3D Graphic Design/iStock via Getty Images

Introduction

I’m sure I speak for everyone when I say we all love a good sale. Especially when some of your favorite stocks are selling at a discount. With interest rates remaining high for the foreseeable future, it’s not easy finding quality business development companies trading at attractive valuations. As an avid BDC investor I’ve not added to any of my holdings since interest rates have become elevated over the past 24 months or so.

But even though some are trading at large premiums to their NAV prices currently, there’s one in particular that still trades at a discount at the time of writing. In this article I discuss what makes Bain Capital Specialty Finance (NYSE:BCSF) attractive and why income investors may consider adding this to their portfolio.

Why The Discount?

With many quality BDCs trading significantly above their NAVs currently, one has to wonder why Bain Capital Specialty Finance is the exception. One reason may be the stock’s track record. The BDC, compared to peers like Capital Southwest (CSWC) and Ares Capital (ARCC), hasn’t been around as long.

The BDC IPO’d at the end of 2018, so they have only been public a little over 5 years. I’m not saying that’s the reason for the discount, but it very well could have something to do with it. Most investors prefer a longer track record when looking to invest in a company.

How did they do during the last economic downturn? How long have they paid a dividend? Did they cut the dividend during the last recession?

These are all valid points when looking into a company, especially one that pays out a large chunk of their profits in the form of dividends like BDCs or REITs typically do.

But then again there are some companies with shorter track records that trade at premiums as well. Take another favorite in the sector and holding of mine, Blackstone Secured Lending (BXSL). Their external manager Blackstone (BX), who is one of the most well-known companies in the world, may also have something to do with that though in my opinion. Either way BCSF seems to be doing all the right things and could very well become the next superstar within the sector.

Improved Dividend Coverage

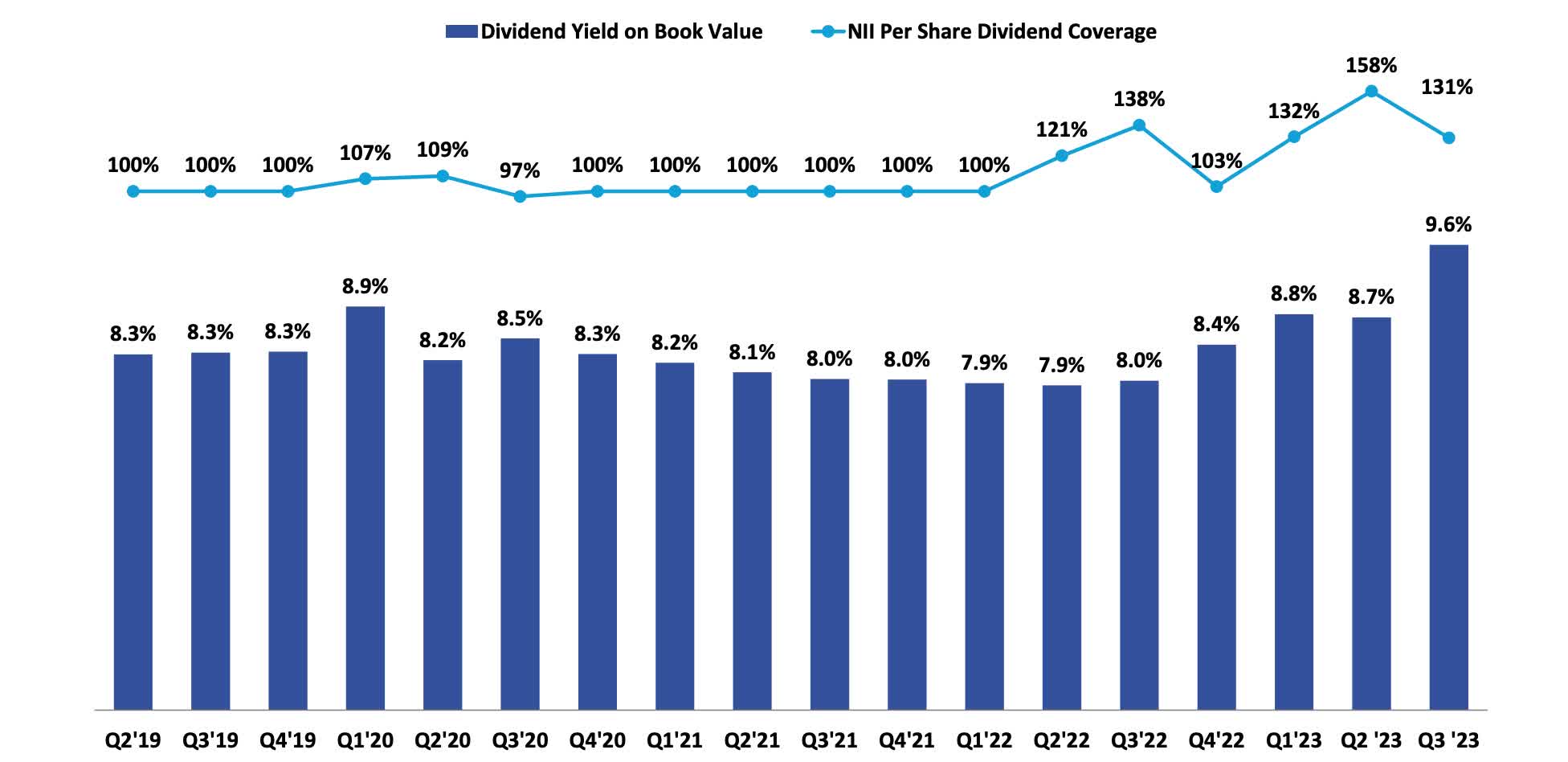

Probably the most attractive thing about Bain Specialty is their dividend coverage. Another reason for the discount could be the dividend cut the company did back in 2020 when they slashed the dividend roughly 17% from $0.41 to $0.34. But as most may know, the pandemic was a tough time for many businesses and forced several companies to default on loans.

But since then, the company has quickly gotten back to growth, raising the dividend from $0.34 to the current $0.42 a share. And they’ve been out-earning their dividend by a sizable margin. The BDC reported Q3 earnings back in November, bringing in net investment income of $0.55, beating estimates by $0.01. This was down from $0.60 in Q2 but seeing by the current dividend, they comfortably out-earned their dividend with coverage well above 100%.

In the chart below, you can see since the start of rate hikes BCSF has comfortably covered their dividend. The BDC has not rewarded investors with a special or supplemental like some of its other peers, but the coverage has remained strong with room to award shareholders in the future if they see fit.

BCSF investor presentation

But I think it’s smart not to as they have been focused on growing their portfolio recently. At the end of Q3, they had a total of 143 portfolio companies valued at $2.4 billion across 30 industries. This grew from 130 companies and a total portfolio fair value of $2.29 billion year-over-year.

Aerospace & Defense is their largest sector and during their latest quarter they continued with new investments in companies who provide mission-critical software & surveillance solutions to the defense industry and medical companies that provides on-site services to patients at skilled nursing facilities. Over the year they’ve invested a total of $616 million with 84% in first-lien loans.

Their first-lien percentage currently stands at 64%, down from 66% in Q1. Management attributed the drop in first-lien loans to growth in new investments. Although they are not as defensively positioned as Capital Southwest whose first-lien loans currently stand at 84%, they are significantly higher than their largest peer Ares Capital’s 43.1%.

But seeing by the smaller market cap of the company, I expect this to rise over the years as they continue to make new investments to grow their portfolio.

Strong Balance Sheet

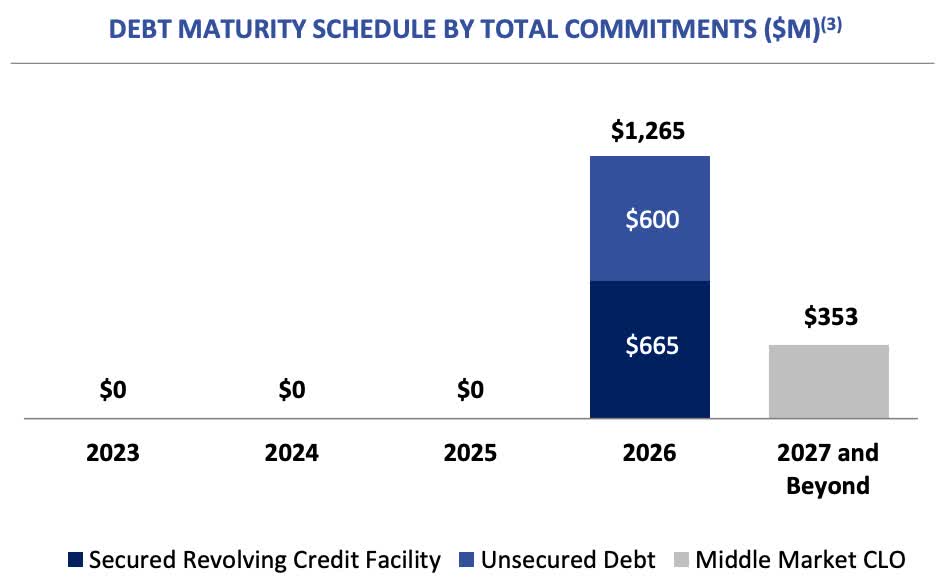

Although not as defensively positioned as some peers, the BDC does have a strong balance sheet with no debt maturities to worry about until 2026. So, if the economy does experience a recession or rates remain higher, the company is in a strong financial position to navigate. Furthermore, they’ve increased their cash balance from $29.6 million in Q1 to $79.5 million in Q3.

BCSF investor presentation

They also boast investment-grade credit ratings from all three major rating agencies. Additionally, they’ve managed to decrease their debt-to-equity ratio to 1.12x, down from 1.13x in Q2. This is in comparison to peer, ARCC’s 1.03x. One thing I like about BCSF is they appear more fiscally conservative like ARCC, a preference of mine.

Rewarding shareholders in the form of specials & supplementals is great and all, but paying out all your income in the form of dividends and not retaining any cash can be detrimental if the economy experiences an unexpected downturn. Or if one of their portfolio companies experiences financial hardship. The company’s spillover income increased from $0.44 to $0.79, or 1.9x in Q3. And I expect the company to continue carrying over spillover income, similar to peer ARCC.

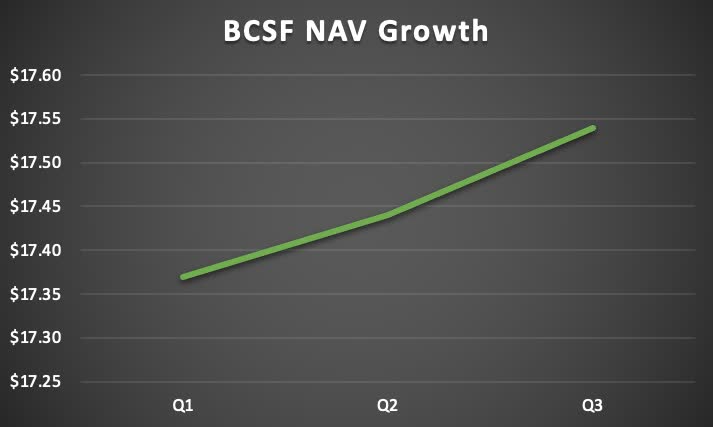

NAV Growth

With the company comfortably out-earning its dividend, the NAV price has increased steadily quarter-over-quarter from $17.37 in Q1 to $17.54 in the latest quarter. This was also up from $17.29 at the end of 2022. Part of this can be attributed to their increased dividend growth and dividend coverage well-above 100% over the past year. At a price of less than $15 at the time of writing, the stock is attractive, offering a double-digit discount of 17%.

Author creation

Risks To Thesis

Some investors may be skeptical about investing in BCSF because of the dividend cut in 2020 and/or their relatively short track record. But the company has been conservative since the start of rate hikes, strengthening their financial position in the past year. With the FED electing to hold rates recently making rate cuts seemingly out for next month, the BDC will enjoy extra income for a while longer, mainly due to its predominantly floating rate debt portfolio.

At 94% and not being as defensively positioned in first-lien loans like some peers, this could cause tighter dividend coverage when rates are cut. Which many are expecting sometime this year. And although they covered the dividend prior to the start of rate hikes, this coverage was less than some of their larger, and more popular peers in the sector. Furthermore, if dividend coverage becomes significantly tighter, their share price will also likely suffer in the process. So, investors currently holding or looking to potentially buy BCSF, this is something to keep an eye on going forward.

Bottom Line

Bain Capital Specialty Finance is a fairly newcomer to the BDC space and despite their financial troubles during the pandemic that saw them cut the dividend, they have been growing their portfolio impressively since then. They’ve also elected to be more fiscally conservative than some peers, allowing them to retain extra income in the form of spillover (income).

This, along with the strong balance sheet puts the BDC in a strong financial position if portfolio companies become too stressed from higher for longer rates. At the end of the quarter, they only had 3 companies on non-accrual status, but this could rise in the near future. But seeing by their well-laddered debt maturities, strong cash position, and well-covered dividend, I rate the BDC a speculative buy.

Q2 2024 Earnings Call Transcript")