Mike Kemp/In Pictures via Getty Images

Introduction

LondonMetric (OTCPK:LNSPF) is a UK-based REIT focusing on triple net lease assets, predominantly in the logistics segment. The low LTV ratio means the increasing interest rates on the financial markets can be dealt with. Additionally, a substantial portion of the portfolio is currently leased out at below market rates which means we can expect a rent uplift as leases expire and have to be renewed.

Yahoo Finance

LondonMetric’s primary listing is in London where the stock is trading with LMP as its ticker symbol. There are currently 1.01 billion shares outstanding, resulting in a market capitalization of approximately 1.9B GBP. The average daily volume in London is 4.5 million shares.

Strong results, with additional rent increases

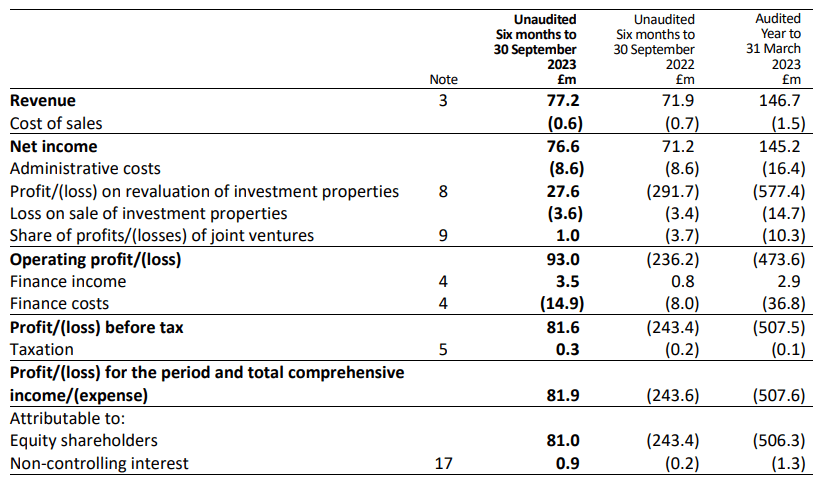

As LondonMetric is a triple net lease REIT, its financial performance is pretty straightforward and with a net rental income of approximately 76M GBP in the first semester, the main elements to determine LondonMetric’s financial performance are obviously the overhead expenses (these were just 8.6M GBP in the first half of FY 2024) as well as the interest expenses.

LondonMetric Investor Relations

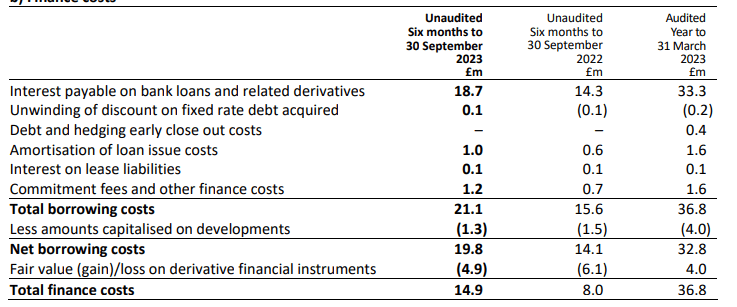

Fortunately LondonMetric is running a clean balance sheet with an LTV ratio of less than 30% so the higher interest rates definitely aren’t slowly suffocating the REIT, but there obviously is a noticeable impact. As you can see in the image above, LondonMetric recorded a total net finance expense of 11.4M GBP compared to 7.2M GBP in the first semester of the preceding year. Keep in mind not all of the finance expenses are interest expenses but as you can see below, there is a noticeable increase in interest expenses, partially offset by a gain on derivatives.

LondonMetric Investor Relations

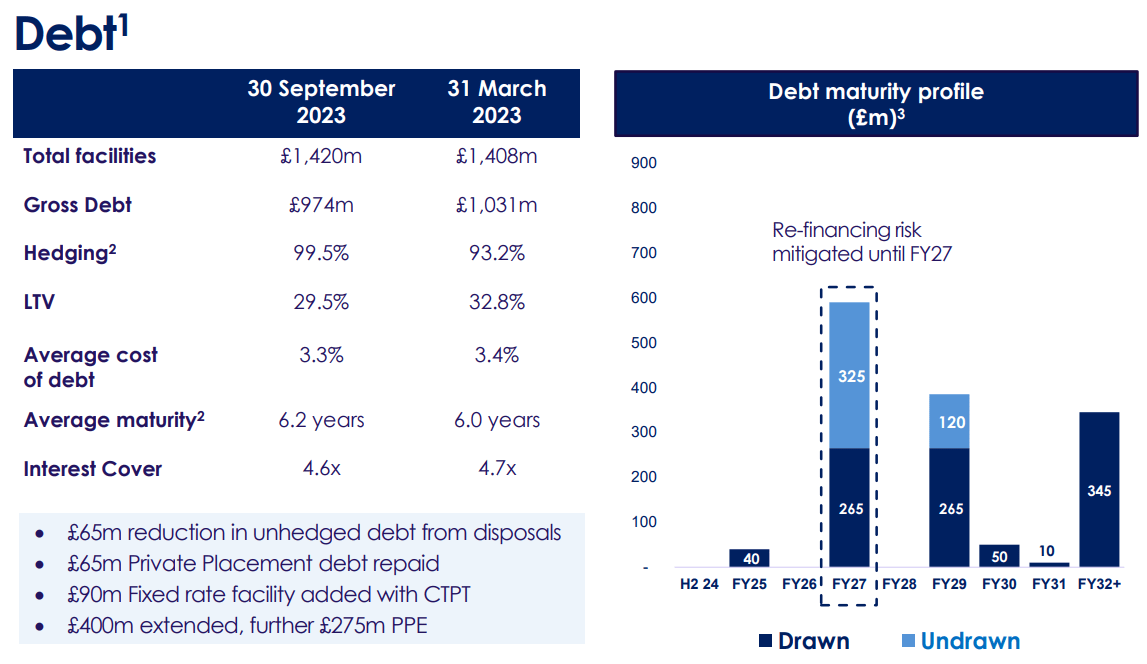

As of the end of the first semester, the REIT had hedged 99.5% of its debt at an average rate of 3.3%, so we shouldn’t see any negative surprises. That being said, future refinancings will obviously happen at a higher rate and that should hopefully be compensated by rent increases.

At the end of September, the total property value was 3.13B GBP, as you can see below. The REIT had 26M GBP in cash and 966M GBP in debt for a total net debt of approximately 940M GBP (excluding lease liabilities). This represents an LTV ratio of 30% versus the investment properties and just 29% if you’d include the investment in equity accounted joint ventures.

LondonMetric Investor Relations

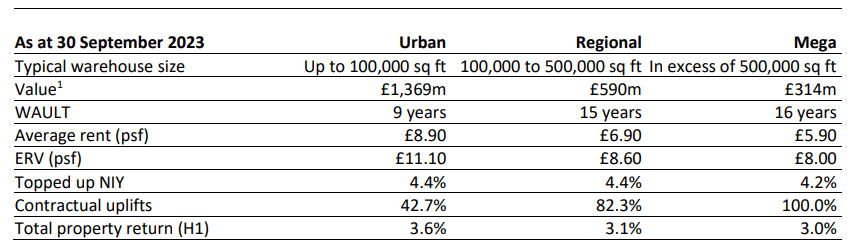

A very conservative balance sheet, indeed. And even if the average cost of debt would double to 6.6% over the next three years, and assuming an average annual rent hike of 3.5%, the net impact on the bottom line would be just 16M GBP or 1.6 pence per share per year. Needless to say the increased interest rates won’t have a major impact on the REIT’s income profile and its shareholder returns. The EPRA earnings came in at 5.25 pence per share in the first six months of the current financial year, while the Net Tangible Assets represented a value of 199 pence per share. This is valued at a net initial yield of 4.8% across the portfolio. While that is low, I like the index-linked rent reviews and the long duration of the contracts. Additionally, the market rent value is substantially higher than the current contractual rent. As you can see below, the urban logistics division, which accounts for in excess of 40% of the portfolio has a current average rent that’s approximately 20% below the market rent. And we see a similar difference in the Regional and Mega categories as well.

LondonMetric Investor Relations

And while I like the visibility offered by the long-term lease contracts, it also means that the leases that will have to be renewed soon may see a pretty interesting rent uplift. The REIT has guided for an anticipated 15M GBP annual income uplift between now and March 2026. This would imply the assets are valued at a 5.35% net rental income yield.

The proposed acquisition of LXi REIT

Earlier this year LondonMetric launched an offer to acquire LXi REIT, another UK-based REIT. As per the proposed terms, LondonMetric is offering 0.55 of its own shares per share of LXi. This ratio was based on the adjusted Net Tangible Assets of both REITs which was the most fair approach for both REITs.

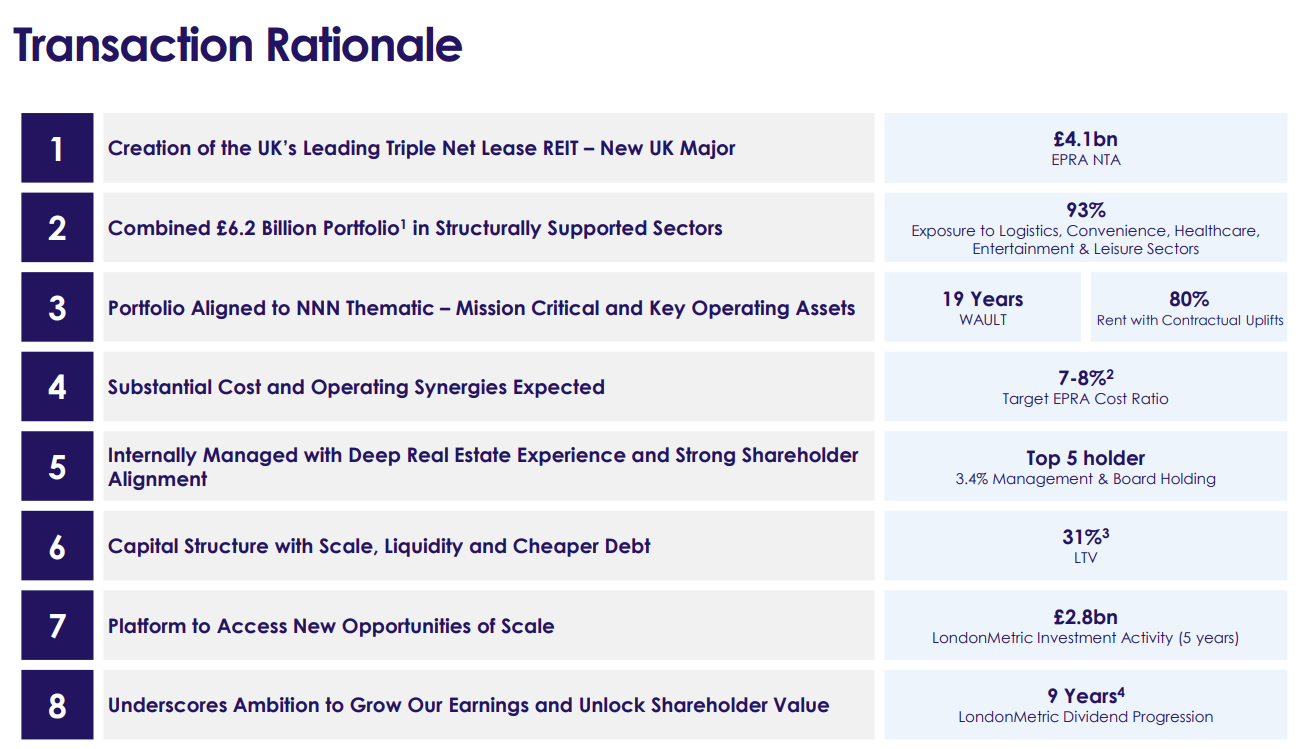

The combination of both entities will create the largest UK-based and UK-focused triple net REIT with north of 6B GBP in assets with a conservative balance sheet as the anticipated LTV ratio will be just 31% based on the current appraisal values of the assets of both REITs. As there should be some synergy benefits as well, LondonMetric anticipates it will be able to hike its dividend and currently suggests a 7.4% increase to 10.2 pence per share. This represents a dividend yield of approximately 5.5% based on the current share price, subject to a 20% dividend withholding tax.

LondonMetric Investor Relations

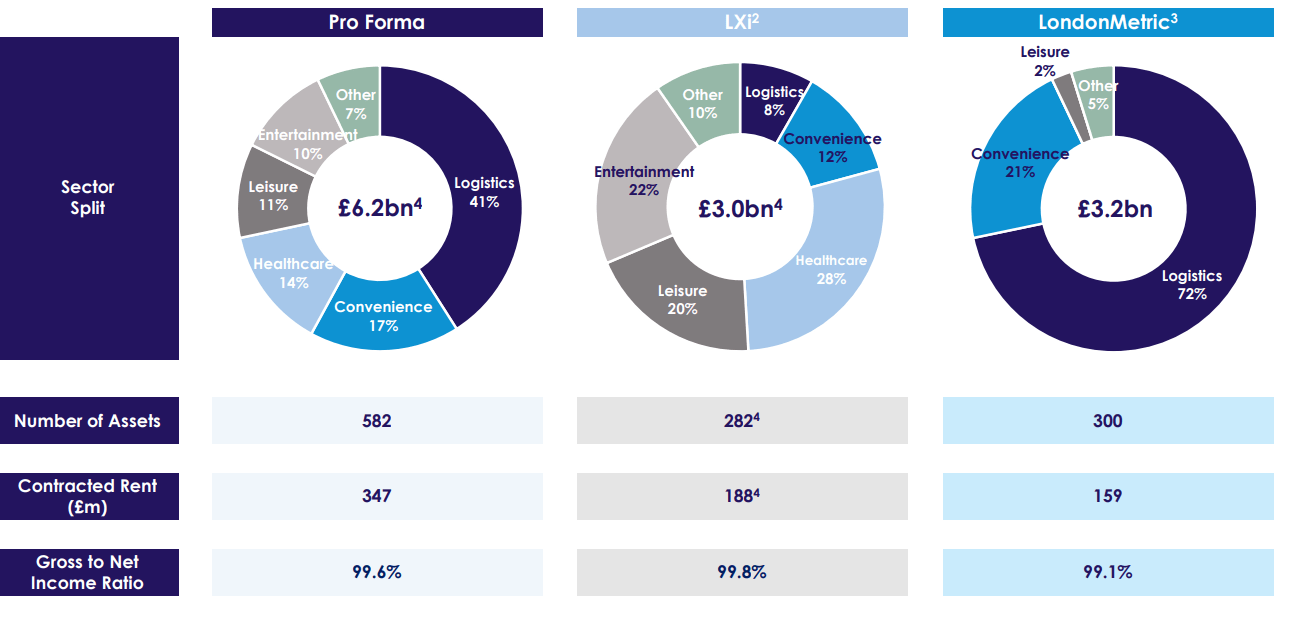

I think the proposed deal makes sense but the one downside I see is that I really liked LondonMetric’s focus on logistics while that category is the smallest in the LXi portfolio. As you can see below, on a pro forma basis, the combined entity will have an exposure of approximately 41% to the logistics sector.

LondonMetric Investor Relations

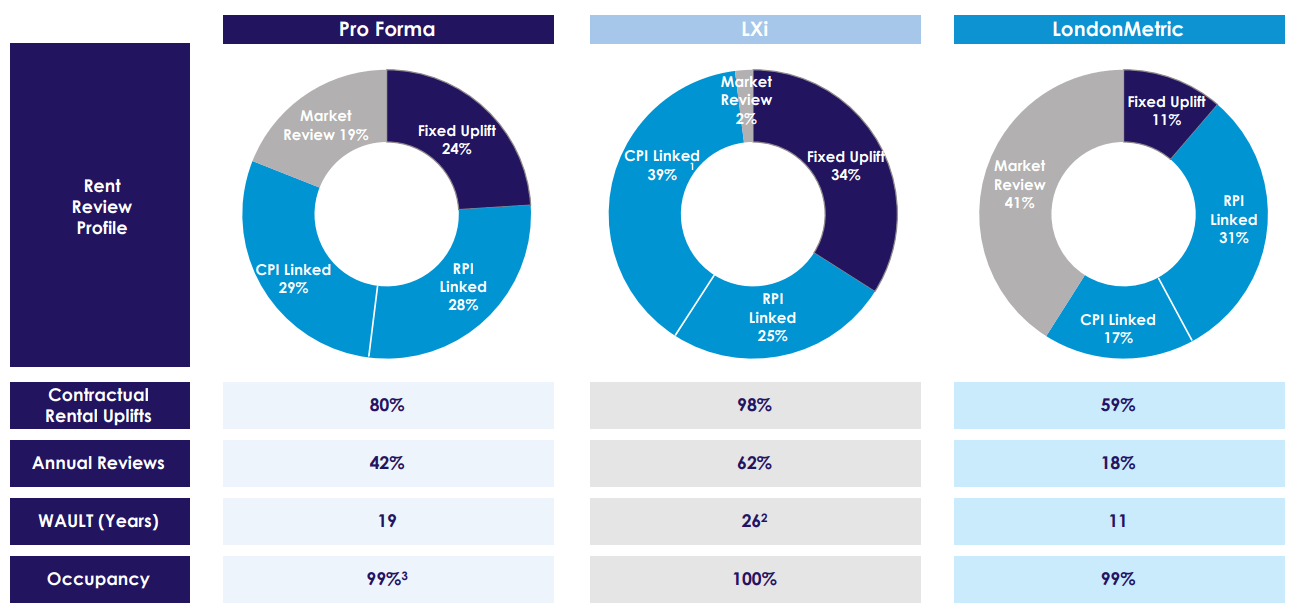

It looks like LXi shareholders should be in favor of the deal as it derisks their investment, while LondonMetric shareholders should like the deal as it unlocks additional synergy benefits and the combined entity will provide a strong platform to pursue further growth. Additionally, LXi’s portfolio has a weighted average unexpired lease term of 26 years so as long as its tenants don’t go bankrupt, LXi increases the visibility of the future earnings.

LondonMetric Investor Relations

As a conclusion: it looks like the acquisition of LXi REIT could create a win-win situation for the shareholders of both entities.

Investment thesis

I currently have no position in LondonMetric but my interest has definitely been triggered now. I think the acquisition of LXi REIT is a good move as well, and I may be looking to establish a long position on any weakness during the acquisition process. I will also keep an eye on the share price of LXi REIT as being able to buy it at a lower price than 0.55 times the LondonMetric share price would be a good move as well.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")