JuSun

Most people who track the market today know that growth stocks are back in favor again, especially the large cap ones, which have outside influence on the S&P 500 (SPY) as the index flirts with all-time highs. At the same time, many investors know that income stocks are again out of favor with the market as the market chases growth.

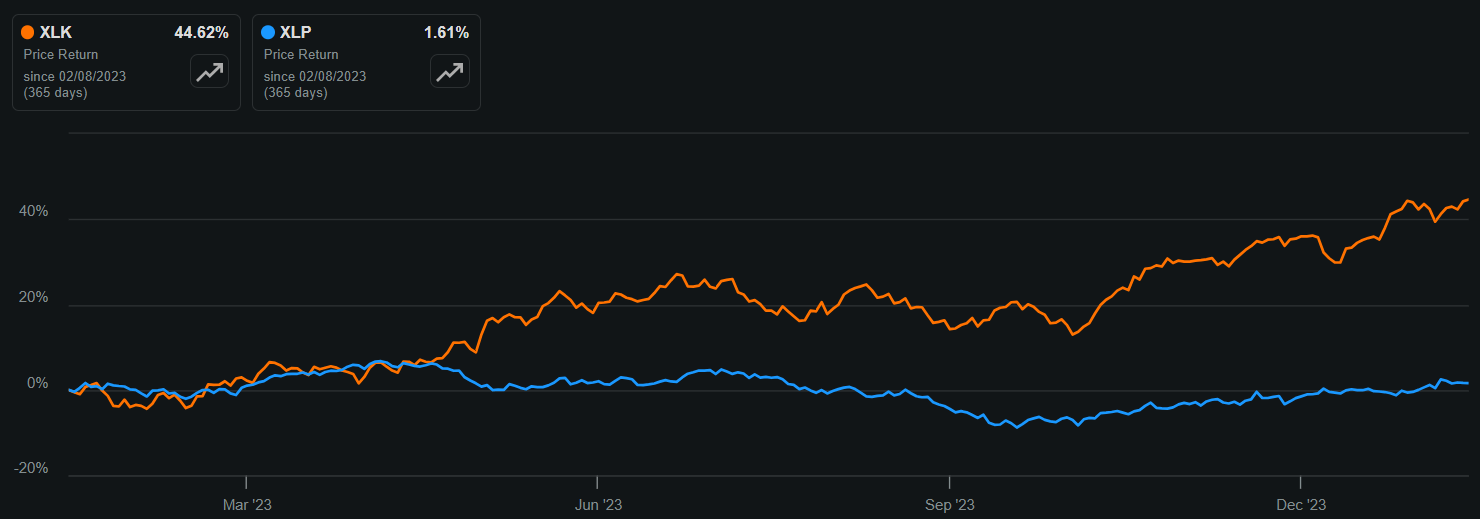

As shown below, the divergence between the SPDR Technology Sector ETF (XLK) and SPDR Consumer Staples ETF (XLP) over the past 12 months has become fairly wide, with a 43% price gap over this timeframe.

XLK vs. XLP 1-Yr Price Return (Seeking Alpha)

This is what I would call “everyone knows” investing, a term coined by famed value investor Howard Marks. The point that he made is that this style of investing isn’t helpful for someone who follows the general trend of buying growth and selling value. This could result in disappointment, since market prices already reflects sentiment, which can quickly change should growth stocks disappoint and value stocks impress investors.

This brings me to Kenvue (NYSE:KVUE), which I haven’t covered before, but yet find the valuation to be opportunistic. In this article, I visit this stock including its recent earnings results, and discuss why value and income investors ought to consider this moat-worthy name while it can be had at a decent price, so let’s get started!

KVUE Stock (Seeking Alpha)

Why KVUE?

Kenvue was once Johnson & Johnson’s (JNJ) consumer products segment before it was spun off into an independent entity in August of 2023. It carries a portfolio of 15 strong brands including Aveeno, BAND-AID, Listerine, Neutrogena, and Tylenol that generated $15.4 billion in net sales last year.

KVUE recently reported respectable 2023 results with net sales and organic sales growing by 3.3% and 5.0% YoY, respectively. However, fourth quarter sales were slightly disappointing, with net sales and organic sales both declining by 2.7% and 2.4% YoY, respectively. The fourth quarter decline was driven by 8.2% YoY volume declines, which were partially offset by 5.8% net price realization.

While the decline in fourth quarter sales was disappointing, it’s worth noting that a later than expected start to the cold and flu season due to warmer weather than last year, combined with some product discontinuations, were the primary drivers behind the volume decline compared to the prior year. These factors masked otherwise strong business fundamentals, including strong 8.4% organic growth in the self-care segment for the full year 2023, on top of 10.9% growth last year.

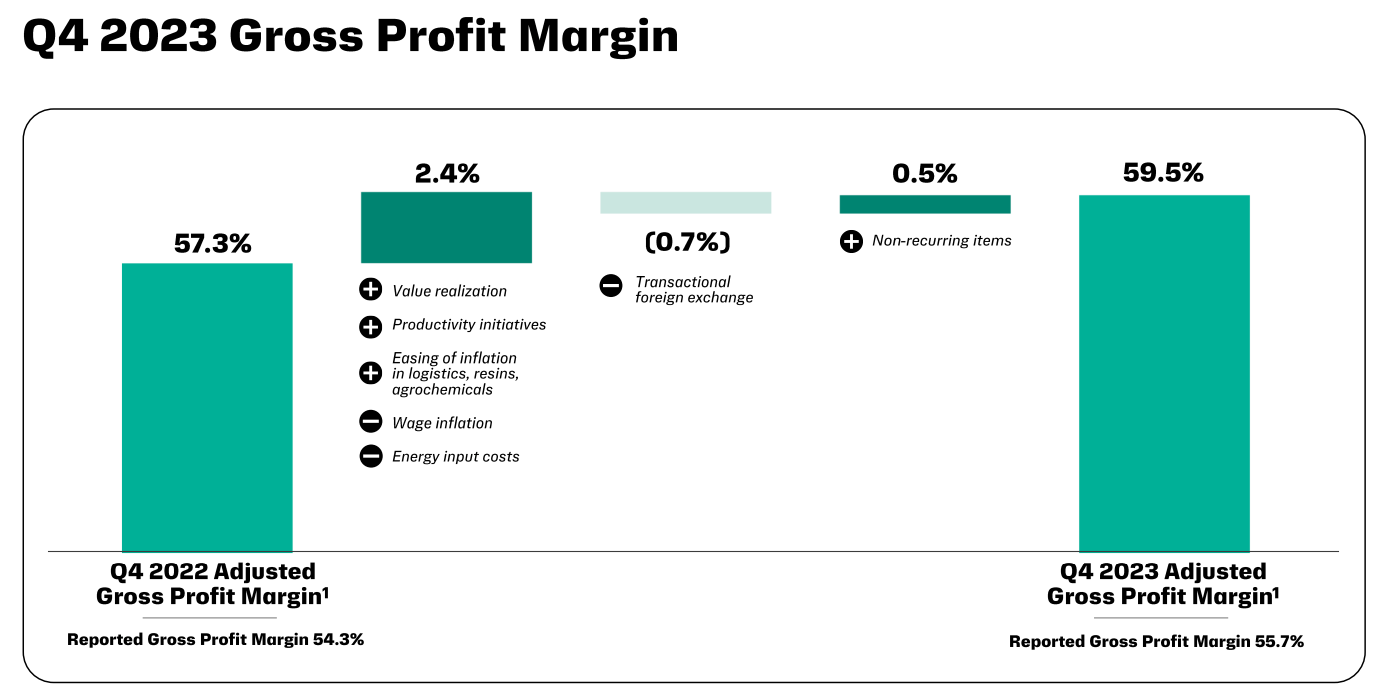

Moreover, Adult Tylenol continued to gain market share in the U.S. with 78 consecutive weeks of growth despite category share decline in a weaker cold and flu season compared to 2022. Also encouraging, Oral Care grew by 8% in 2023, driven by Listerine, which is seeing double digit growth even though its 5x larger than its next largest competitor. Growth in these types of premium brands combined with supply chain efficiencies helped to drive fourth quarter gross margin improvement of 230 basis points to 59.5%, as shown below.

Investor Presentation

Looking ahead to 2024, KVUE expects organic revenue growth in the 2% to 4% range through growth in its core brands and product innovation. This should include the recently launched Listerine gum therapy, which has reached 1% share of the oral care category in just 12 months after its launch. Other product innovations include Neutrogena Hydro Boost, which is seeing strong growth in EMEA and Latin America, the latter of which is seeing double-digit growth in the Neutrogena brand.

Risks to KVUE include potential for a weaker than normal flu season, which could suppress Tylenol sales. In addition, China sales have been disappointing and could continue to pose as a headwind due to recent concerns around deflation in the country. In addition, it will be up to management to turn around the Skin Health and Beauty segment in the U.S., which saw just 1.8% sales growth in 2023 due to in-store execution missteps.

Meanwhile, unlike some spin-offs that are saddled with debt from the parent company, KVUE carries a strong A credit rating from S&P. This is supported by reasonably low leverage with a net debt to TTM EBITDA of 2.3x, sitting well under the 3.0x level generally considered to be safe by ratings agencies.

This lends support to KVUE’s 4.1% dividend yield, which is well-covered by a 64% payout ratio. While KVUE has less than a year’s worth of dividend history, the fact that it was spun off from dividend aristocrat Johnson & Johnson makes it likely that management will be committed to shareholder returns with dividends being a centerpiece.

Turning to valuation, I find KVUE to be attractive after the recent post-earnings drop, at the current price of $19.33 with a forward PE of 15.6, sitting below the 18-22x range that I find to be fair for most moat-worthy consumer staples companies with strong brands.

While analysts expect a 4% EPS decline this year due to continued supply chain normalization and headwinds in China and the U.S. they expect for KVUE to resume bottom line growth thereafter with 3% to 7% annual EPS growth in the 2025 to 2027 timeframe. Plus, I believe that KVUE has the potential to surprise to the upside this year, considering the aforementioned brand innovations and potential for a turnaround in the Skin Health and Beauty segment in the U.S.

Investor Takeaway

In conclusion, Kenvue offers investors a unique opportunity to invest in a spin-off from Johnson & Johnson with strong brand names and balance sheet. While there are some short-term headwinds to consider, the current valuation coupled with the potential for long-term growth and a solid dividend make this stock an attractive option for value and income investors alike. As such, I view the current price as being an attractive entry point while market sentiment is working against the stock, and I Initiate a ‘Buy’ rating on KVUE.

Q2 2024 Earnings Call Transcript")