What would you do if you could rewind the clock 20 years and buy Amazon stock? I would guess just about everybody would buy it knowing what they do today — and watch their investment gain more than 7,000%.

Since you can’t turn back the clock, you might be interested in buying stock in a company that, in many ways, is quite similar to Amazon, but reporting even higher growth rates than Amazon did 20 years ago. MercadoLibre (MELI 0.54%) stock has gained about 6,000% in its lifetime — but you should still buy it. Here’s why.

Incredible growth in a huge market

MercadoLibre operates an e-commerce platform in 18 Latin American countries that’s similar to Amazon, and it also offers many fintech services that were developed as a way to help underbanked customers shop on its platform. Both of these segments have reliably reported high growth over the past few years despite changes in multiple economic variables.

In 2023’s third quarter, revenue increased 69% year over year to $3.8 billion. To put that into context and get a sense of the opportunity here, it’s 2.7% of Amazon’s revenue in the same period.

MercadoLibre charts e-commerce progress with gross merchandise volume (GMV), or the product sales that moved through its system. GMV growth accelerated 59% year over year in the third quarter. There were several factors that worked in its favor. First, shoppers are returning to e-commerce after a resurgence in physical stores.

Second, MercadoLibre has been upgrading its logistics network to get products to customers faster. The number of orders delivered next or same day increased 22% year over year and accounted for 80% of total orders. That’s hard to compete within the region.

Fintech is MercadoLibre’s fastest-growing business. Total payment volume (TPV) increased 121% in the third quarter, but off-platform TPV, or payments outside of the MercadoLibre e-commerce platform, increased 145%. This represents an almost limitless opportunity in digital payments beyond the scope of its core business. It also has a credit business, and its portfolio increased 23% year over year in the quarter.

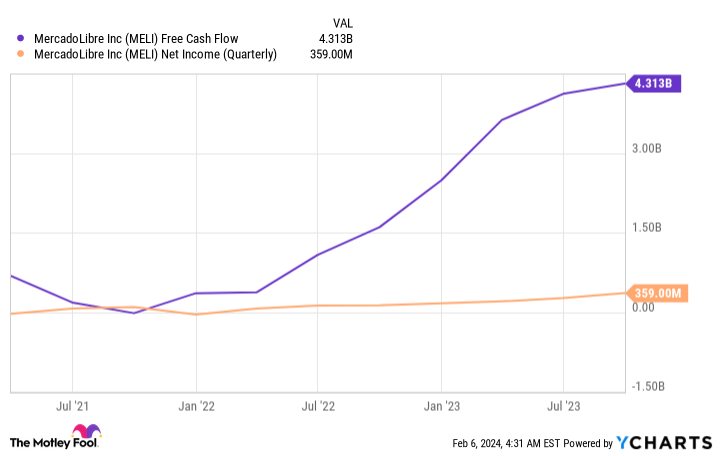

Just like Amazon, MercadoLibre sees a market opportunity in advertising. Ad sales increased more than 70% year over year for the sixth consecutive quarter. Not only is this a high-growth business, but it’s a high-margin business as well, contributing to higher profitability. Total profitability has been improving, and operating margin expanded from 11% last year to 18.2% this year. Net income has been positive for several consecutive quarters, and it’s generating increasing free cash flow.

MELI Free Cash Flow data by YCharts

Are there any risks?

Detractors might point out that many Latin American countries have volatile economies. MercadoLibre is headquartered in Uruguay, but its main market is Argentina, which is having its own economic crisis right now. Its second leading market is Brazil, whose inflation and subsequent interest rates have been skyrocketing.

Management noted that it took a hit to net income due to the devaluation of the Argentine Peso, but it has cash management strategies in place to offset these kinds of trends. This led to a significant increase in cash over the past year.

Another risk is that other companies are sensing the opportunity in Latin America, which lags globally in digital penetration and cashless buying. Sea Limited‘s Shopee app had become the top shopping app in Brazil at one point, although MercadoLibre is currently in the top spot, and Shein is no. 3.

It’s not too late to buy MercadoLibre stock

MercadoLibre stock is up 50% over the past year, but it’s still down from previous highs. At the current price, its shares trade at a lofty price-to-earnings ratio of 91. But MercadoLibre’s incredible growth and opportunity could justify a premium, and the company’s efficient risk-management plans inspire confidence in its ability to weather economic volatility.

It’s not too late to buy MercadoLibre stock, and it should provide years of shareholder value for long-term investors.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Jennifer Saibil has positions in MercadoLibre. The Motley Fool has positions in and recommends Amazon and MercadoLibre. The Motley Fool recommends SeaWorld Entertainment. The Motley Fool has a disclosure policy.

Q2 2024 Earnings Call Transcript")