SOPA Images/LightRocket via Getty Images

Introduction

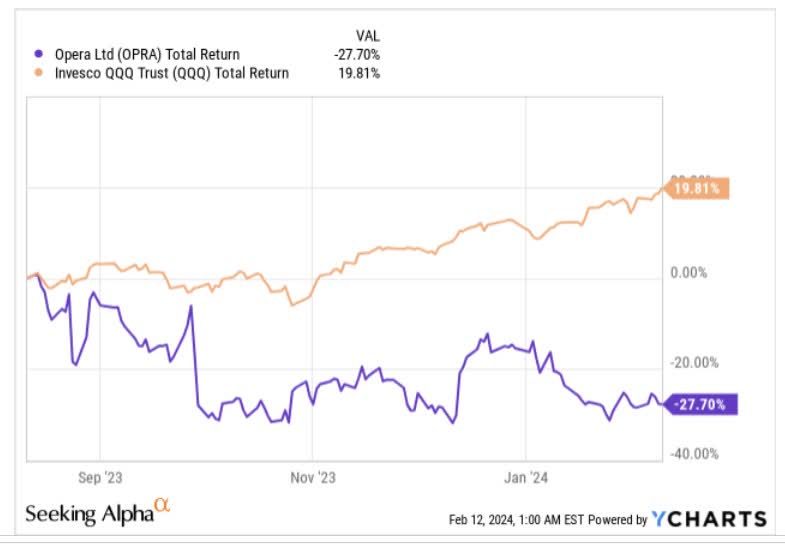

Opera Limited (NASDAQ:OPRA), a business that has been around for 27 odd years, and is primarily noted for its eponymous browser hasn’t done a great job of generating alpha for its shareholders off late. For context, over the past six months, it has grossly underperformed its tech-heavy benchmark (which has generated returns of ~20% during the corresponding period), giving up 28% of its value.

YCharts

Nonetheless, over the last three weeks, there’s been a relative lull in the OPRA counter, as investors wait for another catalyst to determine the next course of action. We could have that sometime within the next two weeks, with OPRA on course to publish its Q4 results. Do note that OPRA is yet to provide a definitive date, but Seeking Alpha and Yahoo Finance have provided two different tentative dates (16th of Feb as per the former, and 26th of Feb as per the latter). Regardless, if you’re looking to take a position ahead of the key event, here are a few things worth considering.

Earnings- Key Metrics

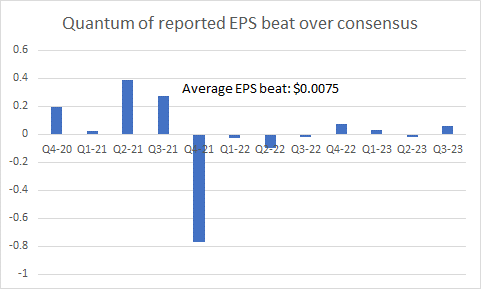

Traditionally, OPRA’s track record during earnings season has been largely mixed. For instance, if you look at how well the company has fared in meeting quarterly bottom-line estimates over the last three years, you’d note that it has fallen short on 5 separate instances (out of 12 quarters). Besides when it has beaten street estimates, the variance in cents hasn’t been overly meaningful, so much so that over 12 quarters, the average beat over expected numbers doesn’t even equate to $0.01.

Seeking Alpha

Now looking ahead to Q4, there are three key headline numbers to watch-

- an expected EPS figure of $0.24,

- an expected EBITDA figure of $23.39,

- an expected topline figure of $112m.

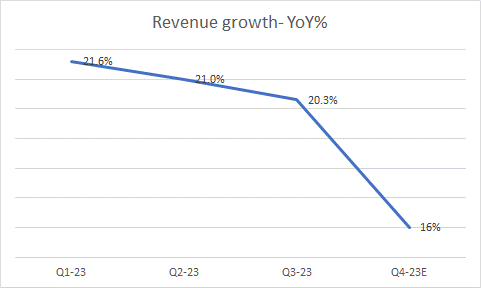

In Q3, OPRA crossed the landmark $100m revenue threshold, and the Q4 number should result in yet another record quarter but do consider that as OPRA’s revenue base gets larger, its ability to keep up stellar YoY numbers will take a hit. We’ll see that reflected quite keenly in Q4, and after delivering 11 straight quarters of 20%+ topline growth, it looks all but certain that topline growth will drop below that threshold in Q4 (16%). In fairness, the pace of OPRA’s topline has been on a declining trend all through 2023, but the drop off in Q4 is likely to be particularly pronounced with the pace of growth coming off by over 400bps (as opposed to just 60-70bps declines in the previous quarters).

Quarterly reports, Seeking Alpha

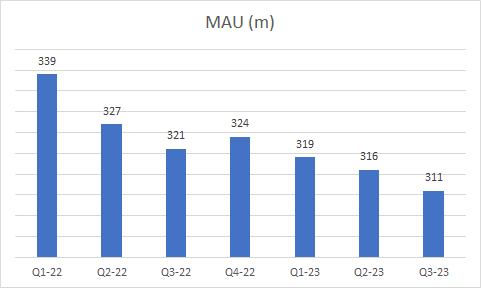

Another metric that may also cause some concerns to a fair few is the declining trend of OPRA’s monthly active users (MAU), which too has been sliding over the last 3 quarters.

Quarterly reports

Independent browser companies such as Firefox and Opera already have such low market shares (both have similar market shares of around 3% in the global browser market) and a stumbling active user count may be seen by the company’s critics as another stick to beat it with However, investors shouldn’t get too bogged down by the trajectory of this trend, as management is not too hung-up about losing low-ticket users, particularly in the emerging markets.

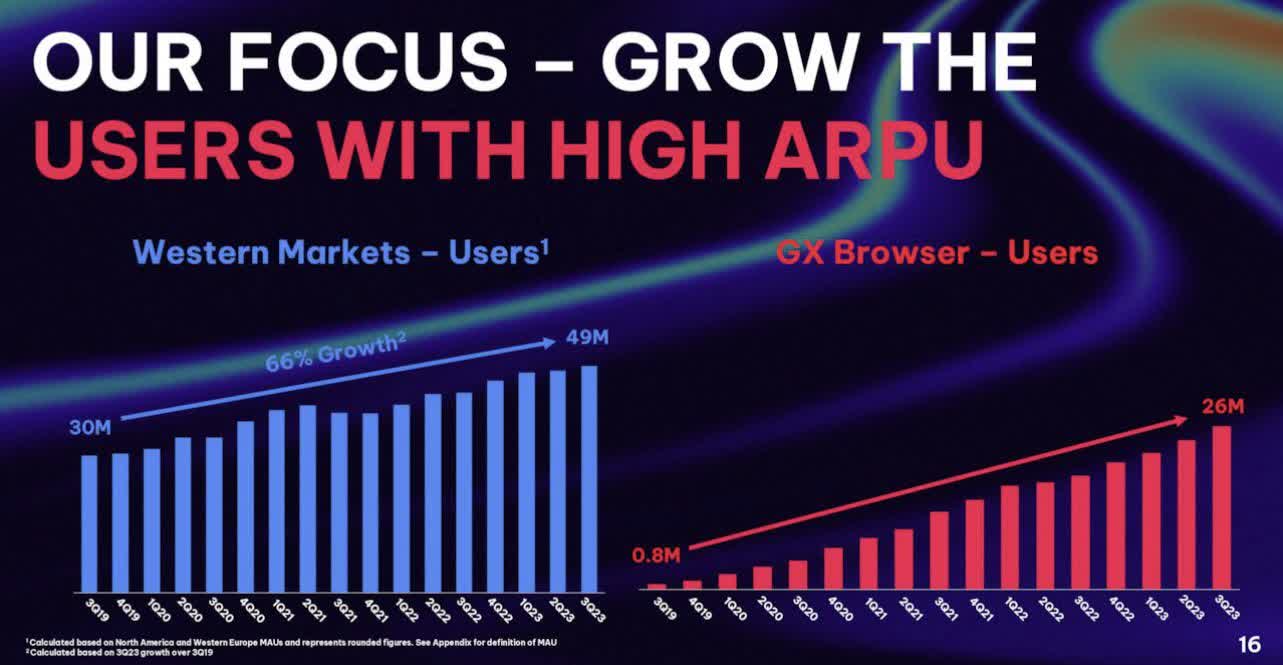

OPRA’s goal for a while now has been to cling to more lucrative users from the Western markets of North America, and Europe which are key to driving the firm’s overall ARPU (Average Revenue Per User), which we feel is the more valuable metric. As of Q3-23, users from the Western market accounted for 49m of total users. Note that over the last four years, this cohort has grown at an impressive CAGR of 66%, and we think the sky is the limit here, as they currently only account for 16% of OPRA’s total user base.

Investor Presentation

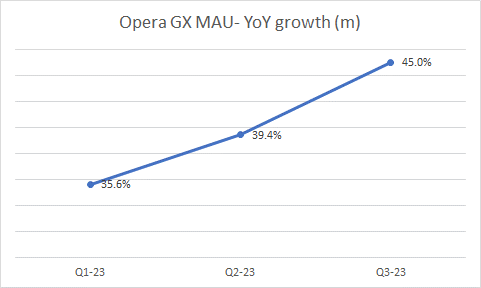

OPRA is also in the midst of developing a name in the gaming ecosystem, and the growing clout of Opera GX, their gaming-focused browser, is another high-value tool that should reflect well on the underlying ARPU. Investors should pay close attention to the growth rate of GX Browser users, as the annual growth here has only been expanding at outstanding YoY rates every quarter. Even though they will be up against a high base ( they had just crossed 20m users back in Q4-22), we feel the user-friendly nature of GameMaker Studio (which provides a platform for anyone to develop low-code 2D-type video games) could continue to drive traction for the user count of Opera GX.

Quarterly reports

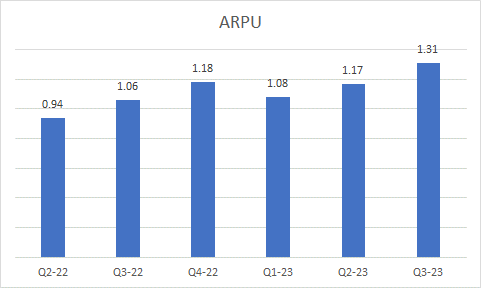

All in all, this thrust towards Western markets and gaming-centric products should continue to generate healthy sequential growth in Q4 (although a strong Q3 where the ARPU hit $1.31, growing at 12% sequentially, may result in growth within single digits on a QoQ basis). All in all, as long as OPRA is getting its users to chip in with more revenue, we don’t think investors should fret over the declining user count.

Quarterly reports

On the EBITDA front, Q4 is not expected to be particularly stellar as the company will likely witness a step-up in marketing costs (expected spend of over $30m). All in all, after witnessing an EBITDA margin of 23.1% in Q3-23 (200bps lower on a YoY basis), the expectation is for a further drop off in the margins to 20.8% (which would imply a YoY decline of nearly 300bps).

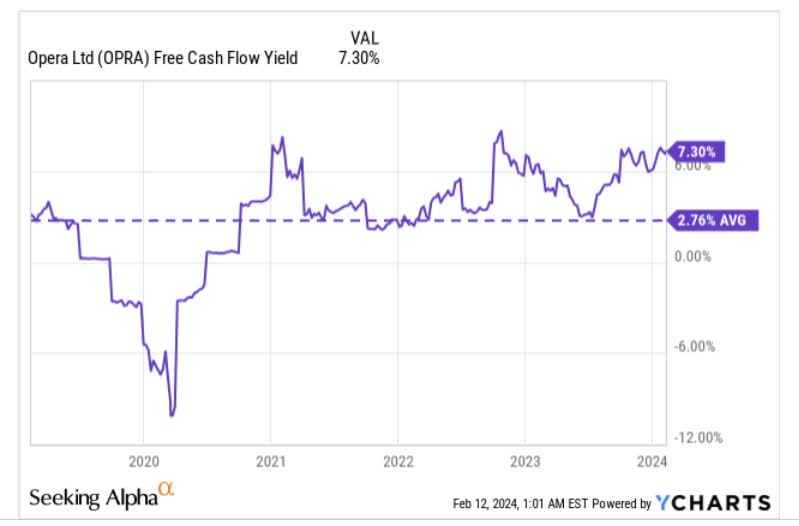

Sturdy revenue of well over $100m also means that receivables will continue to be a strong drag on operating cash flow. So OCF may likely only come in at the mid-teens (which would be in line with Q2/Q3), but even then, do consider that at current price levels, you’re still getting quite an attractive FCF yield of 7.3%, which is a good 450bps more than the stock’s historical average.

YCharts

Closing Thoughts – Why OPRA Is A Good Buy

A decent enough FCF position also opens up the opportunity to be generous with your distributions, and we’ve seen OPRA step up its pace of ADS buybacks in Q3 ($17m), after not doing much in Q1 and Q2. Note that OPRA has a $50m ADS repurchase program that will expire by March this year, so we think the Q4/Q1 pace of buybacks will be resilient enough and could support the price.

Then OPRA’s dividend profile is currently one of its most attractive facets. OPRA currently pays a semi-annual dividend of $0.4, and that translates to a remarkable yield of 7.3%. To highlight how poignant this is, do consider that out of the 190 odd application software stocks around, just 8% pay any dividends at all, and OPRA’s yield is by far, the highest on offer (the industry average yield is just a miserly 2.15%).

StockCharts.com

Then OPRA is also one of 100 odd tech or communication services stocks that make up the Nasdaq Technology Dividend Index, and the image above which captures the stock’s relative strength, highlights how this has the scope to mean-revert to the mid-point of its long-term range (the current gap is around 37%).

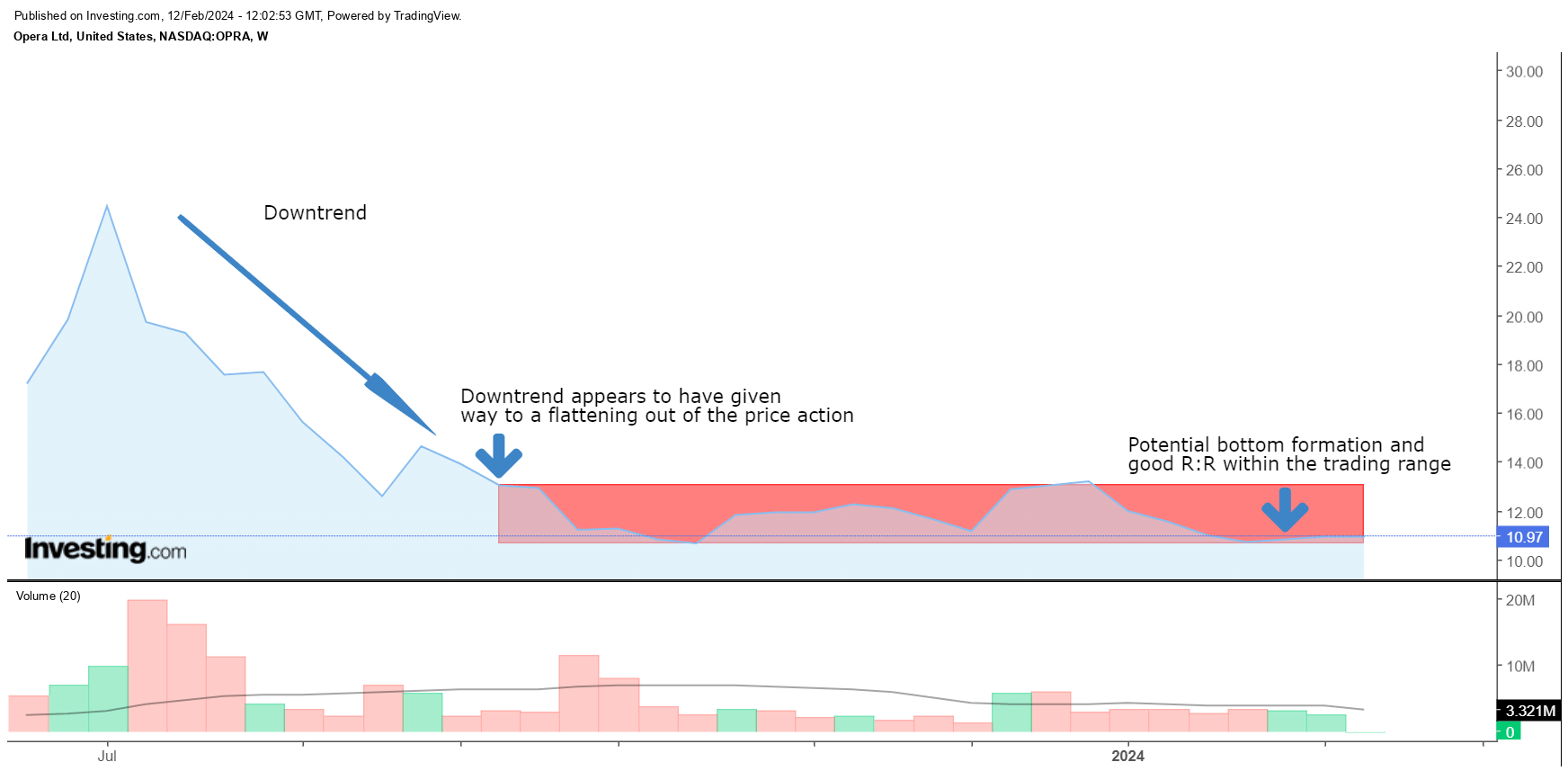

Then, if one looks at OPRA’s weekly imprints over the last 5 months, it looks like it is chopping along within the $10-$13 price band. When it drops around the $10-$11 levels, we see the price flattening out, increasing the scope of support there. Given where the price is currently perched, we think the reward to risk within the $10-$13 band looks quite attractive.

Investing.com

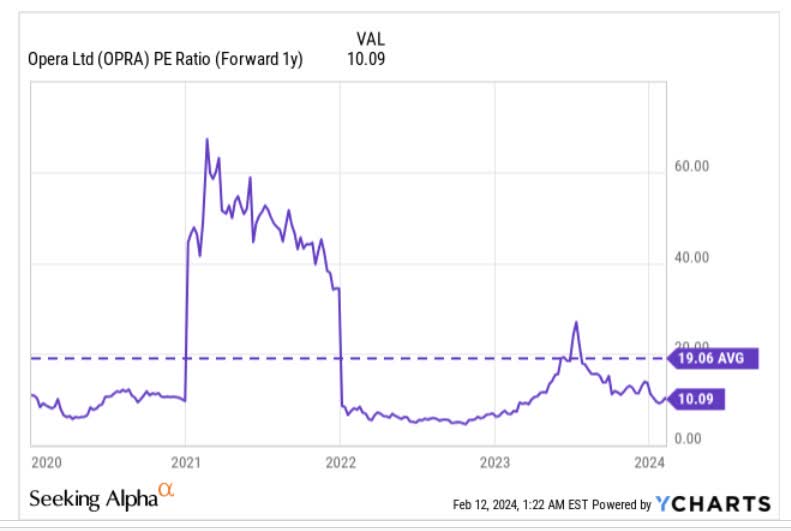

OPRA’s long case is abetted by the fact that forward valuations look exceptionally tasty, particularly in light of the earnings growth on offer. As things stand, OPRA is priced at a lowly forward P/E multiple of just 10x (based on its forecasted FY25 EPS), which represents a massive discount of 47%.

YCharts

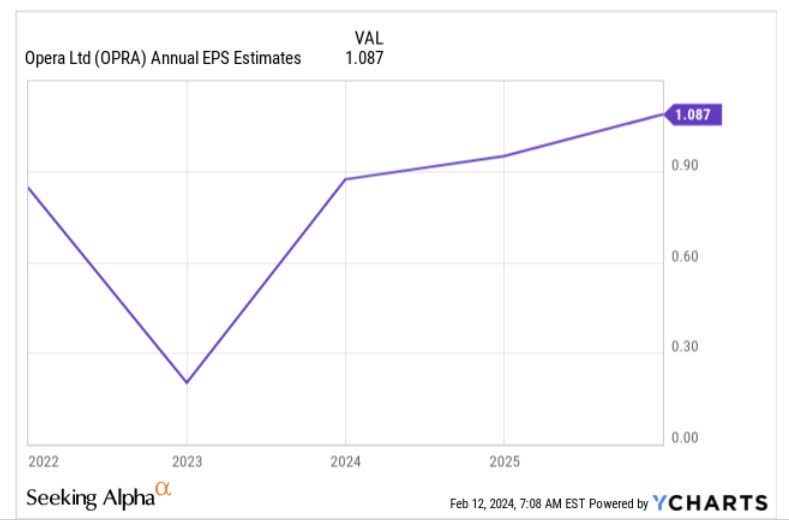

Yet also consider that at 10x P/E, you’re poised to get superior earnings CAGR of 12% through the next two years (between FY23-FY25).

YCharts

All things considered, we feel OPRA would represent a good BUY at current levels.

Q2 2024 Earnings Call Transcript")