tadamichi

Introduction

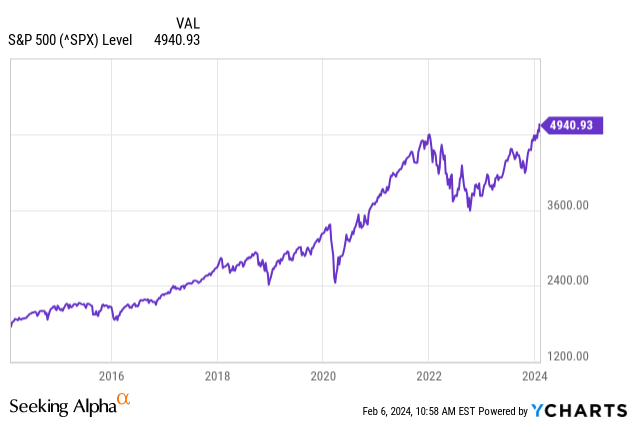

There is a tangible tension in the air since the S&P 500 hit a new all-time recently. We have reached another inflection point in the markets and where we go from here is uncertain.

With headlines overwhelmingly expressing doubt for a continued rally, it is understandable that many investors would be cautiously optimistic about markets. There is still great fear of a pullback, but missing out on another potential rally could leave investors falling behind trying to time this one.

Figure 1 (Seeking Alpha)

Note: I have no affiliation with any of the authors above. This screenshot was taken on 2/6/24.

Investors fearing drawdowns, especially in high flying sectors like tech, may want to build a more defensive equities portfolio that tilts toward companies traditionally more resilient to drawdowns and poor economic environments, as well as on sectors that are positioned to experience outsized growth.

My overall portfolio is very heavy on credit and fixed income, which I still believe is positioned very favorably for the next few years. If you want to see how I invest in bonds and alternatives, I wrote about it here.

Portfolio

Without further ado…

| Ticker | Name | Weight | Yield | ER |

| AVGE | Avantis All Equity Markets ETF | 45% | 1.93% | 0.23% |

| ACWV | iShares MSCI Global Min Vol Factor ETF | 20% | 2.37% | 0.20% |

| SCHD | Schwab US Dividend Equity ETF | 10% | 3.45% | 0.06% |

| DGRO |

iShares Core Dividend Growth ETF |

10% | 1.70% | 0.08% |

| SPGP | Invesco S&P 500 GARP ETF | 7.5% | 1.26% | 0.34% |

| SPHQ | Invesco S&P 500 Quality ETF | 7.5% | 1.36% | 0.15% |

| Weighted Average | 2.12% | 0.19% |

The portfolio is broken down into two parts: the core, and its satellites. This is one of my go-to methods of portfolio construction, as it allows me to use broad-market, cheap index funds to diversify the majority of the majority of the portfolio. Then, we can use the excess capital (in this case: 20%) to allocate to riskier assets with different screeners and strategies.

The Funds

This portfolio is designed using six ETFs, with no mutual funds appearing this go-around.

My usual readers will know that I have a great affinity for mutual funds, but I am trying to exclude them from these articles because of limited investor access. After my last portfolio article, I had a reader mention that Canadians have access to US ETFs, but not mutual fund. To that end, I have made an effort (and intend to continue on doing so) to limit the use of mutual funds in these kinds of articles.

The Core: Diversified World Equities

The core of the portfolio is built with defense in mind, and nothing screams defense to me in equity investors more than the all-world index. Usually, investors might think of Vanguard’s (VT) or their equivalent mutual fund (VTWAX) when it comes to all-world investing. I’m going with a different pick, Avantis’ (AVGE).

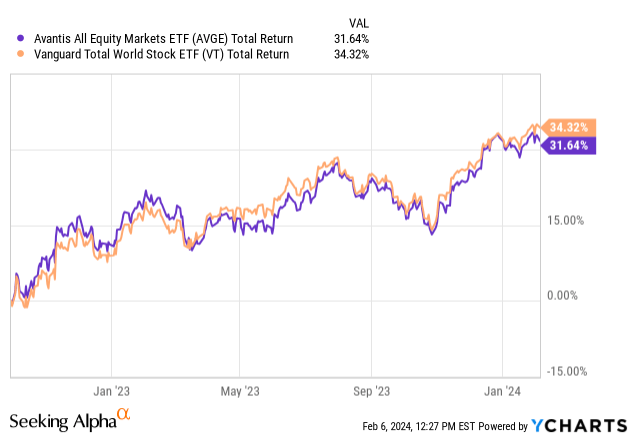

Avantis All Equity Markets ETF (AVGE) – 45%

AVGE is a fund-of-funds that uses Avantis’ equity index ETFs to build a globally diversified portfolio that tilts toward the value and small cap factors. This means that we get to tilt defensively, toward factors that have historically given equities more favorable risk/reward profiles, and keep this allocation to a single ETF.

Figure 2 (Avantis Investors)

Since inception, it has held its own against the index. The fund is too new to tell if this strategy will be a clear winner, since it has yet to be exposed to a black swan crash or any other financial crises.

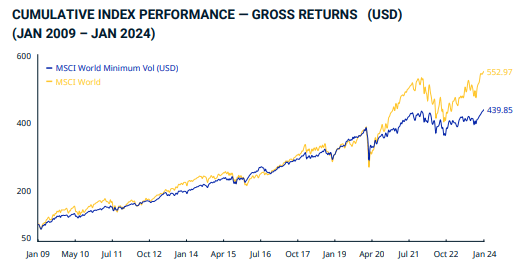

iShares MSCI Global Min Vol Factor ETF (ACWV) – 20%

Regular readers to my column will recognize this ETF as it is consistently ranked as one of my favorite equity ETFs. Along with its US counterpart (USMV), ACWV is a global index that weights its components so as to minimize expected volatility. This reduction in risk should lead to a similar reduction in reward (as one could expect in any situation), but historically, this strategy has matched pace with the index while still providing downside protection. This trend only broke in the last few years, as the “Magnificent 7” has carried the world index to new heights.

Figure 3 (MSCI)

Together with AVGE, this allocation to ACWV gives the portfolio a global stock allocation of 65% with significant weighting toward the value, small cap, and minimum volatility risk premia.

Despite both funds holding global indices, they have a surprisingly low overlap by weight, since the weightings are very different.

Figure 4* (ETF Research Center)

This gives our core holdings a good amount of internal diversity and creates a defensive position in developed and emerging markets if we have another 2000-2010 decade of flat US stock returns.

The Satellite Array: Concentrated Bets on America

In equity investing, I tend to have a preference for holding US stocks. This has to do with macro conditions, as well as home bias, and the lack of a need for currency hedging. I also find the story of US stocks most compelling at the present moment, with indices like the Euro Stoxx 50 (FEZ is the ETF) index not exciting me much with the mounting regulation and stagnant nature of European business development.

I have little knowledge of macro conditions across EM and FM countries, so I leave that exposure to our global positions and prefer to make sector and strategy bets on US indices only.

Schwab U.S. Dividend Equity ETF (SCHD) & iShares Core Dividend Growth ETF (DGRO)- 20%

I have paired up these two funds because they cover the same investment philosophy, but are different from each other.

Both of these funds focus on a few ideas that are important for long-term, stable investments like sustainable dividends and quality balance sheets.

They have mostly kept pace with the broader market, while exhibiting less volatility and paying out much heavier dividends to investors.

Here are some major points of comparison between these two funds that explain why I am holding them in tandem.

- SCHD has 104 holdings, DGRO has 424

- Only 26 stocks overlap, with a weighting overlap of 28%

- DGRO has a significantly higher allocation to info tech, heavier by 14% of its weight compared to SCHD

- SCHD is heavier on energy, with about 6% heavier weight than DGRO

- Major non-overlapping stocks that DGRO can contribute include (MSFT), (AAPL), and (JNJ)

Figure 5 (ETF Research Center)

Invesco S&P 500 GARP ETF (SPGP) & Invesco S&P 500 Quality ETF (SPHQ)- 15%

Our last pair of funds are heavily screened ETFs that use very different methodologies that the other holdings. Specifically, these two funds focus on companies found within the S&P 500, which already screens for US large-cap and mega-cap companies that are continuously profitable, among other criteria.

To take a more defensive stance than a broad S&P 500 ETF like (SPY), we can screen these stocks down further and isolate companies that have overwhelmingly favorable fundamentals. This has historically provided significant returns for both funds over the index.

The Invesco S&P 500 GARP ETF (SPGP) focuses on the philosophy of “growth at a reasonable price,” meaning that it is selecting growth companies weighted by their quality and value composite scores. You can read more about their methodology here.

The Invesco S&P 500 Quality ETF (SPHQ) screens the entire S&P 500 to come to 100 stocks ranked by their quality scores, which is measured by the “profitability/quality” factor. You can read more about the specific methodology here.

Major comparisons include:

- SPGP holds 77 stocks, and SPHQ holds 103

- 35 of their holdings overlap, with a 23% overlap by weight

- SPGP is heavier on energy and by 15% and 10% respectively compared to SPHQ

- SPHQ is overweight tech by about 13% compared to SPGP

- Major non-overlap stocks that SPHQ can contribute to SPGP include NVIDIA (NVDA), Mastercard (MA), and Broadcom (AVGO)

Suitability & Risks

Naturally, an all-equities portfolio, no matter how defensive, comes with significant equity risk. Note in the above charts how nearly every ticker suffered during the March 2020 crash. This is indicative of the general trend for equities to exhibit risk.

While this portfolio carries less equity risk with a beta of 0.90 and an annualized standard deviation of 14% in a 10-year backtest.

Note: the backtest uses DFA’s DGEIX instead of Avantis’ AVGE in order to push out to the 10yr mark.

In that 10yr backtest, we find the kryptonite for this portfolio: rising rates.

In both 2018 and 2022, periods of rising central bank rates, the portfolio suffered losing years across its assets. This falls in line with traditional equities.

Figure 6 (Portfolio Visualizer)

Investors need to have a moderate to high risk tolerance to hold this portfolio, with its highest monthly drawdown being as deep as 14%, back in March 2020. All-equities portfolios are not for the faint of heart.

That being said, the portfolio did 11% in both April and November of 2020, so it is important to note that with downside, comes potential upside. The risk is compensated in this portfolio, but risk is still important to consider as it affects investor psychology.

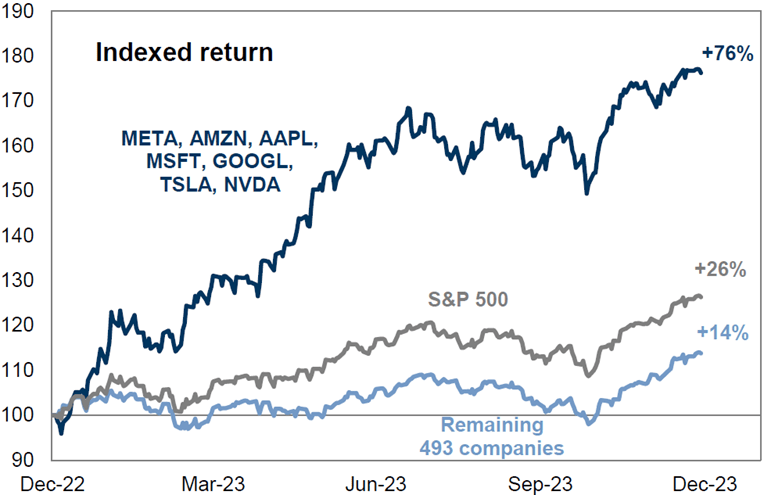

Style investing is also a risk to note, as it can underperform for long periods of time, as we’ve seen with the value effect. This underperformance in the past is part of what makes me bullish on the factor moving forward, as the M7 stocks now have such high valuations that they are making up 30% of the S&P 500’s market cap weight and were at the forefront of its returns last year.

Figure 7 (Goldman Sachs)

I intend to take a contrarian bet that either these stocks will fall back to reality or the other 493 will start to catch-up. That bet comes in the form of quality, some of which are in the M7, and some of which aren’t. None of the M7 stocks included in the various funds in this portfolio are held at market weight. I see this as an advantage. The portfolio, compared to the global index benchmark, is far heavier on large-cap value, US allocations, and mid-cap growth than the global index.

Figure 8 (Portfolio Visualizer)

Conclusion

This portfolio is my take on an all-equity portfolio that I would construct today. With an average expense ratio below 25bps, a yield almost 50% higher than the global index, and heavier weightings toward identified risk premia (profitability/quality, value, etc.), this portfolio is positioned to take advantage of a closing gap from the 493 stocks trailing the S&P 500’s average return.

It’s also poised to gain from a resurgence of global stocks, with a bias toward the US only in specialty weightings that change our risk/reward profile.

Risk is still a major factor to consider. For the moderately conversation investor who wants to incorporate bonds into the portfolio to smooth out its returns and provide fixed, reliable income compared to equities, check out my current fixed income portfolio, which you can read about here.

Thanks for reading.

Q2 2024 Earnings Call Transcript")