opening remarks:

2024 is likely to be somewhat of a transitional year from a financial standpoint…

– CEO Walter Bettinger in the Q4 FY23 earnings call

Given the bullish markets currently, I interpret this statement as a strong signal that Charles Schwab is unlikely to be amongst the stocks enjoying strong outperformance tailwinds. And the data agrees:

Total Revenue (USD mn) (Company Filings, Hunting Alpha Analysis)

Overall revenues have de-grown at an accelerated YoY clip in recent quarters. This is the main weakness in Charles Schwab right now but not the only one as EBIT margins too have been eroding steadily from 40%+ to less than 30%:

EBIT Margin (Company Filings, Hunting Alpha Analysis)

This is contrary to my original expectations when I had rated the stock a ‘Strong Buy’:

Earlier Margin Expansion Thesis Point (Hunting Alpha’s Last Article on Charles Schwab)

As we will see in the next section, these catalysts on short-term borrowing reductions have not really played out. Hence, NIMs have not improved; rather, they have declined. And expenses have also increased in intensity:

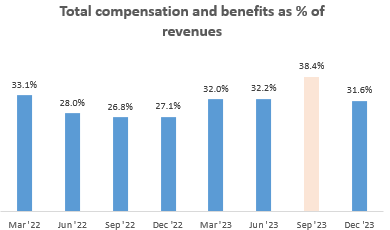

Total compensation and benefits as % of revenues (Company Filings, Hunting Alpha Analysis)

Total compensation and benefits typically make up more than half of overall operating expenses below the net revenues line. These figures spiked up in Q3 FY23 and the drop in Q4 FY23 to 31.6% is not enough to compensate and lead to an overall fall from Q2 FY23 levels (the quarter which influenced by bullish view).

Hence, my expectations on margin expansion have been a miss on all fronts.

Key metrics still need to indicate signs of revenue profile improvement

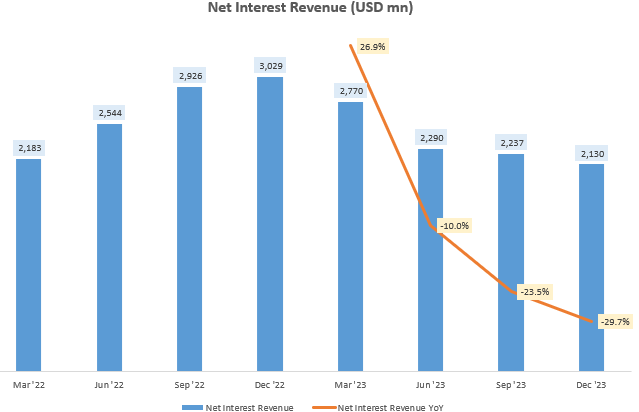

The bulk of Charles Schwab’s revenue woes come from a degrading net interest revenues:

Net Interest Revenue (Company Filings, Hunting Alpha Analysis)

This is driven mostly by the company’s utilization of higher cost funding sources:

Our current revenue and earnings are being pressured of course, by our utilization of the higher cost funding in the form of CDs and FHLB advances. Those are very much a temporary funding source.

– CFO Peter Crawford in the Q4 FY23 earnings call

CD stands for Certificate of Deposit and FHLB refers to Federal Home Loan Bank

These funding sources are more expensive. For example, Charles Schwab’s CDs carry a weighted-average interest rate of 5.06% and the FHLB borrowings incur a 5.28% interest cost. This is much higher than the 1.7% average cost of interest-incurring liabilities. In 2023, reliance on these supplemental funding sources has increased:

Total Schwab Bank CDs (USD mn) (Company Filings, Hunting Alpha Analysis) Federal Home Loan Bank Borrowings Balance (USD mn) (Company Filings, Hunting Alpha Analysis)

Charles Schwab has had to rely on these alternative funding sources because its funding from customers’ cash balances in transactional accounts reduced by 30%. Looking at the client cash as a % of client assets figure, it is clear that there is no meaningful improvement yet:

Client Cash as % of Client Assets (Company Filings, Hunting Alpha Analysis)

Management has been providing reassuring narratives about reduced supplemental funding pressures. However, I believe the market is waiting for proof of execution on management’s plan to reduce reliance on the more expensive funding sources. This would put the company back on-track to hit its net interest margin targets of 3%, aided by relatively higher interest rates. Currently, they are almost 110bps behind target:

Net Interest Margin (Company Filings, Hunting Alpha Analysis)

Discounted valuations make a ‘Sell’ less compelling

I believe my bearish view in mid-January 2024 played out and generated alpha because in bullish market conditions, Charles Schwab’s problems make it lag too far behind other companies that are witnessing a golden period of growth, with broad-based bullish commentary. Microsoft (MSFT) is a prime example that comes to mind.

However, as my ‘Sell’ view played out, I recognize that the valuations have become more discounted:

1-yr fwd PE (Capital IQ, Hunting Alpha Analysis)

Currently, the 1-yr fwd PE for Charles Schwab stands at 18.2x; a 15.6% discount to the 10-yr median multiple of 21.6x. I believe this reduces the margin of safety for bearish views. Hence, I am inclined to hold a neutral stance on the stock.

Technical Analysis

If this is your first time reading a Hunting Alpha article using Technical Analysis, you may want to read this post, which explains how and why I read the charts the way I do, utilizing principles of Flow, Location and Trap.

SCHW Relative Technical Analysis (TradingView, Hunting Alpha Analysis)

In the relative chart of SCHW/SPX500, the ratio prices are currently in a consolidation phase following a sharp move down in early 2023. I anticipate this market state to continue until the key fundamental drivers show signs of consistent improvement. When this happens, I believe SCHW would be ready to begin a sustained alpha-expansion move vs. the S&P 500.

Key Monitorables

Charles Schwab discloses many of the key metrics mentioned above on a monthly basis. The 2 main ones I will be monitoring would be client cash levels and Total Schwab Bank CDs, as this would give a good picture of the additional funding requirements situation; which I believe is the single-most important driver of the stock right now.

Takeaway

My earlier bullish stance in Charles Schwab did not work out; however, the negative alpha here was more than compensated by my ‘Sell’ view in January 2024, as communicated via my last article’s pinned comment (see below article). But due to more discounted valuations, I am revising my stance to a ‘Neutral/Hold’.

From a fundamentals perspective, Charles Schwab has had weak revenue growth and its problems continue as it is reliant on more expensive sources of funding to make up for reduced clients’ transactional cash balances, which is a significantly cheaper source of funding for the bank. I believe the market is still waiting for evidence of reduced reliance on these more expensive funding sources, as the stock is currently in a consolidation phase relative to the S&P 500. Hence, I too remain on the sidelines as I wait for signs of a gradual step-down in the supplemental funding sources. This would be a key driver in helping the company achieve its 3% net interest margin, thereby improving the revenue and margin trajectory as well.

Rating: Neutral/Hold

How to interpret Hunting Alpha’s ratings:

Strong Buy: Expect the company to outperform the S&P 500 on a total shareholder return basis, with higher than usual confidence

Buy: Expect the company to outperform the S&P 500 on a total shareholder return basis

Neutral/hold: Expect the company to perform in line with the S&P 500 on a total shareholder return basis

Sell: Expect the company to underperform the S&P 500 on a total shareholder return basis

Strong Sell: Expect the company to underperform the S&P 500 on a total shareholder return basis, with higher than usual confidence

The typical time-horizon for my views is multiple quarters to around a year. It is not set in stone. However, I will share updates on my changes in stance in a pinned comment to this article and may also publish a new article discussing the reasons for the change in view.

Q2 2024 Earnings Call Transcript")