princessdlaf

Wisdom Tree’s US Large-Cap Dividend ETF (NYSEARCA:DLN) is intended to complement or replace other large-cap value and/or dividend-oriented ETFs. DLN does provide a monthly income stream, but compared to dividend-paying ETFs like SPDR S&P Dividend ETF (SDY), Schwab US Equity Dividend ETF (SCHD) and Wisdom Tree US Small-Cap Quality Dividend ETF (DGRS), its dividend yield and dividend growth rate languishes. For these reasons, we rate DLN a Hold.

DLN’s Stock Selection Criteria

This passively managed ETF’s investment criteria are rather basic. For this diversified ETF of around 300 companies, a stock makes it in the screening process if 1) Dividends have been paid regularly over the last 12 months 2) Market cap is $100 million or greater and 3) Median daily trading dollars is at least $100 thousand.

Composition and Diversification

While this ETF is well diversified with roughly 300 companies, DLN weighs companies in the ETF by dividend streams. This ensures a decent concentration in the technology sector, which outperformed in 2023 and tempers the financial allocation, which did not outperform. Below is a chart comparing sector concentrations of DLN and the Russell 1000 Value proxy (IWD), which Wisdom Tree uses as its secondary benchmark to the EFT and trackable benchmark compared to its propriety benchmark Wisdom Tree US Large Cap Dividend Index (WTDGI). Note DLN is significantly overweight Technology and Consumer Defensives while underweight Financials and Industrials relative to IWD.

| Holdings | DLN | IWD |

| Technology | 20% | 11% |

| Financials | 16% | 21% |

| Health Care | 15% | 15% |

| Consumer Defensives | 14% | 8% |

| Industrials | 9% | 14% |

| Energy | 8% | 8% |

| Consumer Cyclicals | 6% | 5% |

| Real Estate | 5% | 5% |

| Utilities | 4% | 5% |

| Communication | 2% | 5% |

| Basic Materials | 1% | 4% |

*Source Seeking Alpha

Top 10 Holdings

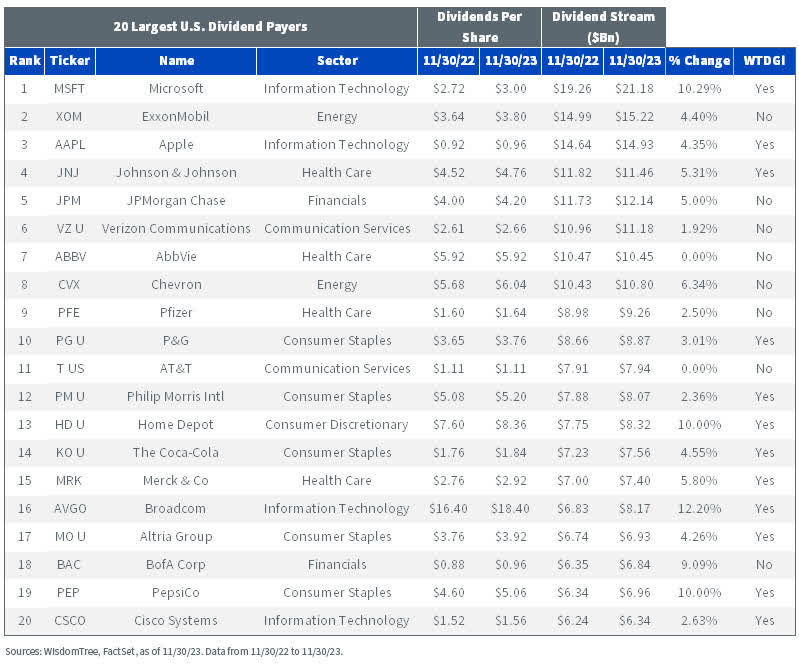

Of further interest, DLN’s top 10 holdings represent 27% of the fund’s holdings. As you can see by reviewing the two following charts, all of DNL’s top ten holdings, with the exception of NVDIA (NVDA), are one of the top 20 dividend payers of US companies by dividend income stream.

| Microsoft (MSFT) | 4% |

| Apple (AAPL) | 3% |

| JPMorgan Chase (JPM) | 3% |

| AbbVie (ABBV) | 3% |

| Broadcom (AVGO) | 3% |

| Johnson & Johnson (JNJ) | 3% |

| Exxon Mobil (XOM) | 2% |

| Procter & Gamble (PG) | 2% |

| Home Depot (HD) | 2% |

| NVDIA (NVDA) | 2% |

| TOTAL | 27% |

*Source Seeking Alpha

20 Largest US Dividend Payers (WisdomTree, FactSet)

Large Cap vs Small Cap Valuation Gap

Large-cap stocks have significantly outperformed small-caps the last several years, if not decades. The 2023 S&P 500 total return, in particular, was driven by the success of mega-cap stocks denoted as the Magnificent 7 (Apple (AAPL), Alphabet (GOOGL), Microsoft (MSFT), Amazon (AMZN), Meta Platforms (META), Tesla (TSLA), Nvidia (NVDA). While the Mag 7 average 2023 performance was 111%, other index sectors struggled to return 24% or less.

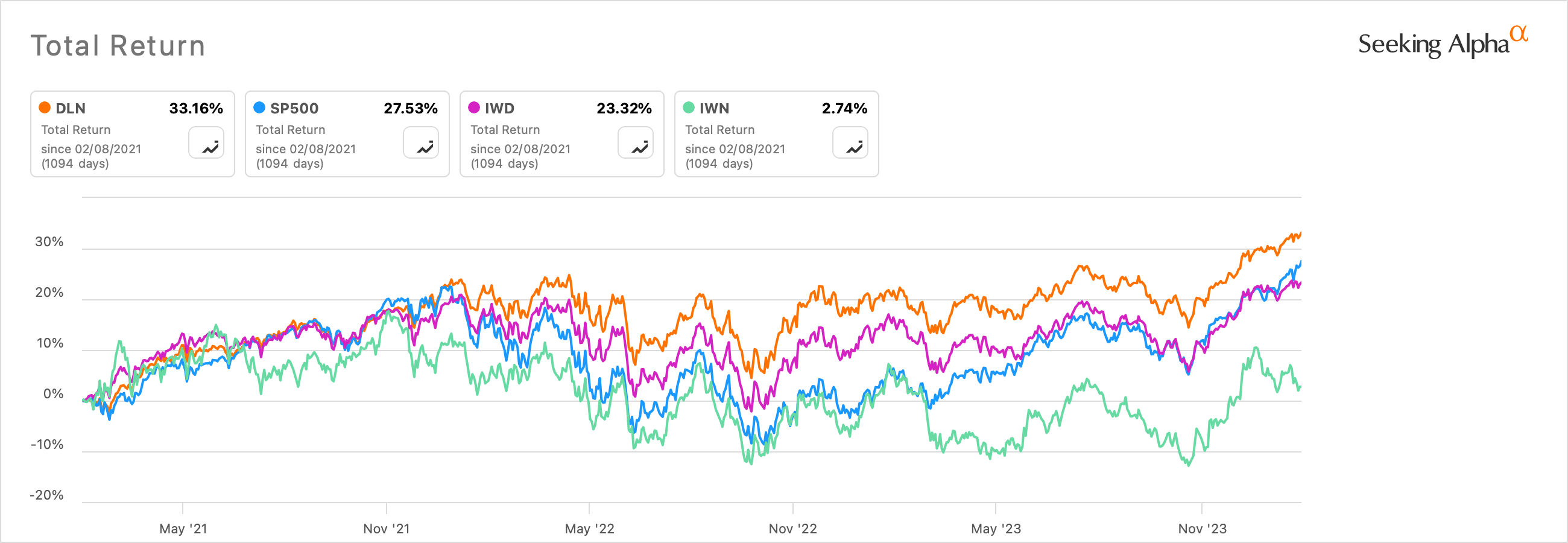

The chart below demonstrates the overperformance of large-caps relative to small-caps over the last 3 years using the Russell 2000 Index, as represented by iShares Russell 2000 Small Cap Value ETF (IWN), compared to the large-cap companies represented by the S&P 500 and the Russell 1000 Index, represented by iShares Russell 1000 ETF (IWD), in addition to DNL.

3YR Total Return Lg Cap vs Small Cap (Seeking Alpha)

In addition to the poor relative performance of small-caps to large-caps, a large valuation gap now exists between large- and small-cap stocks. Since the second half of 2000, the TTM P/E ratio of the Russell 2000 Index has been roughly 98% of the S&P 500 Index’s same metric. However, in June 2000 an anomaly developed where the Russell 2000 traded at only 51% of the S&P 500 P/E. As of last quarter, the valuation gap is again at 59%. Therefore, we believe there is an opportunity for multiple expansion growth in small-caps versus large-caps. For this reason, we believe small-caps have a better chance of overperformance in 2024 than large-caps, further supporting our Hold on DLN.

Another reason for the poor performance of small-caps is the continuing long-lasting inverted yield curve, which is often regarded as a recession indicator. This has supported investors’ desire to hold large-cap stocks relative to small-caps. Larger companies can typically withstand economic downturns better than smaller ones and have added liquidity to weather large drawdowns. Many small-cap companies have been disadvantaged in the lending market as many rely more heavily on floating-rate loans and private equity than large-cap stocks. However, we believe moderating inflation can continue the hiatus of Fed interest rate hikes and believe rate cuts will be part of the Fed policy in 2024. There is, however, always a risk that unforeseen macro events could change our interest rate outlook.

Summing it Up

While DLN is a well-diversified US large-cap dividend-paying ETF, its dividend yield (2.4%), hence income generation, is not as strong as its competition (SDY, SCHD), which ranges between 2.7% and 3.5%. In addition, based on the deep valuation gap between large and small caps as well as the relative overperformance of large caps over the last several years, we believe the small-cap play has a better chance of overperformance in 2024. Therefore, we rate DLN a Hold.

Risks to Investment Thesis

Unforeseen geopolitical and macroeconomic risks could play out making us possibly revert to holding large-cap ETFs as a safe haven as investors often remain in the large-cap space in uncertain times. Thus, we may review our outlook of DLN. In addition, if inflation proves to be stickier than expected and the predicted Fed cuts do not happen, we would likely want to be more heavily invested in large-caps than in the small-cap space as higher rates puts increased pressure on the capitalization structure of smaller companies relative to larger ones.

Q2 2024 Earnings Call Transcript")