Andrii Yalanskyi

Kimball Electronics’ (NASDAQ:KE) Q2 Results missed analyst expectations, and the stock has significant risks related to its momentum and revisions at this time. Over the long term, I believe returns from the shares could be quite good. However, the potential for short-term downside is enough to stop me from making an investment.

Operations & Q2 Results Overview

Kimball Electronics provides electronic manufacturing services, including engineering and manufacturing solutions for automotive, medical, industrial, and public safety clients. Its operations include the full product lifecycle, starting at design through to prototype and manufacturing, packaging, and distribution.

Its engineering process includes options for testing and rapid prototyping to create viable products. Additionally, its manufacturing abilities include printed circuit board assemblies (PCBAs) and custom packaging solutions. The firm manages a global supply chain, focusing on efficiency, material availability, and effective delivery.

Kimball’s Q2 2024 financial results showed a YoY 4% decrease in net sales, attributed to global macro headwinds and reduced consumer demand for the period. The firm maintained stable margins despite the challenges through cost structure adjustments. It ended Q2 with $39.9 million in cash and equivalents but $321.8 million in outstanding borrowings. It spent $13.2 million on capex, with total cash flow from operating activities at $30.7 million.

In the Q2 report, the leadership outlined its commitment to navigating the challenging economic environment with a focus on long-term growth, worldwide expansion, and higher customer satisfaction. They also rightly expressed capital management improvements that need to be made, including cash flow adjustments through better receivables and payables protocols.

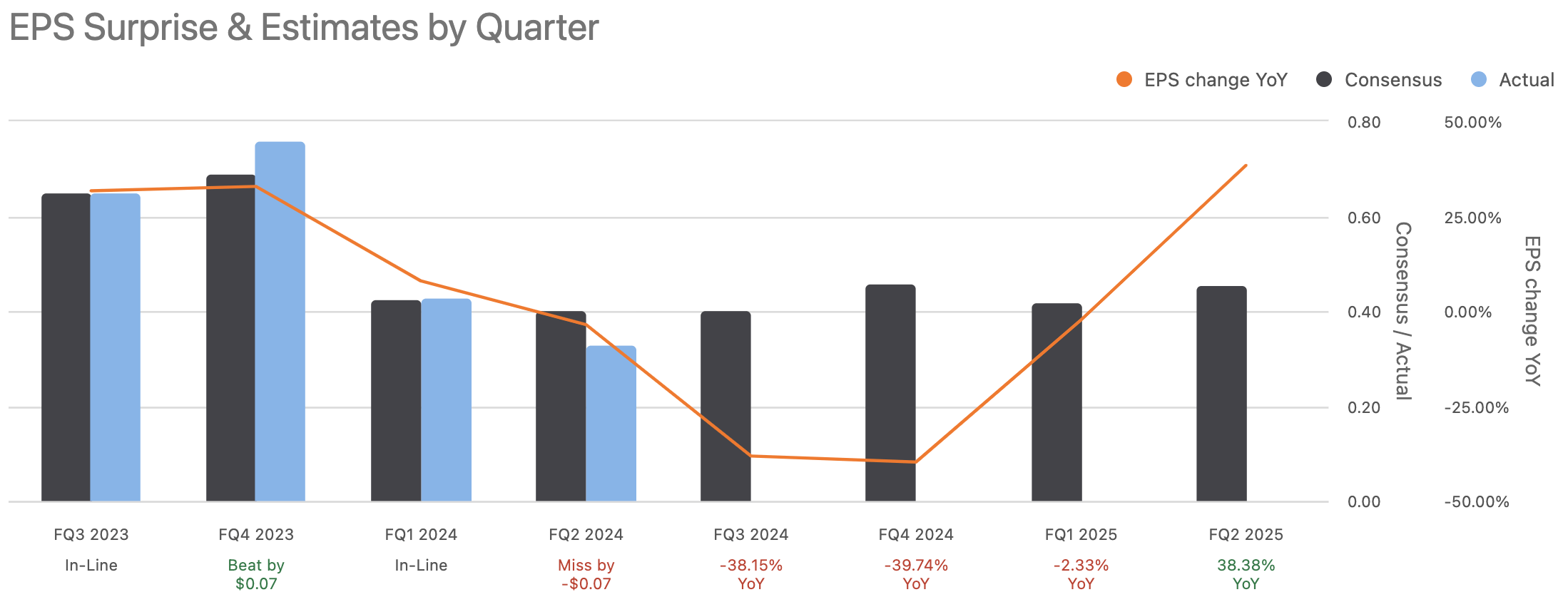

Notably, the Q2 results missed analyst expectations:

Seeking Alpha

Financials

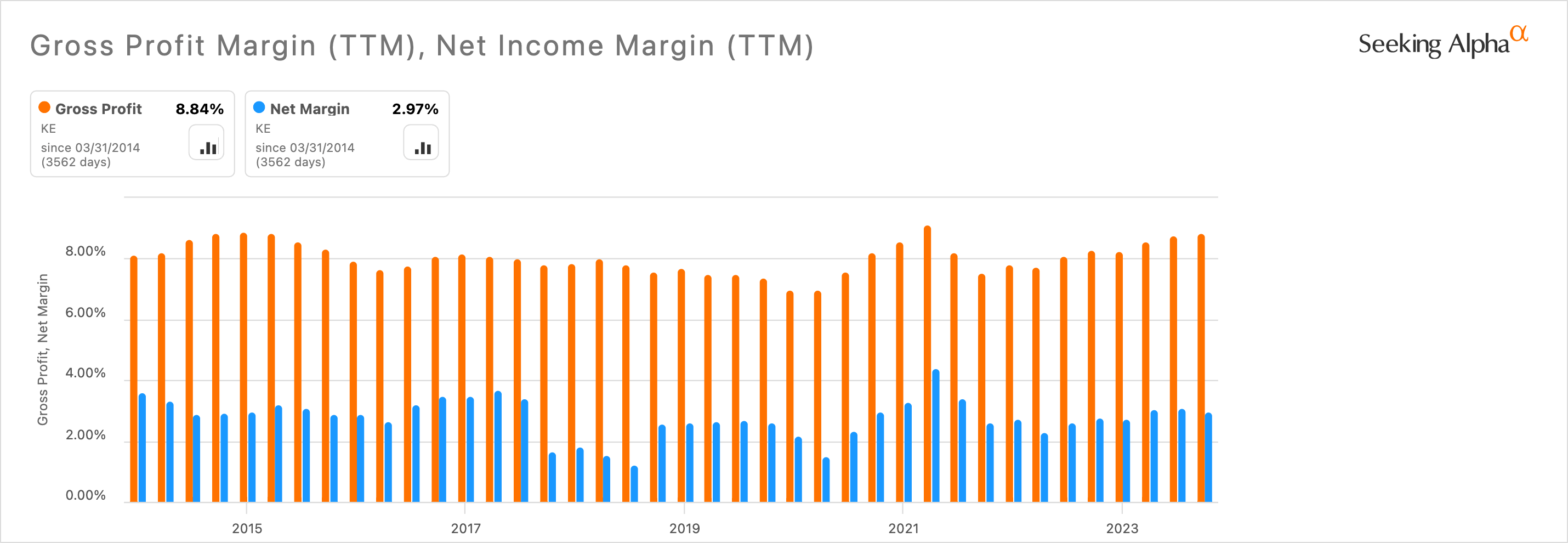

Kimball’s profitability is more average than I would like when considering investing in the stock. Its gross profit margin is the most significantly poor area, at only 8.84%, which is 81.86% lower than the sector median of 48.71%. However, its net income margin of 2.97% is much more promising and is actually 34.92% higher than the sector median of 2.2%. Additionally, the high cost of goods sold that is frequent for Kimball based on its past reports, doesn’t mean this is necessarily a weakness when considered alongside its total net profitability. Of course, the company could aim to improve its gross margin to then bring up its bottom line. However, high costs seem to be a normal part of business for the firm, and I am more focused on its net income competitively.

Author, Using Seeking Alpha

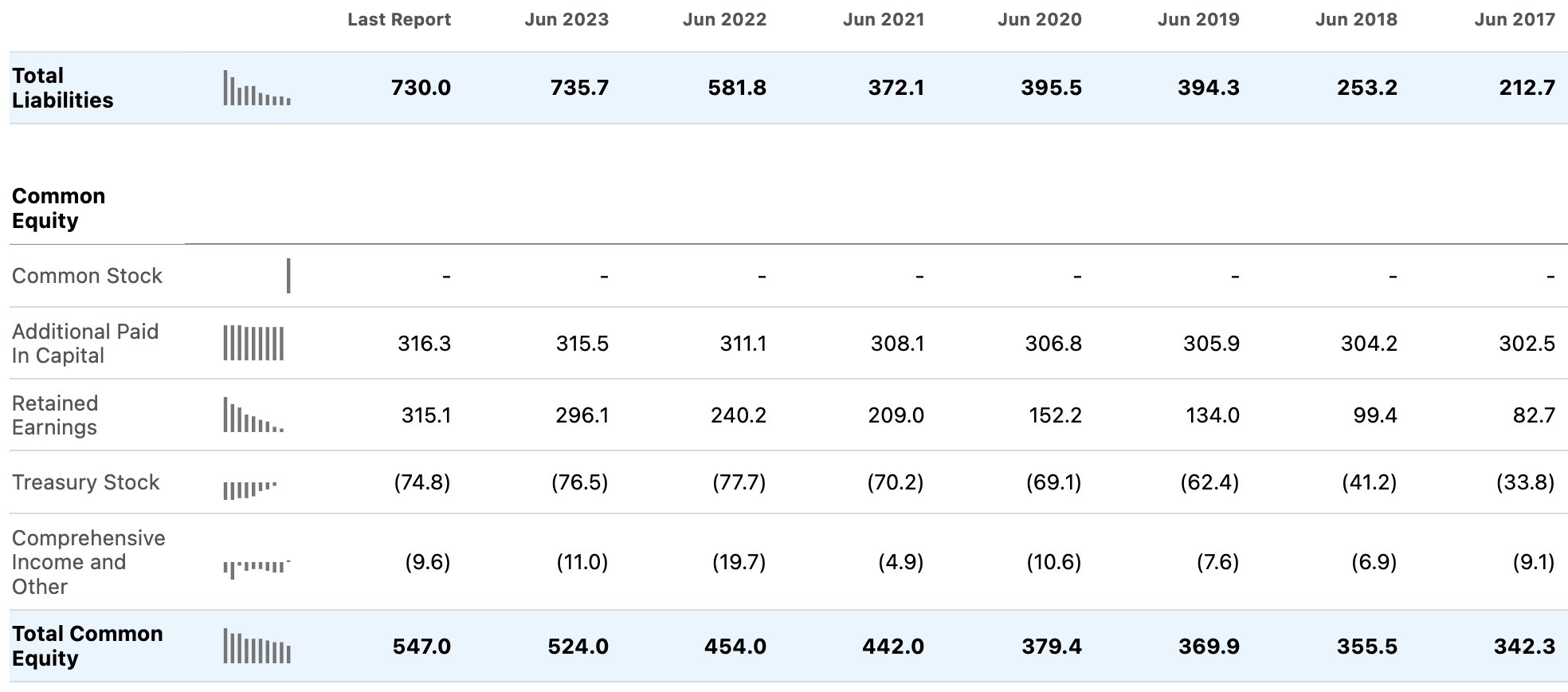

The company’s balance sheet could be a lot stronger, and its equity-to-asset ratio is only 0.43. That is worse than usual for the organization, considering it has a median ratio of 0.54 over the last 10 years.

Seeking Alpha

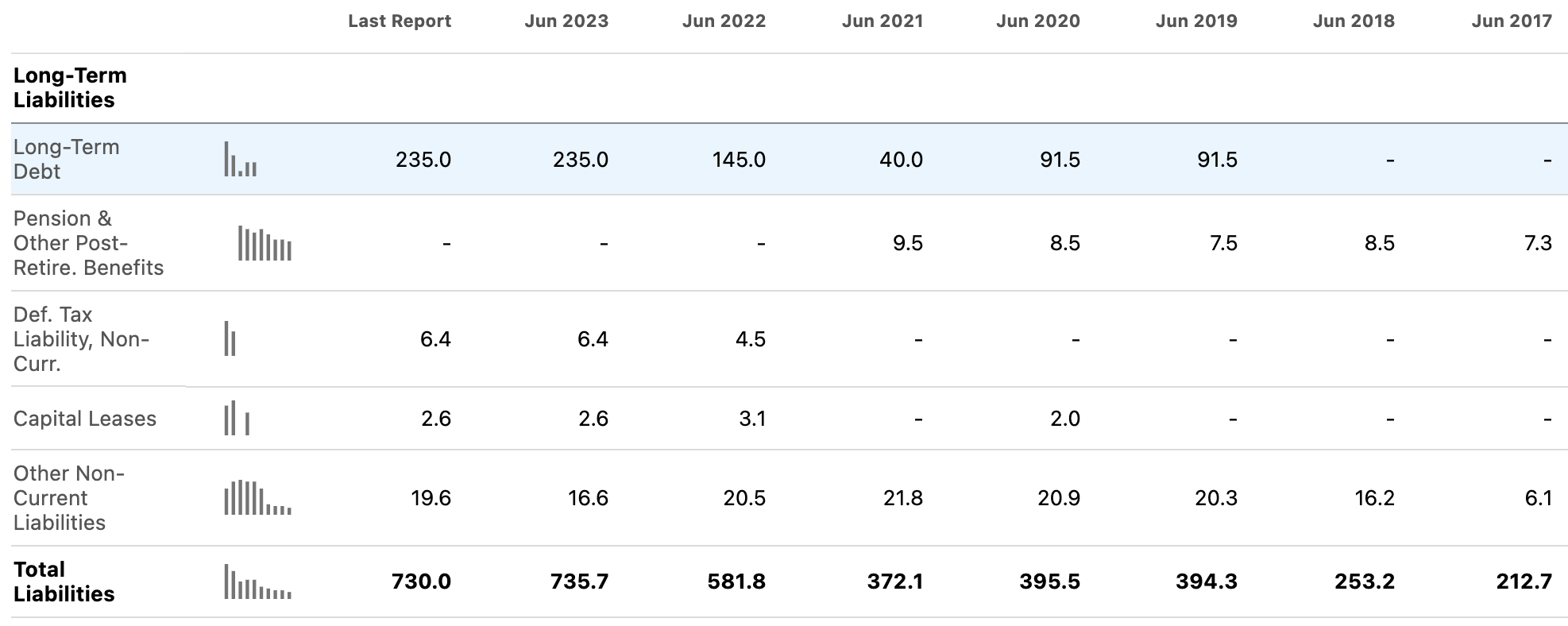

A large contributor to its total liabilities is its long-term debt, which has risen significantly over the last five years:

Seeking Alpha

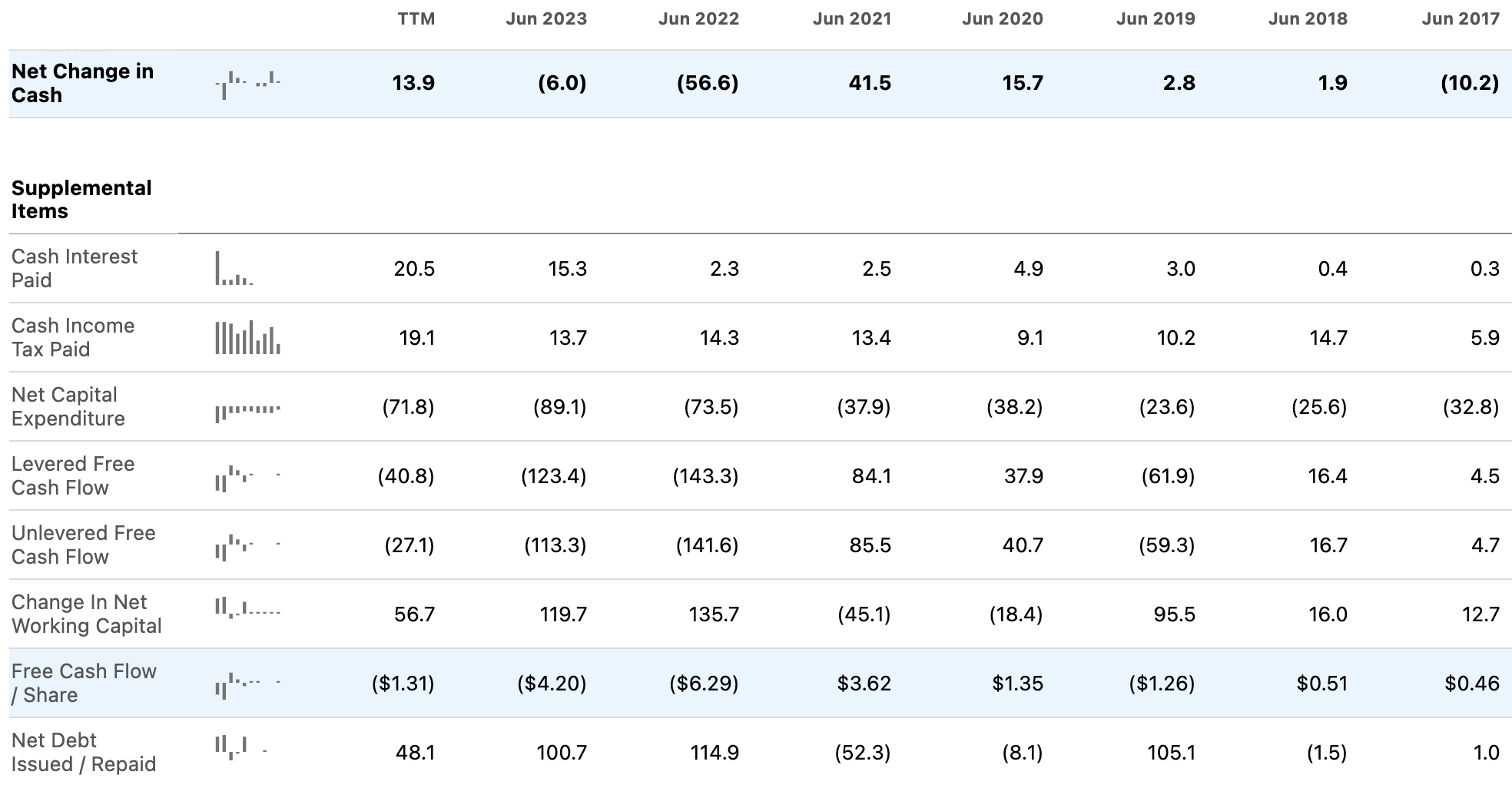

Also, while the company has a positive TTM net change in cash as opposed to its 2023 and 2022 reports, its free cash flow per share at this time is negative and has been since the 2022 report:

Seeking Alpha

KE’s growth is stronger, with 10-year revenue growth of 9.66% per year on average and diluted EPS growth of 8.95% per year on average over the same time frame. Its future growth will be largely driven by market growth in medical and automotive, advanced technology, including automation and AI, and customization in electrical products. As such, the organization is well-positioned to capitalize on these growing trends.

Valuation

Kimball Electronics has a very strong valuation at the moment, with a forward P/E GAAP ratio of 13.17, which is 52.97% lower than the sector median of 28. Its five-year TTM P/E GAAP ratio average is 13.91, 29.07% lower than the sector’s five-year average median.

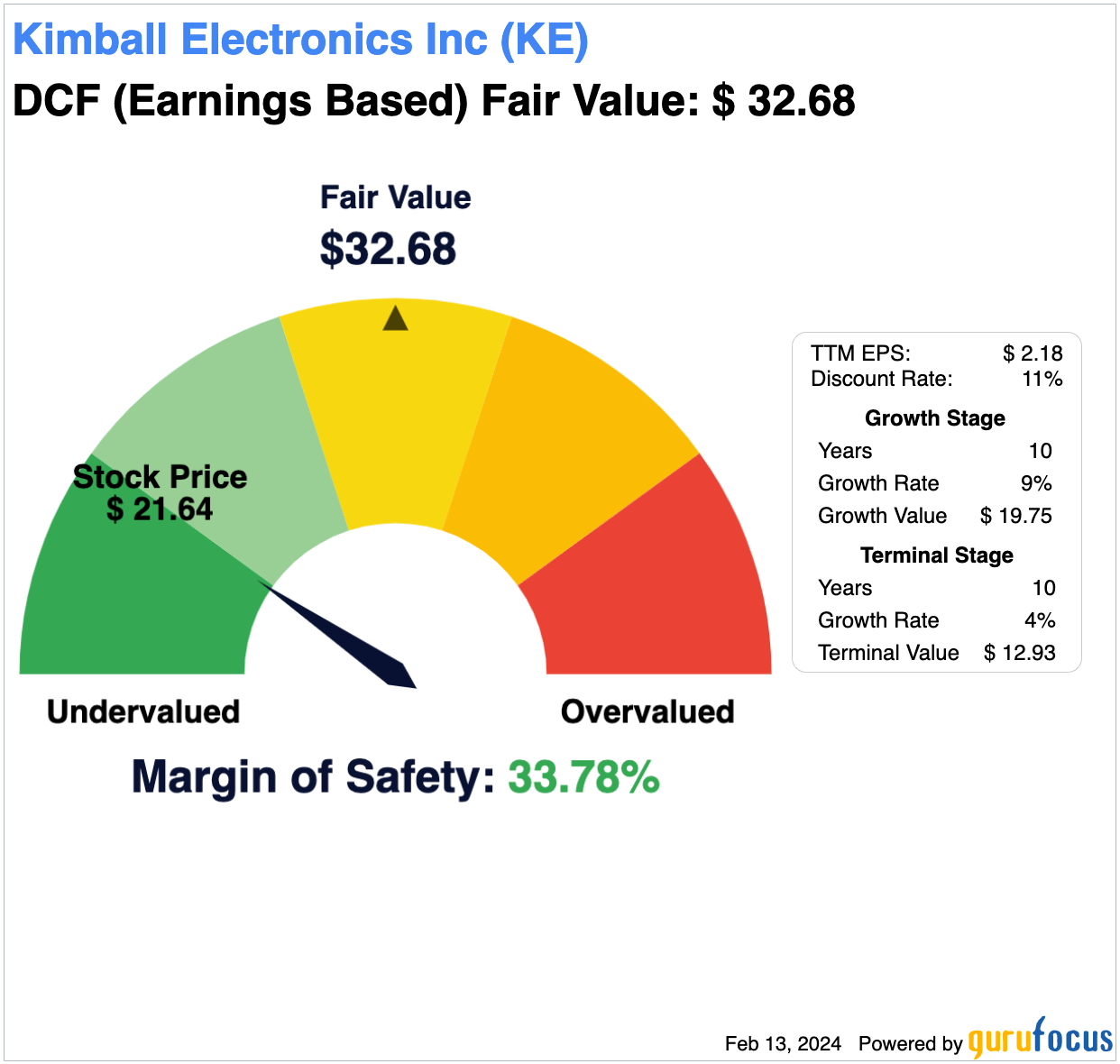

Based on my discounted cash flow analysis, the stock could be 34% undervalued if I consider the potential that the company can maintain 9% EPS growth over the next 10 years as an annual average. I used a terminal stage growth rate of 4% and a discount rate of 11%:

Author, Using GuruFocus

Momentum & Revision Risks

The greatest risks, as outlined by Seeking Alpha’s Quant, and the reason the system allocates a Strong Sell rating to it, are its low performance in momentum and revisions. Therefore, I will discuss the weaknesses present at this time, which I believe do significantly detract from an otherwise appealing stock.

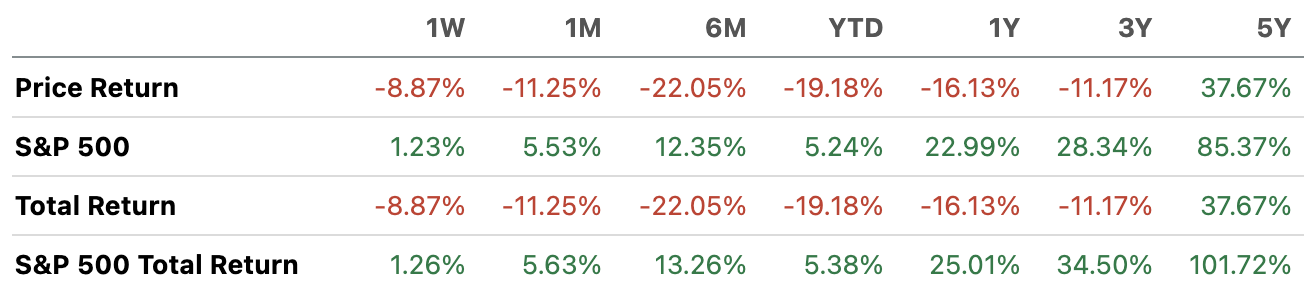

KE has a 6M price performance of -23.84%, which is very poor considering the sector median is 6.13%. Now, notably, its 5Y average is 7.47%, which significantly improves its long-term outlook and means that its present results could be temporary. KE has underperformed the S&P 500 significantly over five years:

Seeking Alpha

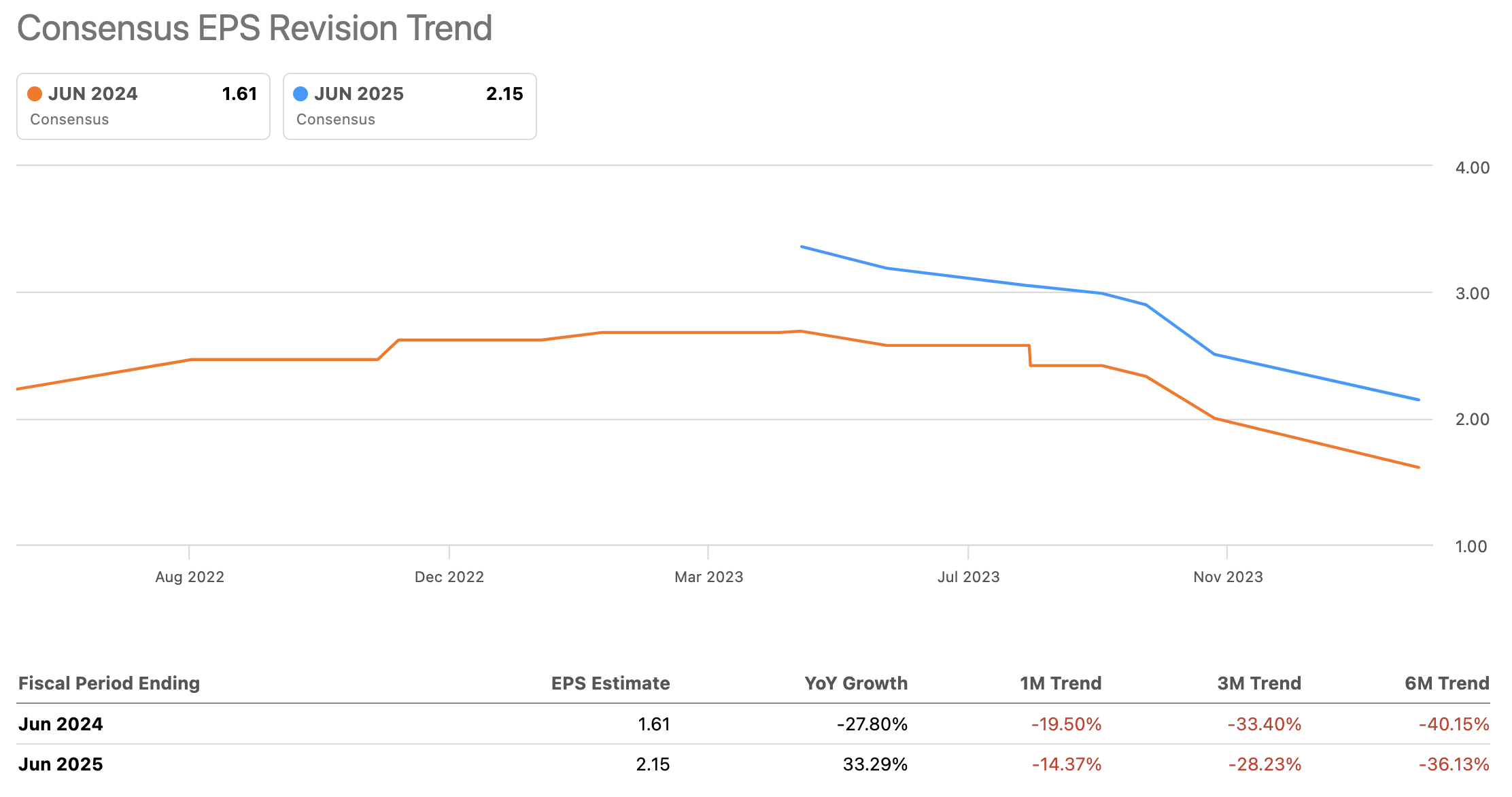

EPS estimates are also getting lower over time, representing real operational challenges ahead but also signifying lower investor sentiment that should be a considerable concern for potential shareholders. The next few years are likely to see slower growth than now anticipated, and negative returns in the short term are not unlikely. However, I do believe the long-term, 10+ year holding period should provide decent price appreciation.

Seeking Alpha

Conclusion

Kimball Electronics remains a worthy investment to own. However, buying it at its present price could be problematic in the short term due to high risks related to downward momentum and poor revisions primarily. Coupled with an uncompetitive balance sheet and cash flow statement at this time, the value opportunity is based on favourable market growth and my long-term EPS expectations. However, due to the uncertainty surrounding these factors, my analyst rating for KE stock is a Hold.

Q2 2024 Earnings Call Transcript")