Social Security is a large part of the finances of tens of millions of retirees. Some depend on it for all or most of their retirement income, and some treat it as strictly supplemental income. Whatever the case, people have paid Social Security taxes for years, so it’s well-earned.

Regardless of the role Social Security benefits will have in your retirement finances, claiming benefits doesn’t mean you have to quit working or earning money. However, if you plan to continue working while receiving Social Security benefits, here are a few things to know that could help you maximize your earnings while minimizing the chances of getting penalized.

Image source: Getty Images.

It all starts with your full retirement age

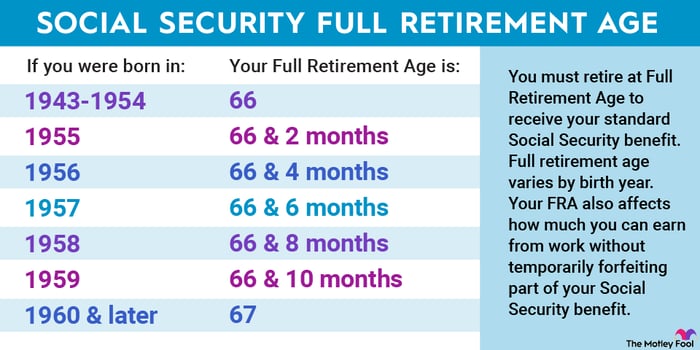

One of the most important numbers in Social Security is your full retirement age. It’s when you’re eligible to receive your primary insurance amount (PIA), which is the baseline Social Security uses to calculate your benefits if you decide to claim before or after your full retirement age.

Claiming benefits early reduces them based on how many months away you are from your full retirement age. Claiming benefits late increases them by two-thirds of 1% each month until you turn 70.

Your full retirement age is determined by your birth year as follows:

The Motley Fool.

You don’t have to stop working when you claim benefits

Plenty of people claim benefits and continue working for various reasons. Some do it for financial reasons, some to keep busy, and some just truly love what they do and aren’t ready to give it up. Whatever the case, one caveat is that if you claim Social Security benefits before your full retirement age and continue working and earn over a certain amount, you’ll face the Social Security retirement earnings test (RET).

With the Social Security RET, people earning over the threshold will have their benefits reduced based on how much over the limit and how far they are from their full retirement age.

If you won’t reach your full retirement age in 2024, the limit is $22,320. Earning above that amount will reduce benefits by $1 for every $2 over. If you’ll hit your full retirement age in 2024, the limit is $59,520. Earning above that amount will reduce benefits by $1 for every $3.

The RET income limit changes annually (with a couple of exceptions), so staying current with the year’s limit is important. In 2023, the limits were $22,320 and $56,520, so it could be a situation where you’re over the threshold in one year but not another.

Think of it as more of a temporary withholding

The good news is that benefits are not permanently lost when they’re reduced because of the RET. When you turn your full retirement age, Social Security recalculates your benefits in a way that gradually adds back the withheld amount.

Imagine if your full retirement age was 67, and you decided to take benefits at 64 while making over the allowed threshold. If the RET lowered your yearly benefits by $1,000, Social Security would’ve withheld $3,000 over the three years until you reach age 67. Once you turn 67, that $3,000 will be added to your monthly benefits, spread over the rest of your life.

Having your benefits reduced may not sit well with some people, but sometimes it’s worth earning over the limit if you have the opportunity and the reduced benefits don’t affect your livelihood. There are financial and other personal benefits to it. Ideally, if you’re working in retirement, it’s because you want to and not out of necessity, but in either case, knowing how the Social Security RET works is essential.

Q2 2024 Earnings Call Transcript")