Bloomberg/Bloomberg via Getty Images

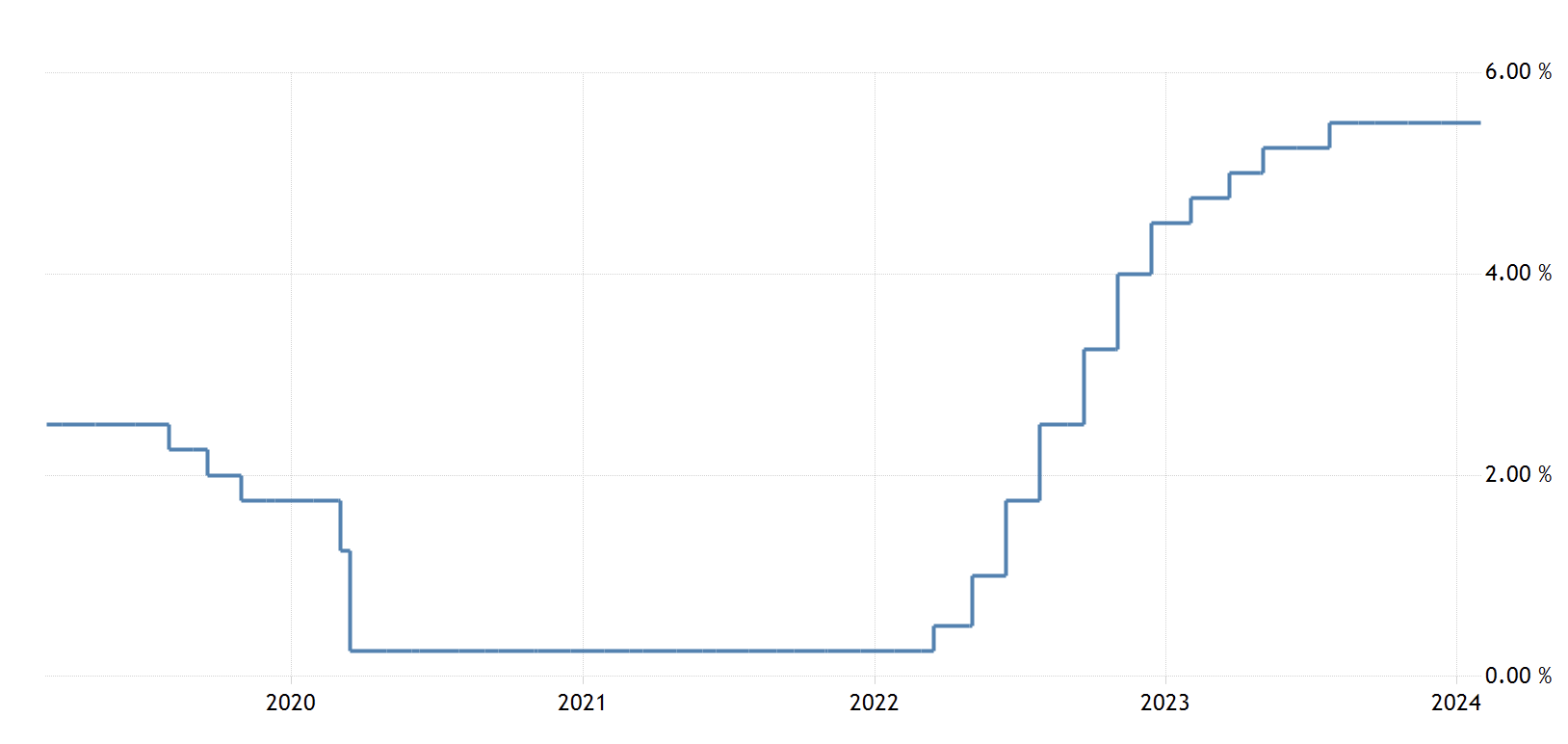

Today, I continue my research among the most compelling dividend companies with another dividend king: Colgate-Palmolive (NYSE:CL). The Federal Reserve’s decision to raise interest rates in the last couple of years has prompted many investors to favor risk-free rate bonds over stock dividends. As rates have approached a stationary level and are expected to commence a decrease in the second half of 2024, I believe it is the right time to consider buying dividend-oriented companies. Incorporating stalwarts like Colgate-Palmolive and many other robust companies in our portfolios should give investors a good balance between income generation and the potential for capital appreciation over time.

Interest rates evolution in the US (tradingeconomics.com)

I will start discussing the company’s business and financial data, reflect on the opportunity given by the interest rate decrease, analyze risk factors in my investment thesis, and finally conclude with a valuation.

Company’s business overview

Today Colgate-Palmolive is a massive conglomerate encompassing different brands available in more than 200 countries around the globe. It produces and distributes a vast variety of household products for everyday use that can be split into four different parts:

- Oral Care: Colgate is recognized for its oral care products, including toothpaste, toothbrushes, mouthwash, and dental floss.

- Personal Care: The company offers personal care products such as soaps, shower gels, deodorants, and shampoos under various brand names like Palmolive, Sanex, or Protex.

- Home Care: Colgate-Palmolive produces household cleaning products, including dishwashing liquids and detergents marketed through various brands like Ajax, Palmolive, and Fabuloso.

- Pet Nutrition: The company has a segment dedicated to pet nutrition, offering pet food products under Hill’s brand.

This strategic diversification allows Colgate to serve a wide range of customer needs solidifying its position as a leading provider of household products on a global scale.

Colgate-Palmolive Brand Portfolio (Company’s presentation)

The company’s sales strategy revolves around two fundamental pillars: communication and innovation. During the last fiscal year, the company increased its advertising investment by 19% witnessing a corresponding rise in ROI. As discussed during the Q4 2023 conference call the company is expected to further accelerate the advertising into 2024. Moreover, managers are focused on product innovation and R&D to enhance customer loyalty and brand strength.

Brand strength and customer fidelity become evident in the company’s significant pricing power. Over the last two years, during periods of inflation, Colgate-Palmolive was able to raise prices to offset rising cost pressure. Considering the essential nature of the products sold and its pricing power, I consider the company to be non-cyclical, able to navigate through economic cycles without worrying about consumer spending.

While the personal care market is expected to grow at a 3.33% CAGR until 2029, the pet food market is going to grow at a slightly higher pace, around 5.5% globally. These figures are in line with the company’s long-term sales growth target range of 3% to 5% as emphasized in the last conference call. Considering the investments in advertising and its pricing power I expect it to be able to grow at the higher level of the range.

Financial data overview

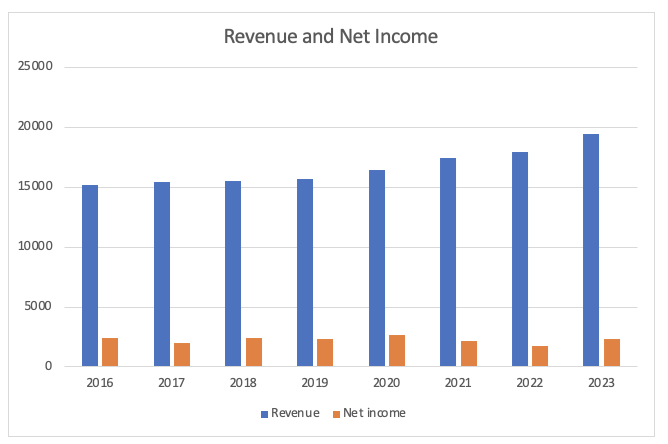

Since 2016 the company was able to increase its revenue at a 3.14% compound annual growth rate while net income slightly decreased in the same period.

Revenue and Net income results (Author’s calculation)

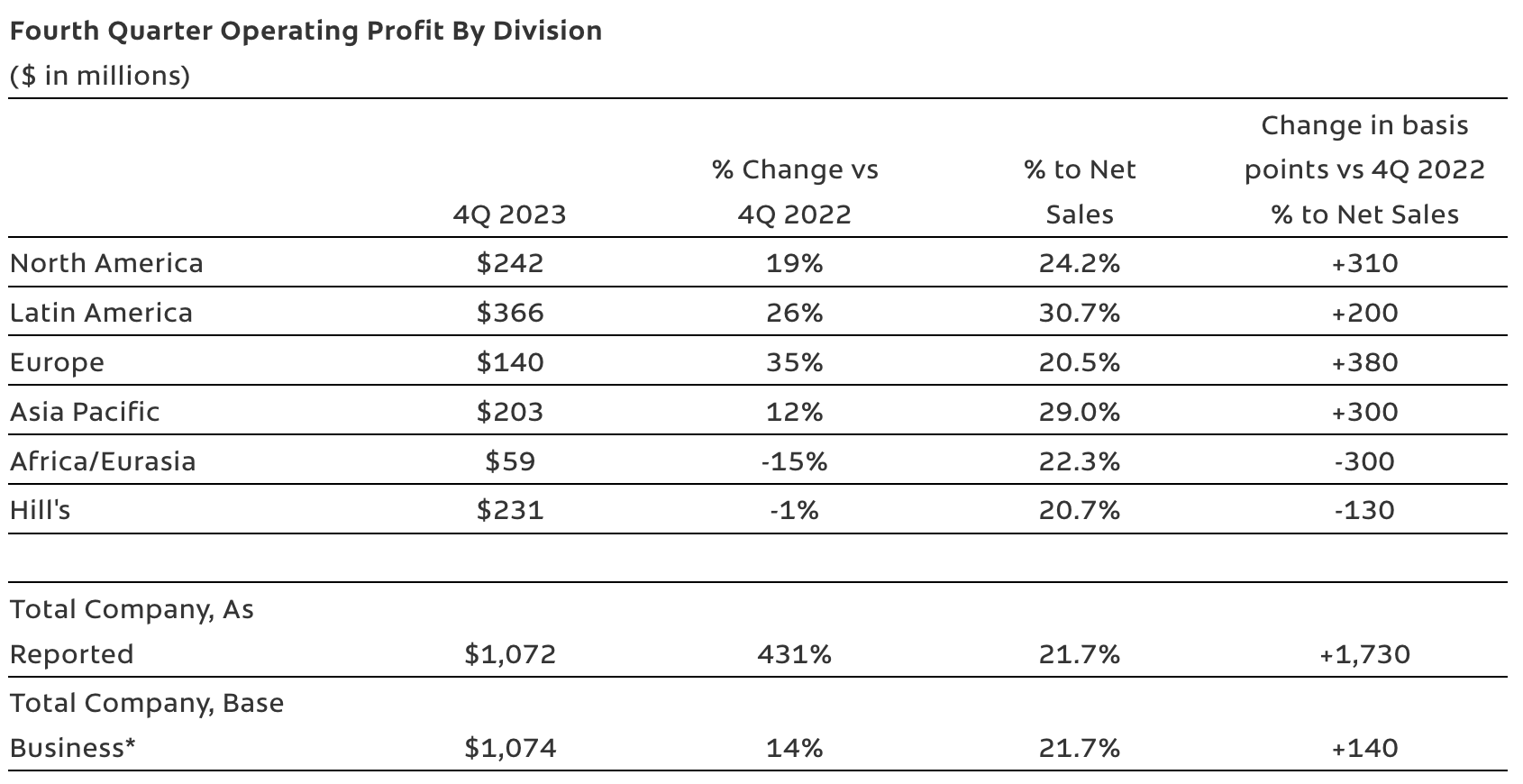

Considering Q4 2023 data, the company exhibits a well-distributed revenue across the world with the smallest market represented by Africa/Eurasia which accounts for only 5% of total revenue. In the long run, as these regions are going to develop, I expect the company to invest more aggressively to expand further its presence in these areas.

Q4 2023 operating profit breakdown (Company’s press release)

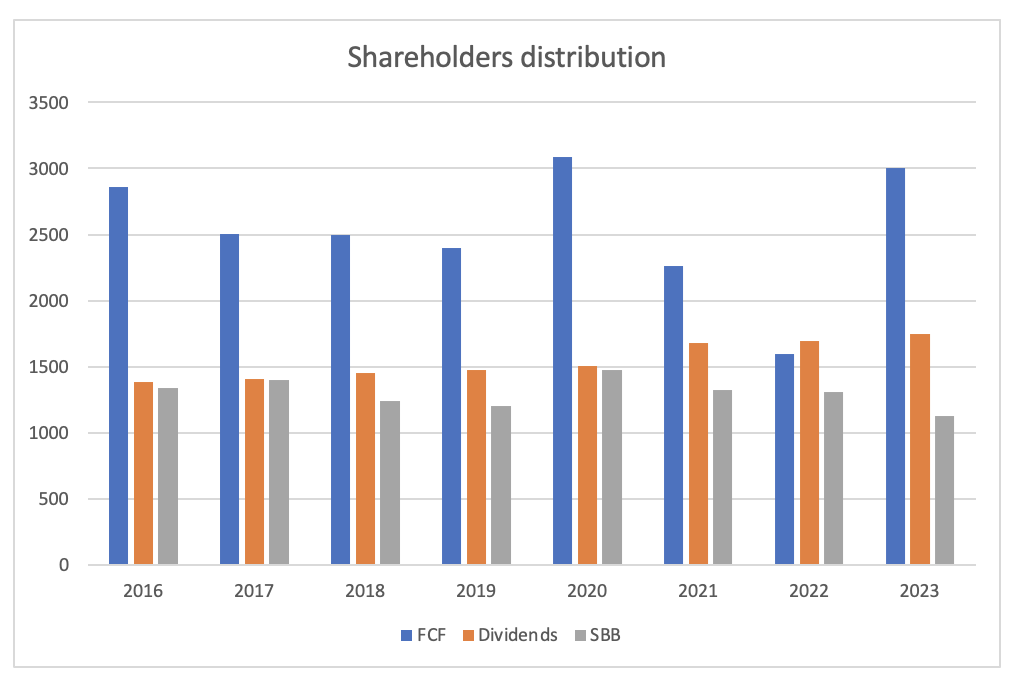

Free cash flow grew at a 0.6% CAGR and the company is mainly focused on rewarding shareholders through dividends and share buyback. Since 2016 the company repurchased around $10.5 billion shares for a total of 46.6 million shares and paid more than $12 billion in dividends.

Distribution to shareholders and FCF (Author’s calculation)

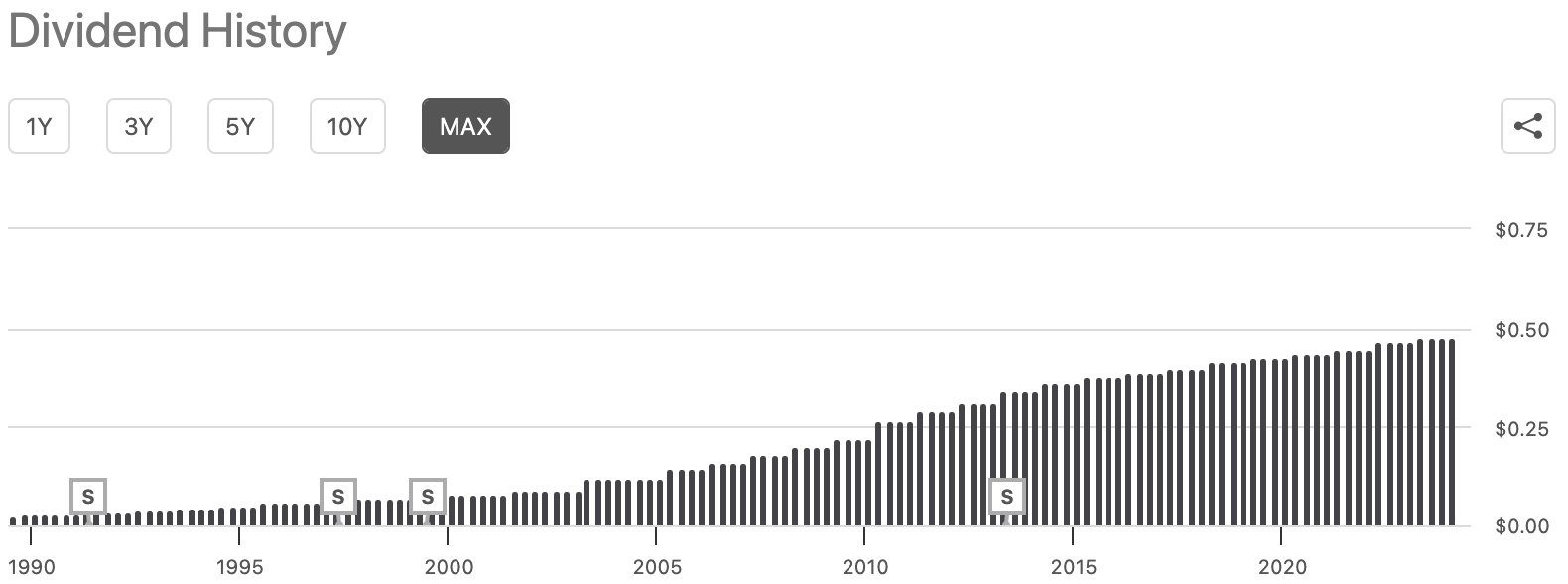

Colgate is a dividend king currently paying a good 2.3% in dividends with 60 consecutive years of dividend growth. Since 1989 the company paid $52.2 per share in dividends, which is a 1757.6% dividend return and 2870% in stock price appreciation. The last dividend increase last year was around 2.1%, which means that the management team feels confident about the future ahead.

Dividend history (Seeking Alpha)

Even though some investors are worried about the debt outstanding, I am not. The company is gradually paying it as we can see from the decrease in total debt that passed from $9.3 billion in fiscal year 2022 to $8.5 billion in 2023. In the same period, the cash per share passed from $0.93 to $1.17, one of the highest levels ever reached by the company. In contrast with these results, the inventory, which slightly decreased since 2022, is still at its highest. I would like to see a clear inversion in this trend in the future to squeeze the net working capital and increase the company’s overall financial performance.

The catalyst given by interest rates decrease

I am a fan of Warren Buffett and I believe that one of his most insightful quotes is:

Interest rates are to asset prices what gravity is to the apple. When there are low-interest rates, there is a very low gravitational pull on asset prices.

Following this reasoning, the investment thesis for Colgate-Palmolive is clear-cut: with the anticipated decrease in interest rates starting in the second half of this year, I anticipate that dividend-oriented companies will become an attractive asset for investors. For example, consider a retiree who has a sum of money aimed at generating a steady stream of income, as soon as interest rates decline, it is likely to see a shift from bonds toward secure stocks like Colgate-Palmolive.

I think CL will be a direct and indirect beneficiary of such a shift in capital allocation. While the 2.3% yield may not be the largest, the company’s dividend track record and commitment to dividend growth should attract new investors. Moreover, as investors seek yields in the stock market, they are also likely to allocate capital toward ETFs that are focused on yield so they can buy a basket of income-producing assets. CL is currently a core holding of more than 250 ETFs with the largest holding represented by Vanguard Total Stock Market ETF (VTI).

Risks

In my opinion, the main risk associated with the company is that, as it is focused on expanding its operations in new areas of the world, it will have to invest a lot of money in new facilities, finally increasing the capital expenditures and resulting in a stagnant free cash flow. This is in line with results reported during the last decade and this trend is likely to continue also in the foreseeable future. I will consider this aspect in my valuation.

Even though the company is non-cyclical, it is not immune to economic slowdowns and geopolitical tensions that may disrupt its supply chain or overall financial performance. This reasoning is in line with what we are witnessing with the current economic slowdown in China and Eurasia due to the Russo-Ukrainian conflict. Such negative situations tend to have a meaningful impact, particularly on the cost of goods sold and the overall cost of revenue, significantly affecting the company’s margins in the short term. This is consistent with the negative result in operating profit in Eurasia and the slowdown in growth in Asia Pacific reported in the financial data paragraph. Despite the negativity affecting China, I still perceive it as a valuable market with a long-term opportunity and I am encouraged to hear the management team expressing alignment with my perspective during the recent conference call. However, as conditions improve in both regions we should expect a continued impact on margins in the short term.

Valuation

Considering that the free cash flow is stable and I expect it to remain stagnant over the next years, I evaluated the stock using a discounted cash flow model.

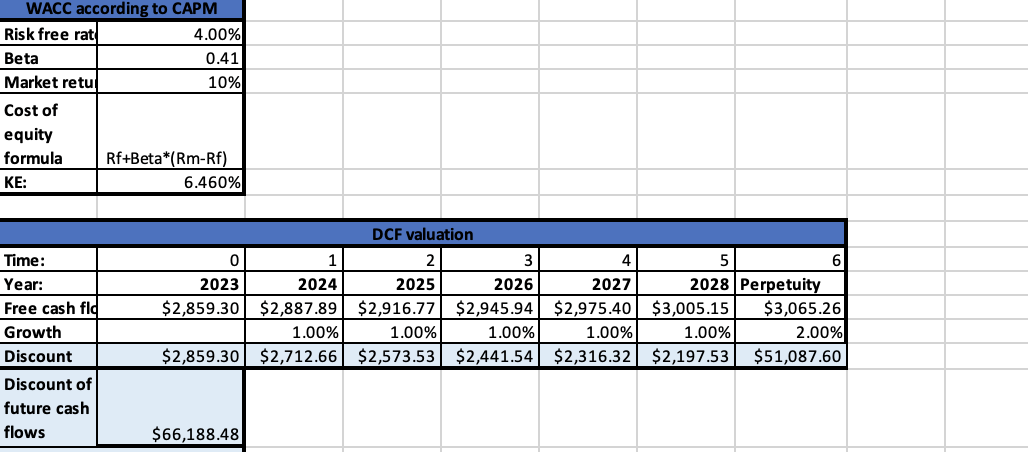

In the upper part of the sheet, I computed the cost of equity that I used as the discount factor. Based on the inputs reported in the picture below I obtained a value of 6.46% for the cost of equity. Aligning with my analysis of catalysts and potential risks in the future, I chose to project the 2023 levered free cash flow with a 1% conservative growth rate until 2028 and a 2% perpetual growth. Finally, I obtained a fair value of $66.188 billion, which is almost in line with the current market capitalization of the company.

Despite the company trading at its fair value, I believe it is a compelling “buy” opportunity because, as stated in my investment thesis, dividend-oriented companies are likely to appreciate in the next 12 months as interest rates start to decline. This strategic alignment, combined with the stability of free cash flow, contributes to the attractiveness of the stock as an investment option.

Valuation (Author’s calculation)

Conclusion

As interest rates will start to decline a lot of people hunting for streams of income will consider investing their money in safe corporations like Colgate-Palmolive that operate in non-cyclical businesses. Despite some concerns about future free cash flow growth, I believe this valuation can be considered safe enough to start building a position in this dividend machine and hold for a long time.

Q2 2024 Earnings Call Transcript")