Marut Khobtakhob

Changes in Federal Reserve rates, and expectations thereof, lead to changes in newly-issued bonds almost immediately. It generally takes a few years for these to completely impact bond fund dividends, as funds must wait for their existing bond portfolio to mature to access new securities.

Recent Federal Reserve hikes have yet to take full effect on most bond funds, as many of these still own older, lower-yielding bonds from before the Fed hiked rates. As these mature, they should be replaced with newer, higher-yielding securities, leading to higher income and dividends for most bond funds.

Due to the above, Federal Reserve cuts might not necessarily lead to dividend cuts for most bond funds, material or otherwise. In other words, the delayed positive impact of prior hikes might cancel out the negative impact of any future hikes.

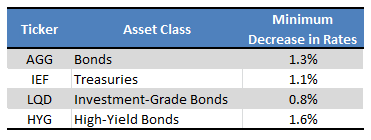

I’ll be explaining the above in more detail throughout the article. A quick table summarizing the minimum decrease in rates that would result in dividend cuts for some of the larger bond funds. These are very rough figures with lots of assumptions.

Table and Calculations by Author

Explanation and Analysis

This might be easier to explain with an example.

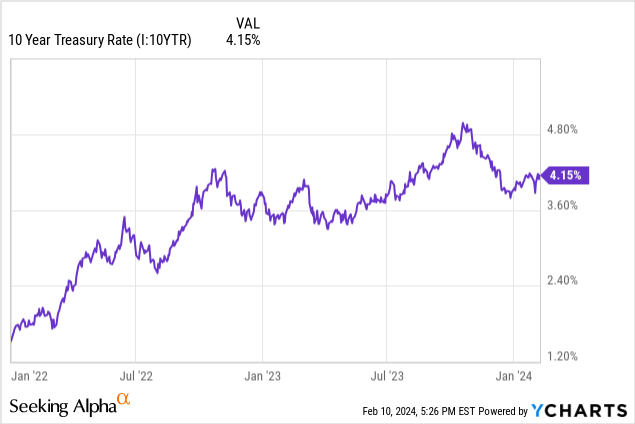

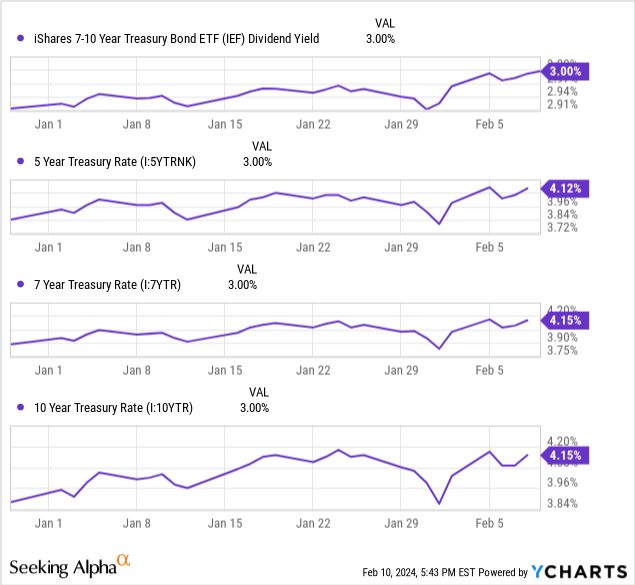

The iShares 7-10 Year Treasury Bond ETF (NASDAQ: IEF) is the largest treasury index ETF in the market. Federal Reserve hikes caused treasury rates to spike from early 2022 to mid 2023.

Higher treasury rates meant that newly-issued treasuries had higher coupon rates. Existing issues maintained their original, lower rates. Due to this, IEF’s existing treasury portfolio did not benefit from higher rates, at least not initially.

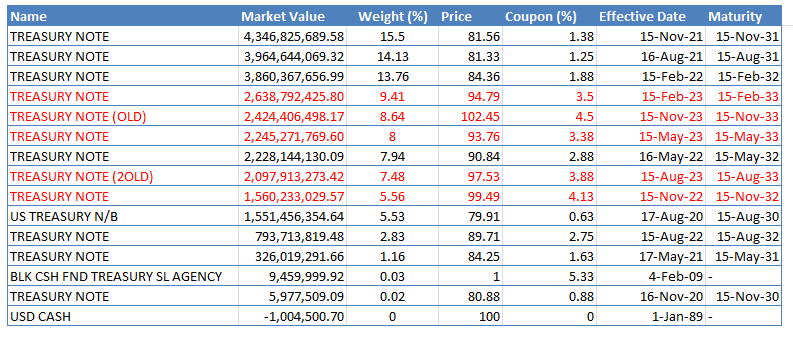

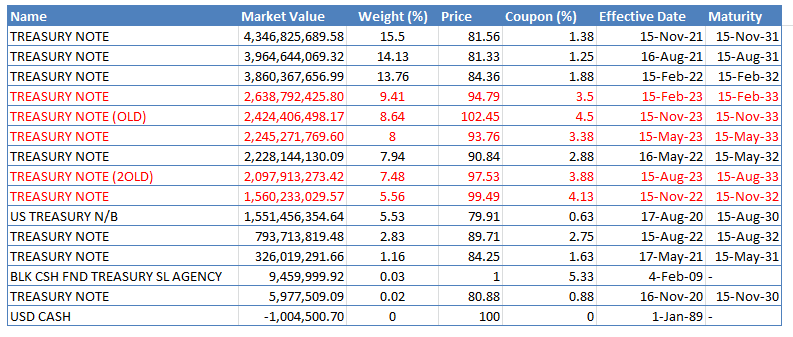

As said portfolio matured, however, the fund was able to replace older, lower-yielding treasuries with newer, higher-yielding ones, leading to greater income. Looking at IEF’s portfolio, newer treasuries account for around one third of its value, and these have much higher coupon rates than average, as expected. Portfolio is as follows, newer treasuries in red.

IEF – Table by Author

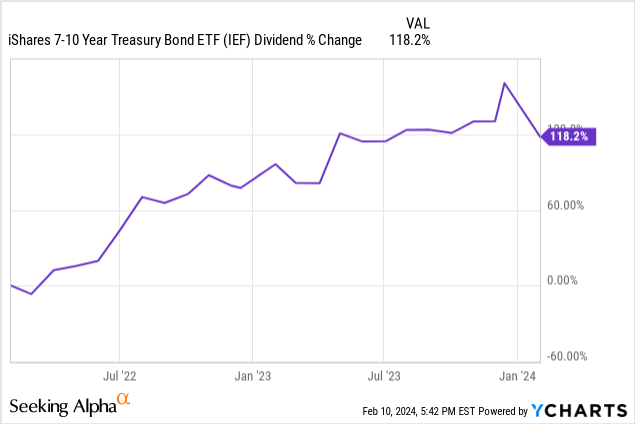

As IEF’s portfolio is slowly replaced with newer treasuries, its income increases, as do its dividends. Fund dividends have grown a whopping 118.2% since early 2022, when the Fed started to hike, in-line with expectations.

The process above can take several years to play out, as bonds generally take several years to mature. IEF has yet to replace its entire portfolio with newer, higher-yielding bonds, so the process has yet to fully play out for the fund. This is readily noticeable in the fund’s portfolio. Older issues in black.

IEF – Table by Author

It is also noticeable in the fact that the fund yields less than treasuries of comparable maturities.

Newly-issued treasuries yield more than IEF, a treasury fund, because the fund has a bunch of older treasuries with lower yields. The distinction between older and newer treasuries matters.

Considering the above, IEF’s dividends should grow until the fund yields around 4.1% – 4.2%, equivalent to prevailing treasury yields, in the coming years. Importantly, said growth is not contingent on any changes to market conditions, including Federal Reserve hikes, and is simply the logical endpoint of present conditions / delayed impact of prior hikes. Treasuries yield 4.1% – 4.2%, so treasury ETFs should yield the same.

An implication of the above is that minor Federal Reserve cuts or interest rate reductions would not necessarily lead to lower dividends for IEF.

As an example, if 10Y treasury rates decline 1.2%, from 4.2% to 3.0%, fund dividends should see no significant movements, as the fund already yields 3.0%. Said decline would simply equalize the fund’s current yield with treasury rates.

In the example above, I used TTM dividend yields. One can do a similar calculation using the fund’s latest monthly dividend payment, annualized. Doing so nets me a 3.0% dividend yield, equivalent to its TTM dividend yield, so no change there. These figures are different for other funds, however.

One can do another similar calculation looking at the fund’s portfolio itself.

IEF – Table by Author

Let’s say 10Y treasuries drop to 3.0%. The treasuries in red have higher coupon rates, so as these get replaced, fund income and dividends should decrease. The treasuries in black, however, have lower coupon rates, so as these get replaced fund income and dividends should increase. The net effect depends on the average coupon rate of IEF’s portfolio. One could calculate the figure from the table above, although some funds report the information themselves, including IEF.

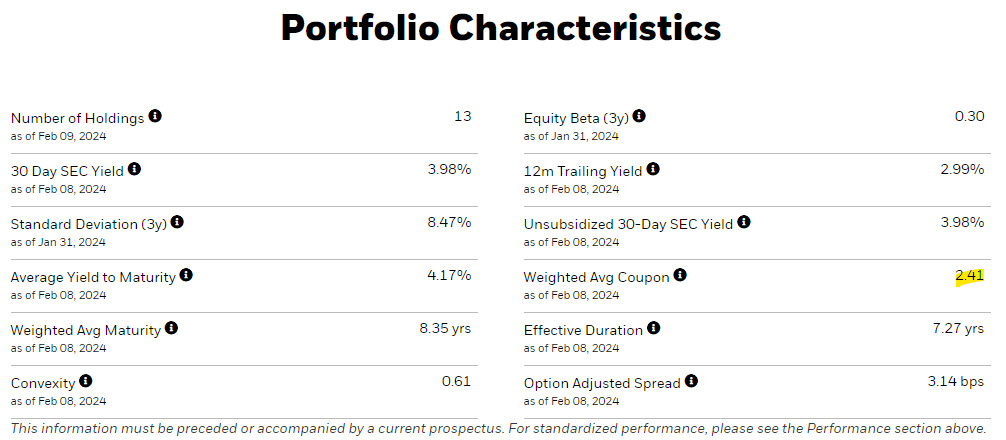

IEF

With 10Y treasury rates at 4.2%, and an average coupon rate of 2.4%, rates would have to decline 1.8% for IEF’s dividends to decline as well.

An issue with the above is that coupon rates are given at par, but bond prices have materially changed these past few years. Accounting for changes in market prices, IEF has an average coupon rate of 2.7%, so rates would have to decline 1.5% for fund dividends to decline as well.

For those keeping account, I think there are four different ways to try and estimate by how much rates would have to fall for bond funds dividends to fall as well. In all honesty, I am not sure which one is more accurate or more ‘logical’, so decided to average them out. Doing so gives me the following results:

Table and Calculations by Author

As can be seen above, some of the larger, more representative bond ETFs would still see positive dividend growth if rates were to decrease by less than 1.0% next year. The same should be true for most bond funds, as these are structural / market issues, and not specific to the four funds above. For reference, the Fed is guiding for 0.75% in rate cuts next year.

As the figures above are very rough, I wouldn’t take them too literally. Still, I do believe that more minor Fed rate cuts would not necessarily lead to significant, material reduction in dividends for most bond funds. Significant rate cuts would almost certainly lead to significant dividend cuts, however.

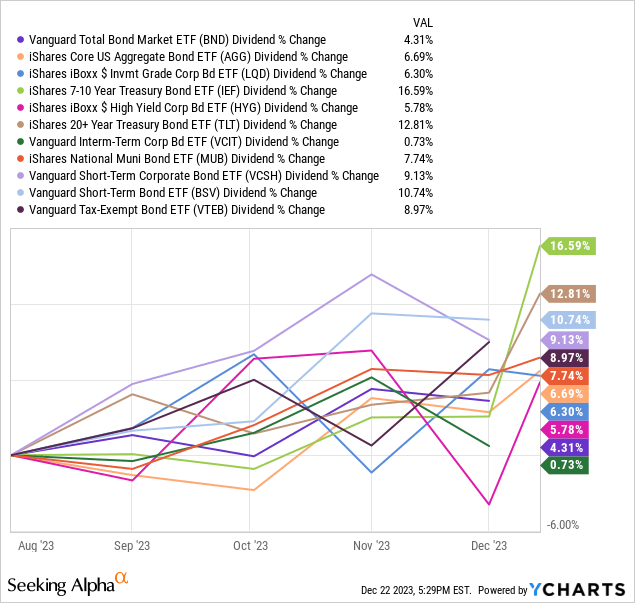

Although having bond funds and Fed rates moving in opposite direction seems a bit odd, there is (partial) precedent for this. Most of the larger bond ETFs have since positive dividend growth since August 2023, even though there have been no rate hikes since.

Data by YCharts

Bond fund dividends have grown even though Fed rates have not moved, due to the delayed impact of prior hikes. Considering the above, I am confident that most bond funds would have seen positive dividend growth from minor Fed rate cuts, of, say, 0.25%. The same seems likely to be true moving forward.

The implications of the above are quite positive for bond funds and investors. With a bit of luck, bond funds should see growing dividends in spite of likely Fed rate cuts. Significant rate would almost certainly lead to sizable dividend cuts, but these should be a bit lower than (naively) expected.

As a final point, do remember that market interest rates might not necessarily move in-line with Fed rates. I would definitely expect this to happen, but the relationship might not necessarily be exact, adding a lot of volatility to these figures and estimates.

Conclusion

Bond funds are still seeing positive dividend growth from prior Fed rate hikes. These might be sufficient to prevent any dividend cuts from future Fed rate cuts, depending on their magnitude and timing.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")