MirageC/Moment via Getty Images

At A Glance

Eli Lilly’s (LLY) revelation of tirzepatide’s potential in treating metabolic dysfunction-associated steatohepatitis (MASH), also known as NASH, represents a significant shift in the competitive landscape, with the potential to further disrupt Madrigal Pharmaceuticals’ (NASDAQ:MDGL) resmetirom’s market positioning. The clinical and financial implications of this development are profound, with tirzepatide demonstrating a meaningful treatment effect in MASH. Despite Madrigal’s solid financial footing, evidenced by a healthy cash reserve and a reduced immediate need for capital, the stock’s market sentiment appears fragile, as evidenced by high short interest and mixed performance metrics. This analysis hints at a nuanced landscape where Eli Lilly’s strategic advancements in MASH research could recalibrate investor expectations and market valuations, particularly affecting Madrigal’s future revenue streams and stock valuation.

MASH-ed by Eli Lilly: Tirzepatide’s New Arena

Just when you thought GLP-1/GIP drugs were at their apex in the clinic, Eli Lilly recently revealed tirzepatide data in MASH. Tirzepatide is also sold under the brand names Mounjaro (diabetes) and Zepbound (obesity).

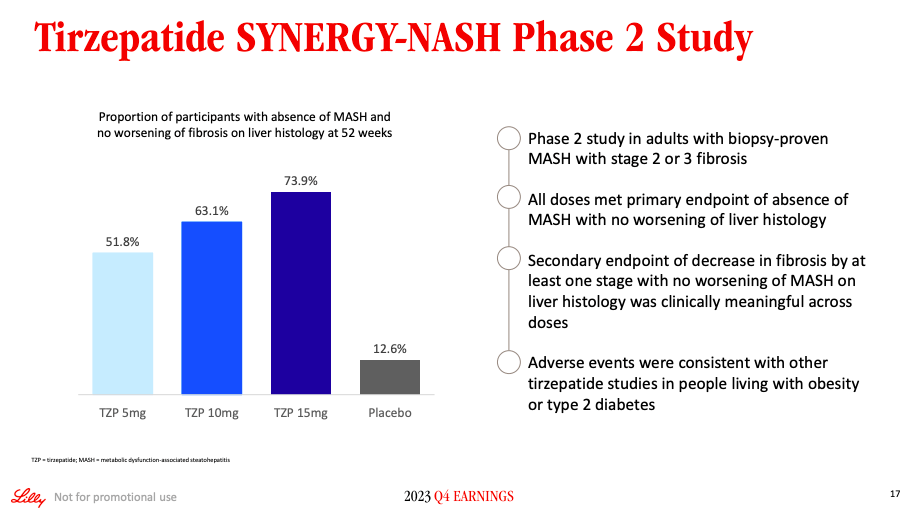

Eli Lilly investor slides

The data above is fairly robust. Since we have prior experience with tirzepatide, it is also assumed to be safe, which is important because MASH is a chronic condition.

Some will point out that the fibrosis endpoint was only deemed “clinically meaningful,” which translates to “didn’t reach statistical significance.” This would be a key differentiator for Madrigal’s MASH drug, resmetirom, which bears a very different mechanism of action (thyroid hormone receptor-β agonist) than tirzepatide. However, during their earnings call, Eli Lilly had this to say regarding the fibrosis endpoint:

While the study was not designed to be statistically powered to evaluate improvement in fibrosis, the study results showed a clinically meaningful treatment effect across all doses on the proportion of participants achieving a decrease of at least one fibrosis stage with no worsening of MASH to placebo.

From the looks of it, I would bet on tirzepatide being successful in a Phase 3 MASH study. For now, we have very clear evidence that tirzepatide is active in MASH. This is a major problem for Madrigal, even with tirzepatide at least three years away from marketization in MASH.

In the future, resmetirom will very likely see decent utilization in NASH patients, but seldom as a first-line treatment. On top of that, weight loss drugs like Zepbound and Novo’s Wegovy figure to reduce Madrigal’s total addressable market, as obesity is a major risk factor for MASH development. This is a double-whammy.

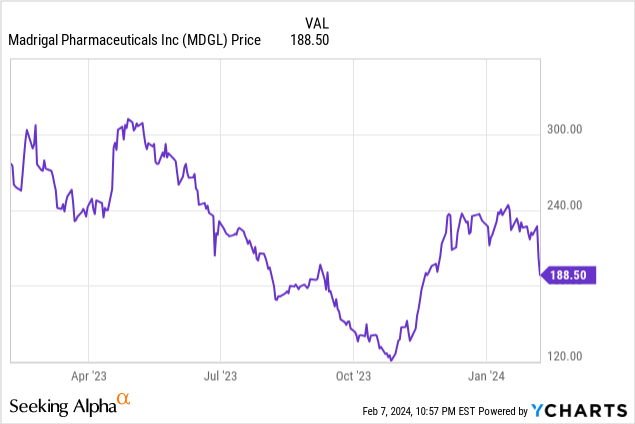

Subsequently, we have to adjust our revenue estimates for resmetirom. It is, in my view, much lower than I had previously projected. I would peg it at no more than $1 billion per year. Following the tirzepatide MASH data, Madrigal’s shares are trading 15% lower, but the market capitalization is still near $4 billion, which seems a little high to me in light of these recent developments.

Financial Health

Following a hefty $500 million public offering in October, Madrigal now flaunts liquid assets at an impressive $732.4 million. This sum encompasses $562.1 million in cash, buoyed by the recent capital influx, plus $170.3 million in marketable securities. Liabilities hold steady at $215.7 million, showcasing a fortified liquidity stance and a more favorable current ratio.

Over the past nine months, the firm’s operational activities consumed $244.3 million in net cash, translating to a monthly expenditure of roughly $27.1 million. Thanks to the bolstered liquid reserves, Madrigal’s financial runway now stretches further. The likelihood of seeking extra capital within the forthcoming year now appears markedly reduced.

Market Sentiment

According to Seeking Alpha data, Madrigal exhibits a market capitalization of $3.98 billion, underpinned by significant growth prospects, with analysts projecting a leap in revenue from virtually none in 2023 to $146.43 million in 2024 and further surging to $515.06 million by 2025. Despite this optimistic outlook, the stock’s momentum presents a mixed picture; it outperformed SPY in the short term with a +36.69% rise over three months but lagged on a yearly basis with a -27.14% return against SPY’s +20.51%.

A high short interest of 26.08% indicates substantial skepticism or speculative interest, potentially signaling volatility or investor caution. Institutional ownership stands strong at 88.49%, with notable movements including 994,681 new positions and 307,861 sold-out positions. Leading institutions like Janus Henderson, Vanguard, and Avoro Capital Advisors demonstrate confidence, whereas insider trades reveal a concerning trend with net sales of 1,114,251 shares over the past three months and 1,059,875 shares over the past year, suggesting possible insider pessimism about the stock’s short-term prospects.

Given the stock performance inconsistency, significant short interest, revenue projections that may need adjusting, and negative insider sentiment, the company’s market sentiment can be qualified as “fragile.”

Is MDGL Stock a Buy, Sell, or Hold?

Eli Lilly’s tirzepatide data reveal in MASH disrupts the medical realm, potentially eclipsing Madrigal’s resmetirom. Tirzepatide’s wide-ranging use and likely MASH triumph spell intense rivalry for Madrigal, prompting a re-evaluation of resmetirom’s revenue expectations.

Despite Madrigal’s robust finances following a capital infusion, tirzepatide’s entrance hints at a valuation mismatch. Mixed market reactions, marked by soaring short interest and bearish insider moves, underscore doubts about Madrigal’s outlook in a tough rivalry scene.

These elements, along with optimistic yet maybe inflated revenue predictions, point to shaky market confidence. Hence, downgrading from “Buy” to “Sell” on Madrigal seems prudent. Fortunately, Madrigal’s stock has been flat since my last recommendation. However, tirzepatide puts Madrigal’s share and worth at risk, hinting at a price closer to $120 per share as it recalibrates to this competitive shift.

However, there are risks to selling Madrigal’s stock. Resmetirom, currently set for a March PDUFA, may achieve FDA approval and a very favorable label. The drug is set to be first-to-market in MASH, which was no easy achievement. Tirzepatide and others could fail in pivotal trials for MASH, diminishing their impact on Madrigal’s total addressable market. Madrigal may achieve much greater than $1 billion in peak annual revenue. Again, it’s not that I don’t believe this will happen 100%. Everything is probabilistic. I just believe the odds are now quite out of favor. The new information has altered my outlook, and it’s time to act accordingly.

Q2 2024 Earnings Call Transcript")