Lauren Nicole/DigitalVision via Getty Images

Fidelity National Financial (NYSE:FNF) is a financial company that offers a variety of financial products and services, including but not limited to title insurance, mortgage related services, real estate technology services, annuities and life insurance products. The company also owns a majority stake in F&G Annuities & Life (FG) which it spans off as a separate company recently.

Business Segments (Fidelity National Financial)

Title insurance is a big part of this company’s business. Basically, when a real estate transaction is done, there is a risk that the asset’s title ownership history might be sketchy. In rare cases, a real estate asset might have hidden or unknown liens or different challenges against its ownership. Some of the ownership documents might have been forged or manipulated, and there might be cases of fraud. These things happen very rarely, but they still happen and this is why bank mortgage issuers require purchase of a title insurance which provides financial compensation in case there is an issue with its title, whether it’s a case of an innocent negligence or actual fraud. A title insurance could also cover legal costs associated with these types of situations, which can get quite costly.

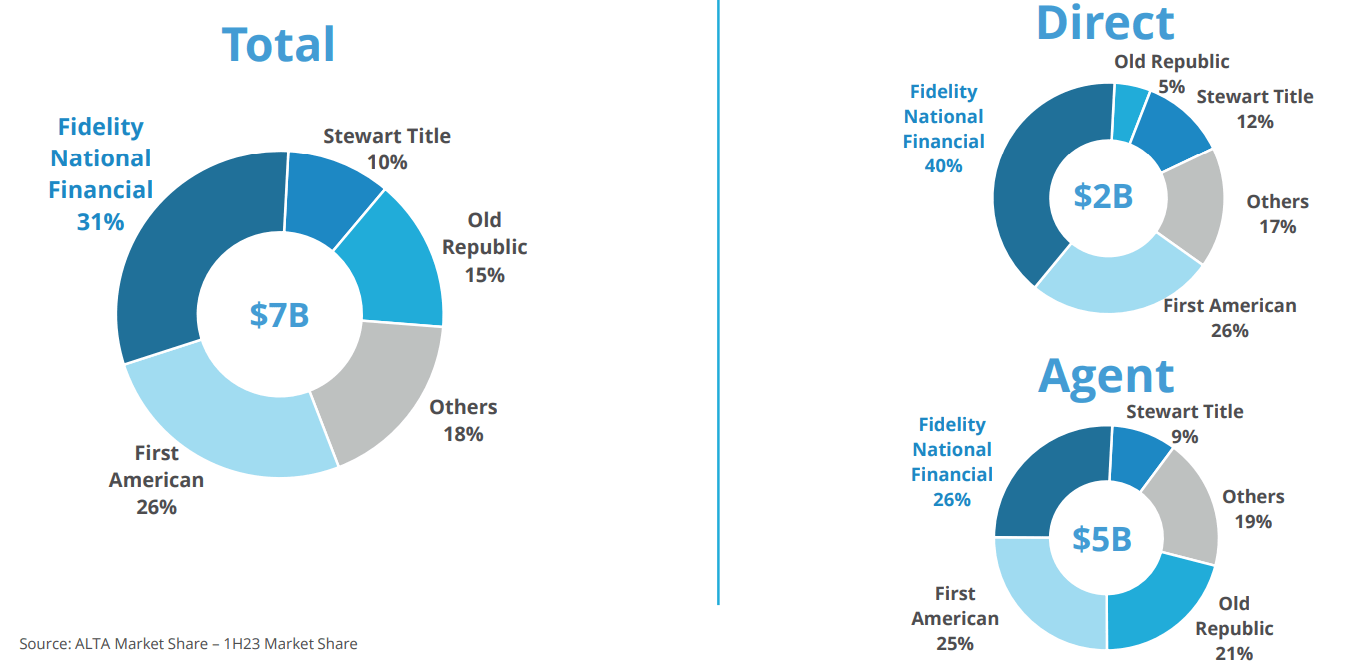

Fidelity National Financial has a nationwide market leadership in total market with a market share of 31%. In direct sales, it also claims a market leadership with a 40% market share and in agent-based sales, it claims a similar leadership albeit with a smaller margin of 1% against its top competitor. On a positive side, this market leadership establishes the company as an almost dominant force, but on a negative side one could also argue that it limits the company’s future growth since having this much market leadership leaves little room for any further growth.

Market Share in Title Insurance (Fidelity National Financial)

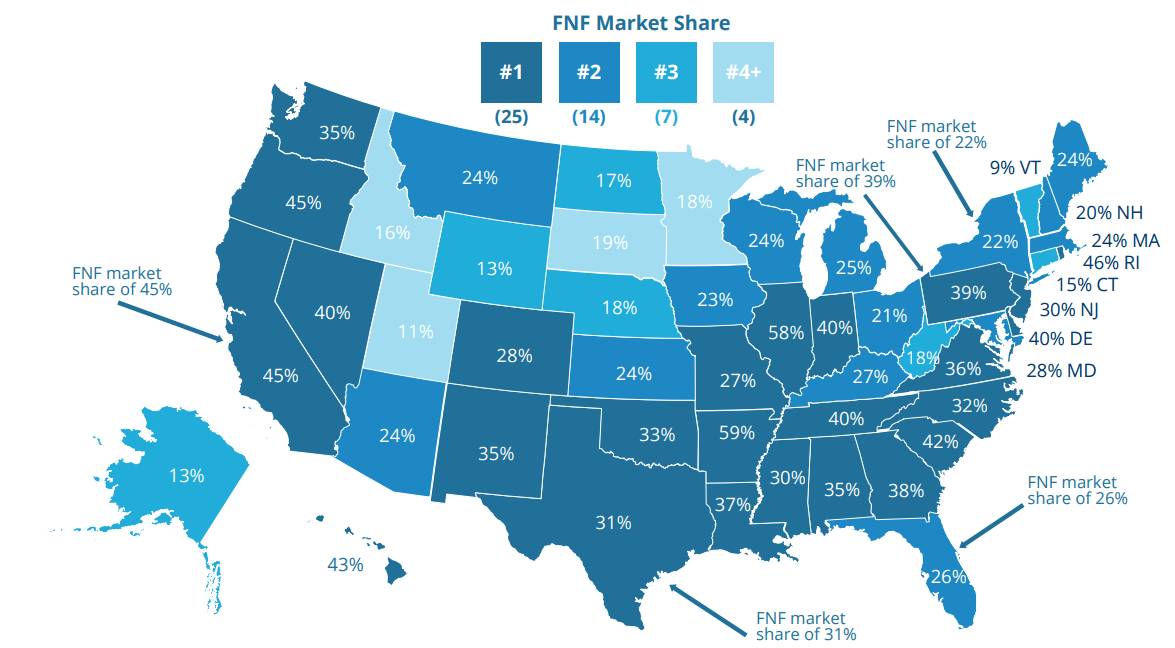

This is even more dramatic on a state by state basis. Out of the 50 states where it operates within the US, the company claims number 1 spot in 25 states, number 2 spot in 14 states and number 3 spot in 7 states. There are only 4 states where it’s not in the top 3. For example, it leads the market in California, where it enjoys a market share of 45%. As part of its business plan, the company uses its strong market presence in the title insurance market to upsell its other products such as mortgage related services and real estate technology-based products. This is likely where future growth may come from.

Market Share by State (Fidelity National Financial)

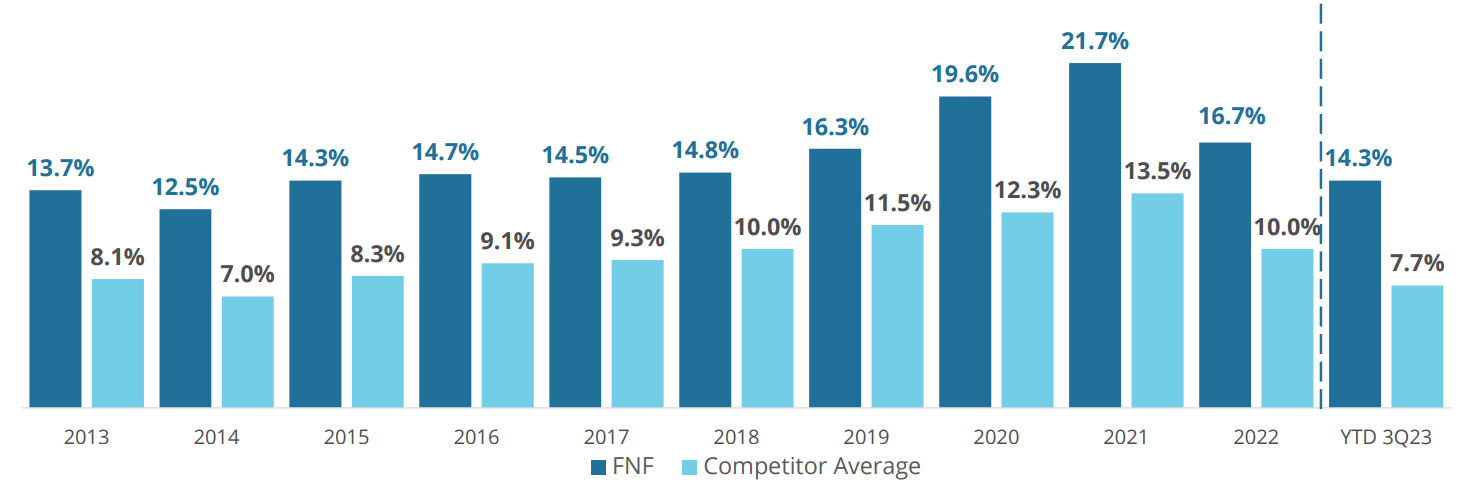

Title business is becoming highly digitalized and automated, which means that a lot of the title authentication checks can be made much quicker now. Not long ago, companies used to take several days or more to check the authenticity of titles while they contact many agencies and use traditional techniques. Now many of the authenticity checks can be completed digitally and within minutes. If there is an unknown lien or suspicious activity about an asset’s ownership, it comes visible fairly quickly, and it can be dealt with much faster. The latest technological advancements and innovations allowed the company to have healthy levels of margins. FNF seems to have significantly better margins than its competition, but the company’s margins started to decline starting 2022 because of the direct and indirect effects of a higher interest rate environment because it meant less demand for mortgage and fewer mortgage transactions which affected both FNF’s title insurance business as well as its mortgage related side businesses.

Margins vs Competition Over Time (Fidelity National Financial)

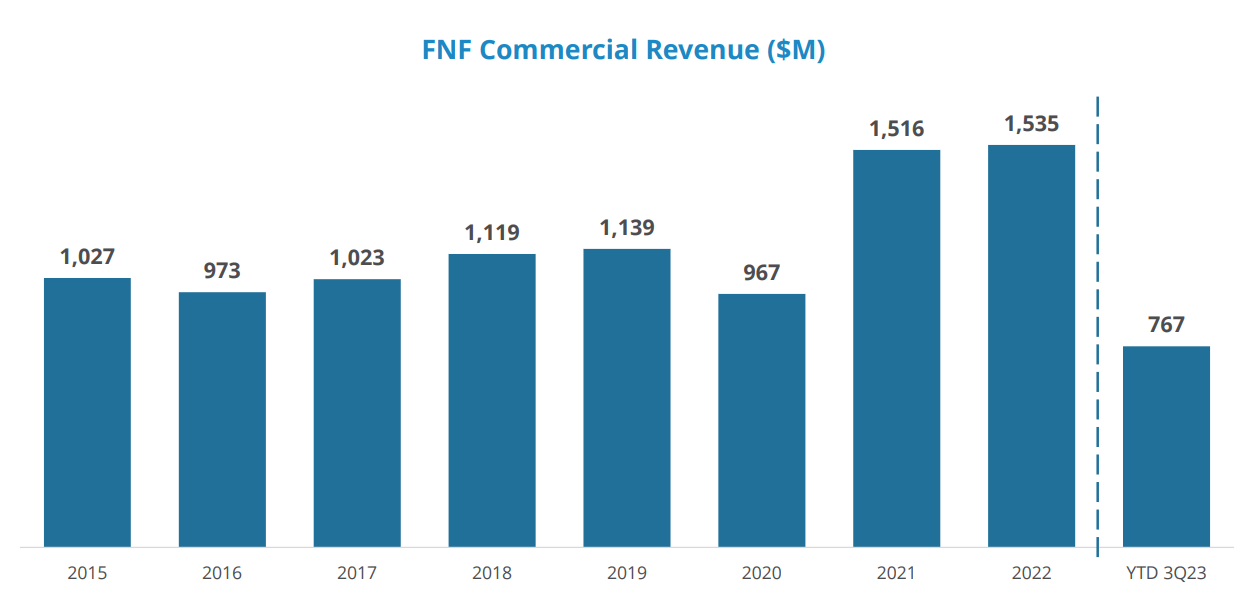

The company’s main business will likely recover once interest rates start dropping and demand for mortgages starts rising again, but there are still some concerns about the company’s growth because it also has a reliance on commercial real estate, which has been struggling quite a bit since 2020 when office buildings started to get less and less utilization due to work-from-home trends, so this is likely to remain a challenge for the company’s business even if residential mortgage demand comes back roaring at some point in the future when interest rates drop again. The company’s commercial revenues actually rose significantly from 2019 to 2022 (up from $1.13 billion to $1.53 billion), but it only generated about $767 million in the first 3 quarters of this year, and it’s on track to end the year a little above $1 billion for 2023 when it announces its results for the full year in a couple weeks.

Commercial Revenues (Fidelity National Financial)

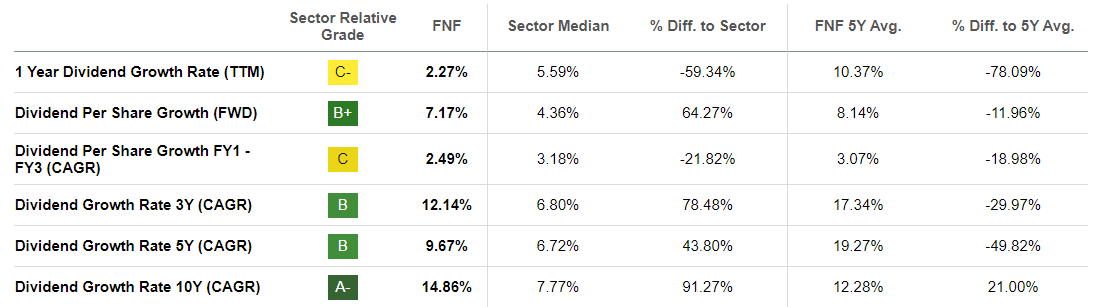

The company has a dividend yield of 3.75%, and it’s been posting strong dividend growth in recent years. In the last 10 years, the company grew its dividends at an annualized rate of 14.86% and in the last 5 years its dividends grew at an annualized rate of almost 10%. This is significantly better than the sector average of 6-7% annual dividend growth.

Dividend Growth (Seeking Alpha)

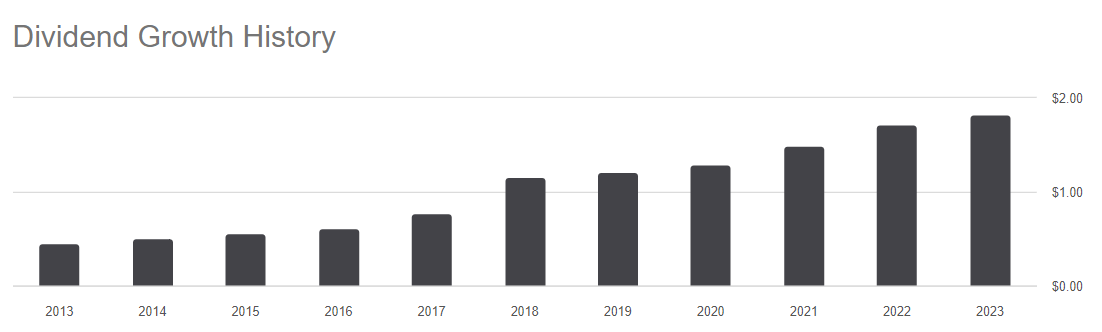

On a yearly basis, the company grew its dividends from 46 cents per year to $1.83 per year per share. The company hiked its dividends for 12 years in a row, and it’s on track to reach 13 years in 2024 as the management seems to be committed to returning cash to investors.

Dividend History (Seeking Alpha)

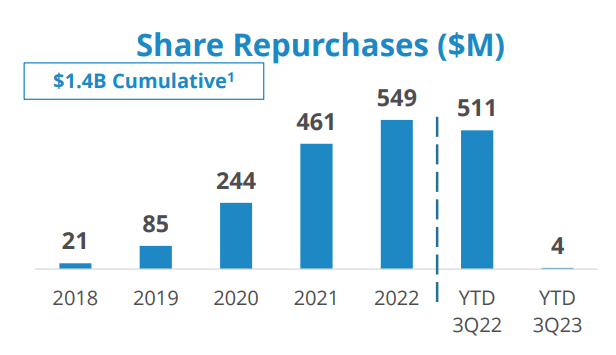

In addition to paying a nice dividend that grows every year, the company also spends a good amount on stock repurchases. Between 2018 and 2022, the company spent $1.4 billion on share buybacks, which accounts for close to 10% of its current market cap. Also, from 2018 to 2022, the company increased its share repurchases significantly from year to year, up from $21 million in 2018 to $85 million in 2019, to $244 million in 2020, to $461 million in 2021 and to $549 million in 2022 which is a 25-fold increase in 4 years. Having said that, the company hardly spent any money on repurchases in 2023 in order to preserve cash since the environment has been more challenging, but dividends continued to grow. Between dividends and repurchases, the company returned about $3.4 billion to investors since 2018, which is pretty significant considering that its total market cap is around $13 billion.

Share Repurchases (Fidelity National Financial)

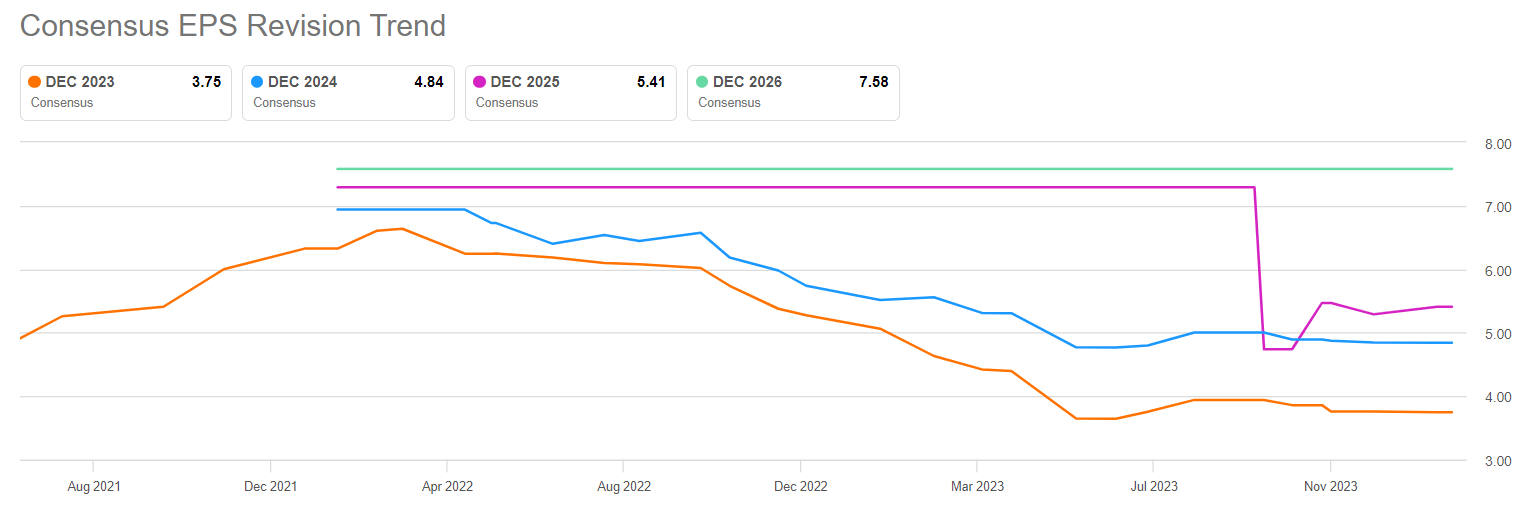

The company’s dividend seems safe for the time being as it is expected to generate $3.75 per share this year in net income, which covers its current dividend of $1.85 since the company’s payout ratio is 49%. Moving forward, analysts expect the company’s profits to rise to $4.84 in 2024 and $5.41 in 2025, which means that its dividend should be not only well-covered but also there may be plenty of room for future dividend hikes if the company can meet or beat these estimates.

Analyst Estimates (Seeking Alpha)

Analysts have been cutting their estimates for this company’s earnings since late 2021, but their estimates seem to be stabilized now. Unless we get another shock from the inflation side which might drive interest rates much higher, the company’s forward earnings should offer more visibility moving forward and things can also get significantly better if interest rates start declining rapidly as some people expect them to do so.

Trending of Analyst Estimates (Analyst Estimates)

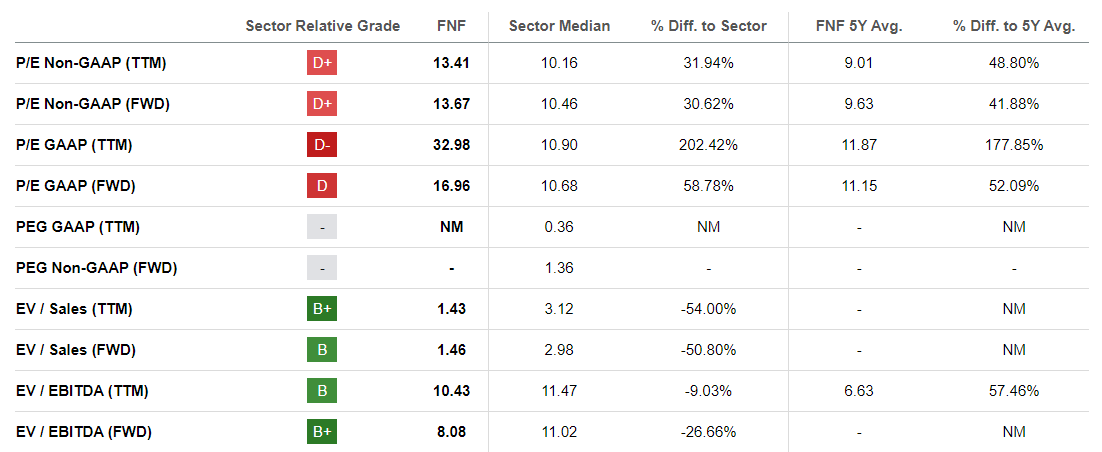

The company’s valuation is not something I’d call cheap, though. Sure, FNF’s P/E of 13 may look cheap when compared to S&P 500’s (SPY) average P/E of 25, but financial sectors as a whole tends to have much lower P/Es than the overall market. Currently, the P/E ratio of the sector median for this company is only around 10, which makes this company pricey at a P/E of 13, which would have looked cheap if it as in any other industry (especially technology or consumer staples). The company itself has a 5-year P/E average of 9, so it is trading at a premium against its own historical average as well.

Valuation (Seeking Alpha)

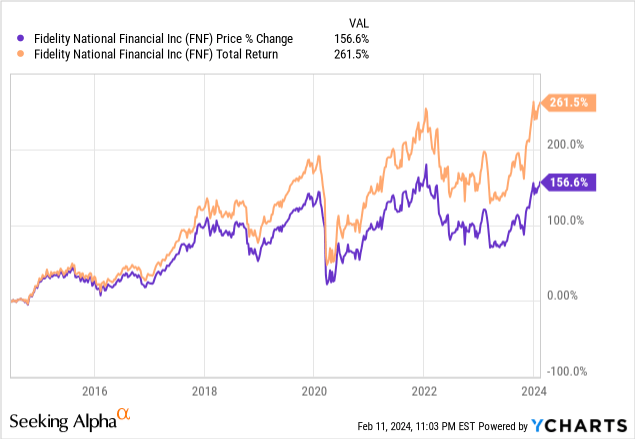

I can see this stock purely as a dividend play, with a nice yield and good track of dividend growth. In the last 10 years, the stock was up 156%, but its total return was a much better 262% thanks to its dividends (assuming reinvestment of these dividends). I wouldn’t expect much upside from the stock in terms of share price, but I wouldn’t be surprised if the dividend hikes continued for quite some time, unless the economy suddenly took a turn for the worse.

At the end of the day, this company operates in a cyclical sector and its long-term performance will be in line with the performance of the overall economy, so if you are bearish on the economy as a whole, you might not want to buy this stock. If you are feeling bullish about the economy overall and believe that there is a rate cut coming soon, this may be a good stock to buy, especially if you are a dividend investor with a focus on dividend growth.

Q2 2024 Earnings Call Transcript")