imaginima

Introduction

Five months after my initial coverage of Western Digital Corporation (NASDAQ:WDC), I remain skeptical that it is a buying opportunity.

The company has recently reported earnings that slightly surpassed the consensus for revenue and EPS. Two out of its three customer segments experienced sales growth, with the third remaining flat. Management specifically highlighted the increasing gross margins of the company’s segments, mentioning that another high growth period might be imminent.

When I compare what the management is saying with what I fundamentally see, I find these positive comments hard to believe. End markets are still weak, the Chinese economy is in trouble, other semiconductor players are guiding for lower sales, and there are other known unknowns that I don’t want to bet on.

Although the stock significantly outperformed the market since my initial coverage back in September, I believe my thesis is still valid, and I reiterate the “Hold” rating.

Quick Recap of the Business

Western Digital develops Flash and Hard Disc Drive (HDD) technologies for data storage. These devices can be found in most electronic devices from your computer and mobile phone to big data centers. That is why there are lots of different customers.

The company categorizes its customers into three main segments: cloud, client, and consumer. It is important to understand who they are to accurately comment on the earnings. Cloud customers are operators of data centers, who need data storage devices to enhance their systems. Client customers are original equipment manufacturers (OEMs) that integrate Western Digital’s storage products into various products they manufacture, such as computers, mobile phones, and automobiles. Lastly, the consumer segment encompasses retailers that distribute these products directly to the end-users.

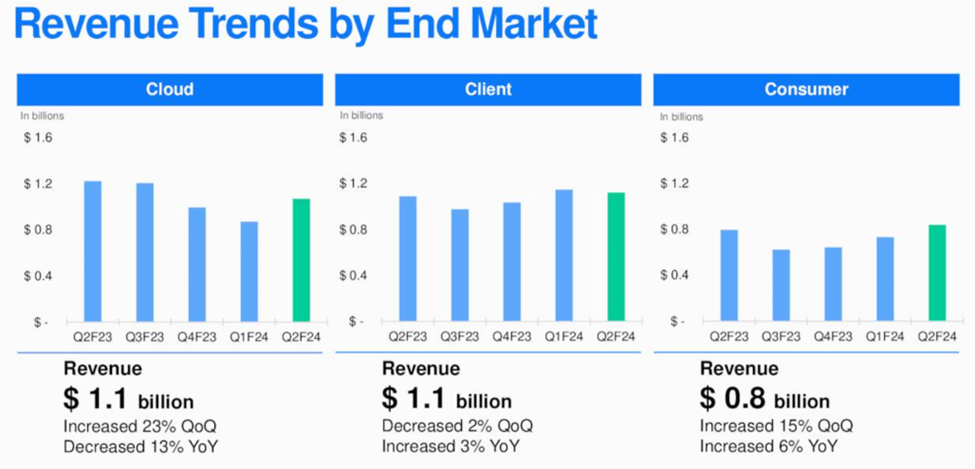

According to the Q2 2024 earnings; cloud, client, and consumer end markets accounted for 35%, 37%, and 28% of the company’s total revenue, respectively.

Western Digital Q2 2024 Earnings Presentation

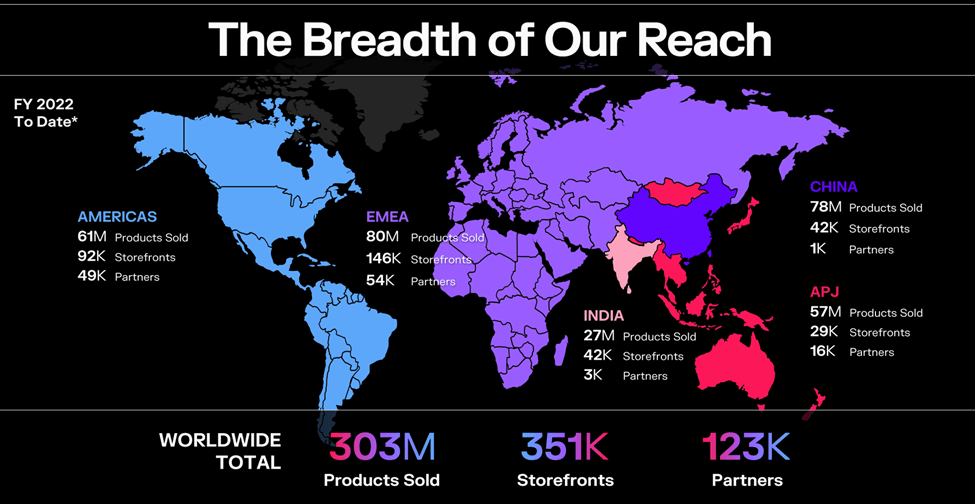

Before we get into the analysis of the earnings call, it is also important to note that a huge part of the company’s products are sold in China. According to the Investor Day held in May 2022, China was the second biggest region in terms of sales. With 78 million products sold, China closely follows the EMEA region, which leads with 80 million products sold.

Western Digital Investor Day 2022

Q2 2024 Earnings Results

Western Digital disclosed its Q2 2024 earnings on January 25, 2024, leading to a 5% decrease in share value immediately following the announcement.

Despite a 2.6% decline in revenue year-over-year and remaining unprofitable for the fifth consecutive quarter, the company managed to slightly surpass both revenue and EPS projections.

Management expressed satisfaction with the quarter’s performance and optimism for the year ahead, primarily attributing this to recovering margins and sustained strength in end markets. As you saw earlier in the article, sales were higher quarter-over-quarter in cloud and consumer end markets, and flat in client. Management thinks this is an indicator of end-market resiliency. Additionally, the gross margins for both segments improved compared to the previous quarter.

CEO David V. Goeckeler highlighted the anticipated short-term demand surge from the adoption of new technologies, such as Generative AI, stating:

In addition to the recovery in both Flash and HDD markets, we believe storage is entering a multiyear growth period. Generative AI has quickly emerged as yet another growth driver and transformative technology that is reshaping all industries, all companies in our daily lives. […] In addition, we believe the second wave of generative AI-driven storage deployments will spark a client and consumer device refresh cycle and reaccelerate content growth in PC, smartphone, gaming, and consumer in the coming years. Our flash portfolio is extremely well-positioned to benefit from this emerging secular tailwind.

While the management paints a significantly positive picture about the quarter and future outlook, after zooming out, we can understand the company’s situation better.

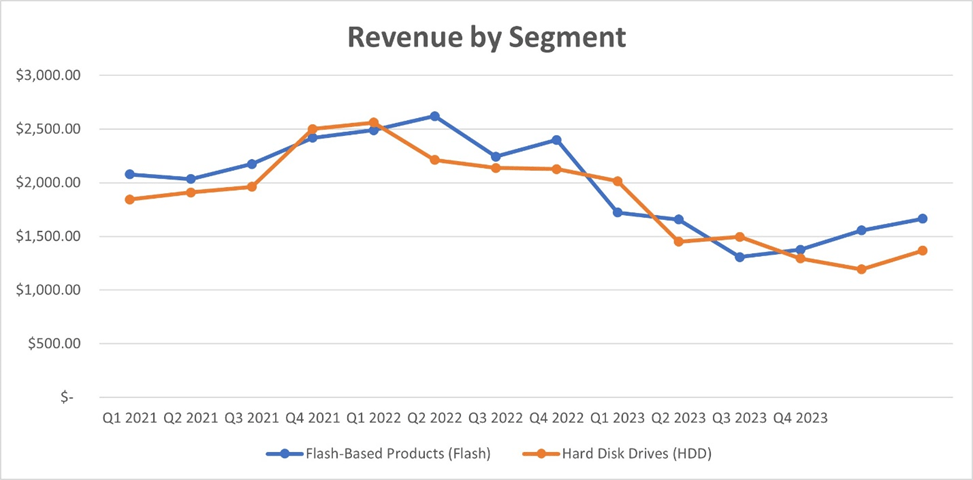

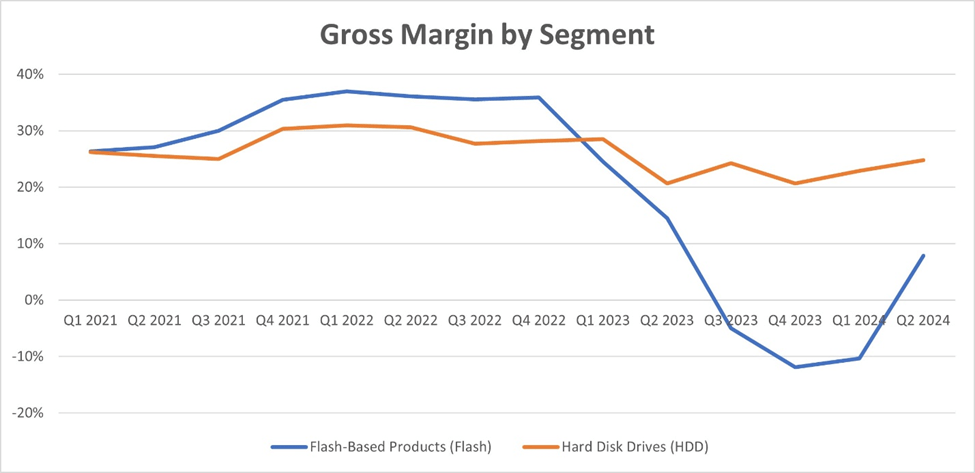

This was the seventh straight quarter of year-over-year revenue decline for the company. In the meantime, the Flash business became unprofitable due to weak consumer demand and increasing COGS, and HDD kept margins higher mostly thanks to Generative AI and the sudden need for more data centers. These trends can be seen below.

S&P Capital IQ S&P Capital IQ

The company recorded increased sales and improved gross margins in the last two quarters compared to Q4 2023. However, I think the management is downplaying how big the problem is.

A Multitude of Challenges Ahead

Let’s delve into the end markets that management claims are robust. As previously discussed, “clients” refer to OEMs producing consumer electronics, while “consumers” denote the end-users themselves, indicating that these markets share similar dynamics.

First of all, a strong global economy is crucial to believe that consumer electronics sales will increase and drive growth for the company. According to Gartner, worldwide PC shipments declined a whopping 14.8% in 2023. Global smartphone shipments were down 4%. Consumers are weak and OEMs know this. Combined with high interest rates, these producers of consumer electronics are not motivated to grow.

Additionally, as I mentioned in the description section, China and the rest of Asia are critical markets for Western Digital. That region brings in most of the revenue. The Chinese economy is in turmoil. There are serious structural issues that prevent the anticipated sustainable growth of the economy. The country struggles with deflation, as customers are still wary of spending.

On a different note, the cloud end market has been relatively strong during this period. Thanks to the pace of innovation in Generative AI, we have gone through a period of higher need for data storage and higher demand for data centers. This kept the cloud business and HDD margins alive. As seen above, the CEO expects a second wave of growth in this field. I cannot see another growth period as strong as the first one, especially when interest rates are at these levels for longer.

Moreover, the broader semiconductor market, with a few exceptions like Nvidia (NVDA), has been struggling. Intel (INTC), for instance, has recently guided for lower-than-expected earnings and has issues with the end market demand.

Finally, two main developments add lots of uncertainty to this potential investment. First, the company has announced its intention to split into two entities, one focusing on HDD and the other on Flash, targeted for the second half of 2024. Yet, details of the execution remain unknown.

Furthermore, there are ongoing rumors about the Japanese chipmaker Kioxia trying to revive merger talks with Western Digital, potentially following the company’s division. It’s too early to predict the outcome of these talks.

Valuation

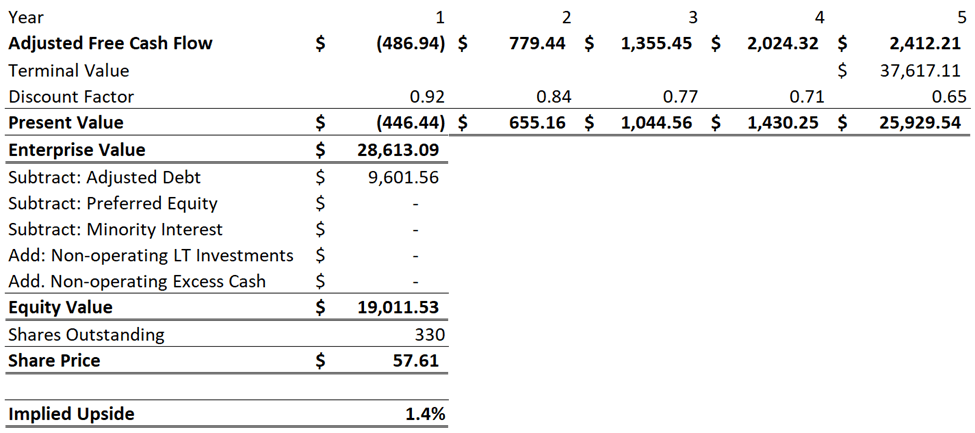

As the stock surged 28% after my initial coverage was published, I will update my DCF analysis and share the revised figures.

My estimated adjusted free cash flow is -$487 million in 2024 and $2.41 billion in 2028 as demand recovers.

I am using a terminal growth rate of 2.5%, as I believe the industry can grow faster than long-term inflation with strong growth drivers. The cost of equity is calculated as 10.9% using a long-term risk-free rate of 2%, a market risk premium of 5.7%, and the stock’s 5-year equity beta. The cost of debt is taken at 6.28%, considering the yield-to-worst (YTW) the company’s 2029 bonds have.

Using these numbers, I find an equity value of $19.011 billion, which means a target share price of $57.61. This is only a 1.4% upside over the current share price at the time of this article’s writing.

S&P Capital IQ – Author

Conclusion

I believe that the industry Western Digital is in is going to benefit a lot from the demand for more data storage solutions. As technology develops (not necessarily Generative AI), we will generate more data, requiring more data centers. Western Digital stands well-positioned to capitalize on this growth trajectory.

Its Q2 2024 results were not bad. When compared to two quarters prior, gross margins in both segments have improved, and management’s remarks underscore the resilience of the end markets. That said, I find it hard to believe that end markets are actually strong.

Many points of concern prevent me from investing in this name. These include less demand for consumer electronics, stagnant growth of the data space partly because of high interest rates, an awful Chinese economy, and known unknowns such as the company splitting into two and a potential merger with Kioxia.

Combined with a valuation that does not look cheap, I reiterate my “Hold” rating for Western Digital.

Q2 2024 Earnings Call Transcript")