Pitney Bowes Inc. (NYSE:PBI) recently announced a company-wide cost reduction program, which I believe could have a beneficial effect on future FCF growth. In addition, I would expect new net sales growth driven by strong volumes of domestic parcels, network productivity, and new technological solutions in the e-commerce business. Furthermore, given previous sale of assets and divisions in the past, we could expect new transactions in 2024, which may boost the balance sheet. These are good reasons to believe that Pitney looks like a buy. There are obvious risks associated to financial dependence and the total amount of debt. However, PBI does look undervalued at its current price mark.

Pitney Bowes Inc.

Pitney Bowes Inc. is a shipping and mailing company. It provides technology, logistics, and financial solutions to small and medium-sized businesses as well as large corporations, including more than 90% of the Fortune 500 companies, retailers, and government clients worldwide. These customers place their trust in the company to simplify processes and improve efficiency in sending mail and packages.

Pitney Bowes offers a wide range of services and technologies to meet the needs of its customers. Its business model includes national parcel services with sorting and fulfillment centers for fast and efficient delivery. It also focuses on cross-border services that facilitate the international shopping and shipping experience with proprietary technology.

Additionally, it offers digital delivery services, allowing for flexible options and real-time tracking. Its pre-sorting services include working with USPS and other sorting services for optimal postal discounts.

With that about the business model, I believe that it is worth having a look at Pitney because of the recent guidance given by management. Among the new beneficial information reported in the last quarter, there are some new savings from actions taken in 2023 annualize and revenue growth expected for 2024. I included some of these assumptions in my financial model.

We expect revenue growth to range from flat to a low-single digit decline and EBIT margins to remain relatively flat on a year-over-year basis. We expect incremental benefit in 2024 from our company-wide cost reduction program as savings from actions taken in 2023 annualize and we further execute on the plan. Source: Quarterly Report

We also expect similar levels of capital expenditures in 2024 as in 2023 and interest expense to remain around the elevated rate incurred in Q4 2023. Source: Quarterly Report

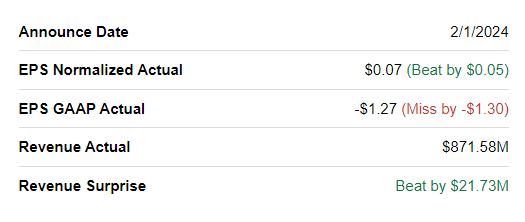

Pitney reported quarter revenue of close to $871 million, which was higher than expected. In addition, EPS Normalized stood at $0.07, which was also higher than expected. The market did not really celebrate the new quarterly earnings. The stock price recently declined, and the shares are being traded at approximately the same price seen in April 2023.

Source: Seeking Alpha

Source: Seeking Alpha

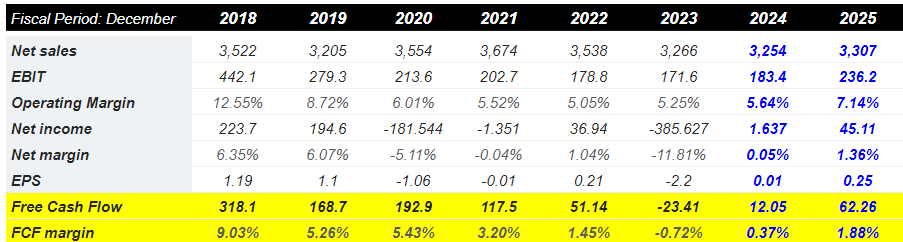

With that about the most recent market sentiment and earnings, I believe that the expectations of market analysts appear beneficial. In 2024 and 2025, market expectations include net sales growth, net income growth, and FCF growth.

More in particular, net sales are expected to be close to $3.307 billion, with 2025 EBIT of $236.2 million, 2025 operating margin of about 7.14%, and 2025 net income worth $45.11 million. Finally, with 2025 free cash flow of about $62.26 million, 2025 FCF margin is expected to be close to 1.8%.

Source: Market Screener

Balance Sheet

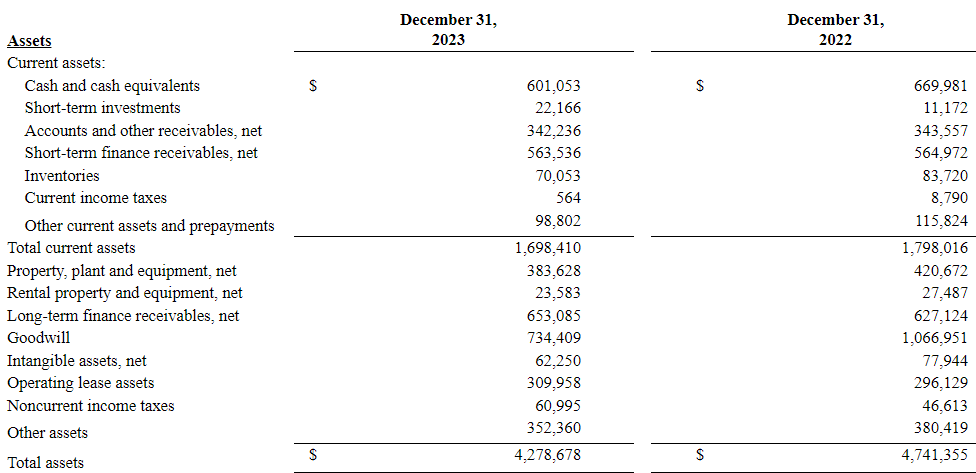

As of December 31, 2023, the company noted cash and cash equivalents of $601 million and short-term investments of $22 million. Besides, with accounts and other receivables of close to $342 million, short-term finance receivables worth $563 million, and inventories of $70 million, total current assets are equal to $1.698 billion. The current ratio is lower than 1x, which I do not appreciate. Some investors may not buy shares because of this fact.

Property, plant, and equipment stand at close to $383 million, with rental property and equipment worth $23 million, long-term finance receivables of $653 million, and goodwill worth $734 million. In addition, total assets stand at about $4278 million, and the asset/liabilities ratio is lower than 1x. In my view, if the company successfully offers a balance sheet with an asset/liabilities ratio larger than 1x, Pitney will most likely receive more stock demand.

Source: Quarterly Report

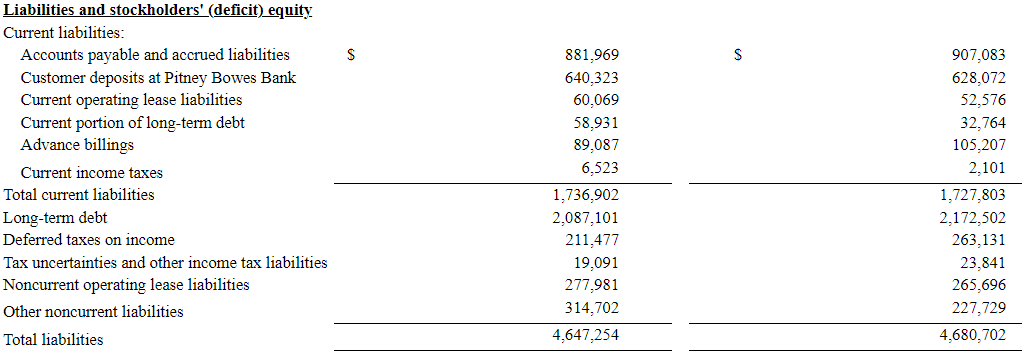

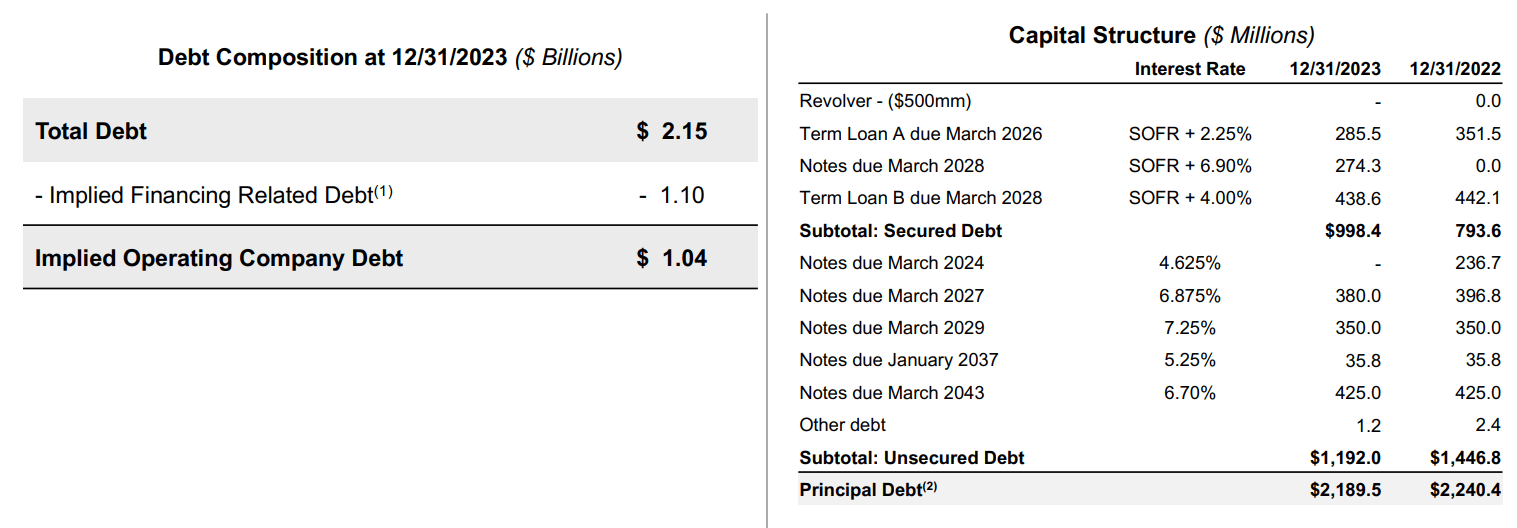

The list of liabilities includes accounts payable and accrued liabilities worth $881 million, customer deposits at Pitney Bowes Bank of close to $640 million, and total current liabilities of about $1736 million. Long-term debt stands at $2087 million, with deferred taxes on income worth $211 million, tax uncertainties and other income tax liabilities of about $19 million, and total liabilities of $4647 million. Given the total amount of debt, I think that studying carefully the debt terms and cost of debt may help design the company’s financial model a bit better.

Source: Quarterly Report

I believe that the company is in compliance with the financial and non-financial covenants of its revolving credit facilities and secured term loans. In the last presentation, management noted loans and notes including interest rate close to SOFR +2% and 6% as well as interest rate of about 7% and 4%. With these figures, I assumed a WACC close to 10%, which I believe is a conservative cost of capital.

Source: Quarterly Report

E-commerce Solutions And Technological Solutions Could Bring FCF Growth

According to the last 10-k, Pitney Bowes’ business strategy focuses on driving stable, profitable growth. It seeks to achieve a mid-single-digit increase in consolidated revenue, outperforming EBIT growth primarily through improved profitability of the global e-commerce segment. I believe that management will most likely be able to obtain these profitability targets thanks to growth in national parcel delivery, productivity improvement in all its operations, and expanding its shipping technological solutions. Under the best case scenario, I think that these measurements could lead to FCF growth. In the last quarterly report, management noted strong volumes including a double digit growth in domestic parcels as well as EBIT improvement. Pitney Bowes also reported that network productivity appears to be helping financial improvements in the e-commerce solutions business.

Global Ecommerce experienced strong volumes during peak, processing 61 million domestic parcels in the fourth quarter, which is up 13 percent from fourth quarter 2022. Domestic parcel revenue grew 7 percent in the fourth quarter versus prior year, which was more than offset by a loss in revenue from cross-border. Improved EBIT in the fourth quarter reflects the positive impact of cost actions, higher domestic parcel volumes, and increased network productivity. Source: Quarterly Report

Increases In Restructuring Charges May Bring FCF Growth

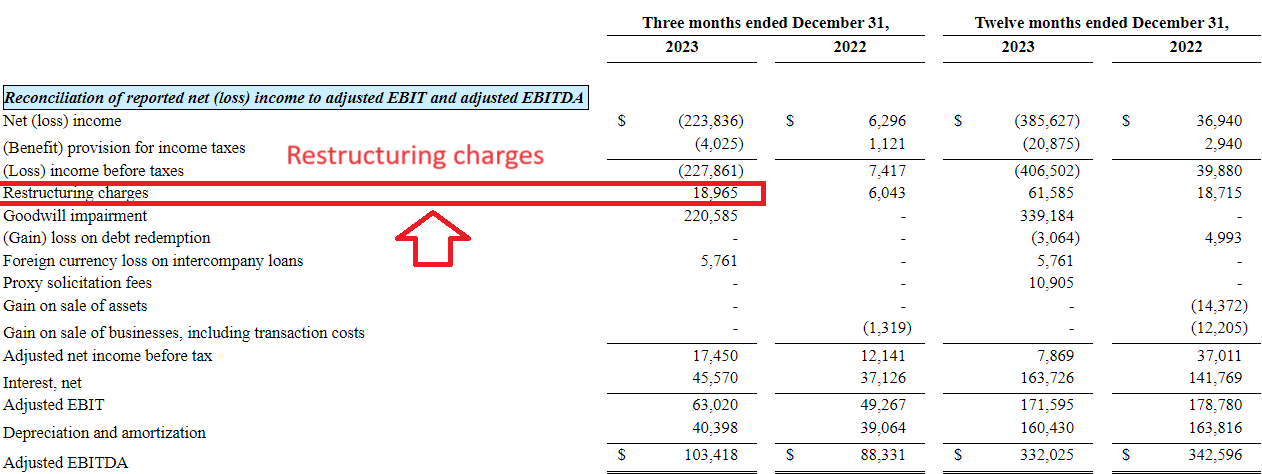

In the most recent quarterly report, the company noted cost reduction efforts as well as increases in restructuring. It was noted in the last quarterly press releases and the quarterly presentation.

Source: Quarterly Presentation

In the twelve months ended December 31, 2023, restructuring charges multiplied by close to three times. In the three months ended December 31, 2023, restructuring charges also increased as compared to that in 2022.

Source: Quarterly Presentation

Sale Of Businesses And Assets Could Lead To Cash In Hand And Leverage Decrease

According to the last annual report, the company sold an office building, a division called Borderfree, and other businesses. I did not find many references in the last quarter about new transactions. With that, I assumed that new transactions could be announced, which could lead to balance sheet improvements and lower net leverage. As a result, I believe that we could see improvements in the stock valuation.

Other income for the year ended December 31, 2022, of $22 million consists of a $14 million gain from the sale of our Shelton, Connecticut office building, a $5 million gain from the sale of Borderfree, and a gain of $7 million from deferred proceeds received related to the sale of businesses in prior years. Source: 10-k

Source: Quarterly Report

My DCF Model Based On Previous Financial Figures, And My Own Assumptions

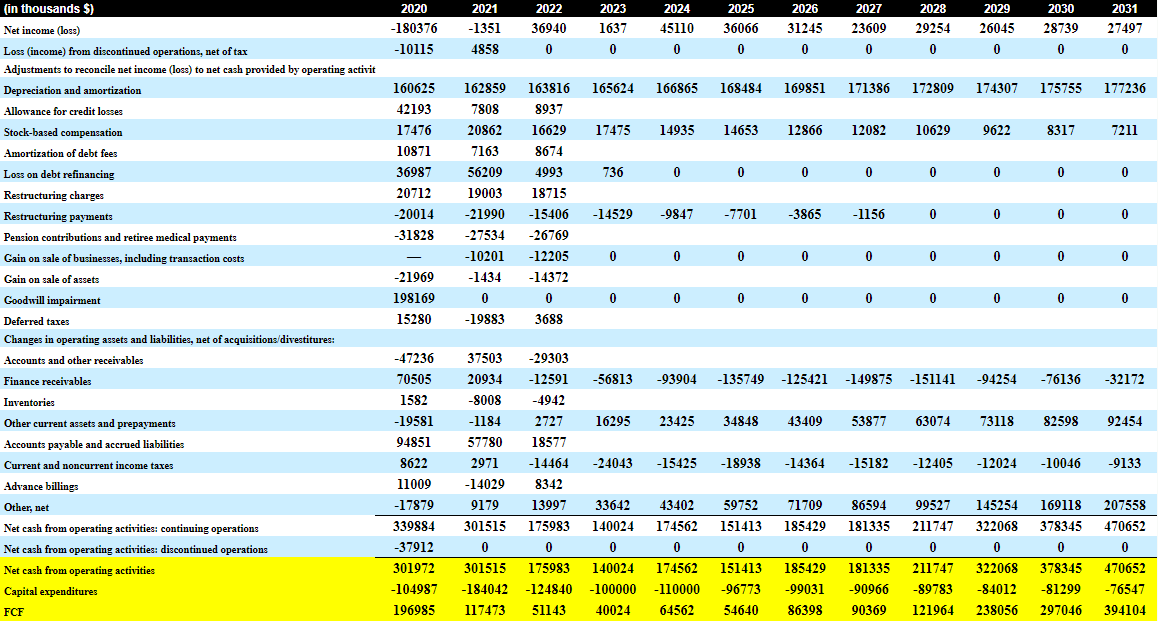

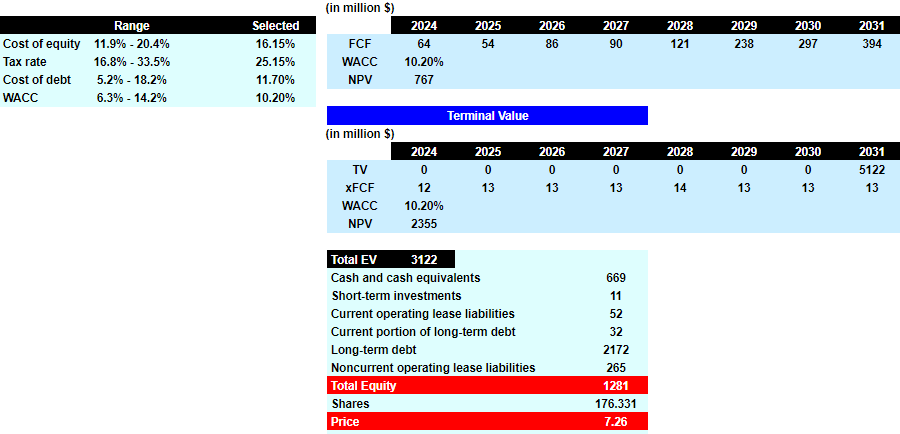

My cash flow projections include 2031 net income of close to $27 million, 2031 depreciation and amortization worth $177 million, and stock-based compensation close to $7 million. I did not take into account amortization of debt fees, loss on debt refinancing, restructuring charges, or restructuring payments as I believe that they are not recurrent part of the business model.

In addition, with changes in finance receivables of about -$33 million and changes in other current assets and prepayments worth $92 million, changes in others stand at about $207 million. Finally, 2031 net cash from operating activities stands at close to $470 million, with 2031 capital expenditures of about -$77 million and 2031 FCF of $394 million.

Source: Author’s Work

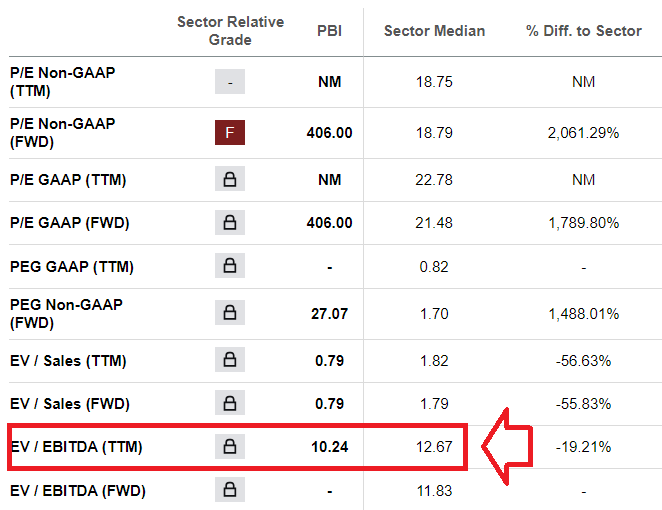

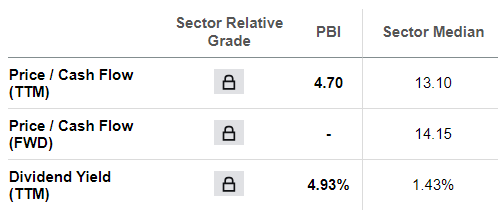

Competitors in the sector trade at close to 12x EBITDA, which is close to 19% higher than what Pitney reports. Competitors also trade at 14x cash flow. With these figures, I assumed a valuation of 13x FCF.

Source: Seeking Alpha

Source: Seeking Alpha

I assumed a WACC of 10.2%, which I believe is conservative for Pitney. With these assumptions, total enterprise value would be close to $3.12 billion. If we sum cash and subtract debt and operating lease liabilities, the implied equity would be close to $1.2 billion. The forecast price would stand at $7.2 per share.

Source: Author’s Work

Risk, And Competitors

In my opinion, Pitney Bowes faces various risks that may affect its financial performance. Financial dependence on national postal services, especially USPS, could impact the income if the company faces financial challenges. Contractual relationships with USPS for package and digital delivery services could impact competitiveness and profitability. Postal regulation may limit products and rates, and changes in regulation or physical mail volume could have a negative effect. In addition, changes in laws or postal operating models may affect the performance of the company. The company must be agile to face these risks and maintain its competitive position.

Pitney Bowes Inc. faces intense competition in its various business segments. In the global e-commerce market, it competes with large multinational companies as well as regional and local companies, some of which offer complete solutions and global delivery services.

For the digital delivery services business, the company competes with a variety of technology providers seeking to make shipping easier. In presorting services, it competes with local suppliers, consolidators, and large mailing companies. In shipping technology solutions, it faces competition from other providers of mail equipment and solutions as well as alternative communication methods. In the financial field, the company competes with large and small financial institutions with a wide range of solutions. Despite the competition, Pitney Bowes stands out with its extensive network of facilities, innovative technology, and integrated financing solutions.

My Conclusion

In my opinion, the Pitney Bowes has proven to be dominant in the shipping and mail sector, providing technological and logistical solutions at a global level. Its focus on stable and profitable growth, along with the expansion of cross-border and digital delivery services, shows its ability to adapt to changing market demands. I believe that network productivity increases mainly in e-commerce, growth in domestic parcels, and restructuring announced could bring significant FCF growth in the coming years. These are good reasons to believe that Pitney is a buy. There are risks associated to financial dependence on national postal services, competition in the market, and the total amount of debt. With that, I believe that Pitney clearly trades undervalued.

Q2 2024 Earnings Call Transcript")