kate_sept2004

Investment Thesis

The existing composition of our investment portfolio plays a crucial role in guiding the selection process of potential additions.

Nonetheless, there are certain companies that, in my opinion, are versatile enough to align with various investment strategies and can therefore be included in diverse investment portfolios. Among these companies are Realty Income (NYSE:O) and U.S. Bancorp (NYSE:USB), which stand out due to their effective combination of dividend income and dividend growth, in addition to their currently attractive Valuation.

While I suggest overweighting Realty Income in a long-term oriented dividend portfolio, due to the company’s reduced risk-level and attractive Valuation (which leads to an increased likelihood of reaching an attractive Total Return), I suggest underweighting U.S. Bancorp, given its higher risk exposure.

I am following the same strategy with The Dividend Income Accelerator Portfolio, in which Realty Income holds a predominant position (currently representing 3.09% of the overall portfolio), while U.S. Bancorp represents a smaller percentage of 0.63% (due to the portfolio’s stake in Schwab U.S. Dividend Equity ETF (NYSEARCA:SCHD)) .

With these strategic allocations, both Realty Income and U.S. Bancorp effectively contribute to optimizing The Dividend Income Accelerator Portfolio’s risk-reward profile.

In comparison to U.S. Bancorp, JPMorgan (NYSE:JPM) and Bank of America (NYSE:BAC) come attached to a lower risk level (while the three have similar Valuations). Therefore, I suggest overweighting them within a long-term investment portfolio, as opposed to U.S. Bancorp.

It is important to note that both Realty Income and U.S. Bancorp effectively combine dividend income and dividend growth, given their Dividend Yields [FWD] of 5.68% and 4.80% respectively, and their 3 Year Dividend Growth Rates [CAGR] of 4.16% and 4.73%. Therefore, both can be important strategic additions to your dividend portfolio during this month of February.

Furthermore, it is worth noting that both have an attractive Valuation at this moment in time, as evidenced by their P/AFFO [FWD] Ratio and P/E [FWD] Ratio, which stand below the Sector Median.

In addition, I believe that both Realty Income and U.S. Bancorp pay sustainable dividends, which can help you to invest with a reduced risk level, thus elevating the chances of reaching successful investment outcomes.

Before diving deeper into these two companies, I would like to repeat the general benefits of including high dividend yield companies into your investment portfolio.

General Benefits of Investing in High Dividend Yield Companies

- The Generation of Income: Dividend paying companies bring you the enormous benefit of helping you to produce income. This provides you with much higher financial flexibility and offers the enormous benefit of not having to sell some of your stocks when you might need some extra money at a time when the market is not in your favor.

- Significant Reduction of the Volatility and Risk Level of Your Overall investment Portfolio: Companies that pay a relatively high and particularly sustainable dividend, tend to come attached to a lower risk level, particularly when compared to growth companies, thus contributing to reducing the volatility and overall risk level of your investment portfolio (their lower risk level can be reflected in their lower Beta Factor).

- Psychological Investor Benefits in Times of a Stock Market Decline: In times of high volatility and declining stock markets, receiving dividend payments can bring you a psychological effect that can lead you to keep the positions in your portfolio to continue benefiting from dividend payments, acting like a business owner, instead of a stock market trader. This behavior can help you to significantly increase your wealth over the long term.

Realty Income

Realty Income is a real estate investment trust (“REIT”) with a portfolio of 1,324 clients from 85 different industries. The company has a strong balance sheet, evidenced by an A3 credit rating from Moody’s. Its extensively diversified product portfolio includes 13,282 commercial real estate properties, underscoring the company’s ability to successfully mitigate risks.

Realty Income’s Current Valuation

Different metrics suggest that Realty Income is presently undervalued: the company’s P/AFFO [FWD] Ratio currently stands at 13.56, which is 6.94% below the Sector Median. In addition, it can be highlighted that Realty Income’s current Dividend Yield [FWD] of 5.68% is 16.97% above the Sector Median of 4.86%, further indicating that it is undervalued at this moment in time. Moreover, Realty Income currently receives a B- rating in terms of Valuation as according to the Seeking Alpha Factor Grades, underscoring that the company is undervalued.

Realty Income’s Dividend and its Combination of Dividend Income and Dividend Growth

Realty Income has shown 26 Consecutive Years of Dividend Growth (while the Sector Median is only one year). The company’s enormous potential to provide investors with dividend growth is further underlined by a 10 Year Dividend Growth Rate [CAGR] of 3.81% in combination with its FFO Growth Rate [FWD] of 12.48%, which is significantly above the Sector Median of 4.28%.

With an Annual Payout [FWD] of $3.08, Realty Income presently pays a Dividend Yield [FWD] of 5.68%. The sustainability of the company’s Dividend is underscored by its Payout Ratio of 73.92%, in combination with its EPS Diluted Growth Rate [FWD] of 20.90%.

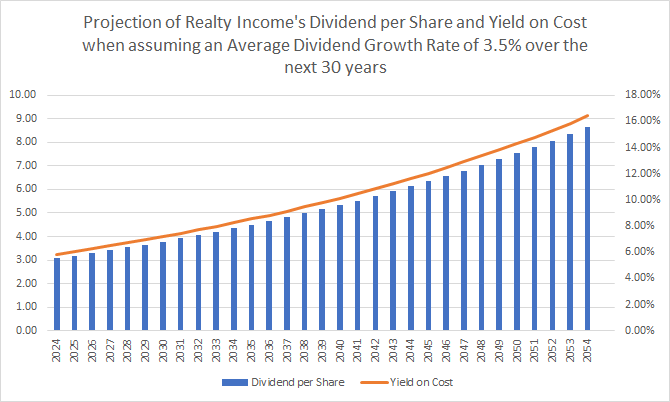

The Projection of Realty Income’s Dividend and its Yield on Cost

The chart below illustrates a projection of Realty Income’s Dividend and Yield on Cost when factoring in the company’s present stock price and assuming an Average Dividend Growth Rate of 3.5% over the next 30 years. This projection is grounded in the company’s 10 Year Dividend Growth Rate [CAGR] of 3.81%.

Source: The Author

The graphic illustrates the potential to achieve a Yield on Cost of 8.25% by 2034, 11.64% by 2044, and 16.42% by 2054. It highlights that Realty Income is an attractive option for investors looking to combine steady dividend income with dividend growth.

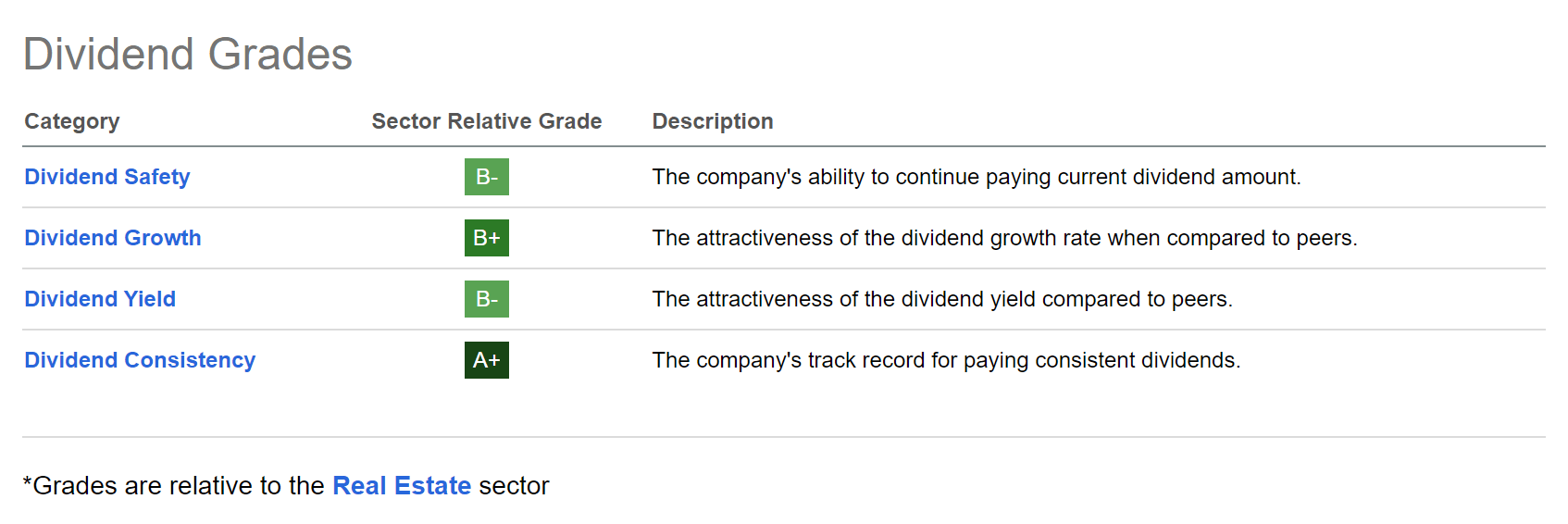

Realty Income According to The Seeking Alpha Dividend Grades

According to the Seeking Alpha Dividend Grades, Realty Income has an A+ rating for Dividend Consistency, while it receives a B+ rating for Dividend Growth. For both Dividend Yield and Dividend Safety, Realty Income gets a B- rating.

Source: Seeking Alpha

These ratings further emphasize Realty Income’s proficiency to effectively combine dividend income with dividend growth.

U.S. Bancorp

Founded in 1863, U.S. Bancorp is a financial services holding company that boasts an A3 credit rating from Moody’s and currently pays a Dividend Yield [FWD] of 4.80%.

Given the bank’s proven capability of delivering growth in dividends to its shareholders, it offers an attractive mix of steady dividend income and the potential for dividend growth. This makes the bank an attractive choice for long-term investors that seek to combine stability and growth at the same time.

U.S. Bancorp’s Current Valuation

Considering U.S. Bancorp’s current stock price, it exhibits a P/E GAAP [FWD] Ratio of 10.44, which is 3.84% below the Sector Median and 12.66% below its 5-year average. Both metrics suggest that U.S. Bancorp is presently undervalued and that investors can invest with a margin of safety.

It is also noteworthy that the bank’s Price/Book [FWD] Ratio of 1.22 is 19.12% lower than its average from the past 5 years of 1.51, underscoring its current undervaluation.

U.S. Bancorp’s Dividend and its Combination of Dividend Income and Dividend Growth

Several metrics underline that U.S. Bancorp is an attractive pick in terms of dividend growth: the bank’s 10 Year Dividend Growth Rate [CAGR] stands at 8.11%, which is above the Sector Median of 7.89%. The company’s EPS Diluted Growth Rate [FWD] lies at 5.65%, significantly exceeding the Sector Median of 0.88%.

With its Annual Payout Ratio of $1.96, the U.S. bank presently pays a Dividend Yield [FWD] of 4.80%. This Dividend Yield is not only 38.61% above the Sector Median, but also 22.99% above its average over the past 5 years.

Both are additional indicators that confirm U.S. Bancorp’s undervaluation, and strengthen my thesis that the bank is presently an attractive pick to be added to a long-term investment portfolio that aims to combine dividend income and dividend growth.

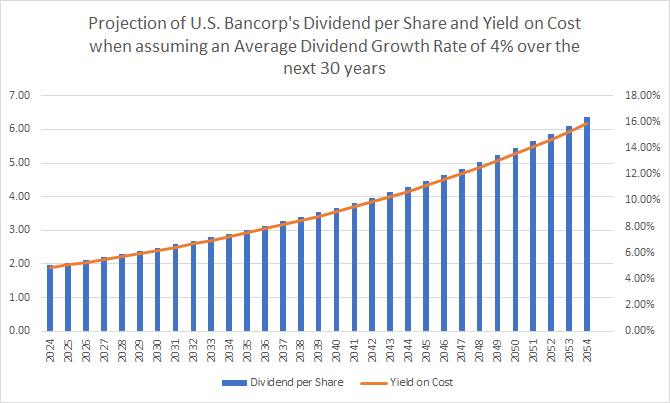

The Projection of U.S. Bancorp’s Dividend and its Yield on Cost

The graphic below presents a forecast of U.S. Bancorp’s Dividend and Yield on Cost based on an assumed Average Dividend Growth Rate of 4% over the following 30 years. This projection is based on the company’s 3 Year Dividend Growth Rate [CAGR] of 4.73%.

Source: The Author

The graphic shows that you could reach a Yield on Cost of 7.24% by 2034, 10.71% by 2044, and 15.85% by 2054, further highlighting the bank’s attractiveness for investors looking for ways to combine dividend income with dividend growth.

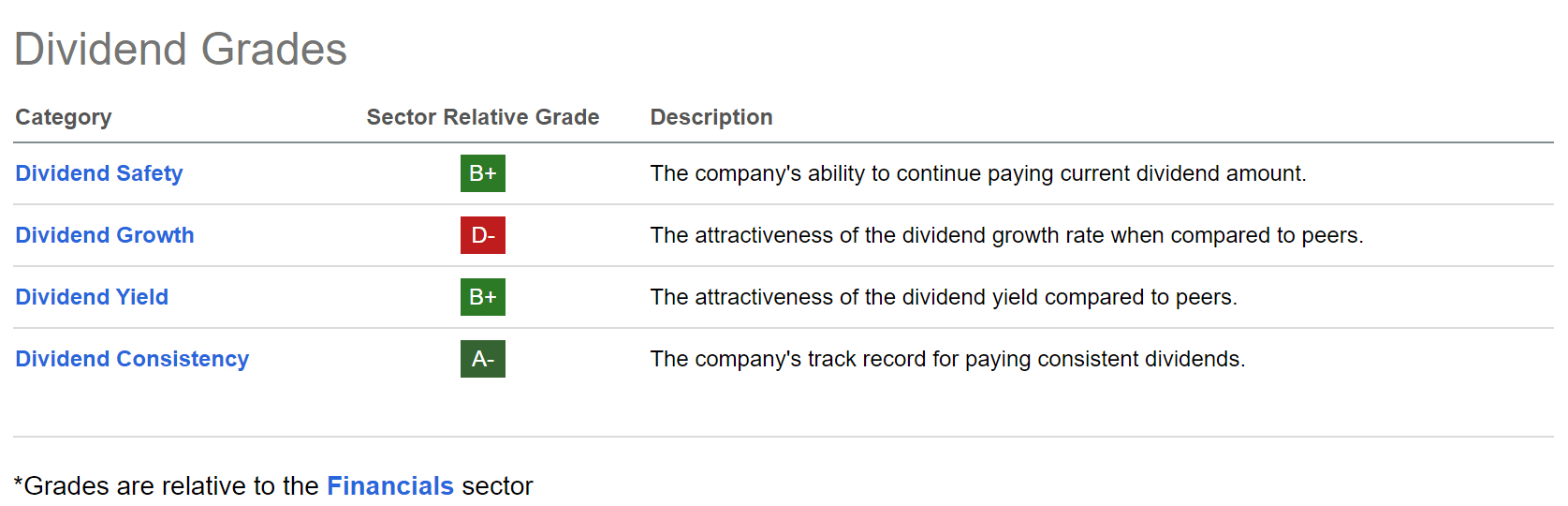

U.S. Bancorp According to The Seeking Alpha Dividend Grades

According to the Seeking Alpha Dividend Grades, U.S. Bancorp receives an A- rating for Dividend Consistency, while it receives a B+ for both Dividend Yield and Dividend Safety, underscoring its attractiveness for dividend income investors.

Source: Seeking Alpha

Risk Analysis

A risk analysis of a stock is crucial for investors, since a company with a low risk level offers an enhanced probability of delivering successful investment outcomes. On the other hand, companies with a high-risk level often tend to present a reduced chance of favorable investment returns. This is mainly because they are subject to more uncontrollable factors, thus reducing the prospects for attractive investment results.

Risk Analysis – Realty Income

The Reduced Risk Level of an Investment in Realty Income

An investment in Realty Income appears to hold a comparatively low level of risk. This assessment is underlined by the company’s strong balance sheet, evidenced by its A3 credit rating from Moody’s, strong dividend track record, and extensively diversified product portfolio.

Nonetheless, adverse market conditions pose a potential threat to Realty Income’s existing clientele, which could adversely impact the company’s financial operations.

It is noteworthy that Realty Income has a high-quality portfolio of clients, with no single client constituting more than 4% of the total portfolio. This shows that the bankruptcy of any individual client would have a significantly reduced impact on Realty Income’s financial health.

It is further worth highlighting that the company reaches a strong industry diversification, since no industry represents more than 11.4% of the overall contractual rent, once again, underscoring its ability to mitigate industry-specific concentration risk.

Reducing Portfolio Risk When Investing in Realty Income for Improved Investment Outcomes: The Case for a 5% Allocation Limit and for a Long-Term Investment Approach

Due to the relatively low risk level of an investment in Realty Income in addition to its currently attractive Valuation, I suggest overweighting the company in a long-term oriented investment portfolio. However, I suggest limiting the position to a maximum of 5% of your overall portfolio, ensuring a lowered company-specific concentration risk.

Risk Analysis – U.S. Bancorp

The Elevated Risk Level of an Investment in U.S. Bancorp

For a diverse number of reasons, I firmly believe that the overall risk level of an investment in U.S. Bancorp is higher when compared to larger banks like Bank of America or JPMorgan.

I am of the opinion that Bank of America and JPMorgan are the superior options when it comes to Profitability: Bank of America exhibits a Net Income Margin [TTM] of 28.15%, while JPMorgan’s is 33.93%. In comparison, U.S. Bancorp presents a lower Net Income Margin [TTM] of 21.09%, underscoring the superior Profitability metrics of Bank of America and JPMorgan and their reduced risk level when compared to U.S. Bancorp.

Furthermore, both JPMorgan and Bank of America have a superior A1 credit rating from Moody’s when compared to U.S. Bancorp’s A3 credit rating from the same agency, once again, underlying their reduced risk exposure.

The significantly lower risk level of Bank of America and JPMorgan strengthens my confidence to overweight both in a broadly diversified dividend portfolio, while only underweighting U.S. Bancorp due to its elevated risk exposure.

Reducing Portfolio Risk When Investing in U.S. Bancorp for Improved Investment Outcomes: The Case for a 2.5% Allocation Limit and for a Long-Term Investment Approach

Due to the elevated risk level of an investment in U.S. Bancorp, I suggest limiting its position to a maximum of 2.5% of your investment portfolio. This strategy helps you to maintain a reduced risk level for your overall investment portfolio, striving to reach an attractive Total Return with a high likelihood.

Maximizing Investor Benefits when Investing in Realty Income and U.S. Bancorp

In my opinion, by including Realty Income and U.S. Bancorp in a diversified dividend portfolio with a reduced risk level, investors can maximize their investment benefits. This is even more the case if such a portfolio successfully balances dividend income and dividend growth.

The Dividend Income Accelerator Portfolio is a diversified dividend portfolio that allows investors to invest with a reduced risk level through extensive diversification across companies, sectors and industries, as well as its inclusion of companies that pay sustainable dividends while effectively blending dividend income with dividend growth.

Through the portfolio’s strategic composition, you can generate a substantial and annually increasing extra income via dividend payments.

The Reasons for Incorporating Realty Income Into The Dividend Income Accelerator Portfolio

Realty Income provides a strategically important component of The Dividend Income Accelerator Portfolio, presently accounting for 3.09% of the overall investment portfolio.

I have added Realty Income due to the company’s significant competitive advantages, its positive growth perspective, reduced risk level, attractive Valuation, and its combination of dividend income with dividend growth, effectively aligning with the investment strategy of The Dividend Income Accelerator Portfolio:

Realty Income: A Strong Alignment With The Dividend Income Accelerator Portfolio Approach

Why U.S. Bancorp Is an Attractive Candidate for Potential Inclusion Into The Dividend Income Accelerator Portfolio

The Dividend Income Accelerator Portfolio is still not directly invested in U.S. Bancorp, only indirectly via Schwab U.S. Dividend Equity ETF.

Due to its stake in Schwab U.S. Dividend Equity ETF, U.S. Bancorp currently accounts for 0.63% of the overall portfolio, representing a relatively small percentage.

I will consider including U.S. Bancorp into The Dividend Income Accelerator Portfolio within the following weeks as an individual position. This is due to its attractive combination of dividend income and dividend growth, in addition to having a presently attractive Valuation.

However, when adding U.S. Bancorp to The Dividend Income Accelerator Portfolio as a single position, I plan to continue underweighting the U.S. bank within the portfolio. Doing so follows my suggestion of limiting the position to a maximum of 2.5% of the overall portfolio, providing investors who follow the investment approach of The Dividend Income Accelerator Portfolio with a reduced risk level. This then leads to an elevated likelihood of reaching an attractive Total Return when investing over the long term.

Conclusion

I firmly believe that both Realty Income and U.S. Bancorp are presently attractive choices to be incorporated into a diversified dividend portfolio.

Both pay an attractive Dividend Yield [FWD] of 5.68% and 4.80% respectively, have shown significant dividend growth in recent years (3 Year Dividend Growth Rates [CAGR] of 4.16% and 4.73% respectively), and have attractive Valuations (their P/AFFO [FWD] Ratio and P/E [FWD] Ratios stand below the Sector Median).

Incorporating both Realty Income and U.S. Bancorp in a broadly diversified dividend portfolio with a reduced risk level, such as The Dividend Income Accelerator Portfolio, offers you multiple benefits: it allows you to generate a substantial amount of annually increasing extra income through dividend payments, while, at the same time, it allows you to reach an attractive Total Return with a high likelihood.

By overweighting Realty Income in your dividend portfolio (while not providing it with more than 5% of your overall investment portfolio to reduce company-specific allocation risks), and underweighting U.S. Bancorp (while not providing it with more than 2.5% of your overall portfolio), you strategically position your portfolio to reach an attractive risk-reward profile.

I suggest the implementation of an investment approach, in which JPMorgan and Bank of America represent a larger percentage of the overall portfolio when compared to U.S. Bancorp, given their lower risk-level (while all three have similarly attractive Valuations). This strategy allows for further improvement and to optimize the risk-reward profile of your dividend portfolio.

Author’s Note: Thank you for reading! I would appreciate hearing your thoughts on this article on Realty Income and U.S. Bancorp. Which high dividend yield companies are you considering investing in during this month of February?

Q2 2024 Earnings Call Transcript")