Eugene Mymrin/Moment via Getty Images

Investment thesis

Our current investment thesis is:

- We believe it is very unlikely Backblaze will be able to generate healthy shareholder returns. The company is losing money considerably while having long-term capex commitments. It must raise prices considerably, eliminating its competitive advantage, or find several hundred million dollars to fund further losses. The only realistic option is the former, which will decelerate growth before the business even reaches >$200m in revenue.

- At this scale, we struggle to see any value for shareholders. We suspect this business will be taken over, not necessarily at a level where shareholders win (particularly existing ones).

Company description

Backblaze (NASDAQ:BLZE) is a data storage and cloud backup service provider. Backblaze offers both personal and business cloud backup solutions, known for its simplicity, affordability, and commitment to data security.

Backblaze

Share price

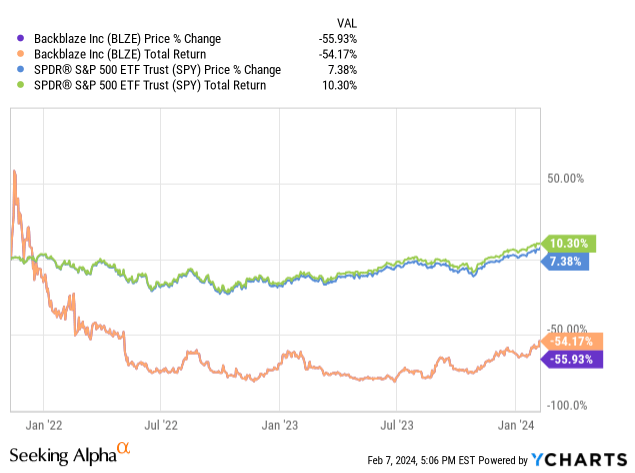

Backblaze’s share price performance has been disastrous, losing over 50% of its value in an incredibly short period of time. This is a reflection, in part, of timing given the current macroeconomic conditions, as well as its current financial progression.

Commercial analysis

Capital IQ

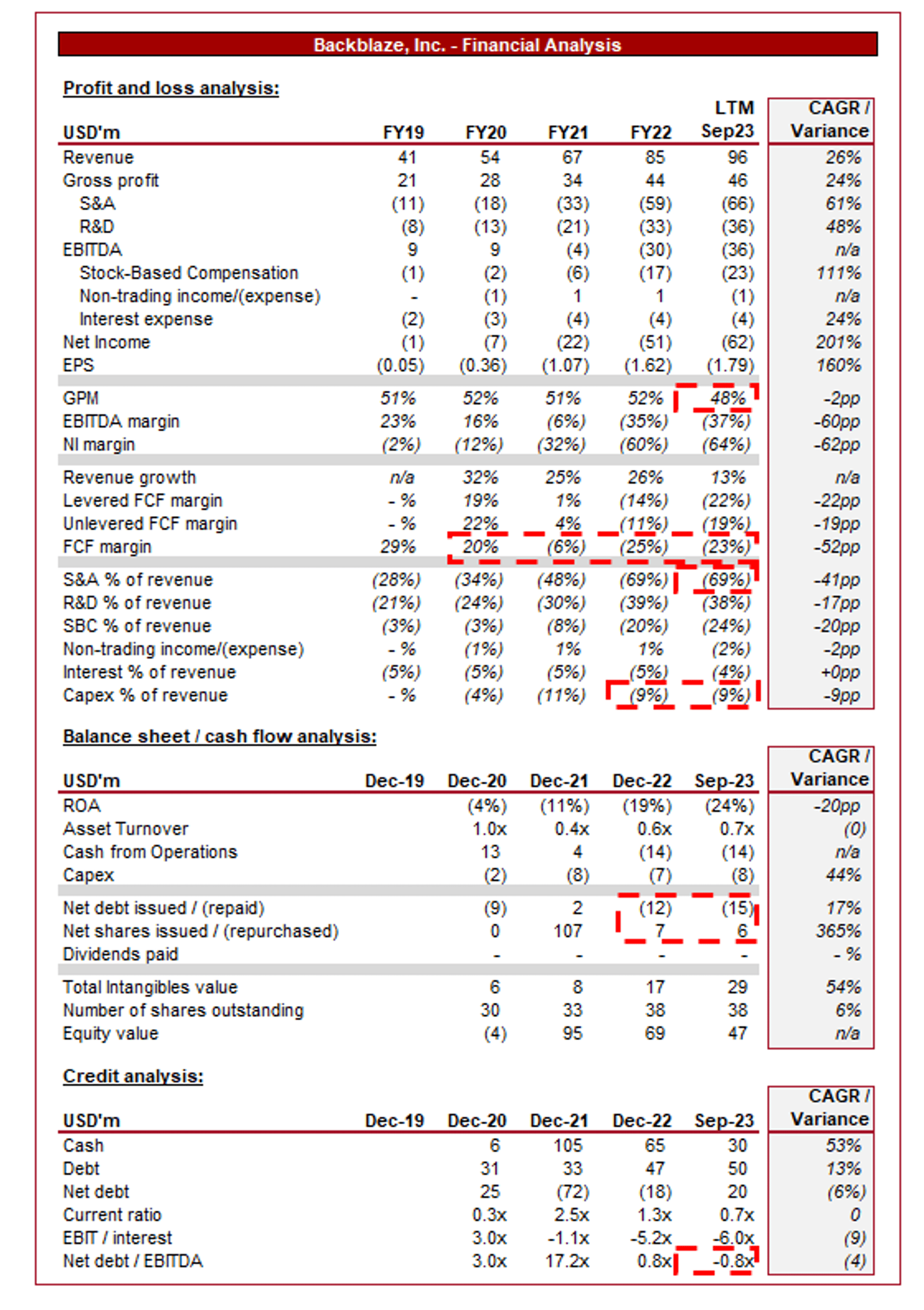

Presented above are Backblaze’s financial results.

The company has achieved strong growth in recent years, with a CAGR of +26% since FY19.

Backblaze

Business Model

Backblaze provides cloud backup services that enable individuals and businesses to securely store and access their data remotely. Customers install Backblaze’s software on their devices, which continuously backs up files to Backblaze’s data centers over the internet.

Backblaze offers unlimited cloud backup storage for a flat monthly or annual fee, which offers excellent value for customers, especially compared to traditional backup solutions that may charge based on storage usage or device count. Further, the company has added free egress (network fees levied by most for moving data on the cloud), a major pain point for clients.

This pricing model eliminates the need for customers to worry about storage limits or pay extra for additional storage space, providing simplicity and cost-effectiveness. This said, from the company’s perspective, it limits the scope for up-selling its customers, limiting its long-term growth potential.

Backblaze employs robust security measures to protect customers’ data, including encryption both in transit and at rest. Additionally, the company stores data redundantly across multiple geographically dispersed data centers, minimizing the risk of data loss due to hardware failures or natural disasters.

Backblaze is currently investing in R&D to improve its backup solutions, specifically focusing on speed, scalability, and security.

Competitive Positioning

We are not entirely convinced by Backblaze’s competitive position. The company’s current approach to gaining market share is through the following:

- Cost-Effective Pricing Model – Backblaze’s flat-rate pricing model appeals to budget-conscious customers who seek cost-effective backup solutions, particularly those smaller in size. This has allowed Backblaze to grow well but we are concerned that the company is limiting its long-term growth potential and is risking alienating customers with future price rises.

- Marketing – Backblaze is developing its brand reputation based on its affordability and the ability to try its services for free. Whilst this investment has been successful in drawing in customers, we are unsure if selling its services based on price is wise given the company is loss-making and so price increases are ahead.

From a secondary perspective, the company offers:

- Scalable Infrastructure – Backblaze’s scalable infrastructure enables it to accommodate the growing demand for cloud storage services efficiently.

- Continuous Innovation – Backblaze’s commitment to innovation ensures that its backup services remain competitive in a rapidly evolving market.

- Partnerships and Integrations – Backblaze is increasingly working with strategic partners and is integrating its backup solutions with third-party platforms and applications, expanding its reach and market penetration.

Our issue is that none of these factors are remotely unique, limiting differentiation. This is an industry that is quickly becoming commoditized, with differentiation through broader factors such as an ecosystem (multiple other services), which Backblaze cannot offer.

Storage Industry

Backblaze’s industry is expected to grow well in the coming years, with a CAGR of +19% into 2028. This is expected to be driven by the increasing volume of digital data generated by individuals and businesses, with a growing need for reliable and affordable backup solutions.

We are living in a data generation where information is utilized to optimize businesses and improve sales generation. The current AI trend will only accelerate this further.

The concern for Backblaze, despite this positivity, is the level of competition in the industry. The most notable of which is Amazon S3 (AMZN), which offers comparable quality while having integration with a broader set of services and AWS. Backblaze can challenge currently due to its pricing strategy but if the company wants to transition to profitability, this competitive advantage will evaporate.

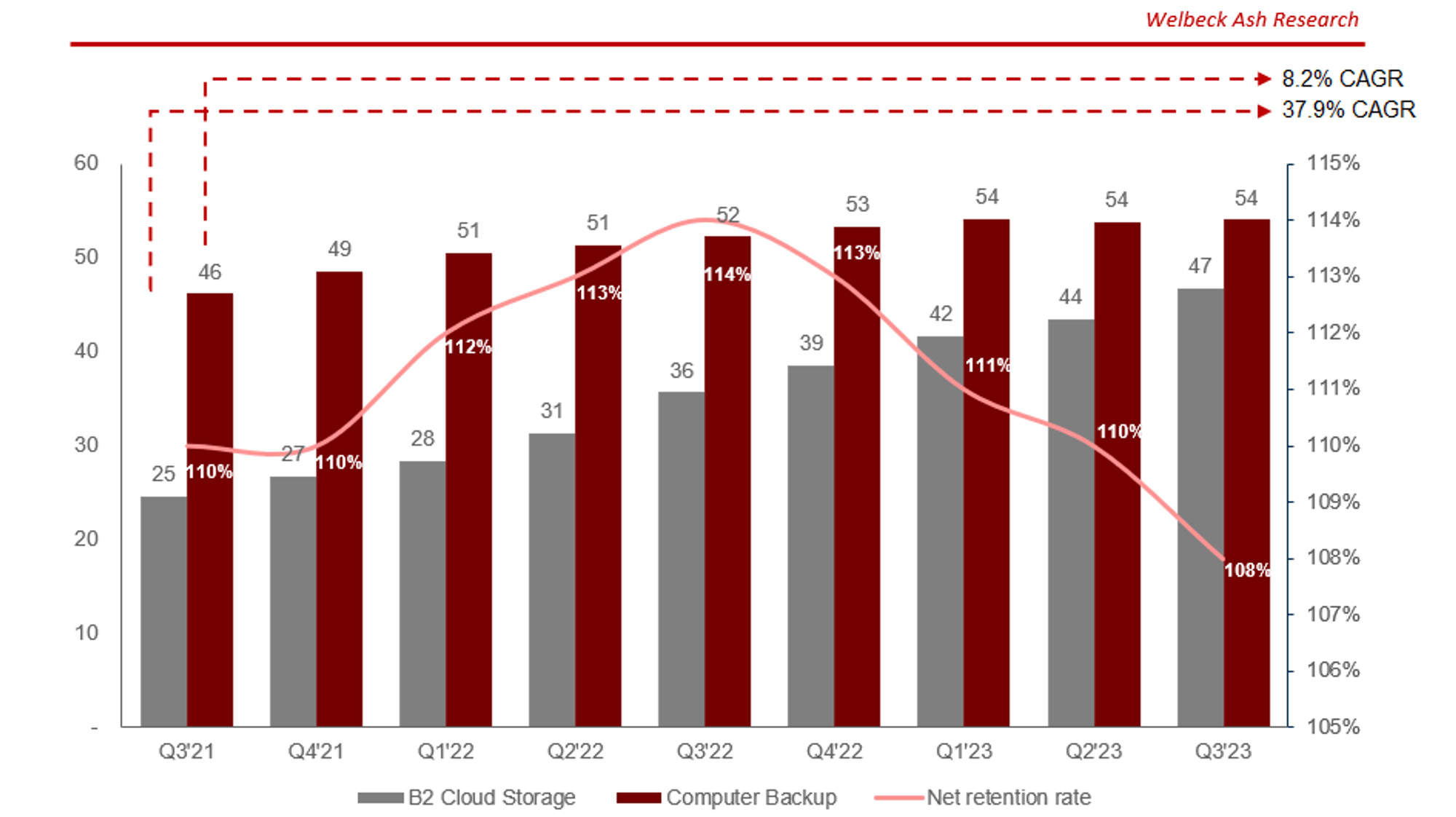

Growth progression

Backblaze data

Presented above is Backblaze’s ARR development over the last 2 years on a quarterly basis, split by its two revenue streams.

Whilst Backblaze’s revenue growth of 26% appears attractive, we see areas of concern in the detail. Firstly, the company’s ARR is actually split almost 50/50 between the fast-growing B2 Cloud Storage and the decelerating Computer Backup segment. This weighting will mean the slowdown materially impacts the company’s top-line growth, particularly as Computer Backup has stagnated for 3 quarters.

Secondly, Backblaze’s net retention rate is rapidly decelerating, across both revenue streams (120% for B2 and 100% for Computer Backup). We would expect a ~$100m ARR SaaS business to be consistently boasting 120-130%, as early-stage up/cross-selling drives value. This supports our assessment that the company is fundamentally lacking a key lever for driving growth, the ability to up/cross-sell.

Based on this, we see Backblaze decelerating to single-digit growth within the coming 5 years, which implies any considerable scale is unlikely, inherently limiting shareholder returns. The company is increasing prices, most recently in Q3’23, which will elongate this process.

Opportunities

We see the following as key opportunities for improving its growth rate:

- Market Expansion – Growth opportunities in untapped international markets, particularly those underserved by its larger peers.

- Partnerships and Alliances – Collaborations with other software providers, hardware manufacturers, and IT service providers.

- Product Innovation – Continuous improvement of services and introduction of new features. Management believes value can be extracted from utilizing AI.

Backblaze

Notable threats

We consider the following to be key threats:

- Security Breaches – Potential data breaches and cyber attacks compromising customer data.

- Technological Disruptions – Rapid advancements in cloud and storage technologies by its peers.

- Competitive Pricing Pressure – Pressure to balance pricing with profitability, particularly as the price of its peers continues to decline due to scale economy benefits.

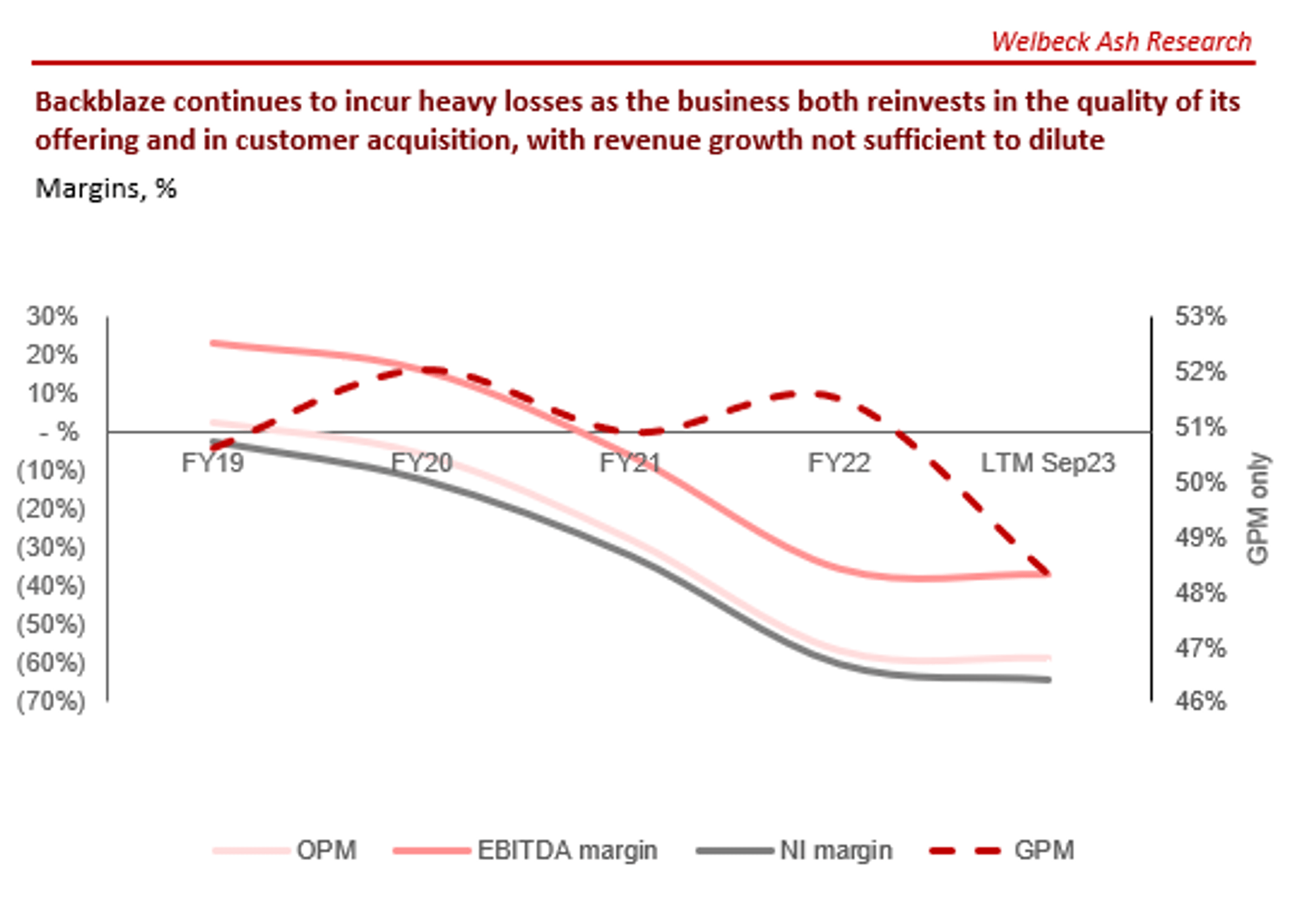

Margins

Capital IQ

Backblaze has been unable to improve its margins, primarily due to the investment required in customer acquisition in order to maintain growth. In an alternative manner, the above graph when contextualized by revenue growth reflects the criticism we have raised above.

We struggle to see how meaningful progress can be achieved, particularly if prices are not considerably raised or a fundamental shift in its cost base occurs.

Balance sheet & Cash Flows

As if investment in customer acquisition was not enough, the company also has considerable capex costs associated with data centers, which will only scale alongside revenue in the medium term. This will weigh on cash generation.

In the LTM period, Backblaze’s FCF was $(22)m, with a remaining cash balance of $30m. This means the company will need to raise cash imminently, and realistically, considerably so. This is while it has been forced to repay a portion of its debt.

We are concerned that with the current state of the debt market, shareholders will be forced to finance this through share issues.

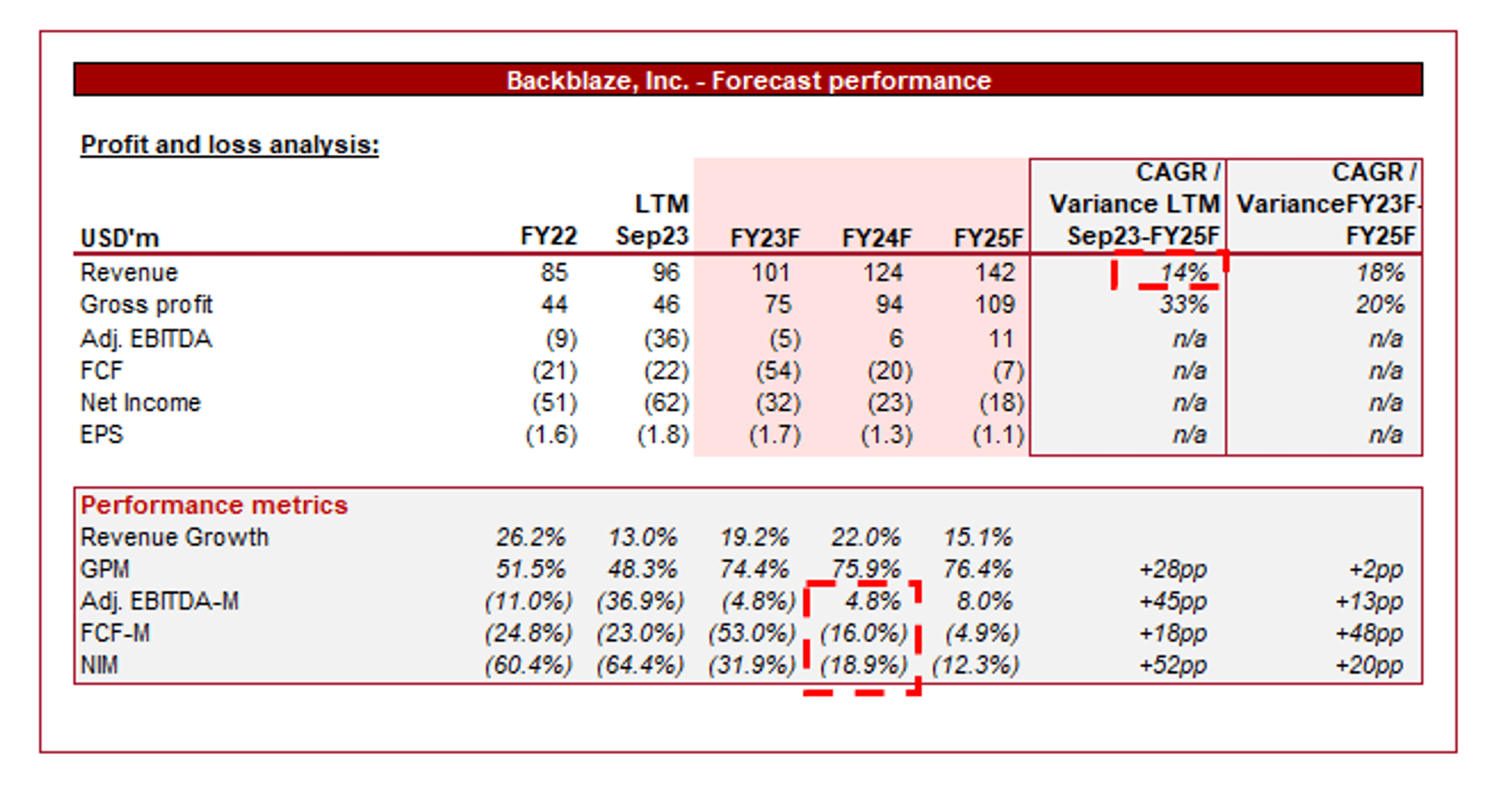

Outlook

Capital IQ

Presented above is Wall Street’s consensus view on the coming years.

Analysts are forecasting revenue growth of low double-digits into FY25F, alongside continued losses. We concur with these forecasts, although we suspect growth may not be as high. This is concerning as based on these forecasts, the company will need to find ~$100m to be comfortable, which represents ~30% of its market cap.

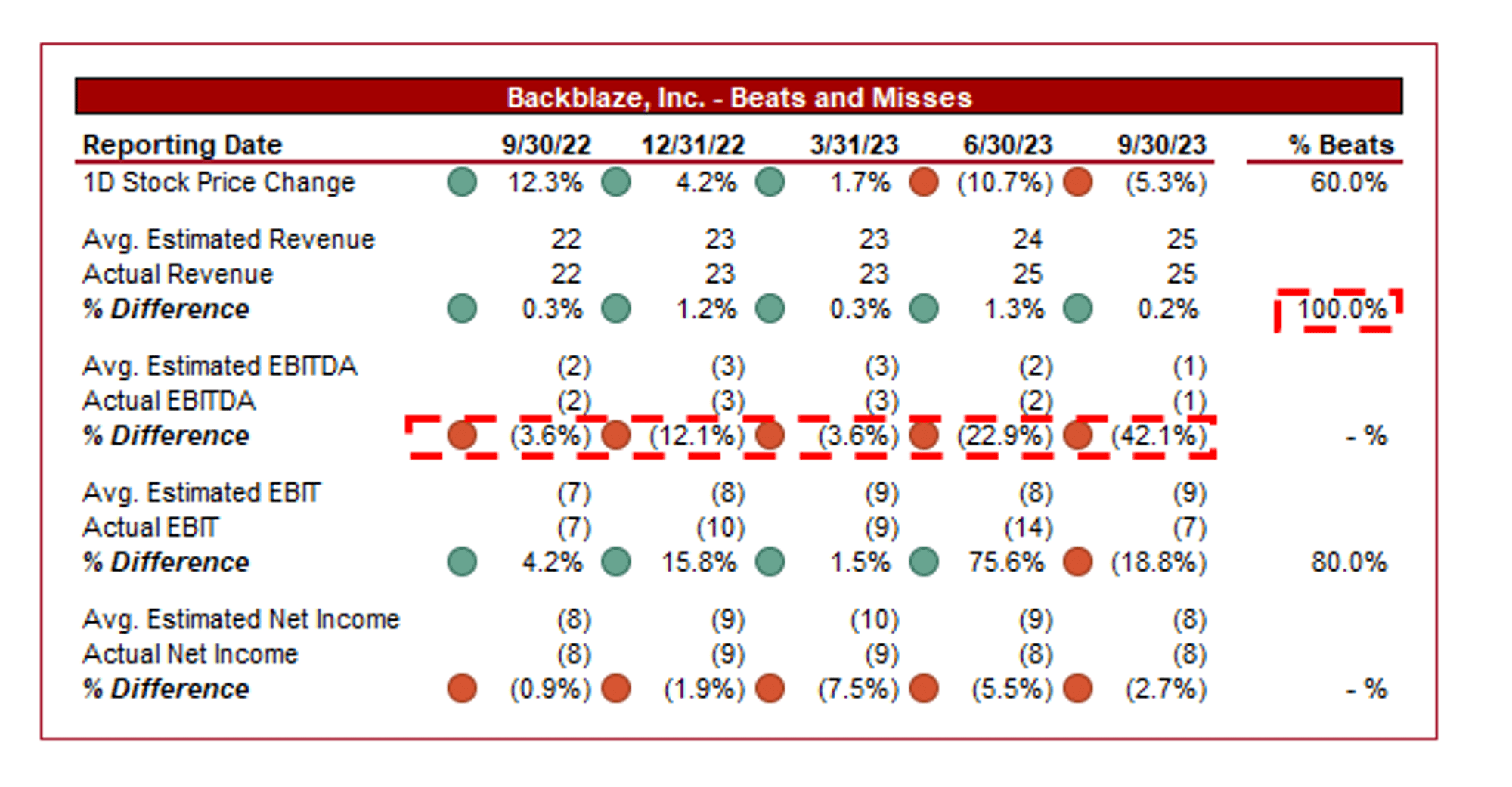

Beats and Misses

Capital IQ

Whilst Backblaze has marginally beat analyst estimates on revenue, the company’s margin development has been disappointing, implying price action has not been to the level expected.

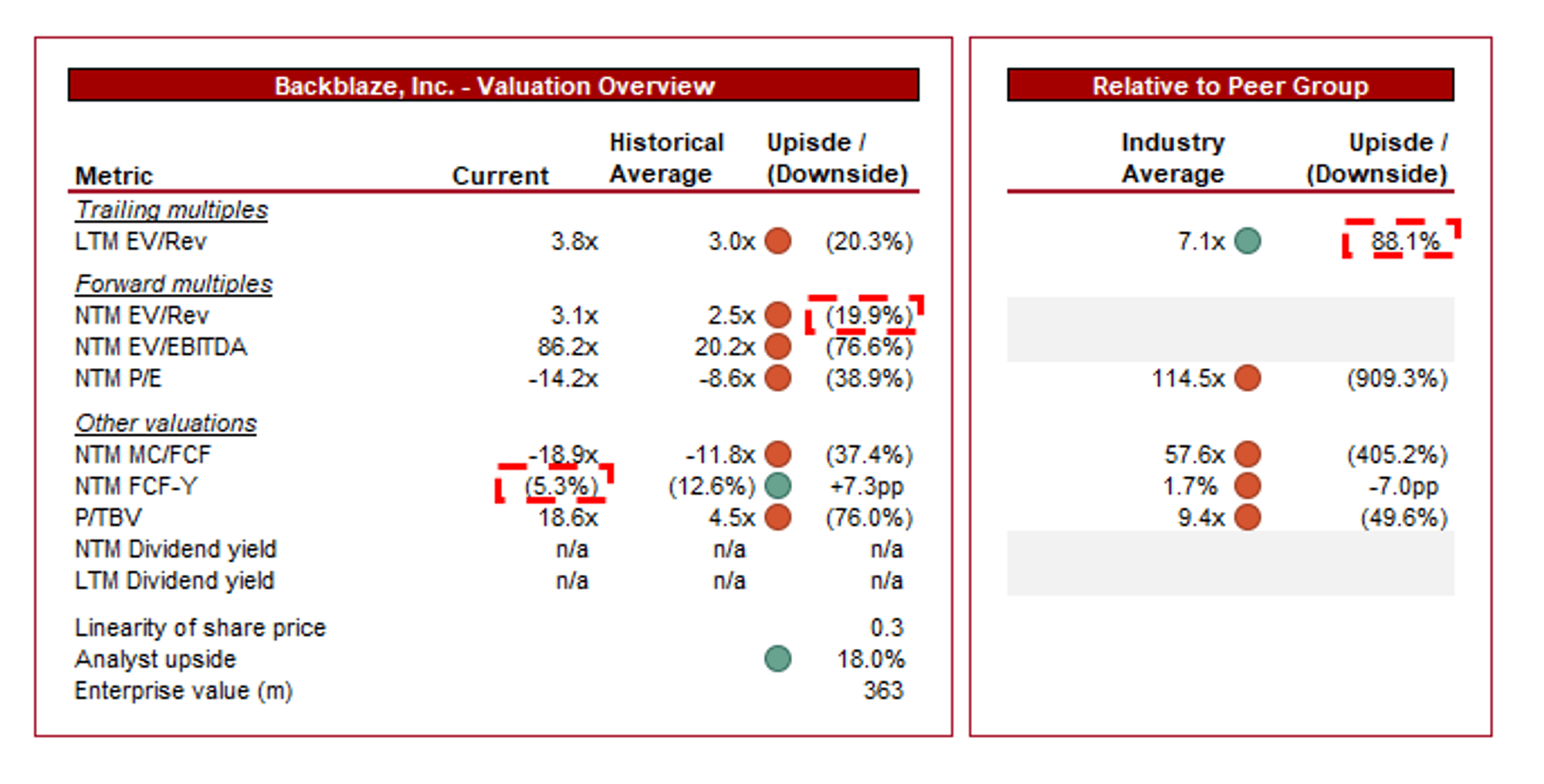

Valuation

Capital IQ

Backblaze is currently trading at 4x LTM revenue and 3x NTM revenue. This is a premium to its historical average.

We believe there is a material risk to Backblaze’s ability to achieve consistent profitability while growing at a reasonable level. The company could theoretically lift prices considerably but growth would evaporate. Equally, it could keep attempting to raise cash and fund losses till sufficient scale is achieved for margin positivity but we see this as inexecutable. This leaves Backblaze in the value-destroying middle ground. The company will gradually increase prices and cut costs, slowing revenue growth and widening the quality of its service vs. its leading peers. Ultimately, we see this as a route to it being taken over by a larger Software business seeking its infrastructure.

The only potential for upside in the near-term (and a risk to our thesis) is an immediate takeover. We are seeing mediocre listed Software businesses being taken private in growing numbers recently, as debt markets are shut and companies require funding. Backblaze could end up a target.

Final thoughts

We are not convinced by Backblaze as an investment. It is offering a valuable service in a growing industry, but lacks sufficient differentiation to be a long-term winner. The industry is commoditized and competition is high. We believe the company faces a considerable uphill battle to deliver attractive margins and shareholder returns, while gaining market share.

Given the issues presented, we rate Backblaze a sell.

Q2 2024 Earnings Call Transcript")