Editor’s note: Seeking Alpha is proud to welcome Eric Brierley as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

NurPhoto/NurPhoto via Getty Images

The purpose of this article is to look at Aritzia (TSX:ATZ:CA, OTCPK:ATZAF) through the lens of a long-term investor and try and project what they will be worth in 3-4 years. As of today, the two most important drivers of growth for Aritzia are 1) their ongoing expansion into the US, and 2) the expansion of their eCommerce business. I will attempt to project how these factors will play out in the coming years and tie that into a valuation to determine if the current price is reasonable.

I believe Aritzia is a Hold at its current valuation. The opportunity to expand their store footprint into the US presents a significant opportunity, and as I will show later, if management is able to achieve their stated goals for F2027 (revenue of $3.5-$3.8B CAD, 19% adjusted EBITDA margin, and 8-10 new US stores opened per year) with this expansion, then the stock does appear undervalued. Additionally, the US stores do have some unique aspects which could make them more profitable on a per store basis. However, if management achieves the lower-end range of their stated goals, then Aritzia is likely only fairly valued, and the return potential does not adequately compensate investors for the idiosyncratic risk.

I will cover the following topics in this article:

- The unique aspects of Aritzia’s business

- Why they struggled in 2023

- Their ongoing expansion into the US and how the US market is different from Canada

- Fashion risk

- A detailed valuation using the DCF and EV/EBITDA methods under different scenarios (bull/bear/base)

Business Overview

Aritzia is a Canadian-based women’s “everyday luxury” retailer with operations in both Canada and the US. As of FQ3’24 they had 68 stores in Canada and 49 in the US with revenue starting to slightly favour the US. The company was founded in 1984 by Brian Hill who remained the CEO until 2022 when he stepped down and was replaced by current CEO Jennifer Wong, though he remains the Executive Chair of the company.

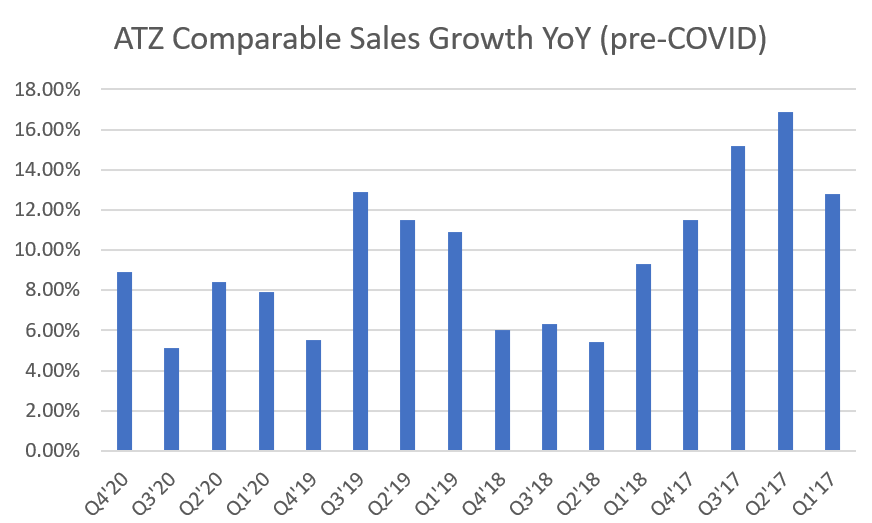

Aritzia IPO’d in 2016 and has expanded rapidly since then. From their IPO until the end of 2022 they returned ~170% (17.3% p.a.) and grew sales from $542MM CAD in F2016 to $2.2B CAD in F2023. And it wasn’t just new stores that drove this revenue growth, from Q1’17 to Q4’20 (i.e., the “pre-COVID era”), comparable stores sales growth averaged just under 10% YoY.

ATZ Comparable Sales Growth YoY (Author)

2023 Struggles

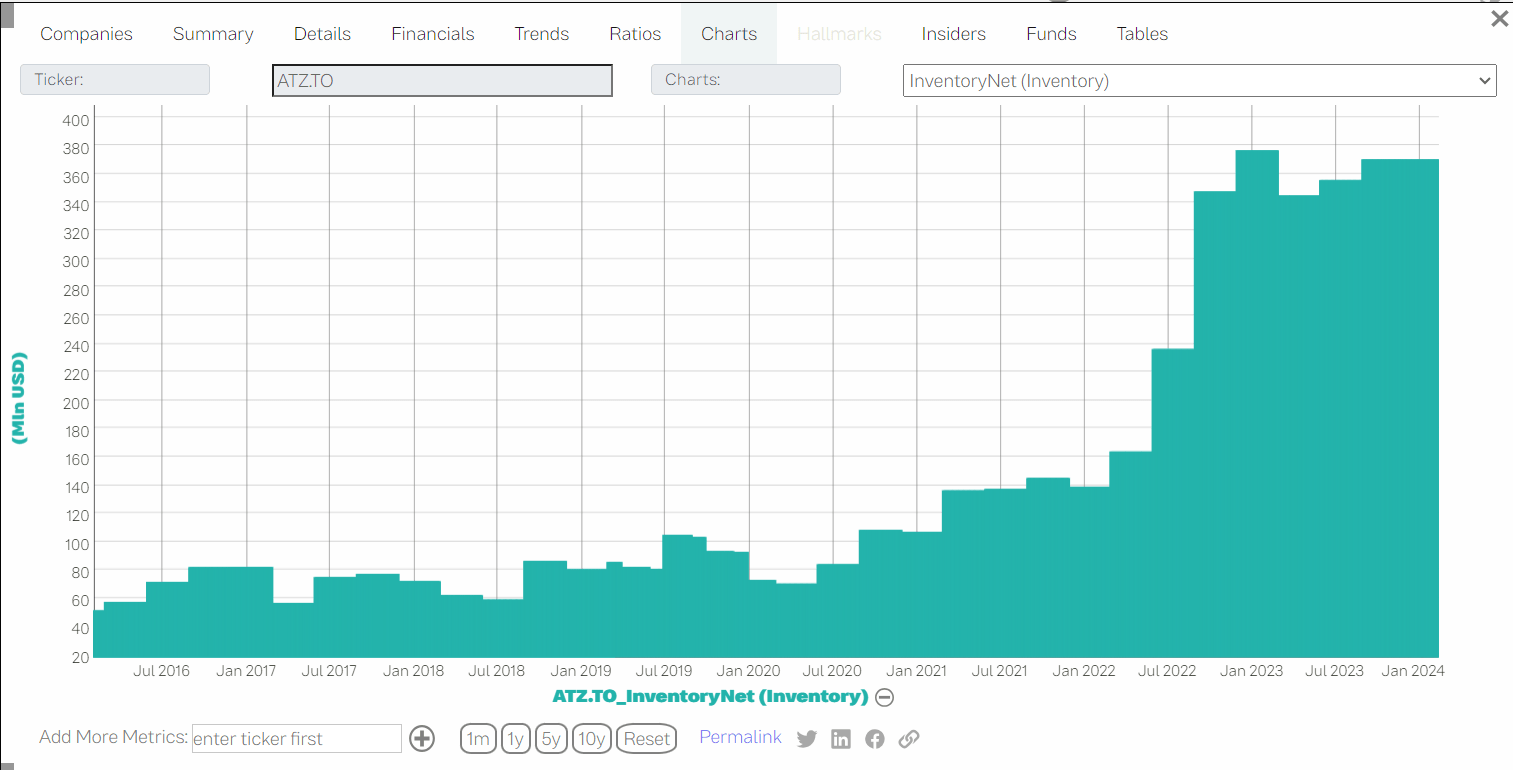

Aritzia had been firing on all cylinders since their IPO, but 2023 brought a unique storm of challenges that led to far worse than expected performance. For starters, Aritzia’s inventory balance had been elevated since mid-2022:

ATZ Historical Inventory Balance (Tickernomics)

Source : Tickernomics – Charts

Carrying a high inventory balance means your warehousing costs will increase (more staff is needed, you have to lease more space to store it, etc.), which likely also means a lower gross margin and operating margin. This was specifically referenced in their Q4’23 MD&A when their Gross Margin declined 240bps YoY:

ATZ Q4’23 Gross Margin Commentary (MD&A – Q4’23)

The same was also true for the next quarter (Q1’24) when Gross Margin declined 540bps:

ATZ Q1’24 Gross Margin Commentary (MD&A – Q1’24)

This issue was compounded by the lower-than-expected revenue and comparable sales growth throughout F2024, which they attributed to “the level of new styles in its product assortment as well as a mixed consumer environment“. Management even vaguely stated that revenue was negatively impacted by “missed opportunities” in their Q2’24 press release. This essentially means the company didn’t order products customers actually wanted, which is something they haven’t historically had issues with. However, this does highlight the key risk of investing in Aritzia, which is that they must always stay on top of fashion trends or else sales will suffer.

When these issues first came up, investors weren’t sure how long these issues would persist for. I think another less-obvious reason for their decline in 2023 was the broader sell-off in retail goods as consumers were forced to deal with rising inflation and largely stagnating wages in North America.

Aritzia then released their Q3’24 results on January 10, 2024 and performed much better than expected. They reduced their inventory balance from $467.6MM CAD in FYE’23 to $397MM CAD in Q3’24 (15% decrease) while still managing to grow revenues 2.5% Q3’24 vs Q4’23. And comparable store sales growth YoY was 0.5% when it was expected to decline. As a result, their stock price increased 35% from Jan. 8th – 12th as this demonstrated to investors that Aritzia was much closer to being the company it was pre-2023.

Looking Forward: 2024 – 2027

Aritzia is a fairly straightforward business. I think most retail investors who aren’t industry experts can learn enough about this company to get to a point where they know what needs to happen for it to be successful, and by extension the stock to do well long term.

A successful expansion into the US is they key driver of growth for this company. The US isn’t just an interesting opportunity because they can open new locations there, but the US stores actually generate far more sales. For example, in Q3’24 Aritzia had 68 stores in Canada and 49 in the US. They also generated $326M in sales from Canada and $327M from the US, which means Canadian sales per store for this quarter were $4.8MM and US sales per store were $6.67MM. The reason this is the case is 1) US stores tend to be larger (~7.5-8.0k square feet vs. ~6.0-6.5k in Canada), and 2) items are generally sold at higher price points in the US. The key insight here is that revenue growth will likely accelerate as the US expansion continues, and assuming modest growth in comparable store sales.

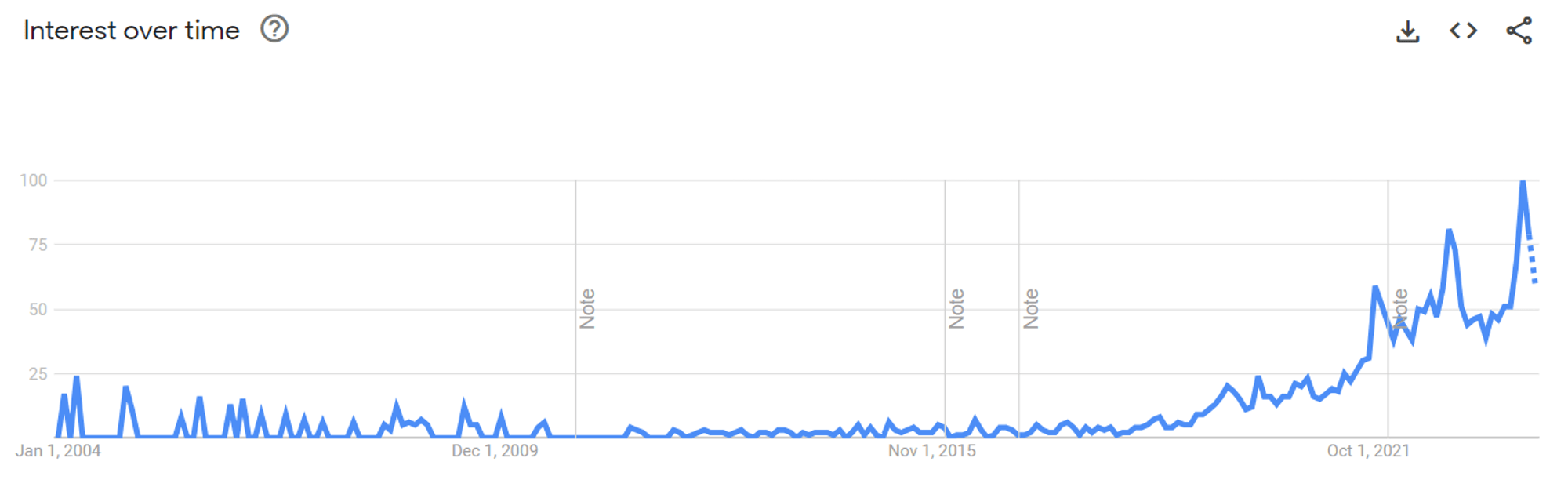

Furthermore, there’s very convincing evidence that brand awareness in the US is quite low. Analysis of Google trends data shows a reoccurring pattern where search volume for the term “Aritzia” increases substantially after a new store in opened in that area. As an example, an Aritzia location was opened in Mall of America in Minneapolis, Minnesota in August of 2019. If we look at the Google Trends traffic going back 10 years for this area, we can see a significant increase from 2019 onwards:

Aritzia Search Trends – Minneapolis (Google Trends)

If customers are searching “Aritzia” more, that more than likely corresponds with an increase in eCommerce sales. The eCommerce business is the other major pillar of growth for Aritzia. This business obviously took off during the pandemic since physical stores were forced to close for ~2 years. But over the last 4 quarters eCommerce sales as a % of total Net Revenue was 35%, and 34% the 4 quarters before that. Compare this with Lululemon where approximately 46% of their sales were direct-to-consumer in the 2022 year.

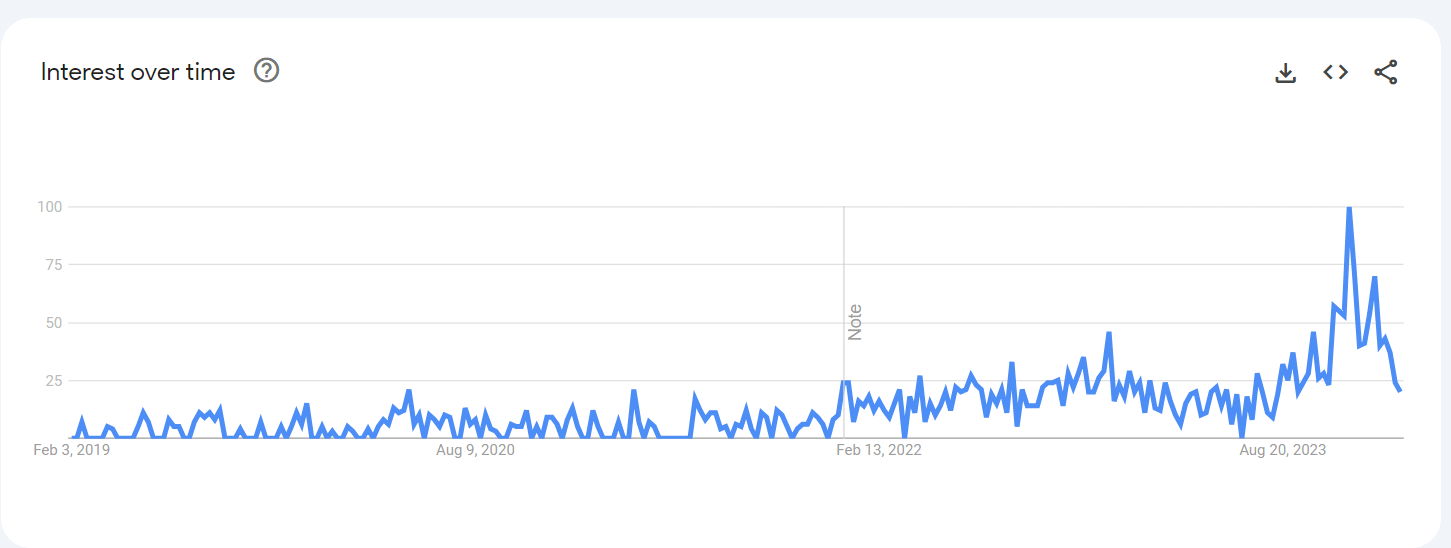

Another more recent example is the Aritzia that opened in SouthPark mall in Charlotte, North Carolina in the Fall of 2023. There was a significant spike in search volume during November and December right after the store was opened that wasn’t seen in this area in previous years:

Aritzia Search Trends – Charlotte, NC (Google Trends)

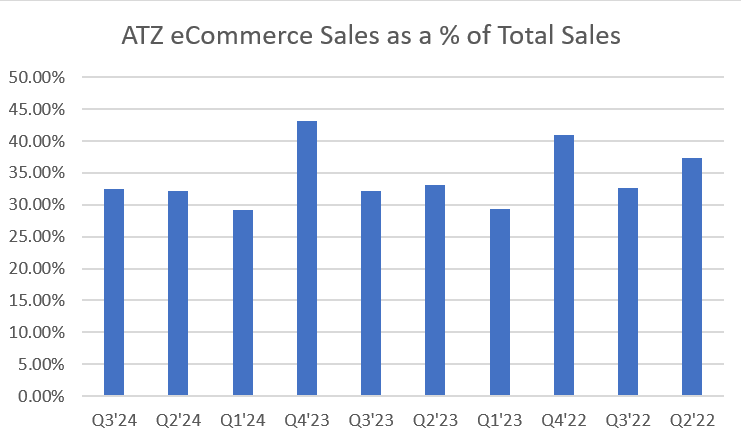

Whether management can actually execute on this remains to be seen as eCommerce sales as a % of revenue have essentially been flat 2 years.

ATZ eCommerce Sales as a % of Total Sales (Author)

In my opinion, the eCommerce business represents low hanging fruit for Aritzia. In the past they have discussed “delivering eCommerce 2.0”, which involves offering personalized product suggestions for the customer using behaviour analytics, improving site design and communication, and optimizing for different devices (phone, tablet, laptop). Management is still in the early innings of eCommerce 2.0, and although they have not released any specific guidance or goals for eCommerce, it is something to keep an eye on going forward.

Fashion Risk

If there’s one thing that 2023 told Aritzia investors it’s that they are not immune to fashion risk. Management must always keep their fingers on the market’s pulse, anticipate what styles customers will want now and in the future, and ensure they can offer those styles while still managing inventory well enough so it doesn’t hurt margins. This risk is very difficult to quantify at its surface, and there are very convincing data points that would suggest that fashion risk is low or even non-existent. For example, it is well known that roughly 80% of retail revenue at Aritzia is derived from customer that spend, on average, $5,000/year there. This signals very strong brand loyalty from a very dedicated customer base who will likely continue to purchase the new styles as they get released. Additionally, the vast majority of their revenue comes “proven sellers” as opposed to new styles. This implies that there is less pressure on management to consistently come up with new styles that customers want to drive sales volume.

While these points do indicate that fashion risk is not necessarily high, they don’t mean it doesn’t exist. Even if we assume that 80-90% of total sales come from these “proven sellers”, that still leaves 10-20% susceptible to fashion risk which is notorious for being unpredictable. Such a risk resurfacing again would send a strong signal to investors that them succeeding in the US market is no guarantee.

Valuation

I’m going to use two different methods and 3 different scenarios (bull case, base case, and bear case) to give you a wholistic view of how this company is likely to perform over the next 3-4 years, and what returns we could expect under the different scenarios. Using multiple different scenarios allows us to understand how we would expect Aritzia stock to perform under varying levels of success for their US expansion. Since we don’t know how well that expansion will go yet, these scenarios can serve as a benchmark for evaluating their underlying business performance going forward. Additionally, using the EV/EBITDA method allows us to understand what their stock price will by in 3-4 years time, and what returns we could expect under the different scenarios, while the DCF method helps us understand what the stock is worth today and what is a reasonable price to pay for it.

EV/EBITDA Multiple Method

Let’s start with what management has guided for. In their most recent Investor Presentation they stated that they have identified 100 potential new locations in the US, and that their goal is to open 8-10 new stores annually in the US until F2027. This implies 15-17% revenue growth per year ($3.5-$3.8B CAD total net revenue by F2027), and they also want to achieve 19% adjusted EBITDA margin by the same year.

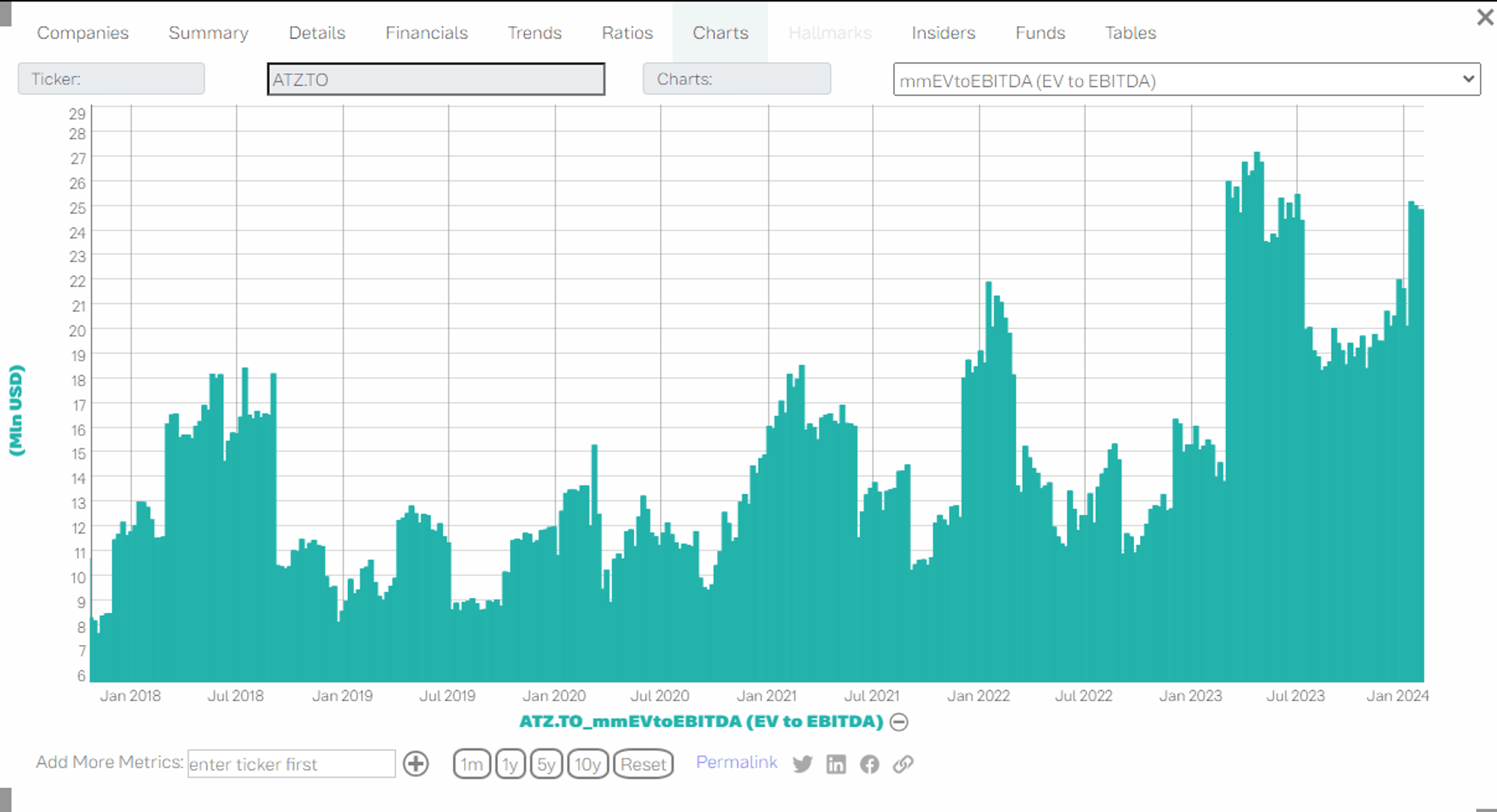

We will start by determining an appropriate terminal value multiple. Aritzia’s EV/EBITDA multiple has historically fluctuated a lot because their EBITDA is earned unevenly throughout the year (majority of their revenue and earnings come in Q3 and Q4):

ATZ EV/EBITDA Ratio (Tickernomics)

Source: Tickernomics Charts

We can see that it’s typically been in the 12.00x – 15.00x range, so to be more conservative and ensure our valuation doesn’t rely on the multiple expanding, we will use 10.00x as the exit multiple.

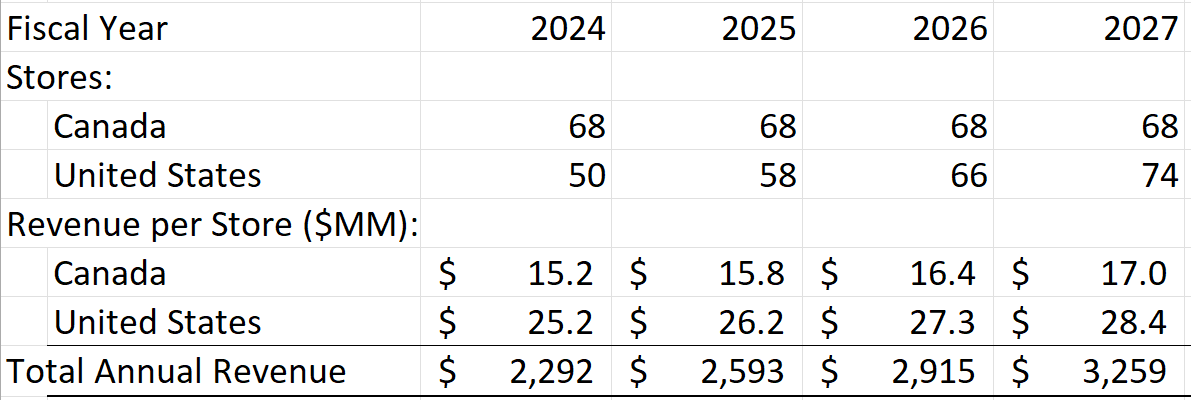

The two most important assumptions that go into this model are Revenue Growth and EBITDA margin. If we assume management successfully opens 8 new US stores per year (remember their stated goal is 8-10), and each US and Canadian store earns approximately the same level of revenue as it historically has, plus some modest growth in same store sales (4%/year, which is well below the growth rate in the “pre-COVID era”) then their revenue will look like the following:

ATZ Revenue Projections (Author)

Achieving $3.26B CAD in revenue by F2027 is below their stated goal of $3.5-$3.8B, so we can assume that this is our base case (since this is their goal and not what they’re guiding for).

As for EBITDA, we’ll need to project out their Gross Margin, SG&A expenses, and depreciation and amortization. Since depreciation and amortization are included in their SG&A, we’ll have the subtract these out when projecting EBITDA. Their Gross Margin was 41.6% in F2023, 43.8% in F2022, 36.3% in F2021, and 41.1% in F2020.

F2021 was when the majority of their stores were closed, so I would consider that an anomaly year, so let’s use 41% for our projections.

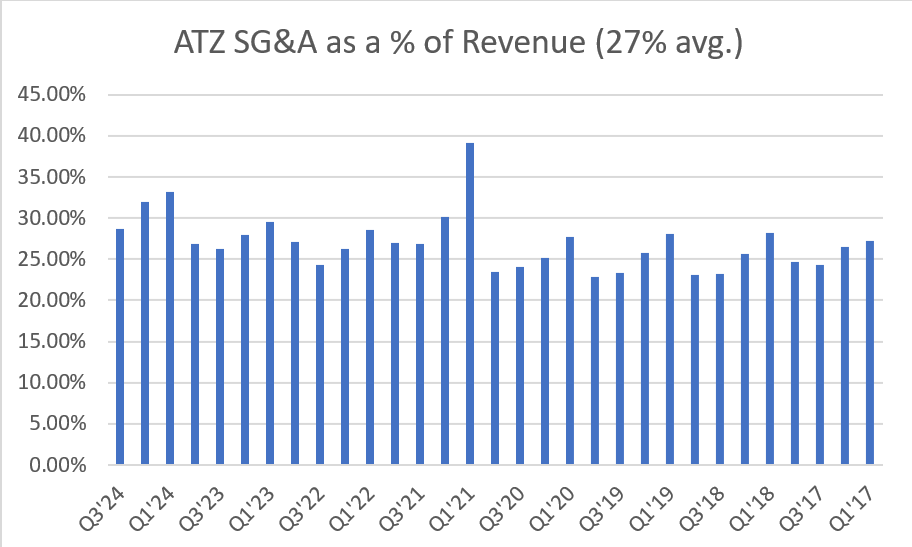

SG&A expenses have averaged ~27% of revenue since Aritzia IPO’d:

ATZ SG&A Expenses as a % of Revenue (Author)

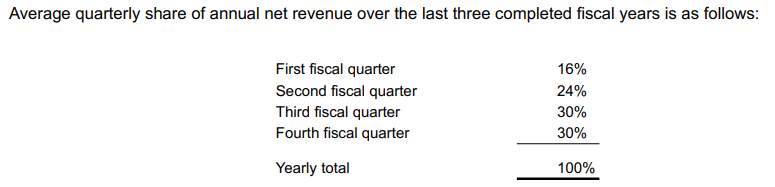

We can see a consistent pattern where Aritzia’s SG&A expenses are higher in Q1 and Q2 of each year. This is simply because they earn the majority of their revenue later in the year:

Revenue Earned by Quarter (ATZ Q3’24 MD&A)

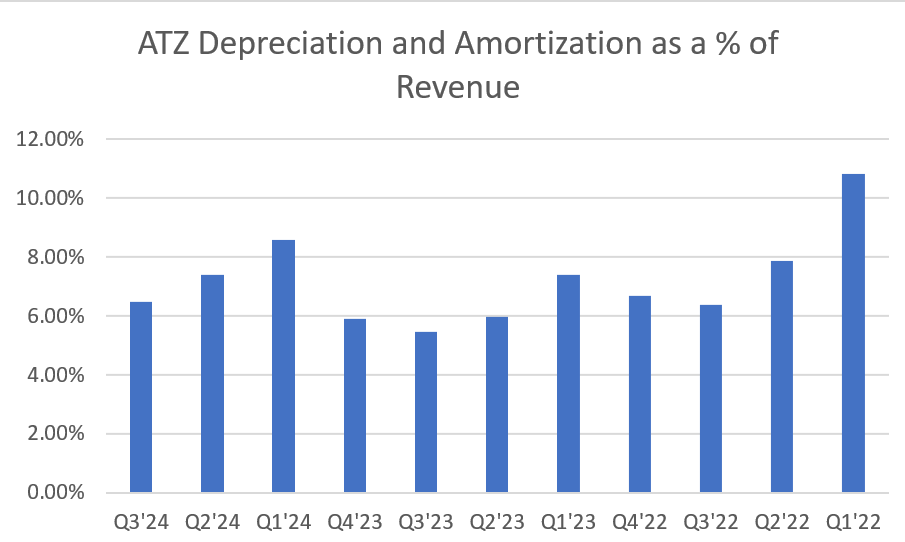

Depreciation and amortization has consistently been ~6.5% of revenue on an annualized basis since revenue has normalized after the lockdown measures were lifted:

ATZ Depreciation and Amortization as a % of Revenue (Author)

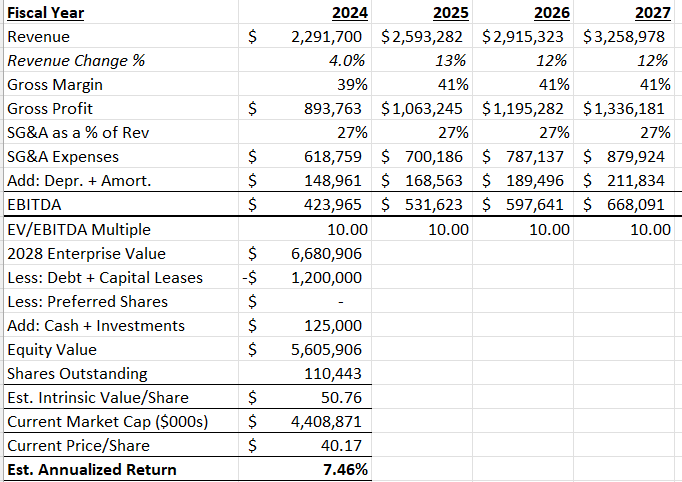

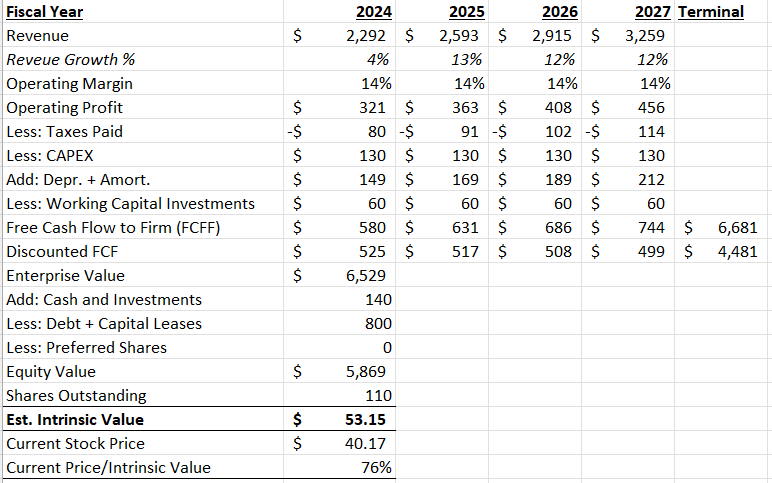

When we put it all together, our base case looks like this:

EV/EBITDA Base Case (Author)

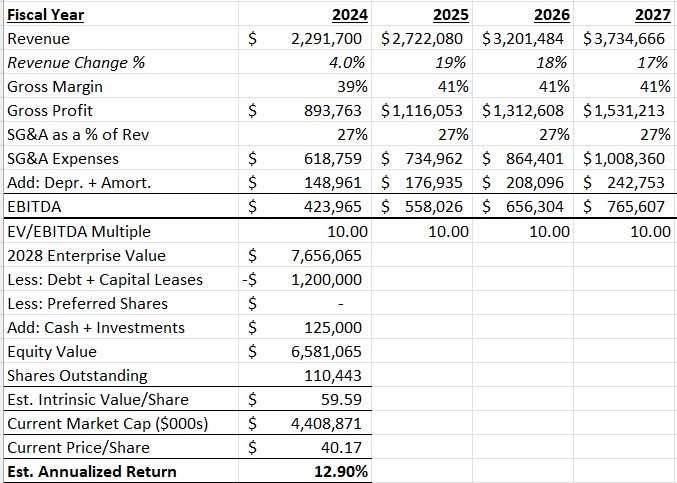

This tells us that if Aritzia can hit these targets, we should expect a stock price of ~$50 by F2027 (May of 2027), which implies ~7.5% annualized returns.

For our bull case, let’s assume they can open 10 new US stores per year and comparable sales growth is 7%/year. In this case, they would reach $3.73B CAD in revenue by F2027 (higher end of their stated goal) and our estimated future stock price is ~$60/share:

EV/EBITDA Bull Case (Author)

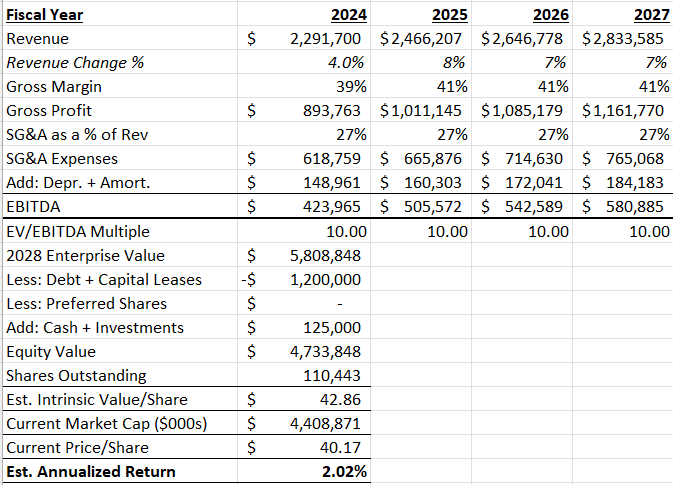

And for the bear case, let’s assume this US expansion goes terribly and they are only able to open 5 new US stores per year and comparable sales growth is only 2% (roughly in line with expected inflation):

EV/EBITDA Bear Case (Author)

The returns don’t look very good in the bear scenario. However, I would assign low probability to this scenario.

Based on the above valuation, it seems clear that investors are starting to get more optimistic that Aritzia will hit their stated store, revenue, and EBITDA goals. Given that our base case (the most likely case) projects a return that is roughly in line with the market risk premium, investors as a whole are expecting them to achieve these targets. Even our bull case only has Aritzia’s revenue being in the upper end-range of their goal with a conservative exit multiple (10.00x) and is only projecting slightly above average returns (~13%/year).

Discounted Cash Flow Method

The DCF method is slightly different since instead of trying to project what their stock price will be in 2027, we are trying to determine what it’s worth today by discounting the expected future cash flows.

Let’s use the same revenue projections as we did in our bull, bear, and base cases above.

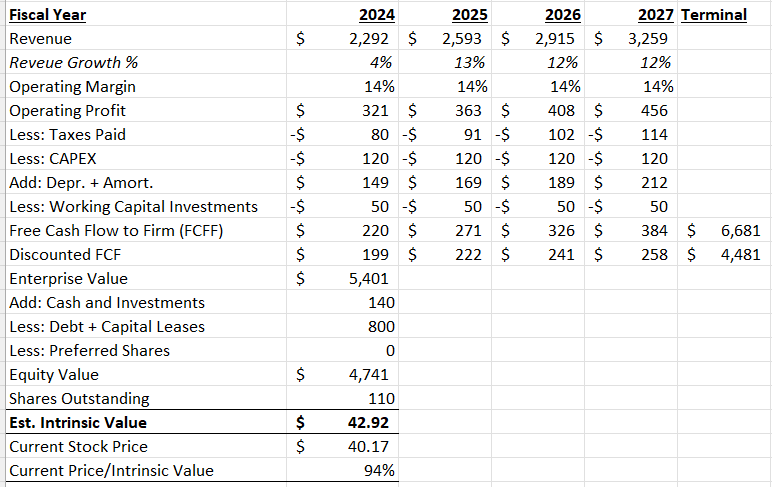

Base Case Key Assumptions

- 4% comparable store sales growth, 8 new US stores per year – low end of their stated goal of opening 8-10 new stores per year, plus modest growth in comparable store sales.

- 14% operating margin – excluding F2021 when their stores we forced to close, Aritzia’s operating margin have consistently been in the 13-15% range over the past 5 years, so I will use the mid-point.

- 27% tax rate – calculated as the average Income Tax Expense / Operating Profit F2023 – F2018, excluding F2021.

- $120MM CAD Capital expenditure – above historical average as more capital investment will be required when opening new US stores. Each new store requires $3MM net investment according to their most recent investor presentation, which includes things like furniture, store design and equipment.

- Depreciation and amortization = 6.5% of revenue. As previously stated, it has averaged this level since the lockdowns ended.

- $50MM in annual working capital investments – primarily relating to inventory purchases required to support higher selling volume with additional stores and slightly above working capital investments over the past 3 years.

- Terminal multiple (EV/EBITDA) = 10.00x (discussed above)

- WACC of 10.5% (see below)

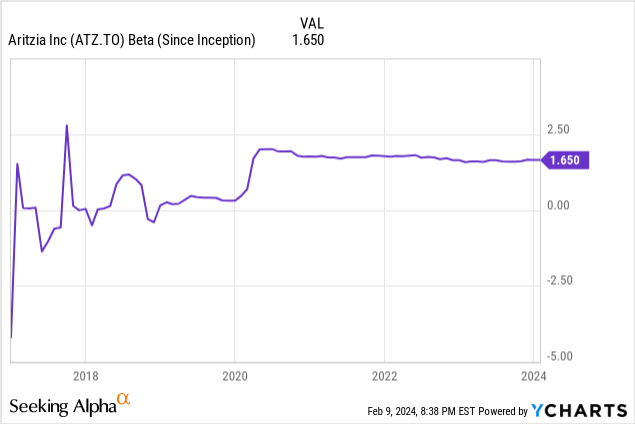

WACC is calculated using the current risk free rate (i.e., the 10-Yr US Treasury Yield) of 4.17%, ATZ’s current Beta of 1.65 (see chart below), and an 8% market risk premium. Since the company has no interest-bearing debt, the WACC will be the same as the cost of equity.

Cost of Equity = ((8%-4.17%)*1.65)+4.17% = 10.5%

When we put it all together, the base case looks like this:

DCF Base Case (Author)

Bull Case Key Assumptions

- 7% comparable store sales growth, 10 new US stores per year

- 14% operating margin – same as above

- 27% tax rate – same as above

- $130MM CAD Capital expenditure – since we are projecting 2 new stores opened each year, slightly more capital investment is necessary

- Depreciation and amortization = 6.5% of revenue – same as above

- $60MM in annual working capital investments – $10M higher than base case as more inventory is required to be purchase to support the higher projected sales volume

- WACC of 10.5% – same as above

- Terminal multiple (EV/EBITDA) = 10.00x – same as above

ATZ Bull Case (Author)

Bear Case Key Assumptions

- 2% comparable store sales growth, 5 new US stores per year (i.e., comparable store growth is roughly in line with inflation, and management can only open 5 new stores per year due to less than expected demand)

- 14% operating margin – same as above

- 27% tax rate – same as above

- $100MM CAD Capital expenditure – less stores being opened means less capital investment is necessary

- Depreciation and amortization = 6.5% of revenue – same as above

- $40MM in annual working capital investments – less inventory investment needed due to lower projected sales volume

- WACC of 10.5% – same as above

- Terminal multiple (EV/EBITDA) = 10.00x – same as above

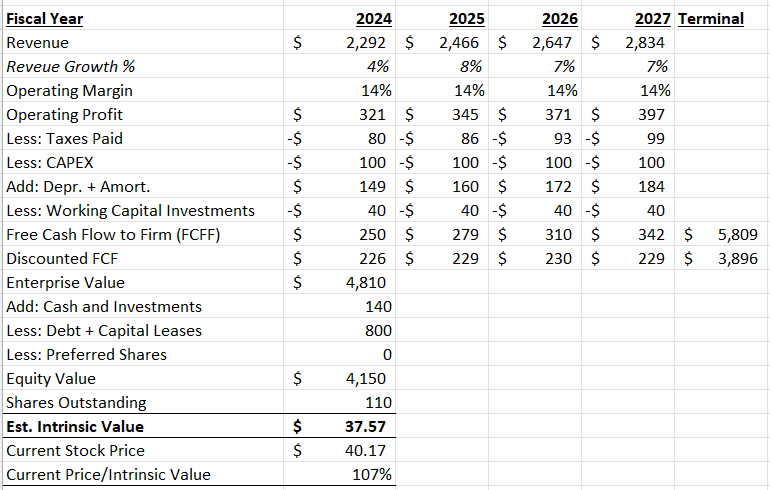

DCF Bear Case (Author)

The above analysis leads me to think Aritzia is currently slightly undervalued. I.e., worth about $42/share and returns over the next 3-4 years would be in the 7-10% range.

Concluding Thoughts

As mentioned earlier, fashion risk is the most prevalent risk facing this company. This is a consumer-oriented market where demand is extremely fickle, and their expansion prospects depend on them successfully gaining market share in a hyper-competitive US market. It’s no easy task and there’s no guarantee future payback periods were remain constant.

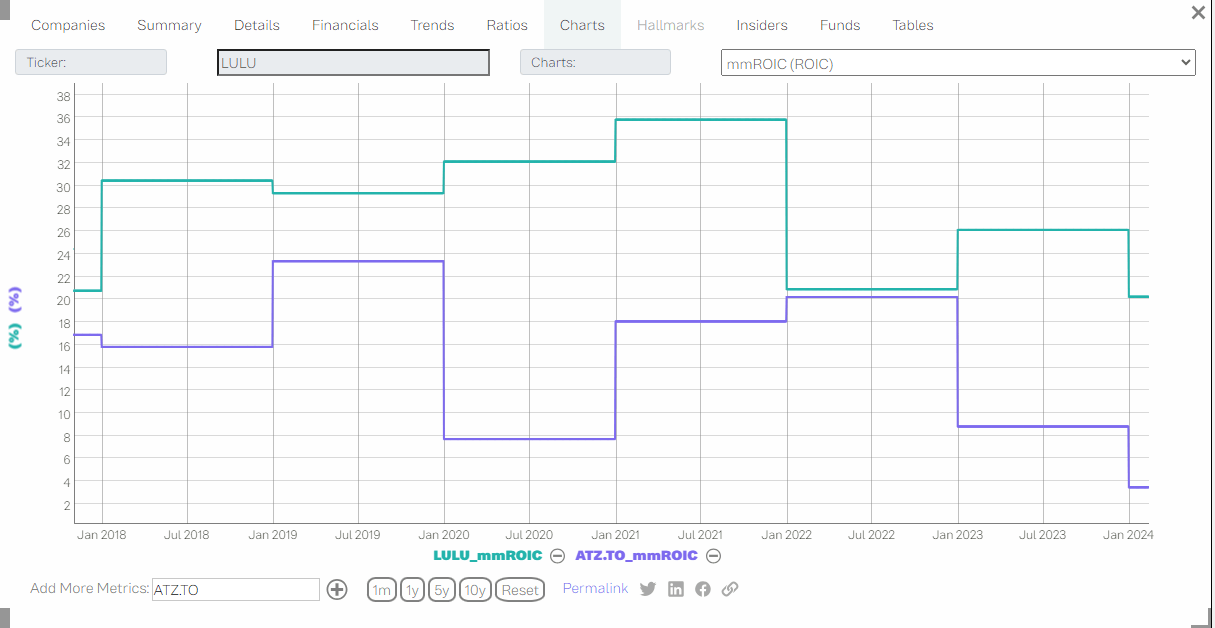

There are certain companies that exist that have an ability to command strong brand loyalty as they grow their business, which makes them less vulnerable to fashion risk and management doesn’t need to constantly keep their fingers on the pulse of the consumer or risk losing them. Lululemon is an example, they are comparable to ATZ in the sense they are a Canadian-based clothing retailer, but their niche product design is inherently unique and specialized to them, this is evident in their best in class ROIC which has been consistently higher than ATZ:

ATZ vs LULU – ROIC (Tickernomics)

ATZ is far cheaper (currently 41 P/E versus LULU with 58). Part of that reason is you assume some level of fashion risk investing in them because if management makes poor product decisions, demand will suffer. And unless ATZ introduces some new brand with a new and innovative design that customers love (like Lululemon did) then it will always be this way. So we need to value ATZ for what it is and not what we wish it is. The beat way for investors to mitigate such a risk in buy in at a good price.

Conclusion: Despite the growth story with Aritzia being very clear, the fashion risk cannot be overlooked. It’s difficult to assess the likelihood of success due to the unpredictable nature of fashion-oriented retail, and 2023 demonstrated to investors that this risk is real and could come up again at any point in the future. However, the low-hanging fruit that exists for them to improve their eCommerce store and continue their expansion into the US represent compelling opportunities that, if executed well, can lead to meaningful upside. My personal entry point is $30.00-$32.50/share. Thanks for reading!

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")