sinology/Moment via Getty Images

My thesis

ASM International NV (OTCQX:ASMIY) is the market leader in Atomic Layer Deposition, which is the most advanced technology enabling the transition toward sub-3 nm semiconductors. Foundry leaders will significantly increase their CAPEX spending starting in 2024 toward new transistor geometries, namely GAA, where ALD technology is needed. I expect ASM to fully benefit from that trend, fueled by the expansion of generative AI requiring more advanced logic chips and memories. My DCF indicates upside potential. To me, it’s a Strong Buy.

Investment overview

ASM focuses on atomic deposition on wafers. In particular, it is a leader with more than 55% market share in Atomic Layer Deposition (ALD). This technology is essential for manufacturing high-end chips and accounts for half of its equipment revenues. The company has recently gained momentum in Silicon Epitaxy and entered the fast-growing Silicon Carbide market thanks to the recent acquisition of LPE in 2022. Finally, it sells vertical Furnaces and PECVD equipment. As its clients are mainly foundries, its customer pool is concentrated, with the top 3 largest clients accounting for 60% of its FY22 revenues and the top 10 close to 80%. ASM owns 25% of ASM Pacific, a firm operating in the semiconductor back-end, providing assembly and packaging services. ASM International was founded in 1968 with its headquarters located in the Netherlands.

ASM

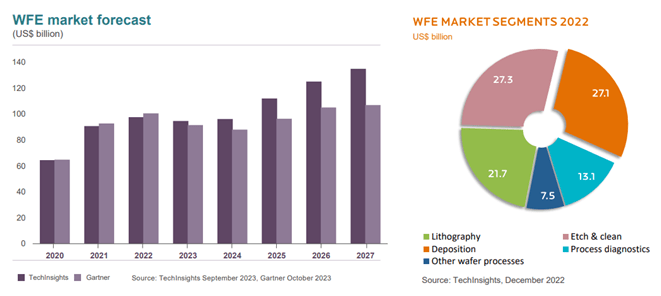

After a disappointing 2023 year, the wafer equipment market is expected to show signs of rebound, especially in the high-end segment. As can be seen in the picture below, Gartner expects a broader recovery by 2025 and onward. ASM operates in the deposition market, representing a fourth of the Wafer Equipment Market. From 2016 to 2022, ASM managed to outgrow the WFE market by a factor of two. Going forward, the management sees this trend to reach 3X.

ASM

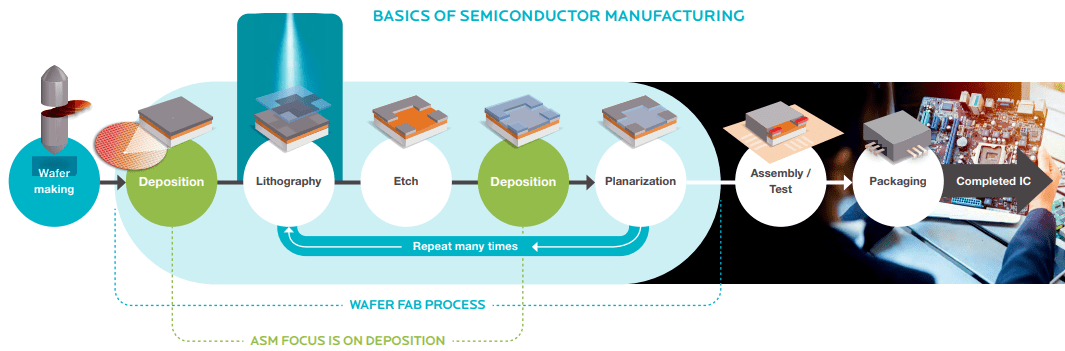

Deposition is an important step of the semiconductor manufacturing process, as can be seen below, and requires several iterations.

ASM

There are three main techniques of atom deposition.

Physical Vapor Deposition (PVD) utilizes a process in which the material changes from a condensed phase to a vapor phase and then back to a thin film condensed phase. PVD is the largest and most mature market with a size close to $21bn, more than two-thirds of the total Deposition market ($27bn), and is growing at a mid-single-digit pace. ASM is not present in this market.

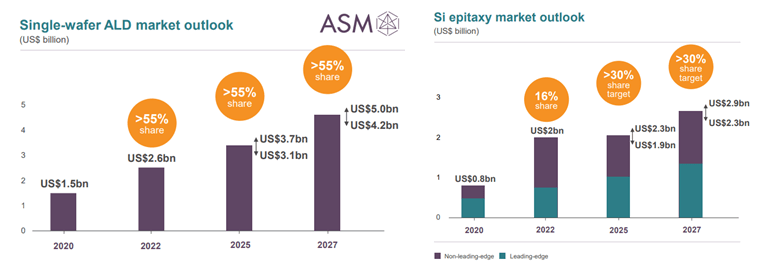

Epitaxy method grows monocrystalline films on a surface and is a fast-growing market. As can be seen in the following picture, ASM is rapidly growing its market share in Silicon Epitaxy. Also, ASM has recently strengthened its Silicon Carbide Epitaxy portfolio: I will come to that point later.

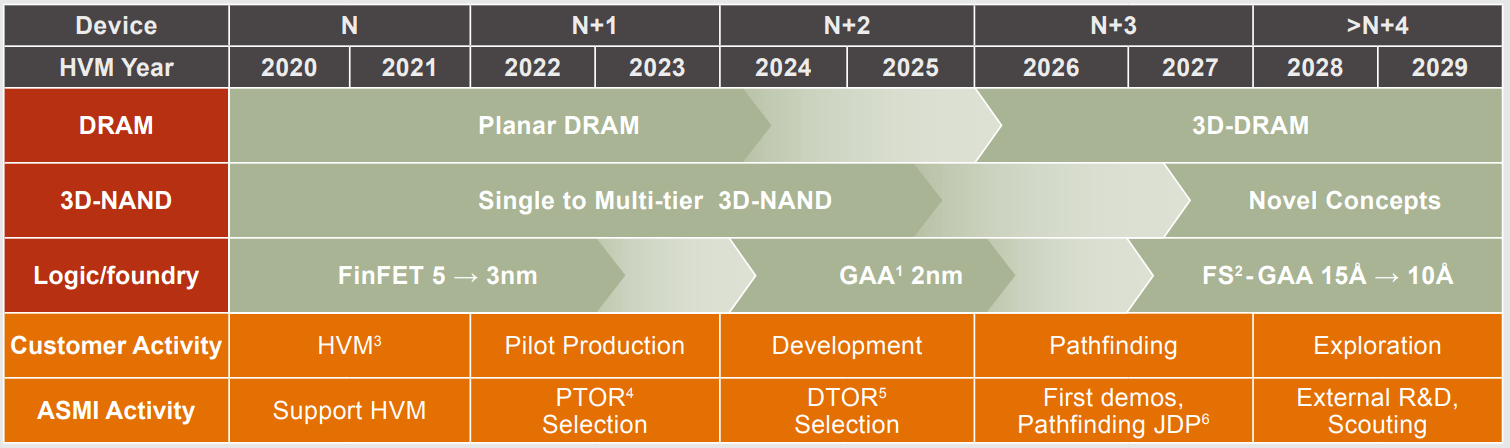

Chemical Vapor Deposition CVD utilizes a gaseous phase in order to deposit thin firm on a given surface. Several technologies use the CVD technique. ASM is exposed to the PE-CVD (Plasma Enhanced Chemical Vapor Deposition) that benefits from a better purity can use more substrates, and operates at lower temperatures than conventional CVD. Finally, the most promising sub-field is the ALD. Atomic Layer Deposition allows the deposition of thin films, atom by atom, on silicon wafers. It delivers atomic-scale thickness layers, high-quality deposition film properties, and large-area uniformity. Such precision enables the use of materials that could not previously be considered, and develop 3D structures vital to the future of electronics, such as GAA transistors. ASM management expects the GAA transition to begin in 2024 and sees the total addressable market to nearly double by 2027 (CAGR above 40%). Tokyo Electron (OTCPK:TOELF) and Applied Materials (AMAT) are ASM’s most important competitors.

ASM

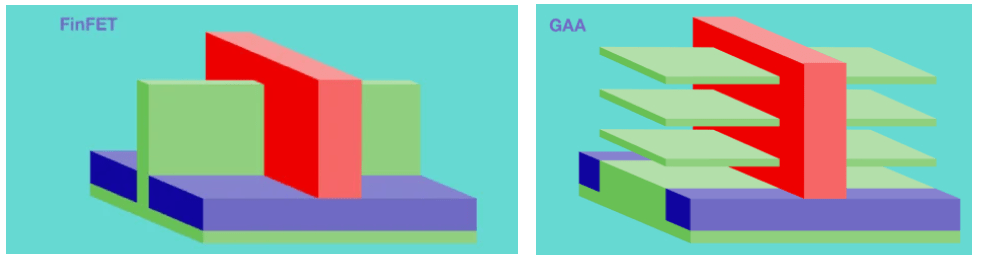

The node transition below 3nm will require more precise deposition and also a more complex one as the structure of the transistor will change from FinFet to Gate-All-Around. While Samsung already started to use the GAA architecture in 2022, Intel and TSMC are expected to follow by 2024-2025. As nodes of high-performance computing semiconductors continue to shrink in size, from the nanometer (10^-9m) to the Angström (10^-10m), more ALD deposition will be required as it has the best capability to cover 3D structures with complex materials.

ASM

GAA transistors have better performance, less leakage, and lower energy consumption than those designed as FinFet. It is possible as the transistor gate can be connected to the channel on all sides and is more scalable.

ASML

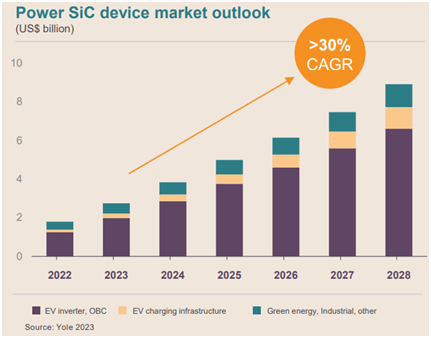

Despite near-term weakness due to a soft EV market, the SiC power market should continue its progression. Displacing Silicon atoms by Si-Carbon helps to lower energy losses within ACDC inverters and optimizes the system efficiency: SiC plays a key role in improving the electric vehicle range and Solar/Wind inverter yields. During the ASM M&A press release, the management stated that the LPE acquired company could outpace EUR100m revenues by 2023 and its end-market grow close to 30% per year, so nearly tripling by 2027. LPE’s solid experience in Epitaxial reactors for SiC could bode well for penetrating the market and cross-selling more ASM equipment.

ASM

Recent quarterly trends

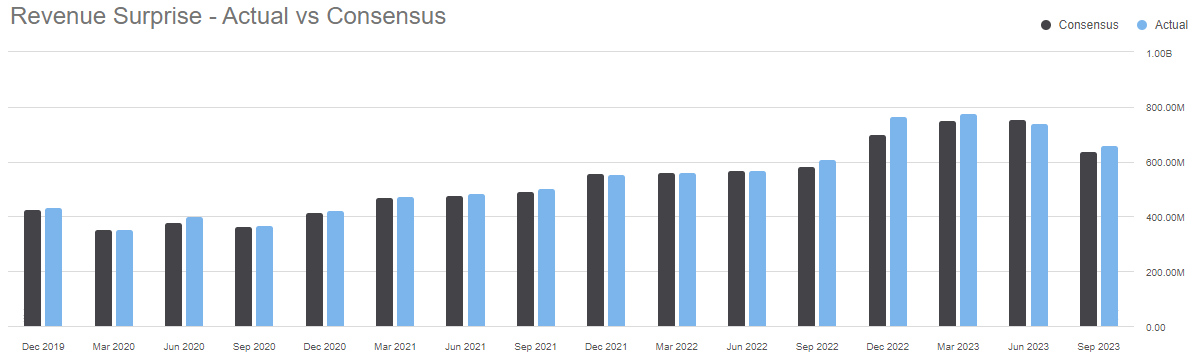

The next results will be released on February 27th. I expect the management to give an updated view on backlogs related to the GAA transition, as its peer ASML recently published an impressive outlook. During the Q3 results, ASM said: “We still expect that our customers will start to move to the gate-all-around node into high-volume manufacturing in 2025“. The firm has recently delivered a material beat relative to expectations: given the positive news flow related to generative AI: the momentum could continue. Note that AI is not just fueling the growth of logic chips, the memory segment should also see more demand: “Generative AI requires that, a lot of other applications need faster and more power-efficient DRAM.” This means more demand for ASM deposition, especially given the new generations of 3D DRAM memories.

Seeking Alpha

What valuation can we expect?

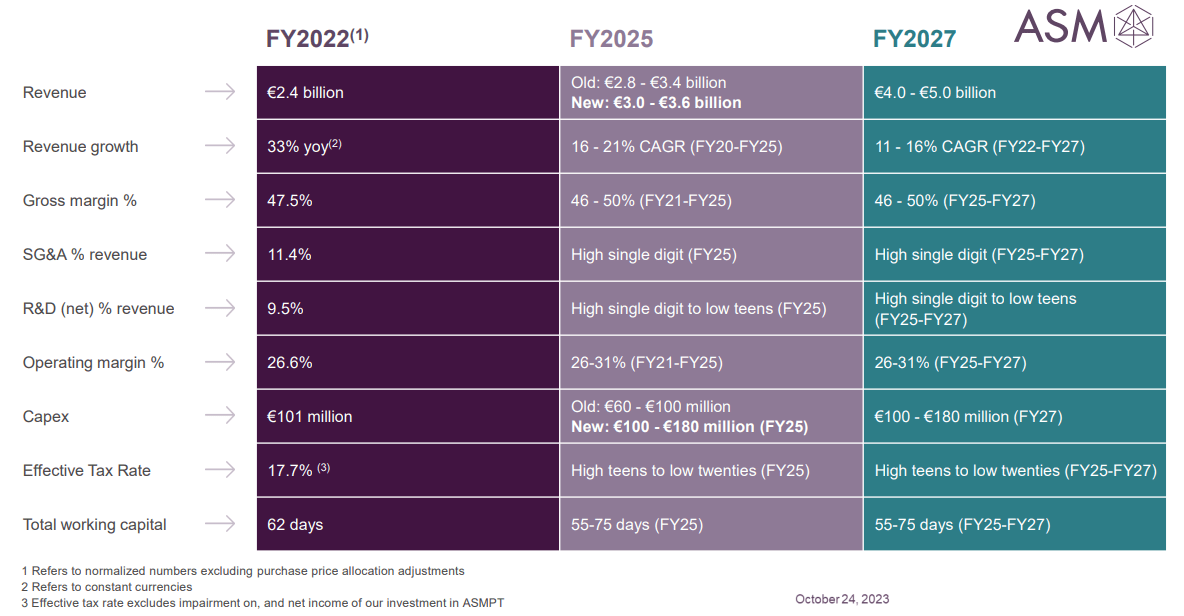

In its 2023 Investor Day, ASM highlighted new medium-term targets.

ASM

ASM’s solid track record makes me confident to use the high range of management guidance in my valuation model. I expect revenues to grow high-double digits, close to 17% from FY22 to FY2027. Operating leverage should be limited in the short term as AMS keeps increasing its R&D to feed its growth. However, SG&A should gradually decline: “to high-single-digit percent of sales“. PP&E spending for FY2023 should be in a range of EUR150-200m, with the majority related to expanding and upgrading the infrastructure. For years FY24-27, the management said to target a range of EUR100m to EUR180m per year as expansions in Korea, the US, and Europe are planned.

Own calculations

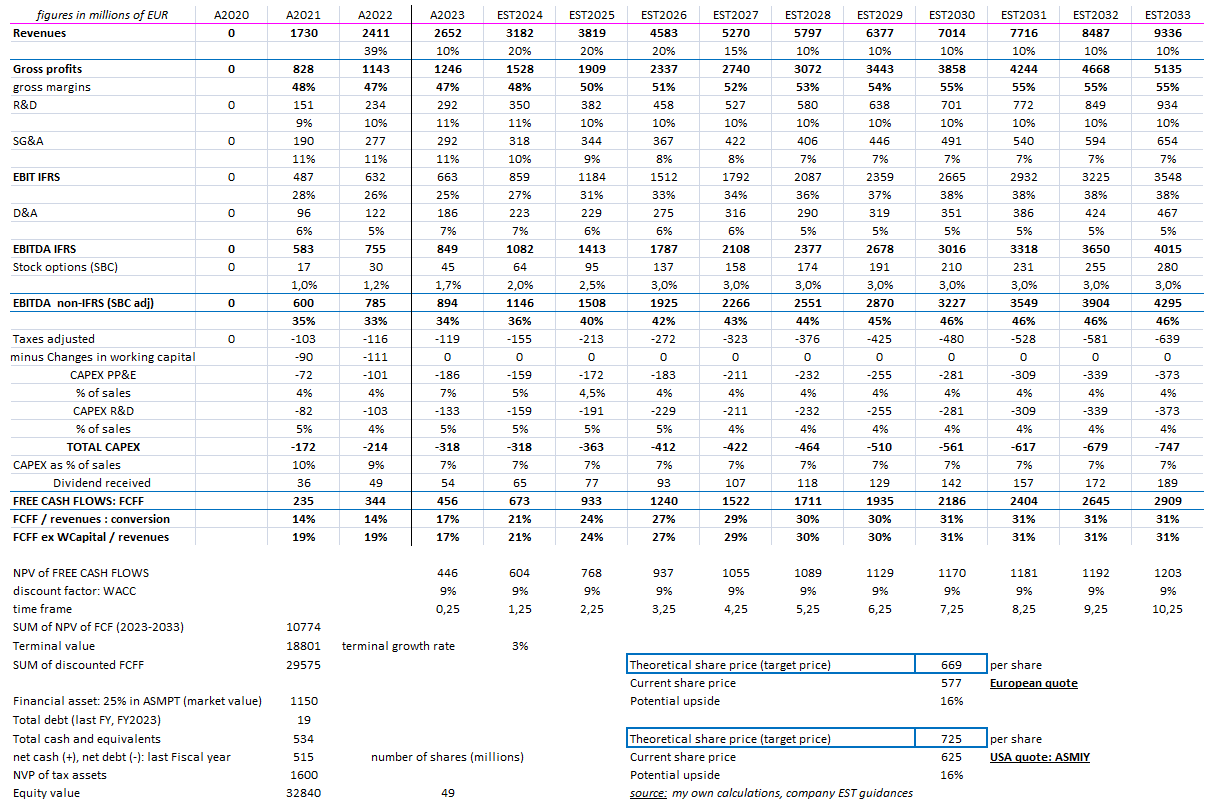

Using a WACC of 9% and my estimates (with an EUR-based risk-free rate), I get a 16% upside potential. To give more perspective, I implemented a sensitivity analysis, varying medium-term (2022-2027) growth rate and the discount rate:

Own calculations

Balance sheet analysis

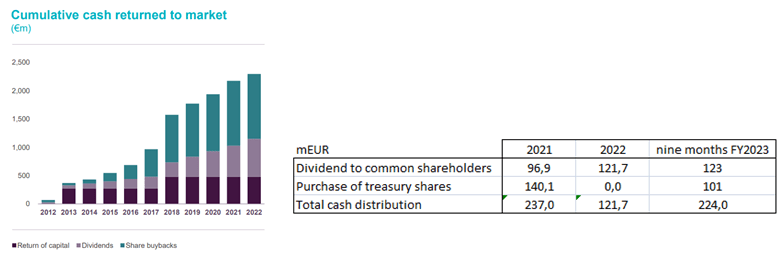

ASM has a net cash balance sheet and intends to distribute its Free Cash Flow to shareholders. I believe the company will have room for more payment as it has now to focus on its newly acquired business, limiting the need for more M&A in the near term, and the FCF generation should improve over the years. The firm stated that it has a “cash target of at least EUR600m”, which is a prudent thing to do, but implies that we will have to be patient to see a strong level of buyback.

ASM

Technical analysis

While the RSI ratio starts to be overbought, ASM stock momentum seems to accelerate upward, reaching all-time high levels. Read-cross from strong ASML results is giving confidence in AI-related equipment companies.

Seeking Alpha

Risks and opportunities

The main risk is related to the intense competition. ASM faces Tokyo Electron and Applied Materials, which have significantly larger financial resources. However, ASM is purely focused on high-end deposition and is highly innovative. It can maintain a solid market share.

The second risk I see is the lack of diversification in clients and products. ASM’s entrance into the SiC market is a good step but will take years to become material in ASM’s financials. More targeted M&A to strengthen its portfolio could create opportunities.

Conclusion

ASM seems well-placed to benefit from the transition toward lower geometries in semiconductor chips and memories. The company’s growth profile should accelerate in 2025, allowing for a solid operating leverage. The current market valuation is not that expensive for such a qualitative growth trajectory. I rate ASM as a Strong Buy.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")