JHVEPhoto

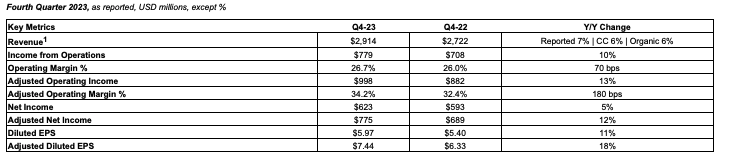

Willis Towers Watson (NASDAQ:WTW) reported Q4 2023 results on February 6, 2023 which beat consensus estimates. The company also issued strong guidance for FY 2024. WTW shares moved higher following the release and are now, as of this writing, up ~8% from where they were prior to the release.

Despite this move higher, I believe the stock remains attractive. WTW trades at a substantial discount to the broader market, despite having growth prospects which are inline or better than the broader market. I also view the company as having less cyclical risk than the broader market. Additionally, WTW trades at a discount to peers despite having similar or better growth prospects.

For these reasons, I am initiating the stock with a Buy rating.

Q4 FY2023 Results

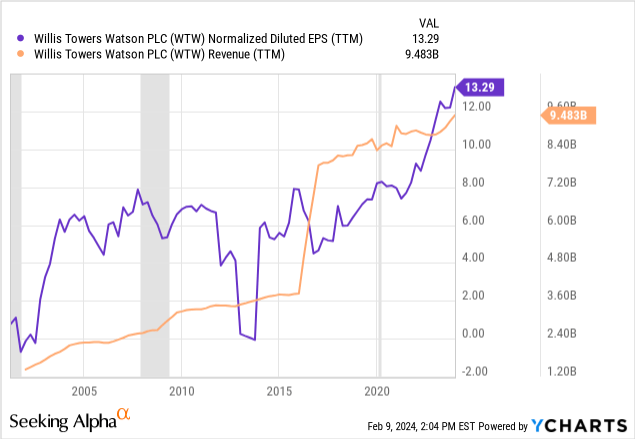

WTW reported Q4 2023 Adj. EPS of $7.44 for the quarter, which beat consensus estimates by $0.38 and represents a 18% increase from the same period a year ago. Revenue for the quarter came in at $2.9 billion, up 7% on a year-over-year basis, which slightly missed consensus estimates of $2.8 billion. For FY 2023, WTW reported Adj. EPS of $9.95 which represents an 8% increase from FY 2022 Adj. EPS. Revenue for FY 2023 came in at $9.48 billion, which represents a 7% increase from FY 2022 levels.

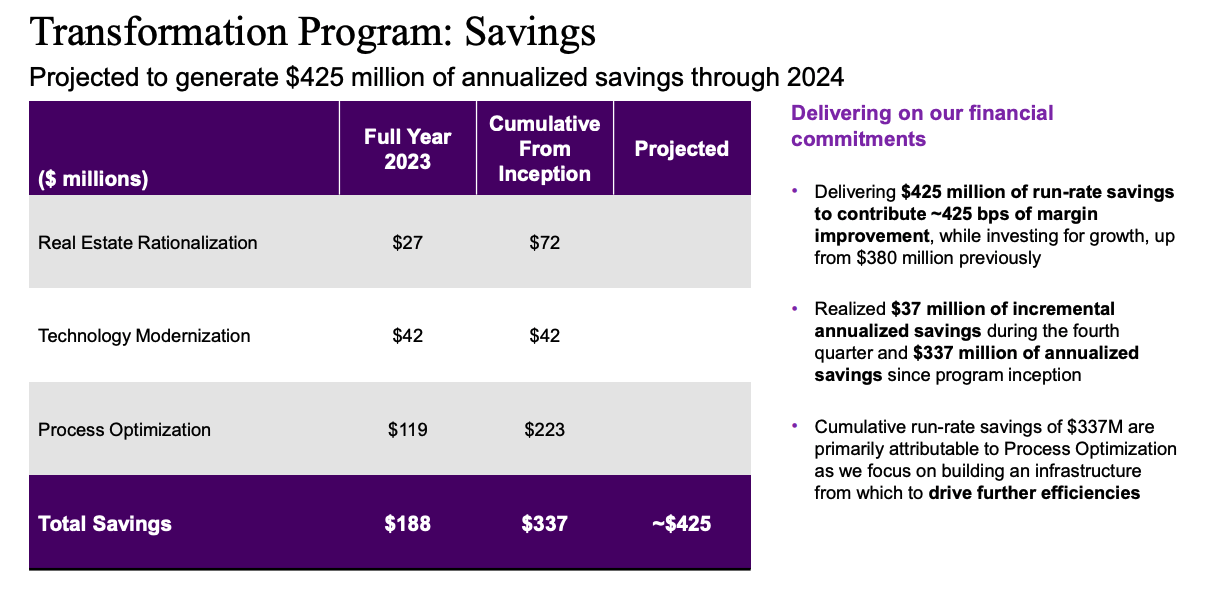

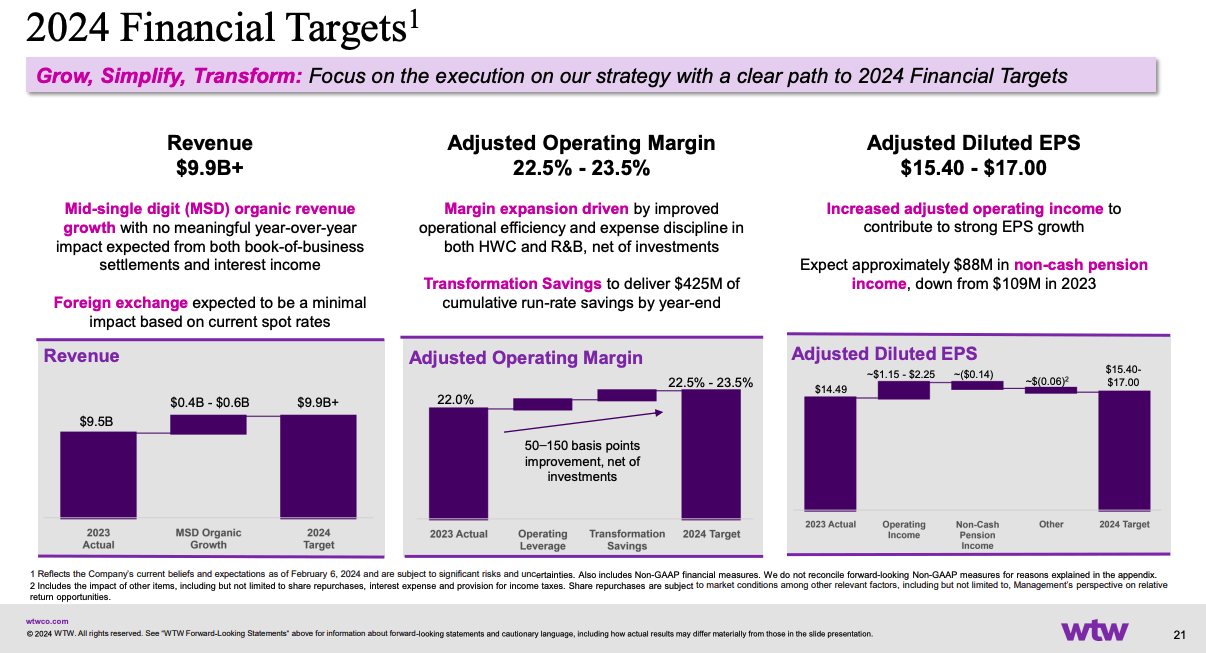

The most impressive part of the quarterly report was the 180bps increase in Adj. Operating margin for Q4 2023 from the same period a year ago. This improvement in margins comes as a result of a transformation plan the company is currently working through to drive efficiency and reduce costs. Benefits from this transformation program are expected to continue in 2024 as the company expects to realize ~$425 million in total savings, an $88 million increase from the run rate savings realized since inception of the transformation plan. The ~$425 million estimate represents an increase from prior guidance of $380 million.

WTW Q4 2023 Press Release WTW Q4 2023 Press Release WTW Q4 2023 Investor Presentation

Full-Year 2024 Outlook

WTW expects FY 2024 Adj. EPS of $15.40 – $17.00 which is broadly in line with consensus estimates which call for Adj. EPS of $16.40. Consensus estimates have increased by $0.20 following the report, as consensus estimates had previously called for FY 2024 Adj. EPS of $16.25 per share.

The estimated impact of further cost savings related to the company’s transformation plan can be seen in the projected Adj. Operating Margin improvement of 50-150 basis points.

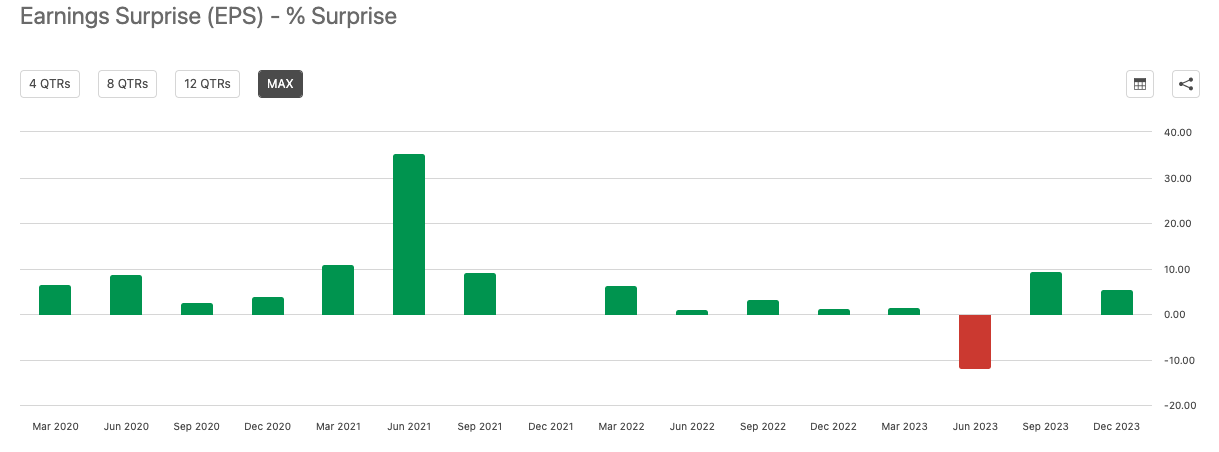

As shown by the chart below, WTW has a solid history of beating consensus estimates. Over the past 16 quarters, WTW has delivered 14 beats. Thus, I would not be surprised to see the company deliver better results than its 2024 Financial Targets suggest.

WTW Q3 2023 Investor Presentation Seeking Alpha

Defensive Business Model With Solid Growth Prospects

WTW is split into two separate business segments: Health, Wealth & Career and Risk & Broking. The Health, Wealth, & Career segment offers commercial consulting and advisory services in the employee benefits, HR, and retirement space. The Risk & Broking business provides risk advice and insurance brokerage services.

The insurance risk and brokerage business are a moderately defensive business, as companies and individuals generally need to have insurance regardless of economic conditions. However, there is some degree of cyclicality to the business, as a slowdown in economic activity results in business closures and some cuts in insurance spending. Similarly, the services provided by the Health, Wealth, & Career advisory business are necessary for most customers regardless of economic conditions, but demand tends to decrease somewhat is slower economic environments.

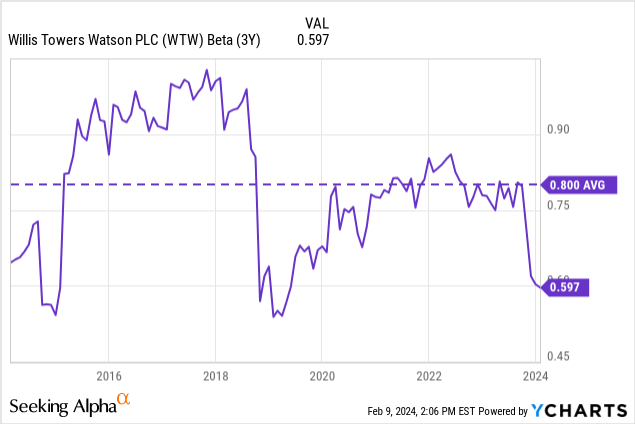

Further evidence for the relatively defensive nature of WTW’s business can be seen by the fact that the stock has historically exhibited a beta of less than 1. The stock has experienced an average beta of 0.8x over the past decade. Additionally, the company experienced very little negative financial impact during the 2020 COVID-19 recession and only moderate earnings drops (but not revenue) during the 2008 financial crisis.

In addition to being fairly defensive in nature, WTW is expected to achieve solid growth over the next few years. Consensus estimates call for the company to deliver 13%, 14.2%, and 11.6% EPS growth over the next three years. Revenue growth over the next three years is expected to be 5.4%, 5.2%, and 4.3% respectively. Thus, the EPS growth story is really about margin improvement and a continued reduction in the share count.

The margin improvement story makes sense as the company is increasingly focused on selling additional services to existing clients, as was noted on the Q3 conference call:

Our intense focus on cross-selling and making it simpler to do business with us is paying off. Across industries and services, more clients are coming to WTW for a full suite of solutions. Just to mention a few from this quarter, we had a software development firm move its global benefits consulting and brokerage work to WTW and appoint us to support their employee experience through our Embark portal and our Engage software. A major global financial corporation’s simple survey request turned into a multiyear engagement for us that includes supporting the client with attracting and retaining talent and the delivery of a fully integrated total reward solution using one of our portals. And we leveraged our existing pension actuarial and outsourcing relationships with a leading regional health system into support for a rollout of major changes to their health and benefits program, which include the creation of a temporary health and welfare service center.

As one of the leading providers of risk, insurance, and other advisory services to commercial clients, WTW is well positioned to benefit relative to smaller players which tend to have more limited advisory offerings.

Attractive Valuation Relative to Broader Market

WTW is currently trading at 16.6x FY 2024 consensus earnings. Comparably, the S&P 500 trades at ~22x consensus FY 2024 earnings. WTW is expected to grow FY 2024 EPS by 13% which is slightly more than the S&P 500 which is expected to grow earnings by ~12%. Overall, I believe WTW has similar growth prospects to the broader market over the long term. Based on this, I believe WTW should trade more in line with the broader market.

Additionally, I believe WTW’s underlying business is less cyclical than the broader market and thus could even trade at a premium.

Attractive Valuation Relative to Peers and Historical Norms

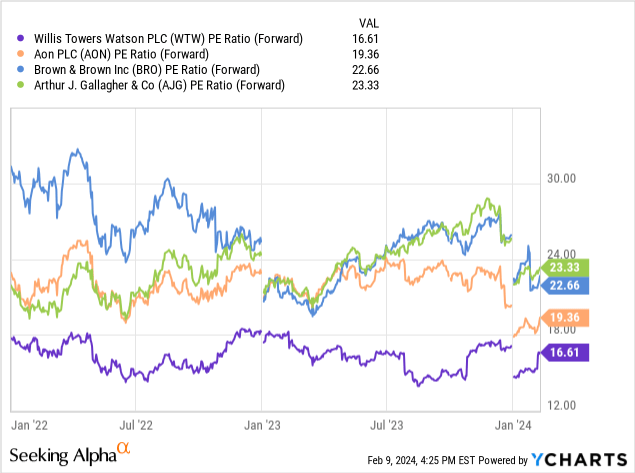

WTW is currently trading at a moderate discount to its peers, which include Aon (AON), Brown & Brown, Inc. (BRO), and Arthur J. Gallagher (AJG). WTW trades at 16.6x FY 2024 EPS. Comparably, AON, BRO, and AJG trade at 19.4x, 22.7x, and 23.3x consensus FY 2024 EPS, respectively.

Historically, as shown by the historical P/E chart below, WTW had traded mostly in line with its peer group and at times traded at a modest premium.

Over the next 3 years, WTW is projected to grow EPS at an average rate of ~13%. Comparably, AON, BRO, and AJG are expected to grow EPS at an average rate of 11.4%, 14.5%, and 13.8% respectively. Thus, broadly speaking, WTW is expected to grow EPS roughly in line with peers.

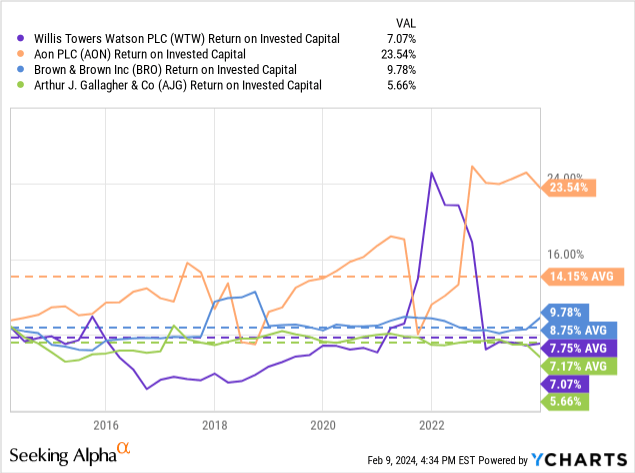

Historically, WTW has generated a ROIC which is in line with AJG and BRO but less than AON. One reason why AON has been able to generate best in class ROIC is that it has more scale than WTW, BRO, or AJG, which leads to increased efficiency.

Overall, given the similarity between WTW and its peers in terms of business and growth prospects, I do not believe there should be a significant valuation gap. Based on the average of AON, BRO, and AJG, I believe WTW could trade at ~21x FY 2024 EPS.

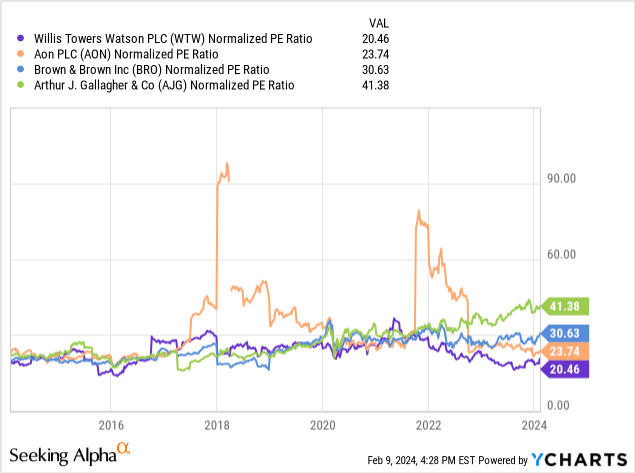

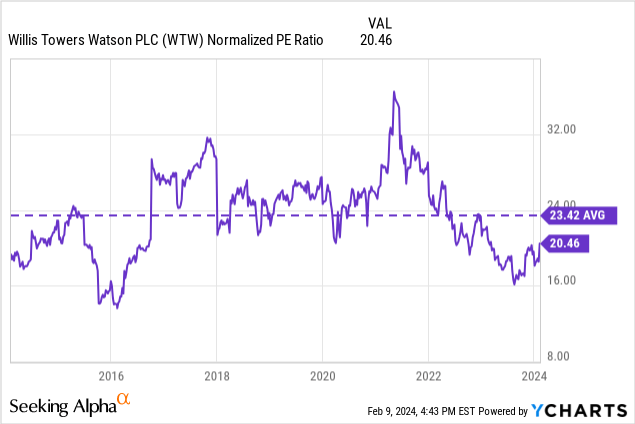

Historically, over the past 10 years, WTW has traded at an average trailing P/E ratio of 23.4x, which represents a modest premium to the stock’s current trailing P/E ratio of 20.5x. Thus, I also find WTW’s valuation attractive relative to its historical norms.

Overall, based on peer valuations and broader market valuations, I think a solid case can be made that WTW should trade at ~21x FY 2024 consensus EPS, which would put the stock at $344, a ~26% premium to the current share price. A share price of $344 would imply a trailing normalized P/E ratio of 23.7x, which is in line with historical averages.

Repurchase Program Is A Positive

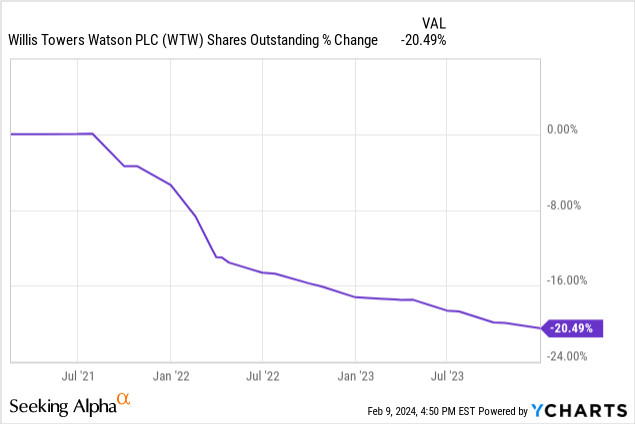

WTW has been a very aggressive repurchaser of its own shares over the past few years. As shown by the chart below, WTW has decreased its share count by more than 20% over the past 3 years.

The company completed $1 billion of repurchases during FY 2023 and currently has another $1.3 billion remaining on its authorization, which represents ~4.6% of shares outstanding based on current prices. On its Q4 earnings call, the company said it expects to repurchase $750 million of stock in 2024.

I view the buyback as an attractive use of cash given the fact that I believe the stock is undervalued at current levels. Moreover, I view buybacks favorably as they allow investors to compound their investment on a tax deferred basis and give investors more control on the timing of tax realization vs dividends.

WTW also pays a healthy dividend of $3.36 per share, which amounts to a total spend of $344 million per year, which is well less than the anticipated size of repurchases for the year.

Risks To The Bull Case

One risk to the bullish case on WTW would be a spike in interest rates. Currently, WTW has $5.2 billion in total debt and a Debt to Adj. EBITDA ratio of 2.1x. Much of the company’s debt is fixed rate in nature, which insulates the company from a near-term impact due to rising rates. However, if interest rates were to increase over the medium-term, WTW would be forced to refinance existing debt at higher interest rates, resulting in increased interest expense. Given the company’s moderate leverage, I believe such an increase in interest rates could be managed, though it may result in more of the company’s cash flow being directed towards debt repayment as opposed to share repurchases.

Another key risk to the bullish case on WTW would be a global economic slowdown. While the company’s business is less cyclical than the broader market, it does have moderate exposure to economic conditions.

The company is also exposed significantly to economic conditions outside of the U.S. WTW gets ~54% of its revenue from the U.S. and thus has significant exposure to the rest of the world. The company’s second-largest market is the U.K. which accounts for 18% of total revenue. 40% of the company’s revenue is generated in currencies other than the U.S. dollar. Thus, a rising dollar can become a near-term headwind in terms of earnings vs expectations.

Conclusion

WTW delivered solid Q3 2023 results and provided strong guidance for FY 2024. The stock has moved higher following the results, but I believe it remains undervalued.

Currently, WTW is trading at a moderate discount to the broader market, peers, and its own average historical valuation. I don’t view this discount as warranted given the strong near-term growth prospects for the company.

I am initiating the stock with a Buy rating and would consider downgrading the stock if the valuation becomes less attractive.

Q2 2024 Earnings Call Transcript")