JulPo

Trane Technologies plc (NYSE:TT) recently delivered its most recent annual report, which included new investments in new products, new innovations, and 2030 Sustainability Commitments. In addition, given recent acquisitions, and the decrease in the net debt/EBITDA levels, I think that Trane could bring new inorganic growth in the coming years. Also with beneficial guidance for 2024, and overall beneficial expectations for the year 2024, Trane looks like a must-follow stock. Yes, there are risks out there from supply chain issues, or changing labor conditions, however, under my DCF models, I believe that there is more upside potential than downside risks.

Business Model, Guidance, And Expectations For 2024-2025

With high corporate recognition in relation to its participation in the energy transition and the adaptation of businesses and projects to climate change, Trane Technologies offers sustainability and efficiency solutions to buildings, residences and transportation markets through its Trane and Thermo King brands.

Trane’s main product line, which in turn means the greatest revenue source for the company, is ventilation and air conditioning solutions, as well as transportation refrigeration. Trane has global facilities and another part of its income comes from customized refrigeration products as well as the rental of some assets.

Its income comes from more than 100 countries where it has a presence outside the United States, where, unlike what occurs in the domestic sphere with its own distribution franchises, the marketing of these products is given through third parties.

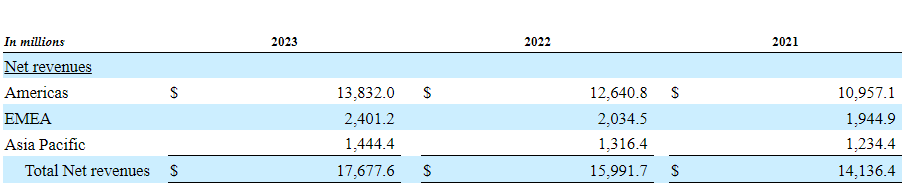

Trane has decided to establish a distinction by geography in its business, leaving it made up of three segments: the Americas, where Mexico, Canada, the United States and South America are included, that of Europe, Africa and the Middle East, and that of Asia-Pacific.

The Americas segment is the one that provides the most revenue to Trane, representing more than 70% of the company’s revenue. This offers commercial cooling and ventilation services, building control, and energy services and related solutions.

As shown in the table below, in 2023, the three business segments included net sales growth. With Trane Technologies successfully working in every part of the world, I believe that Trane runs a solid business model.

Source: 10-k

Better Than Expected Net Sales Growth, And Significant Increase In Expectations.

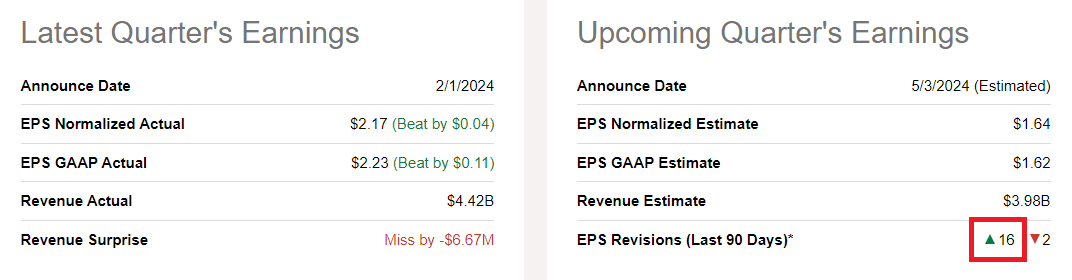

In the last quarter, Trane noted better than expected earnings EPS GAAP of $2.23. But, I believe that the most remarkable thing is that 16 analysts increased their expectations for the new quarter in the last 90 days.

Source: Seeking Alpha

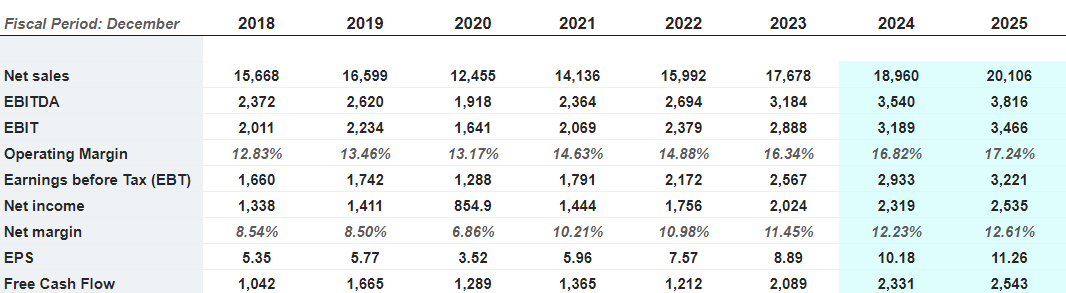

Expectations from other market analysts are overall quite positive. They expect net sales growth, EBITDA growth, net margin growth, and FCF growth. In particular, expectations include 2025 net sales of $20.106 billion, with 2025 Ebitda of close to $3816 million, 2025 Ebit worth $3466 million, and 2025 net income of about $2535 million. Finally, 2025 free cash flow would stand at about $2543 million.

Source: Market Screener

Guidance was also quite beneficial. The company expected 2024 net sales growth of close to 7%, and 2024 EPS of $9.90 to $10.20. Given these new figures, and the recent annual report, I believe that Trane is a good read.

The Company expects full-year 2024 reported revenue growth of approximately 7 percent to 8 percent; organic revenue growth of approximately 6 percent to 7 percent versus full-year 2023. The Company expects GAAP continuing EPS for full-year 2024 of $9.90 to $10.20. This includes EPS of $0.10 for non-GAAP adjustments. The Company expects adjusted continuing EPS for full-year 2024 of $10.00 to $10.30. Source: 10-Q

Balance Sheet, And Cost Of Debt

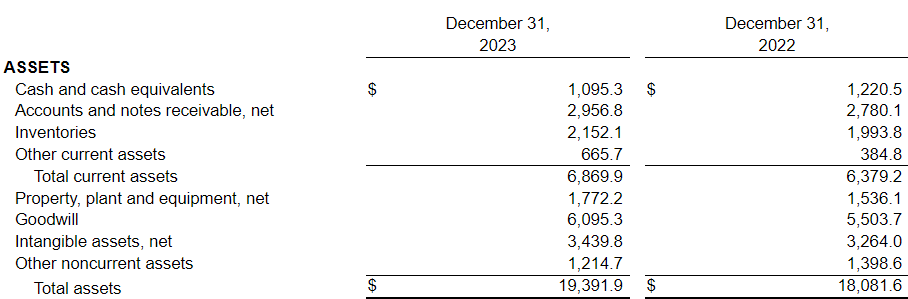

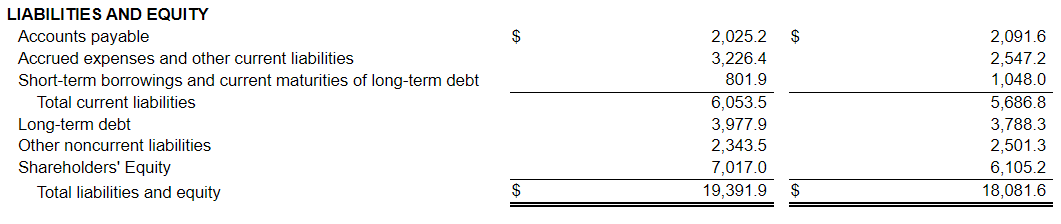

As of December 31, 2023 Trane reported cash worth $1095 million, with accounts and notes receivable of about $2956 million, inventories worth $2152 million, and other current assets of $665 million. Total current assets stand at $6869 million, and the ratio to current assets/current liabilities is larger than 1x. Hence, I do not think there is a liquidity issue here.

Long term assets include property, plant and equipment worth $1.772 billion, with goodwill of $6095 million, and intangible assets close to $3439 million. Finally, total assets are equal to close to $19.391 billion. The asset/liability ratio is larger than 1x, so in my view, the balance sheet appears stable.

Source: 10-Q

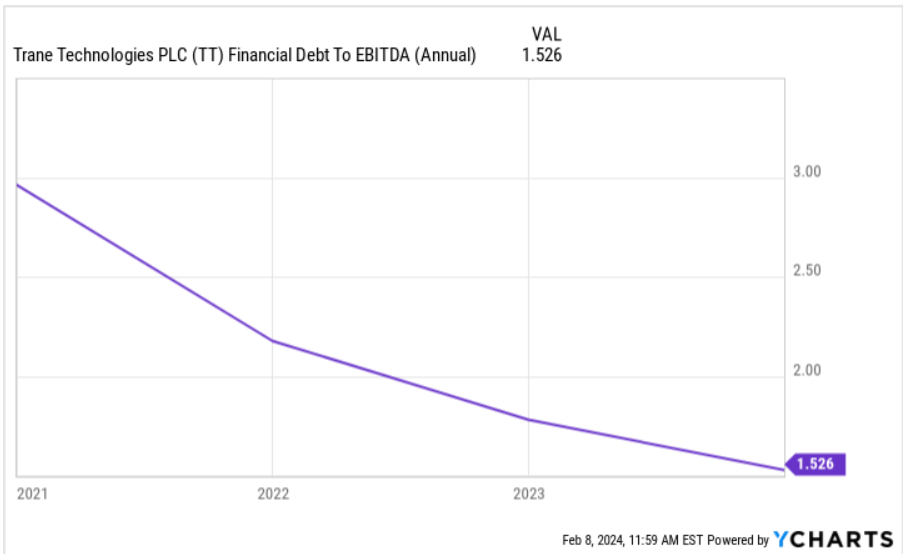

I am not worried about the total amount of debt as the financial debt/EBITDA ratios stand at more than 1.5x. However, the debt is not small. If the company continues to lower its debt levels I believe that the Ev/FCF will most likely increase.

Source: Ycharts

The list of liabilities include accounts payable worth $2025 million, with accrued expenses and other current liabilities of about $3226 million, and short-term borrowings and current maturities of long-term debt worth $801 million. Finally, with long-term debt of about $3977 million, total liabilities and equity stand at about $19391 million.

Source: 10-Q

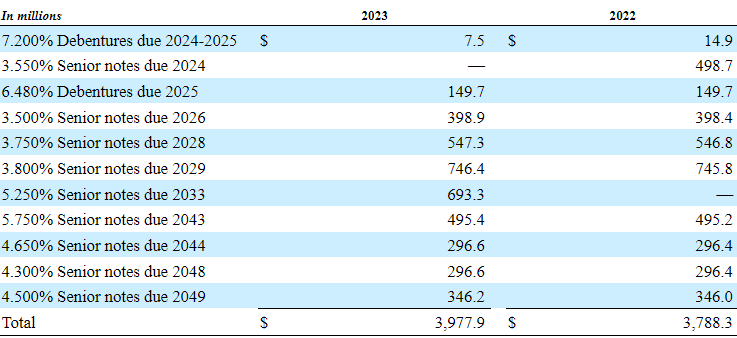

Trane Technologies reported senior notes including interest rate close to 3.5%, and 7.2%. In the last annual report, Trane reported that the weighted-average interest rate stood at close to 4.9% and 6.3%. With these figures, I believe that the WACC could be close to 6%.

Source: 10-k

The weighted-average interest rate for Short-term borrowings and current maturities of long-term debt at December 31, 2023 and 2022 was 4.6% and 4.9%, respectively. Source: 10-k

ESG Efforts Could Bring Demand From Market Participants Focused On ESG Investing

As part of its long-term strategy, Trane has assumed a series of responsibilities in relation to caring for the environment and climate change, among which stands out the reduction of at least one billion tons per square meter. From the beginning of its operation in 2019 to the present, the company has managed to reduce the carbon footprint of its clients by many million tons per square meter. In the last annual report delivered in February, 2024, I believe that Trane made ambitious commentaries with regards to emissions reduction efforts through 2030.

Our 2030 Sustainability Commitments for scopes 1, 2, and 3 will guide our emissions reduction efforts through 2030, with an emphasis on reducing our largest source: the emissions generated from customer use of our products. We are Leading by Example as we make progress toward carbon-neutral operations and zero waste-to-landfill across our global footprint and net positive water use in water-stressed locations. Source: 10-k

In this sense, I would point out that the regulations surrounding carbon emissions are more advanced and generate a fertile field for the appearance and expansion of this type of services, as well as the increase in energy costs also generate a trend for consumers to look for cheaper options for ventilating spaces. I believe that Trane may capitalize on these new opportunities.

In this regard, it is also worth noting that Trane Technologies modified its compensation plans to directors and executive officers in order to include ESG efforts.

We believe compensating our directors and executive officers with a mix of equity-based awards effectively links compensation to long-term shareholder value creation, Environmental, Social, and Governance, and financial results. Source: 10-k

I believe that these efforts would most likely bring the interest of investors focused on ESG and sustainability. We are talking about a market that is expected to grow at a double digit. An increase in the demand for stock could enhance the stock valuation.

Regulatory changes and challenges around disclosure will increase firms’ interest in ESG and sustainability consulting. In Verdantix’s newest report – ESG & Sustainability Consulting: Market Size & Forecast 2021-2027- our research projects a 17% annual growth rate in ESG and sustainability consulting spending in the next five years. Source: Verdantix

Base Case Scenario: M&A Efforts To Bring Inorganic Growth, And Economies Of Scale

In 2023, the company reported the acquisition of MTA S.p.A, Helmer Scientific Inc, and Nuvolo Technologies Corporation. I believe that synergies obtained from these acquisitions, economies of scale, and new know-how acquired could bring significant FCF margin improvements. Given the recent decrease in net debt/EBITDA, in my view, debt holders will most likely approve new acquisitions. In this regard, have a look at more information about the recent acquisition of Nuvolo Technologies.

We completed the acquisition of Nuvolo Technologies Corporation, a global leader in modern, cloud-based enterprise asset management and connected workplace software and solutions. The results of the acquisition are reported within the Americas segment. Source: 10-k

Under Normal Circumstances, New Products Announced To Bring Net Sales Growth

I believe that the company’s international exposure will most likely bring less sales growth volatility than that of competitors. In addition, the company’s new product and services announced in the last annual report in 2024 could serve as net sales catalysts.

Our geographic mix and the diversity of our portfolio, coupled with our large installed product base, provides growth opportunities from replacement demand and within our service revenue stream. In addition, we are investing substantial resources to innovate and develop new products and services which we expect to drive future growth. Source: 10-k

Cash Flow Expectations Under My Base Case Scenario

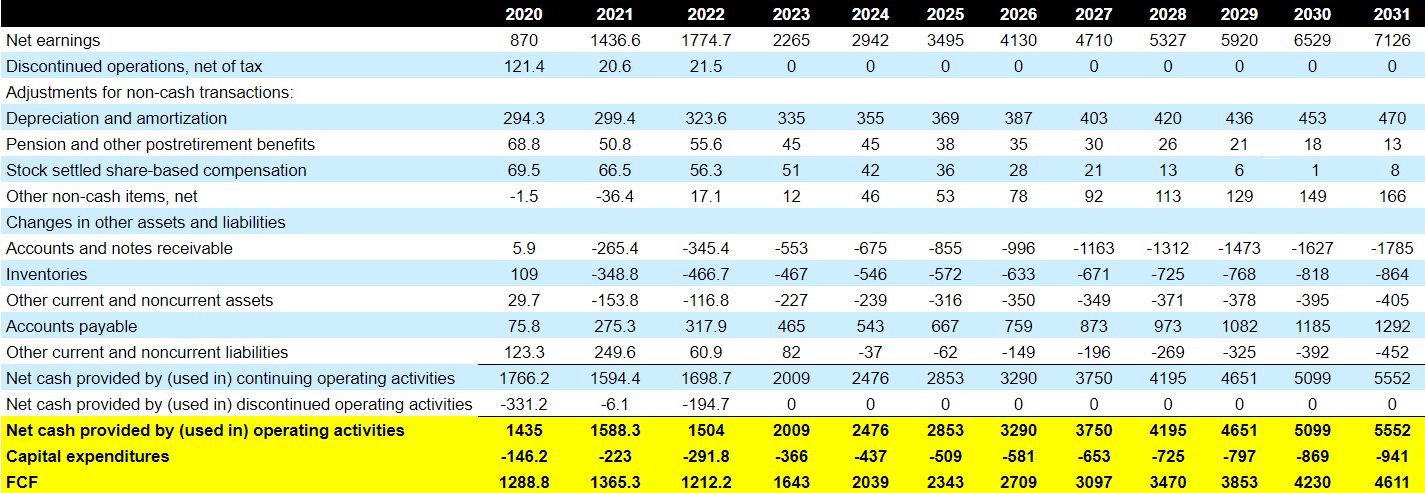

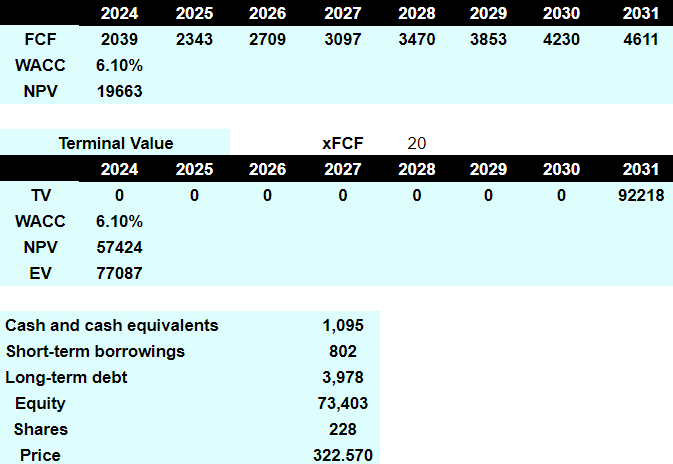

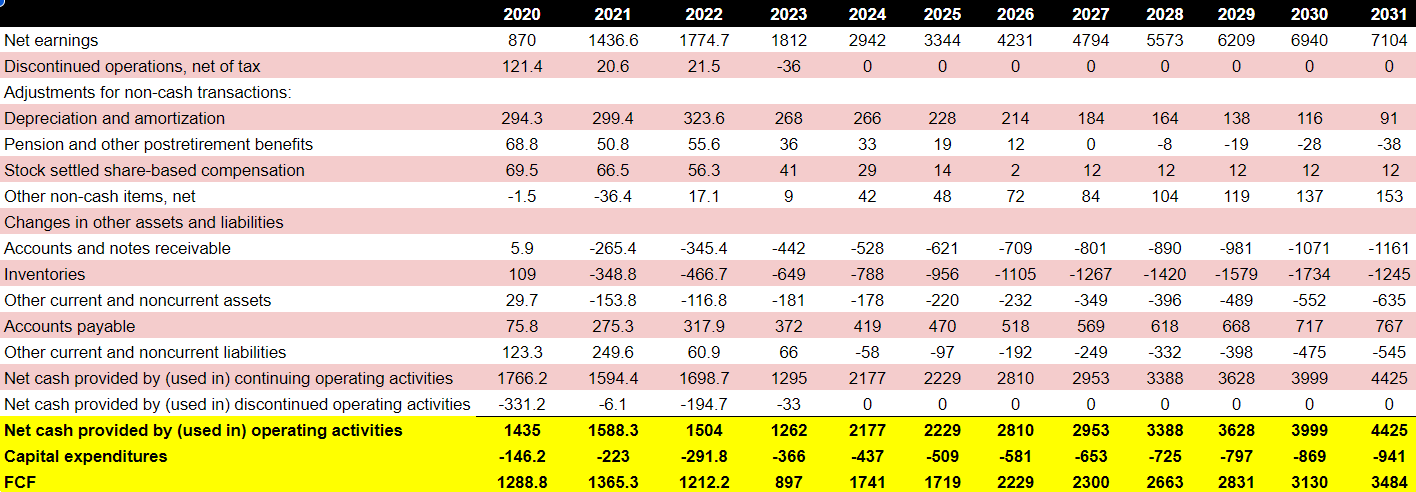

Under this scenario, I included net earnings worth $7.126 billion, with 2031 depreciation and amortization of about $469 million, pension and other postretirement benefits close to $12 million, and stock settled share-based compensation of $9 million. In addition, with 2031 accounts and notes receivable close to -$1786 million, changes in inventories of about -$864 million, changes in accounts payable of $1.291 billion, and CFO worth $5552 million. Finally, with 2031 capital expenditures of close to -$942 million, 2031 FCF stood at $4.610 billion.

Source: My Cash Flow Expectations

Under this scenario, I also assumed a WACC of 6.15%, Ev/ 2031 FCF of 20, which implied an enterprise value of 77.0875 billion, and forecast price of $322.5.

Source: DCF Model

Risks

In my view, the impact on global supply chains could bring complications to Trane, not only due to the arrival of parts for product development, but mainly because part of its services are associated with this industry. Under my bearish case scenario, I assumed that the supply chain crisis may bring lower net FCF margin growth.

On the other hand, I assumed that the possible new regulations that appear around the application of these company’s services based on their growth could condition future cash flow statements. Just as we can point out the risks associated with its tax domicile in Ireland while the bulk of its income comes from US territory.

Under my bear case scenario, I also assumed that transport refrigeration markets may continue to bring lower demand, and net sales growth may diminish. The company made a point about these effects in the last annual report.

Transport refrigeration markets are experiencing lower demand as customers adjust to lower freight rates. Source: 10-k

Finally, I believe that wage and energy inflation, which impacted the cash flow statement in 2023 may continue to damage future net sales growth. In addition, I believe that dramatic changes in the labor conditions, or demands in Europe, or any other region where the company operates is quite likely.

We continue to see material, wage and energy inflation impact our cost structure. Source: 10-k

Cash Flow Expectations Under My Bear Case Scenario

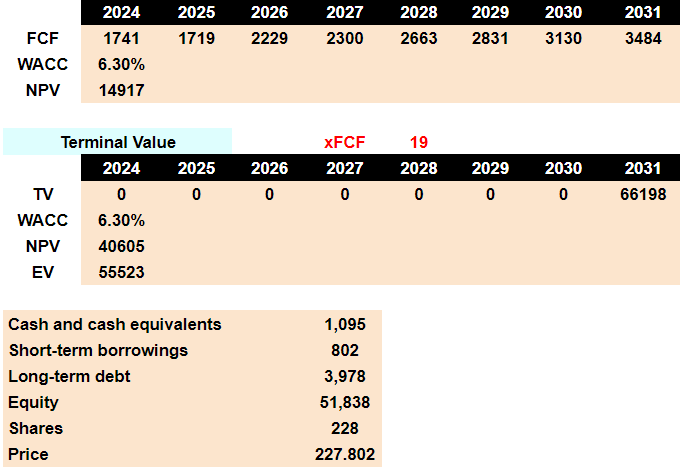

Under my bearish case scenario, I assumed 2031 net earnings of close to $7.104 billion, 2031 depreciation and amortization of close to $91 million, 2031 pension and other postretirement benefits of about -$39 million, and stock settled share-based compensation worth $12 million.

In addition, with other non-cash items of $152 million, 2031 changes in accounts and notes receivable of -$1162 million, changes in inventories -$1245 million, and changes in accounts payable of $766 million. Finally, with net cash provided by operating activities of $4.425 billion, and 2031 capital expenditures of -$942 million, 2031 FCF would be $3.484 billion.

Source: My Cash Flow Expectations

With the previous results, a WACC of 6.3%, Ev/ 2031 FCF of 19x the implied equity valuation would be close to $51.8 billion. If we also divide by the share count the implied fair price would be $227 per share.

Source: DCF Model

Competitors

The competition is broad and differentiated by region, with participants with international reach such as Trane and other service providers that serve a particular area independently.

In any case, competition is higher in relation to less specialized services, while in the offer of sustainability solutions the number of participants is reduced. Trane is one of the largest global manufacturers of HVAC ventilation systems and a major participant in the refrigerated freight transportation markets.

Conclusion

Trane Technologies recently delivered beneficial guidance for 2024, announced the development of new products, and communicated significant ESG efforts. Besides, considering the acquisition of MTA S.p.A, Helmer Scientific Inc, and Nuvolo Technologies Corporation in 2023, and recent decline in the net debt/EBITDA levels, I think that we may see further inorganic growth in the future. Even taking into account risks from supply chain issues, changing labor conditions, inflation, or failed M&A efforts, Trane does look a bit undervalued. Under my DCF models, I believe that there is more upside potential in the stock valuation than downside risks.

Q2 2024 Earnings Call Transcript")