Bloomberg Creative/Bloomberg Creative Photos via Getty Images

Introduction

To paraphrase the famous Wayne Gretzky quote, one should not skate to where the puck is, but to where the puck is going. Whether it knows it or not, Glencore (OTCPK:GLNCY) (OTCPK:GLCNF) is taking this advice to heart by making recycling an integral part of its operations. While it is still essentially a mining company at its core, recycling metals and batteries gives the company a leg up on some of its mining and recycling competitors, and positions Glencore to prosper in perpetuity as a future battery and metals recycling company. However, its financial situation may be a roadblock to achieving this goal.

Balancing its precarious finances against the opportunity in recycling, I consider Glencore a hold for now.

Financials

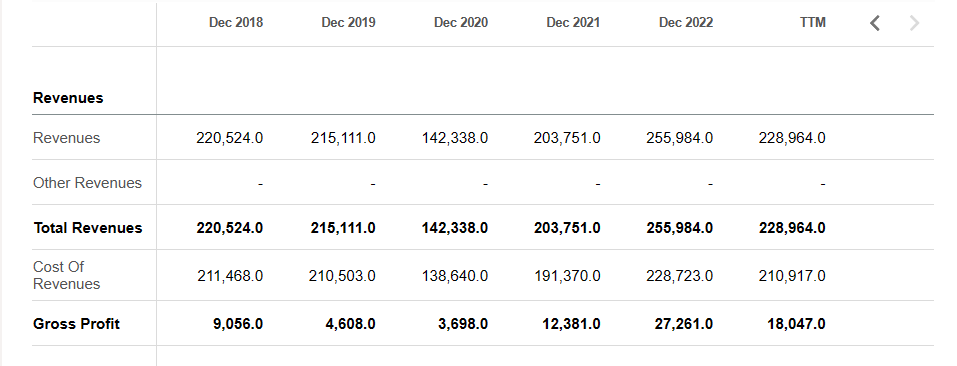

As a multinational mining giant, Glencore’s revenues are predictably enormous. The company pulled in between $200 billion and $250 billion every year between 2018 and 2022, except for 2020, the first year of the Covid-19 pandemic. That year, Glencore gained only $142 billion in revenue, a noticeable and expected dip in an otherwise excellent period of revenue generation. That’s the good news. Unfortunately, while Glencore’s revenues have been eye-watering over the past few years, its gross profit and other measures are rather lackluster.

Seeking Alpha

Glencore made $9 billion, $4.6 billion, $3.7 billion, over $12 billion, and over $27 billion in gross profit in the 2018-2022 period. This indicates that in a good year, Glencore is only managing a ~10% gross margin nowadays. Compared to Vale (VALE) and BHP (BHP) (OTCPK:BHPLF), which average gross margins in recent years of ~40% and ~80% respectively, Glencore seems to be struggling to convert revenues to profit.

Seeking Alpha

For net income, Glencore posted a gain of ~$3.5 billion, a loss of $400 million, a loss of about $2 billion, a gain of about $5 billion, and a gain of about ~$17 billion between 2018-2022, with $9 billion of income posted in the TTM period, revealing net margins of less than 10% at best. This also compares unfavorably to peers like Vale and BHP over the past few years, with average net margins of around 20% and 25%, respectively.

Seeking Alpha

Operational cash flow for Glencore has been U-shaped, with $11 billion in 2018, ~$8.5 billion in 2019 and 2021, ~$13 billion in 2022, and a big dip in 2020 to $2 billion. This compares to Vale’s more steady operational cash flow of ~$15 billion on average in the past 5 years, along with BHP’s cash flow of ~$20 billion.

These differences in core business profitability are rather disturbing, especially considering the vast advantage Glencore has in revenue collection. Vale’s annual revenue has been between $30 billion and $55 billion, and BHP’s revenues have been between $40 billion and $65 billion, yet lately they bring in more operational cash than Glencore, which has over $200 billion in annual revenue.

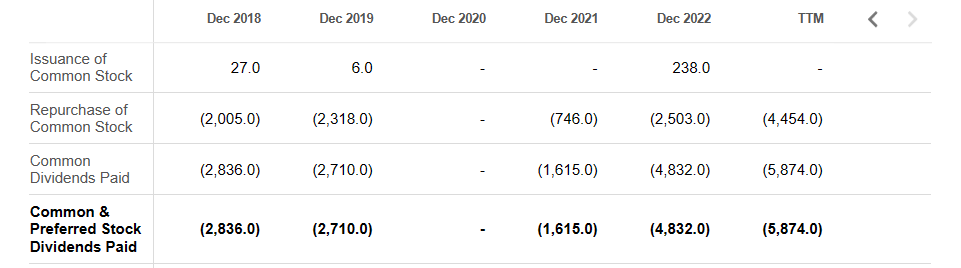

Against these subpar profits and cash flow from Glencore, the company has around $30 billion of debt, with only $2 billion in cash. Oddly, the company offers investors a dividend yield of over 10%, far above the material sector’s 2%; such dividend payments cost Glencore about $6 billion in the trailing twelve months alone, and regular dividends plus share repurchases have cost the company multiple billions for years. The company has also spent billions of dollars buying back its stock. Some of this money could be restricted and put toward the recycling business, or toward paying its debt.

Seeking Alpha

To be fair, it is possible that the costs of ramping up its recycling arm are also eating into Glencore’s capital, though there could be several reasons for its low margins. If the recycling business is the main reason, the financial picture will likely worsen over time. As I discuss later, I think multiple factors may cause recycling to pervade more and more of the mining industry. In any case, Glencore’s arguably undisciplined spending is not helping lay a strong foundation to achieve the long-term goal of becoming a larger recycling player.

Earnings Expectations

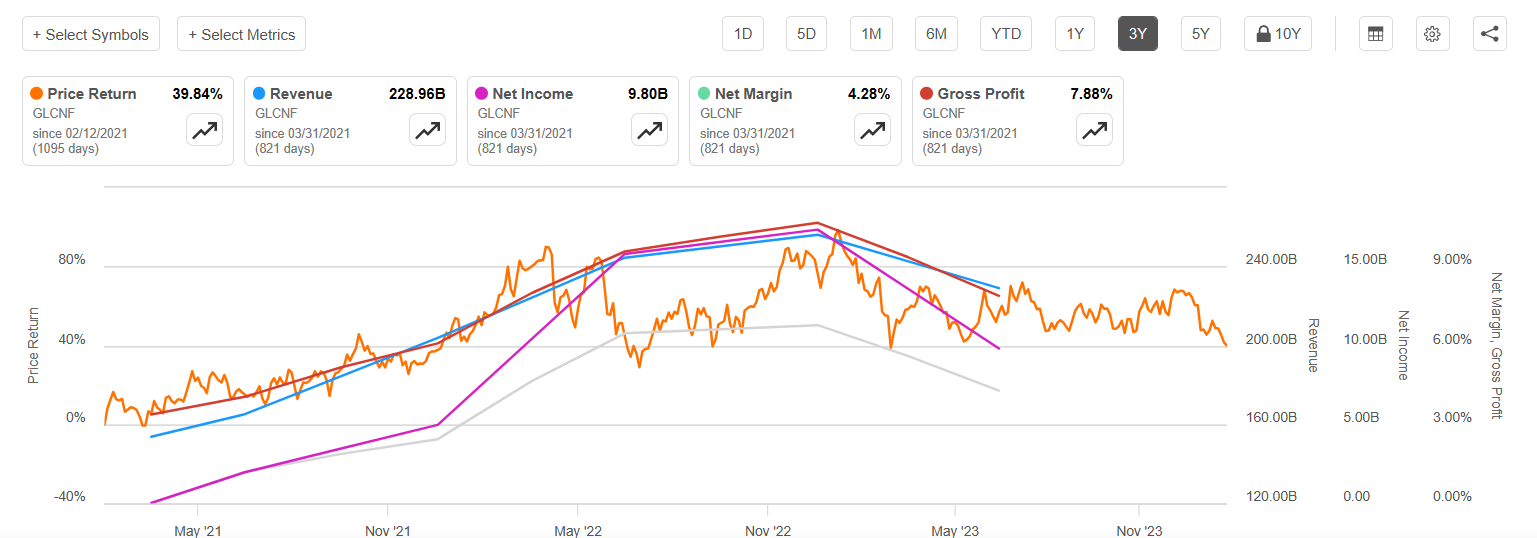

Here is a basic summary of Glencore’s recent performance in one chart:

Seeking Alpha

In essence, Glencore’s performance peaked in the aftermath of the pandemic, reaching highs for stock price, margins, revenue, etc. at the end of 2022. While it isn’t quite visible on the summary chart past H1’23, most of the stats for Glencore in 2023 have shown a YoY decline.

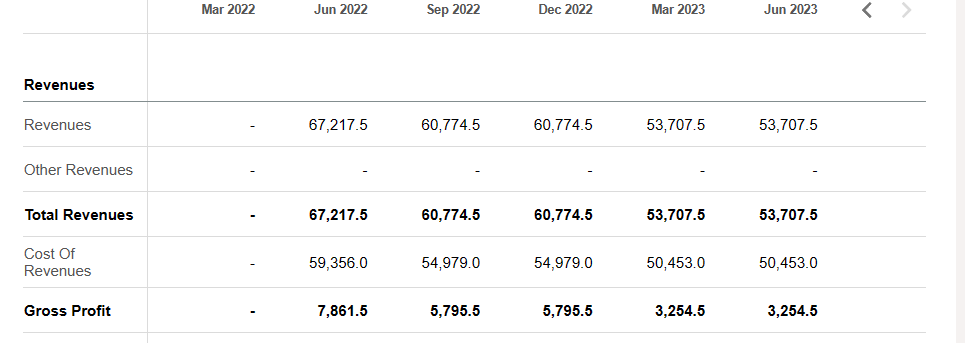

Revenues are down ~20%, and gross profits are down by ~60%:

Seeking Alpha

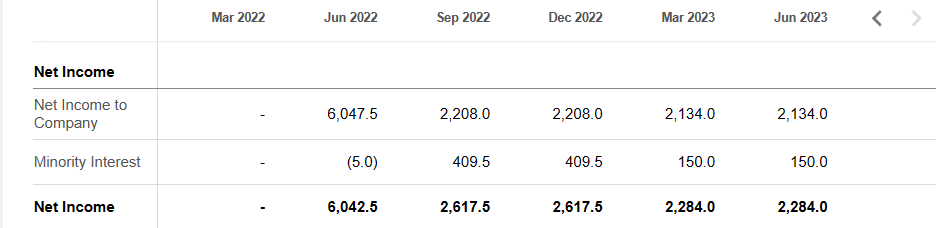

Net income is down by over 60%:

Seeking Alpha

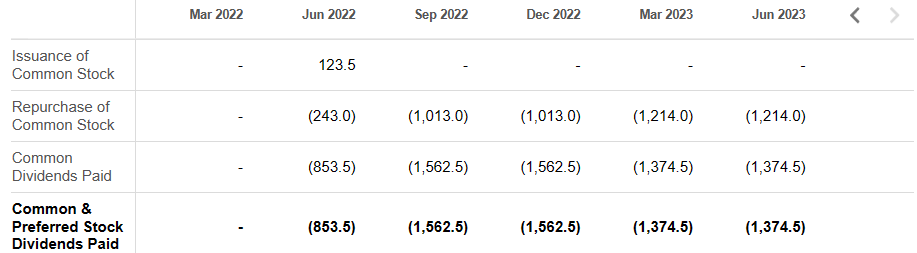

Overall, there is little here for investors to like for a full-year earnings report. Even worse, after a brief period of reduced spending in 2022, Glencore went back to its old habits of buying back stock and paying costly dividends:

Seeking Alpha

Some investors are a big fan of buybacks. I don’t necessarily mind them, provided the company’s finances are otherwise in order. That is not the case with Glencore, so I see this as another piece of bad news.

Considering Glencore has already fallen from its 2022 highs, the market has likely priced much of this disappointing news into the stock, so a summation of it in the upcoming earnings call likely won’t move the needle much. I would hope that Glencore’s management declares its intent to tighten its belt and reinstate cost-cutting measures due to high interest rates or some other negative macro factor, but it is more likely that, without some sort of fiscal wakeup call that makes Glencore’s stock or balance sheet hit rock bottom, management will guide the company toward business as usual, settling for financial mediocrity for the time being.

Glencore Can Transition from Mining to Recycling

Since it is involved in both mining and recycling, Glencore is not strictly a mining company, but a metals company. It can direct huge swaths of revenue toward building out its recycling capacity so that its business can sustainably produce metals without a dependence on mining. Recycling pure plays like Redwood Materials and Li-Cycle (LICY) are newer and smaller, and must start their operations from scratch, reducing their speed of growth. Such pure plays can also be plagued by near-existential financial crises that lead to operational constraints, as seen with Li-Cycle. Despite its subpar financial situation, Glencore has neither issue hampering its recycling ambitions, as it brings in hundreds of billions in revenue that it can direct toward its recycling business.

The Importance of Growing the Recycling Business

The General Importance of Metals Recycling

I have spoken in multiple places about my thoughts on the importance of battery and metal recycling, so I will attempt to consolidate my thoughts in this subsection.

These are my main thoughts on battery and metal recycling, from my July 2023 article on Tesla:

… recycling of batteries and use of recycled [battery] material … will ultimately reduce, if not eliminate … the harms to the environment that stem from mining as an industry. As explained in this article on the benefits of recycling instead of mining, recycling battery materials will ease the strain on the materials supply chain, because the supply used will be continuously circulating and readily available when needed, instead of being stuck in the ground waiting to be drilled for and dug up. Recycling will also result in starting materials with fewer impurities, due to having been purified already for their first cycle in a product’s life. It is quite likely that recycled battery material will become much, much cheaper to produce than mined material, because the high purity of recycled material reduces the need for most refining processes and expenses involved in using it.

Finally, recycled materials will likely also be overproduced and stored when not in need in order to account for fluctuations in demand for a given recycled material. For example, if recycled cobalt is all the rage for a certain class of products, demand will stretch the supply of recycled cobalt thin; however, if the product demand reverses and cobalt demand likewise recedes, the recycled cobalt will simply be stored when these products are disposed of and given to the materials recyclers. The recyclers will then lock up the recovered cobalt and wait for another spike in demand for it to be used again. This will reduce the possibility of shortages for battery materials and other related commodities (barring obscenely and unpredictably high demand), stabilizing the prices for recycled materials compared to mined materials, especially as these closed-loop recycling supply chains mature.

Additional thoughts are as follows:

- In time, I believe all batteries will be recycled and will come from recycled material, as part of a closed-loop battery production system. It could take 10 years, or 100, but it is inevitable. Mining literally cannot continue in perpetuity; there is only so much material in the ground and oceans to dig up, use once, and then discard.

- It is said nowadays that battery supply is set to severely lag future demand, but I think this can be addressed by pivoting from mining to recycling, in part because recycled materials are more accessible; landfills are easier to access than subterranean or ocean floor mines.

- The recycled battery market stands to be quite lucrative, growing at a CAGR of up to 38% from 2023 until 2030 by some estimates.

- Like Tesla, Glencore’s mining peer Eramet (OTCPK:ERMAF) (OTCPK:ERMAY) has a recycling arm that has recently begun to recycle lithium ion batteries, but such a focus on just lithium ignores the multiple other battery types we can use to store energy, including intermittent renewable energy from wind and solar. Examples of alternative batteries include flow batteries and pumped hydro/gravity batteries. Both will likely have several benefits that even lithium ion batteries do not enjoy, such as longer storage times. Some of these battery types, like flow batteries, will need less conventional metals to operate, thus sustaining demand for diverse battery material, at least some of it recycled. Glencore’s recycling division works with a variety of metals that can be used as battery material, bringing copper, cobalt, zinc, nickel, and more into its network of recycled materials; it also works to recycle lithium ion batteries, as some of its peers are starting to do.

- Batteries are being made more efficiently and with fewer metals. Lithium iron phosphate batteries, for example, are mostly comprised of only 2 metals. This simplifies battery production methods by reducing the necessary complexity involved in dealing with more battery metals.

- Recycled materials and increased use of environmentally friendly refining processes will reduce the need for harsh chemicals to purify raw material to make it battery grade, reducing pro-environment groups’ antipathy toward expanding the use and production of metal-based batteries.

If recycling replaces mining as the primary source of metals for batteries and other materials, as I believe will eventually occur over the next few years and decades, Glencore could direct revenues, or just its profits, from its mining division into growing its recycling division to keep pace with the mining-to-recycling transition. This is the strategy Ford is pursuing in transforming its business from producing internal combustion vehicles to producing electric vehicles.

In both cases, this strategy allows a company with a profitable business line that is unsustainable long term to contribute to the building up of a business line that will eventually be the company’s primary source of sustainable profits in the future. Due to Glencore’s size in the mining market, that means a significant amount of profit over the coming years with which to fund its recycling business – that is, if it goes this route of profit transference. Time will tell how well the company transitions, and whether it does so via the aforementioned method.

Regardless, I believe that battery and metals recycling could expand and eventually replace mining, and Glencore is likely to expand along with it, if its finances allow. If it does succeed in becoming a high-volume metals recycler, its finances may improve due to the much lower costs of mining for metal as opposed to refining and reusing available metal supply. The process of scaling the recycling business up so that it is profitable may be difficult, but the reward could be worth it for Glencore in the long term.

The Financial Impact for Glencore

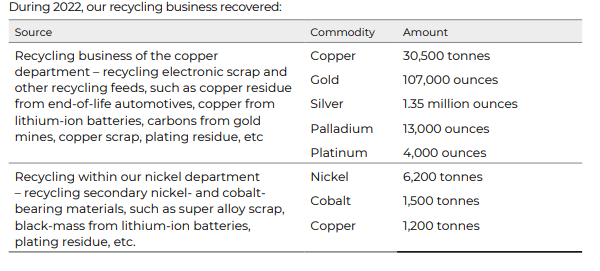

How significant might recycling be for Glencore over mining in terms of cost savings? Per Glencore’s 2022 Climate Report (page 43), Glencore states that energy savings alone from recycling copper can be 80-90%. Further, Glencore estimates that “[s]crap currently accounts for about a third of the roughly 30 million tonnes of annual global copper supplies.” Were this all recycled, the price of copper produced by Glencore and other large miners could fall by up to a third in turn by adding that copper scrap supply back to the mix. However, the cost to produce copper for the miners could fall by a third or more, since this waste copper doesn’t need to be extracted or so thoroughly refined, processes that add significantly to the cost of the metal. This dynamic would probably extend to other metals, too, and would result relative savings for Glencore and others by monetizing scrap waste.

Page 44 of the document reveals the savings potential in more detail for recycling metals. The document includes this chart:

Seeking Alpha

Considering spot prices for metals at time of writing, averaged for the period of mid-January to mid-February 2024 (~$8400 per metric ton for copper, ~$29,000 per ton for cobalt, ~$16,000 per ton for nickel, ~$2040 per troy ounce for gold, ~$22.5 per ounce for silver, ~$930 per ounce for palladium, and ~$900 per ounce for platinum), Glencore’s recycling operation managed to retain over $670 million in revenue that would have otherwise been wasted. A small amount for Glencore considering its revenues, but if this is high margin metal supply added to its reserves, Glencore’s entire operation could become higher in margin if it went the recycling route.

I am unable to find information indicating how profitable the recycling business is for Glencore, as it does not seem to be financially separated from Glencore’s virgin metal production. Still, Glencore’s financial efficiency, i.e. margins, could rise to match its peers if its recycling business raises margins for its operations, due to lower energy, extraction, and refining costs for recycling waste and scrap metal instead of mining virgin metal. Even if a transition to recycling would cut revenues for Glencore in the process, it would go a long way to improving the health of the company’s balance sheet by reducing costs and increasing margins, further underscoring the importance of growing Glencore’s recycling business.

Valuation

Vale and BHP are able to generate significant profit with much less revenue than Glencore, a disappointing state of affairs for Glencore. Glencore is not adept at allocating its large inflow of money, and the stock market has taken notice.

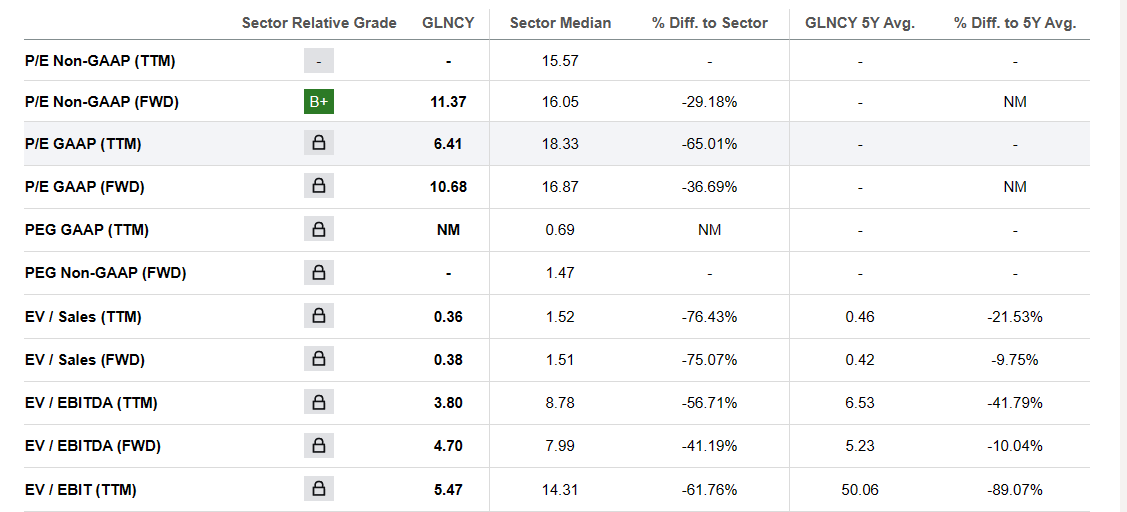

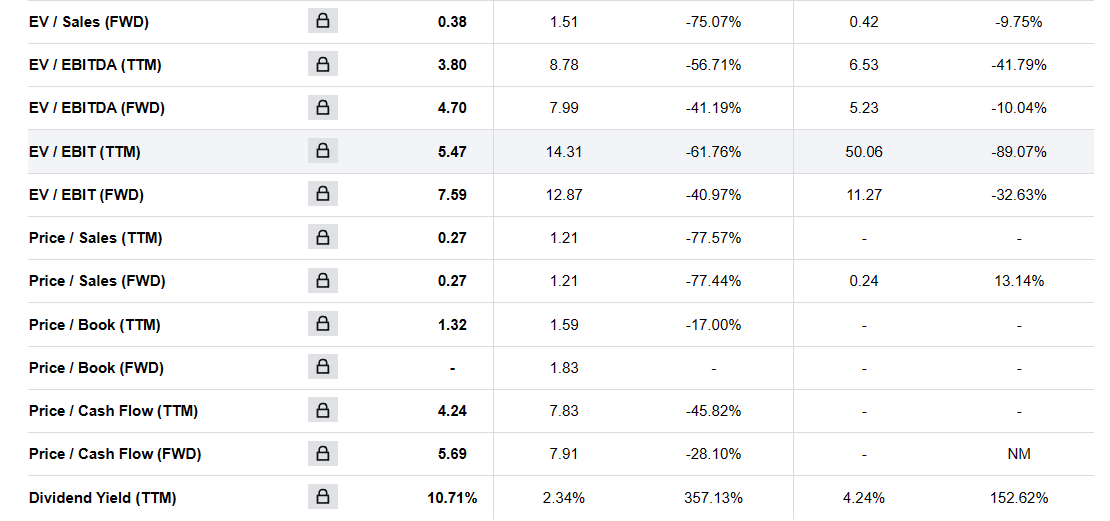

GLNCY/GLCNF’s trailing P/E ratio is ~30% lower than the materials sector average, and its P/B ratio is 17%. These are the only two metrics for which Glencore’s stock sees such slight undervaluation. Forward P/E, P/S, and P/Cash flow ratios are generally at a 50% discount or more for Glencore stock vs the sector.

Seeking Alpha Seeking Alpha

Glencore’s stocks’ valuation metrics handily underperform the materials sector across the board, demonstrating investors’ reasonable hesitance to put their own money into such an inefficient firm. Based on Glencore stocks’ 5-year percentage differences, this has been the case for some time now, and the discount to sector is well-earned.

If Glencore’s margins were as good as Vale’s (i.e. 40% gross margin and 20% net margin) with Glencore’s revenue kept at around $200 billion annually, it would have annual gross profit of $80 billion and net income of $40 billion. That would leave $40 billion of profit to direct toward other ventures, such as paying down debt or, importantly, growing its recycling business from within. If Glencore managed to snag Vale-level margins, I would certainly be pleased; if it snagged BHP-level margins, which are several basis points higher, I would be ecstatic, and would consider the company possibly in the pole position among miners transitioning to metal recyclers.

Should Glencore manage to significantly increase its margins to match or exceed peers, I might consider its stock a value buy at these low valuations, as its balance sheet would actually make it worth a premium in the mining space for being rather far along in the recycling transition. As of now, though, the stock market is right to value GLNCY/GLCNF so much less than the sector average, and I would currently consider it a value trap.

Alas, as far as I can tell, the current business model and spending practices stand as a drag on the company’s financial performance, and would not be a good reason to own GLNCY/GLCNF. Indeed, it is the future opportunities and business lines that interest me regarding this company.

Risks to Thesis

Glencore has the advantage of getting into metals recycling relatively early in the mining-to-recycling transition period, outpacing more cautious peers in the mining industry like BHP and Vale. However, Glencore is not alone in being a miner and a recycler. Mining peers Rio Tinto (RIO), Anglo American (OTCQX:NGLOY) (OTCQX:AAUKF), and Eramet are also recycling metals now or in the near future. Competitive risk is real for Glencore, as these are not small firms in the mining industry, but well-established players with whom Glencore will have to compete for both recycled metal supply and recycled metal customers.

Another risk is that Glencore fails to adequately fund its recycling division so as to become as dominant a player in the recycled metals space as it is in the mining space. This would result in a relative reduction in market share for Glencore in the event that the industry, currently predominantly metal mining, is replaced by metal recycling.

Yet another risk is that in funding its recycling business, the company’s finances dip too far into the red and create solvency problems, or at best require capital injections at the probable expense of shareholders. This is not an unlikely scenario, as Glencore’s finances are pretty precarious compared to its peers. A related and more bullish risk is that Glencore’s finances improve significantly within the next few years, enabling it to direct more profit toward growing its recycling business and growing it without putting the balance sheet at risk.

Finally, there is the risk that recycling is not the successor to mining, either due to not being cost effective or profitable at scale, or for other reasons. In this case, Glencore’s efforts to engage in more recycling are unnecessary, and it would have sacrificed its ability to direct its efforts toward other, more lucrative projects for nothing. All of these risks would reduce Glencore’s attractiveness in the long term. This risk is the least likely to pan out in my opinion, since there is a limited amount of metal to mine in the world, thus necessitating some type of closed-loop network of metals in the future. Still, it is a risk worth keeping in mind.

Conclusion

Glencore is a mining giant caught between an excellent opportunity on one hand and a difficult financial situation on the other. The miner is still generally profitable, but it is in a precarious spot, yet it is positioned well to capitalize on a burgeoning opportunity in metals recycling, which stands to replace mining in the long term.

Ultimately, balancing Glencore’s low margins and poor spending habits against the future recycling opportunity, the company isn’t a clear winner just yet. I rate Glencore’s shares a hold for long-term investors interested in mining and metals recycling. Glencore and its competitors should be watched closely, in terms of both the financial picture and each company’s performance, as recycling ramps up in the mining space. Time will tell whether Glencore or others win big in the end.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")