Torsten Asmus

Short-term interest rates have been quite attractive to me for a while now. Back in January, I wrote up the short-term bond ETF, also known as the SPDR® Bloomberg 1-3 Month T-Bill ETF (BIL). I also included it in my top-5 of best ideas for 2024. I realize it is very dull position, but the current yield on the short end of the yield curve exceeds that on the long end. The potential reward is pretty sizeable in absolute terms (above 5%), and these treasuries are often referred to as the risk-free rate or similar terms.

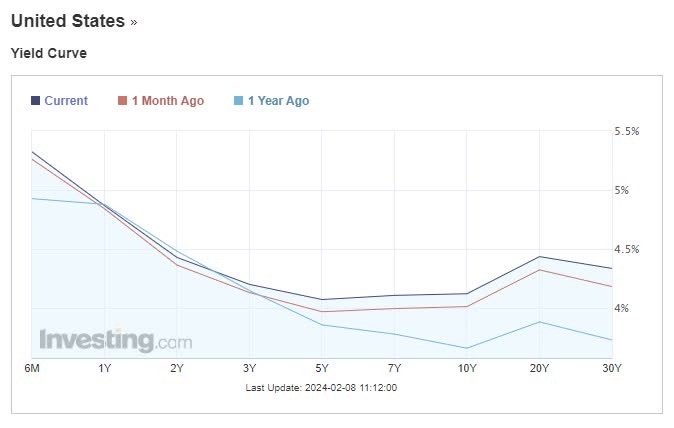

My last article was written a little over one month ago. Yields have increased on the short end and increased on the long end. The curve remains inverted.

US yield curve (Investing.com)

The curve shifted because Fed Chair Powell held another press conference and pushed back on market expectations that rate decreases were imminent. The Fed wants to see further confirmation inflation stays down and out:

That would mean the services sectors would have to contribute more. So in other words, what we care about is the aggregate number, not so much the composition. But we just need to see more. That’s where we are as a Committee. We need to see more evidence that sort of confirms what we think we’re seeing, and that gives us confidence that we’re on a path to, a sustainable path down to 2 percent inflation.

One piece of evidence Powell cited was he’d like to see inflation come out of services sector. He thinks goods inflation is down but

So, as you know, almost every participant on the committee does believe that it will be appropriate to reduce rates, and partly for the reasons that you say. We feel like inflation is coming down. Growth has been strong. The labor market is strong. What we’re trying to do is identify a place where we’re really confident about inflation getting back down to 2 percent so that we can then begin the process of dialing back the restrictive level. So, overall, I think people do believe, and as you know, the median participant wrote down three rate cuts this year. But I think to get to that place where we feel comfortable starting the process, we need some confirmation that inflation is, in fact, coming down sustainably to 2 percent

He also clarified that the labor market holding up well is giving the Fed a lot of leeway holding rates where they are. Given they have 2 mandates; full employment and stable prices, the juxtaposition of inflation rapidly falling and a strong labor market is everything the Fed wants. Why risk inflation coming back when labor isn’t suffering? Lots of commentators are arguing for one way or the other (usually faster rate cuts), but this usually accompanies a view that a slowdown is imminent. It could easily have happened, but it didn’t. So understandably, the Fed is comfortable hanging around where they are. At the same time, Powell appears ready to cut if labor weakens:

CHAIR POWELL. Yes. So let me say that we’re not looking for that. That’s not something we’re looking for. But yes, if you think about, you know, in the base case, the economy is performing well, the labor market remains strong. If we saw an unexpected weakening certainly in the labor market, that would certainly weigh on cutting sooner. Absolutely. And if we saw inflation being stickier or higher or those sorts of things, we would argue for moving later.

One of the important takeaways came when Powell point-blank stated he didn’t think it was likely they would cut rats in March:

Based on the meeting today, I would tell you that I don’t think it’s likely that the Committee will reach a level of confidence by the time of the March meeting to identify March as the time to do that. But that’s to be seen. So I wouldn’t call — you know, when you ask me about in the near term, I’m hearing that as March. I would say that’s probably not the most likely case

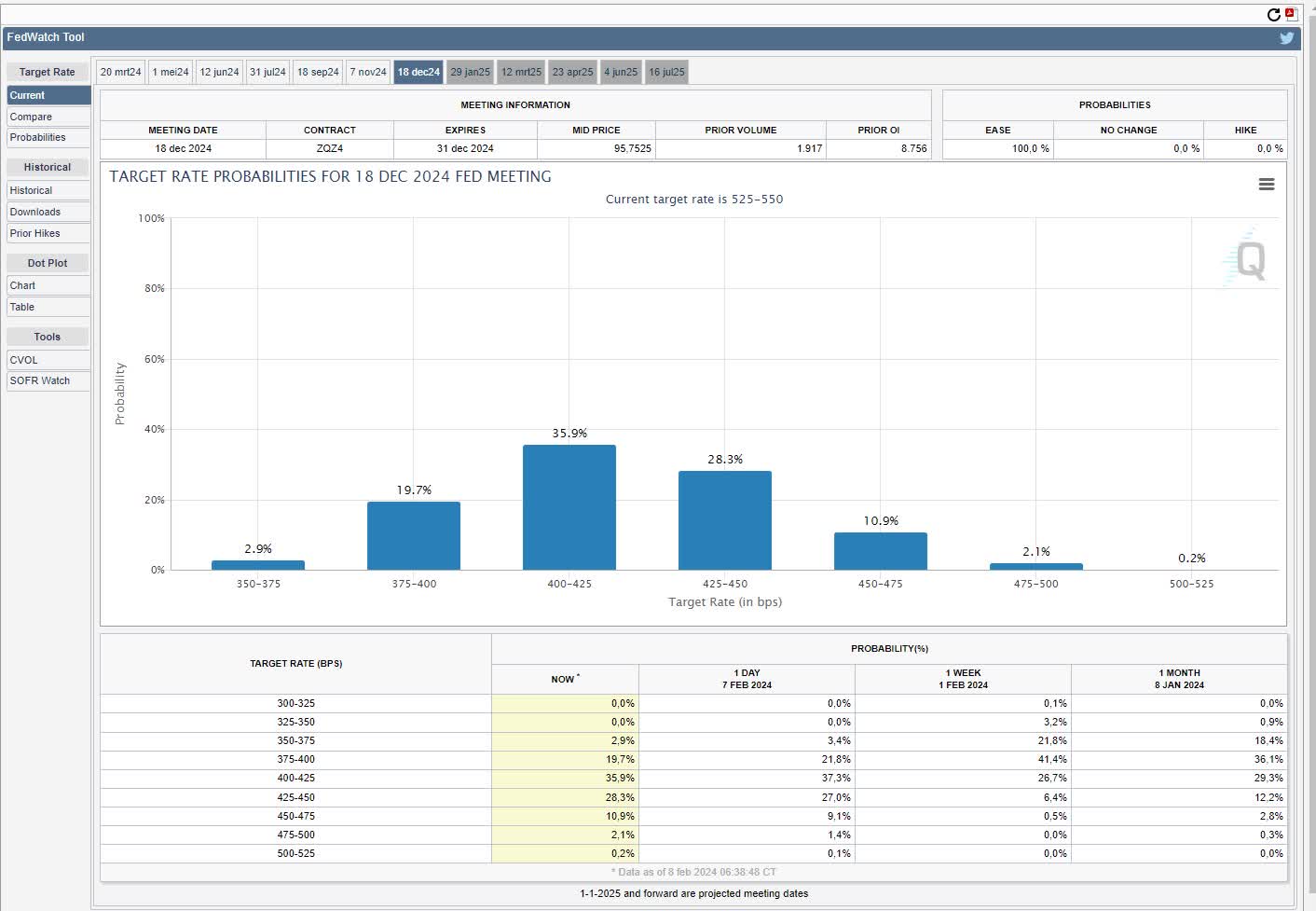

To me, the current yield on short-term paper still looks amazing. There is not a lot of risk (credit or interest rate). With bonds with longer maturity, you could make a lot more if the Fed cuts aggressively. The problem is that quite a few rate cuts are priced in. The CME FedWatch tool points to a 100% probability of rates being cut significantly by the end of 2024.

CME FedWatch tool (CME)

If that happens, long bonds are better. Then there is the chance that inflation surprises by going back up… It seems inconceivable right now but things can change. Suddenly, rate hikes could return to focus (especially if labor somewhat paradoxically holds up). The long end will be carnage.

A comparison with high-yield bonds illustrates well why I like T-Bills. For example, If you look at the iShares iBoxx $ High Yield Corp Bd ETF (HYG), it offers a SEC yield of 7.28% vs 5.23% for BIL. That ETF sports an expense ratio of nearly 0.5% vs 0.14% for BIL. It seems doubtful to me that the 1.7% difference is worth the extra risk. If there’s a recession, high-yield suddenly starts behaving a lot like equities.

Finally, I found another interesting paper on yield curves and forward interest rates by Roni Israelov and Stephanie Lo. They found that when the yield curve is inverted (i.e., like now), the short rate has much higher odds of declining compared to the long end.

In conclusion, treasury bills look quite attractive to me. The shorter, the better. There are various ways to own these. Either directly or through the vehicle I mentioned before or alternatives like the Goldman Sachs Access Treasury 0-1 Year ETF (GBIL), Schwab Short Term US Treasury ETF (SCHO), iShares® 0-3 Month Treasury Bond ETF (SGOV), the Vanguard Short-Term Treasury ETF (VGSH), AB Ultra Short Income ETF (YEAR), or the iShares Short Treasury Bond ETF (SHV).

Despite the potential of higher returns from bonds or high yield, they don’t look as good from a risk/reward perspective. There is indeed a chance the yields on longer bonds won’t be available in the future, but that remains to be seen. For now, the short-end is offering a very high yield, and it is more likely to come down than the long-end is to go down. If rates come down some, it is easy enough to re-evaluate and perhaps reposition. One thing that interests me about bonds is the current high volatility and that’s why I like selling calls on 10-year bonds.

Q2 2024 Earnings Call Transcript")