Kindamorphic/iStock via Getty Images

GigaCloud Technology (NASDAQ:GCT) is a fast-growing company at a reasonable valuation. However, there is a lot of controversy surrounding the stock, and it should see some near-term headwinds the next few quarters.

Company Profile

GCT is a logistics and business-to-business (“B2B”) marketplace operator for large parcel products, such as furniture and fitness equipment. Its B2B platform connects buyers in the U.S., Europe, and Asia with Asian manufacturers, and it will transport products from a manufacturer’s warehouse to end customers.

The company’s revenue comes through three primary sources. Its GigaCloud 3P revenue comes from service revenue for such things as warehouse services, last mile delivery, ocean transport services, and via transactions through its B2B marketplace. The company also sells its own product inventory through its platform. Finally, it also generates off-platform e-commerce revenue through the sale of its inventory on third-party websites.

At the end of Q3, the company had 31 warehouses in five countries, including the U.S., Japan, Germany, U.K. and Canada.

The company was formerly known as Oriental Standard Human Resources Holdings Limited, and it went public in the U.S. in August of 2022.

Opportunities & Risks

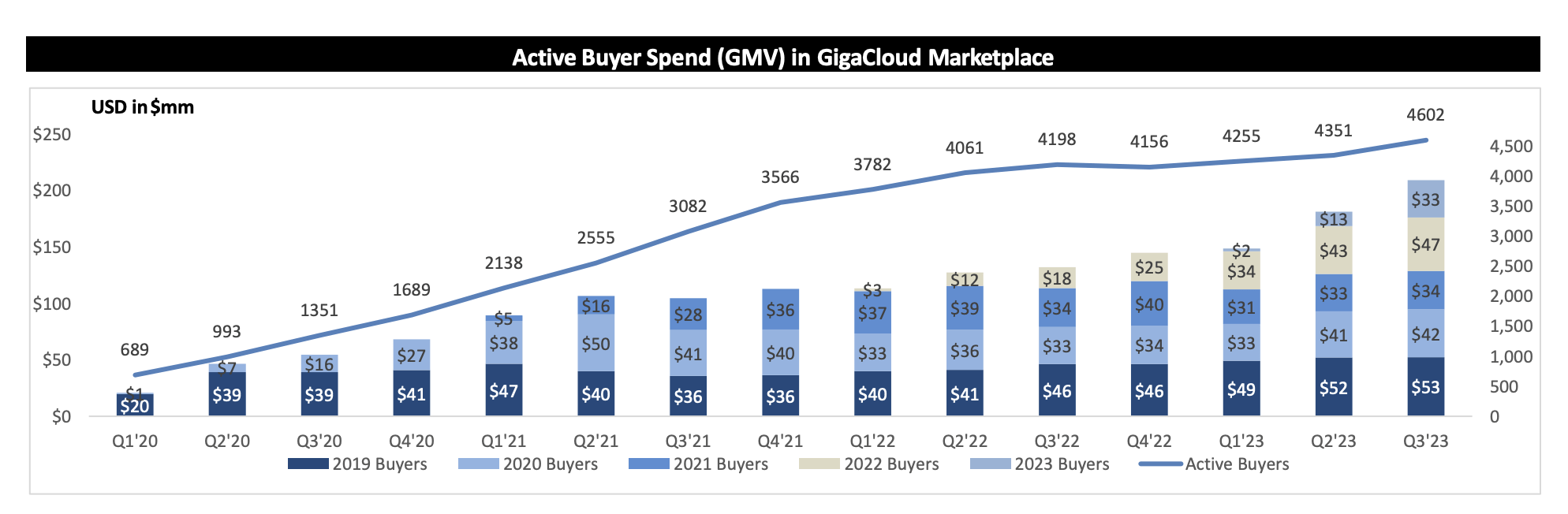

GCT has been growing rapidly, propelled by adding more buyers to its platform and buyers spending more money over time. Last quarter, the company added nearly 10% more buyers year over year to 4,602 from 4,198 a year ago. The company says that most of its new buyers come from referrals or word of mouth, keeping customer acquisition costs low.

Meanwhile, active buyer cohorts spend more money over time. For example, active buyers from its 2019 cohort spent $39 million in Q3 2020, while in Q3 2023 they spent $53 million. Spend per active buyer has gone from $112,777 in 2020 to a projected $149,000 in 2023.

Company Presentation

Fueling the company’s strong growth among its cohorts is its supplier fulfilled retailing model. This model reduces the number of touch points in fulfilling orders when retailers often must make arrangements for last mile delivery themselves, while GCT handles the entire process, from the manufacturer to the ocean transport, to the products’ last mile delivery to the end user. This reduces overall transport costs, which leads to higher margins for buyers and sellers.

In addition, GCT has started to get into other large merchandise categories. It originally focused on furniture, but has since added home appliances, home fitness equipment, and gardening. The company sees future opportunities in auto accessories, seasonal décor, and pet supplies. Furniture represents its biggest category by far, so these other areas have a lot of potential runway.

GCT is also looking to expand its presence with retailers through two recent acquisitions. After the quarter, the company acquired the assets of B2B furniture distributor Noble House from bankruptcy, as well as digital signage and electronic catalog management Wondersign. Noble House had relationships with top retailers including Amazon (AMZN), Target (TGT), Wayfair (W), Lowe’s (LOW), Beyond (BYON), and Walmart (WMT) that GCT will look to leverage selling its goods on. Meanwhile, with Wondersign, the company is looking to use its technology to be able to process e-commerce drop ship transactions in physical stores.

Overall, GCT has been seeing strong growth. Revenue jumped 39.2% in Q3 to $178.2 million. Product revenue rose 45% to $178.2 million, while service revenue grew 27% to $40.5 million. Adjusted EBITDA , meanwhile, surged 150.4% to $29.8 million.

When it comes to risks, being tied to the furniture industry is a big one. This has been one of the worst performing categories coming out of the recession due to the lack of movement in the housing industry. This is by far GCT biggest category, and it is getting over 75% of its revenue from first party sales. Industrywide furniture and home furnishing sales were down –7.3% in November and -4.7% in December.

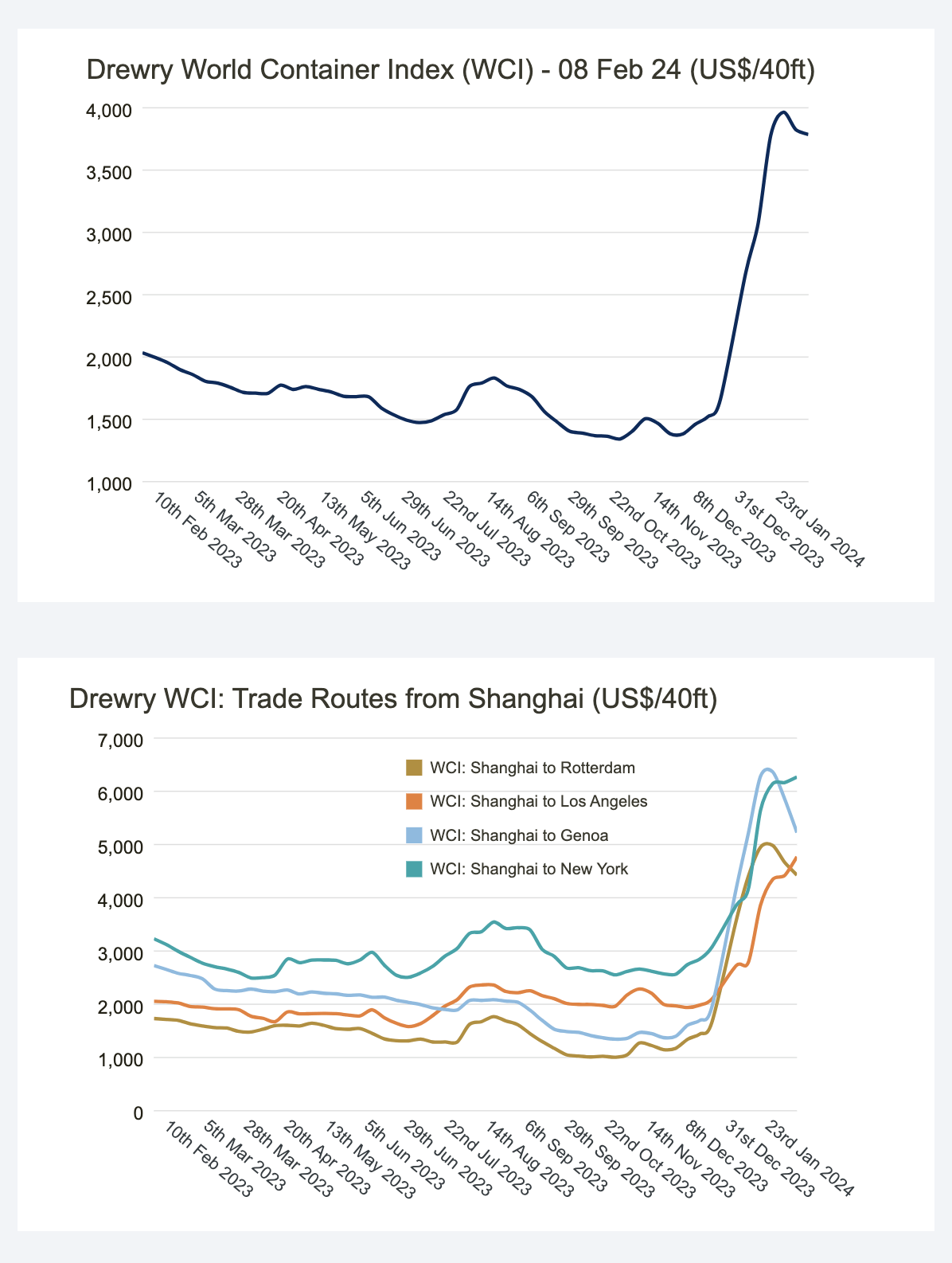

Ocean freight rates is another risk. GCT had been getting a boost to its gross margins the last few quarters as ocean freight rates had come down from pandemic highs to more normal level. However, a combination of issues with the Panama Canal and, in particular, ships being diverted from the Red Sea due to Yemeni Houthis rebels attacking shipping vessels has seen containership prices skyrocket. Shipping rates from China to the U.S. have continued to stay elevated.

Drewry

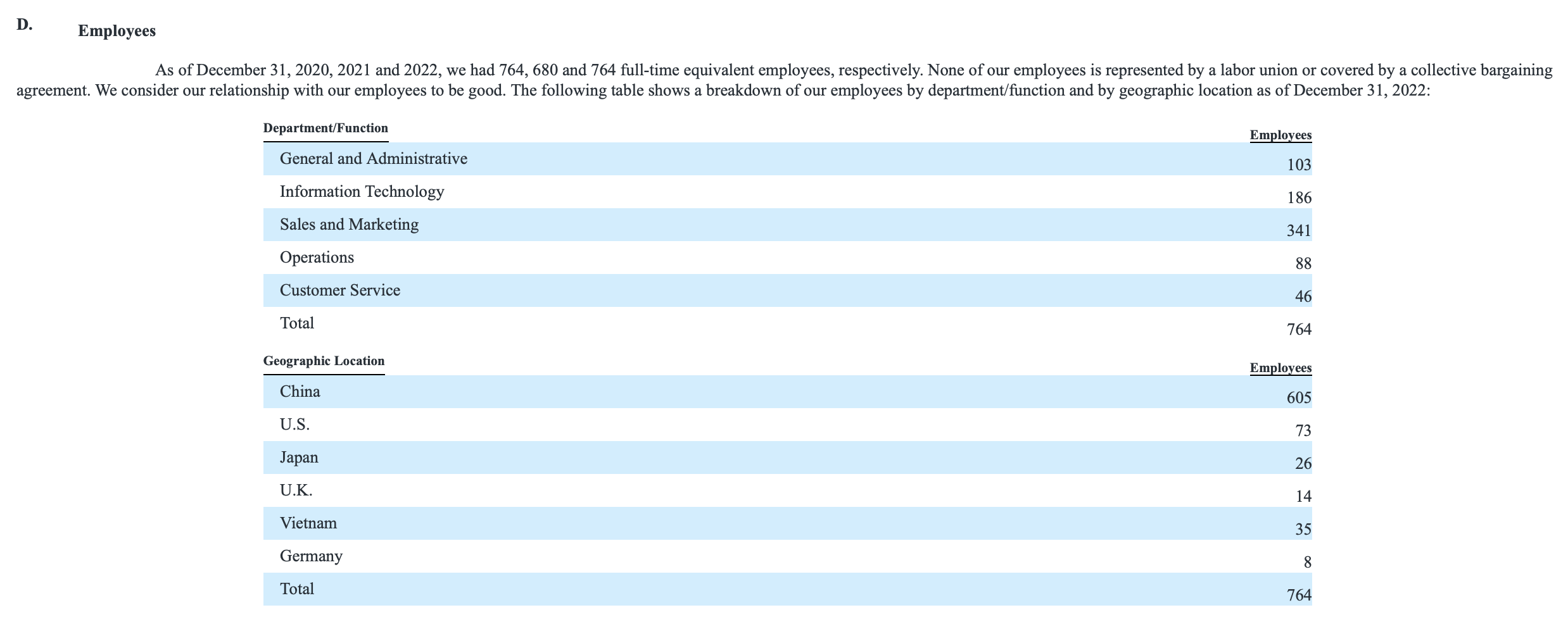

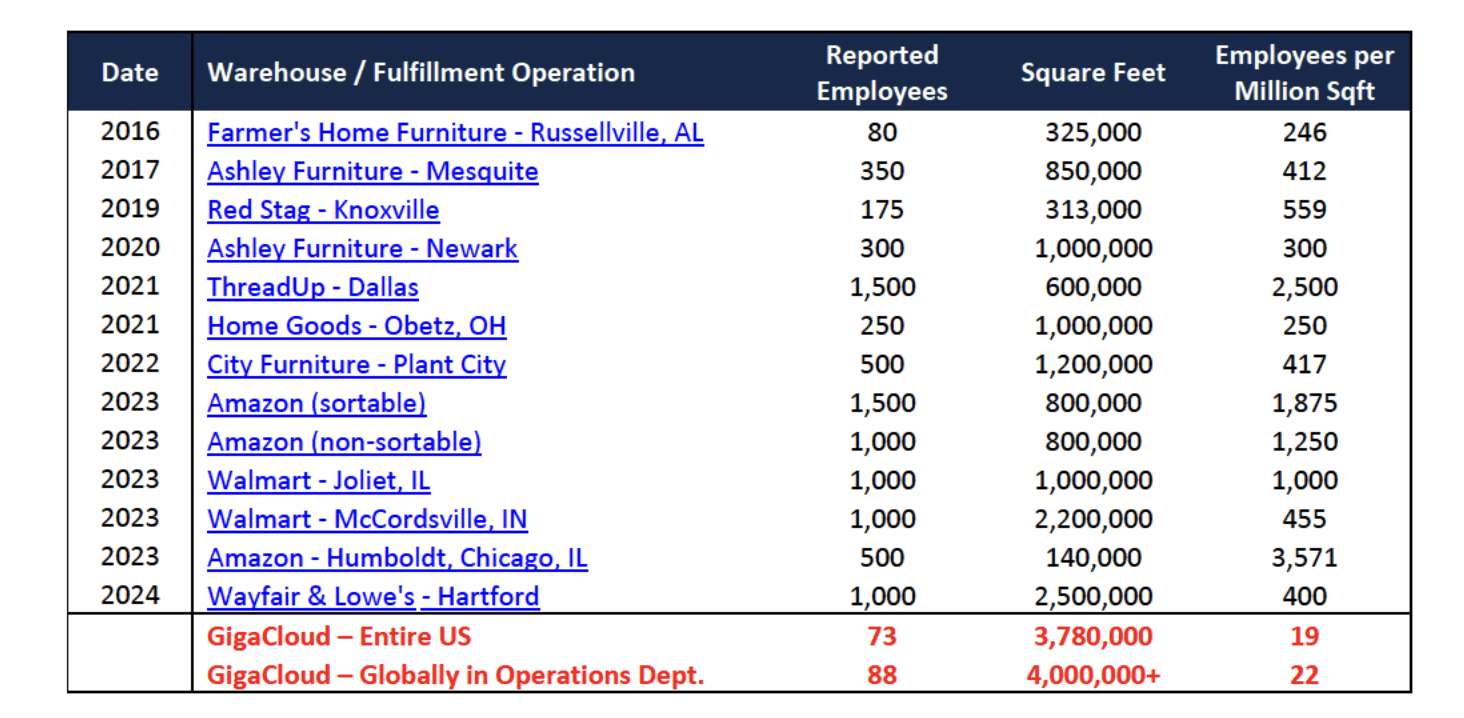

GCT has also been the subject of a scathing short report by Culper Research. The report contains some very intriguing detective work, although unless you are going to spend time sitting outside GCT’s warehouses, it is difficult to verify. However, one interesting fact the firm brings up is GCT’s lack of warehouse employees. Culper notes that GCT only has 73 employees for its 14 U.S. warehouses, which the puts in its last annual report last April. That just doesn’t seem to make any sense whatsoever, especially when not all its U.S. employees are warehouse employees, given that it has an HQ in California. The company’s replies to the short report, meanwhile, have been very generic.

GCT Employees (Company 20-F)

Warehouse Employees (Culver Research)

Valuation

GCT stock currently trades at 10.6x the 2024 consensus EBITDA of $119.9 million and 7.8x the 2025 consensus of $162.5 million.

It trades at a forward P/E of 13x the 2024 consensus of $2.42 and 10.4x the 2025 consensus of $3.00.

Revenue growth is expected to be 32.4% this year, and then grow 31.5% in 2025.

Given its growth rate, GCT could easily be valued at double where it trades today. That’s if you believe its numbers are accurate.

Conclusion

If you think GCT is legitimately going to grow revenue over 30% per year over the next few years, the stock is a clear “Buy” at current valuations. The company has said it will look to shore up its filings in 2024 with regular 10-Qs and 10-Ks, the same as a domestic filer, so there could be more transparency, which could lead to upside.

However, if you have concerns about the legitimacy of the company, then I’d stay away. After all, this is a company with a technology-sounding name that in reality is selling and fulfilling orders for Asian furniture with very few warehouse employees and little spending on sales & marketing (6% of revenue) in a terrible market for home furniture sales. One of its big plans to drive growth, meanwhile, is coming from the assets of a company it bought out of bankruptcy. Anecdotally, GTC’s B2B marketplace website is pretty basic and very slow, so it’s not exactly cutting edge.

GCT’s stock has absolutely crushed any shorts since the Culper Research report. That doesn’t prove its finding are wrong (or right for that matter). However, it does show the risk of being short an optically cheap name that on the surface is growing quickly.

Overall, I’d stay far away from the stock. At the very least, it should feel gross margin pressure from the rise in containership prices. As such, I rate the stock a “Sell.”

Q2 2024 Earnings Call Transcript")