tupungato/iStock Editorial via Getty Images

Big Stock Move, Little Change In Fundamentals

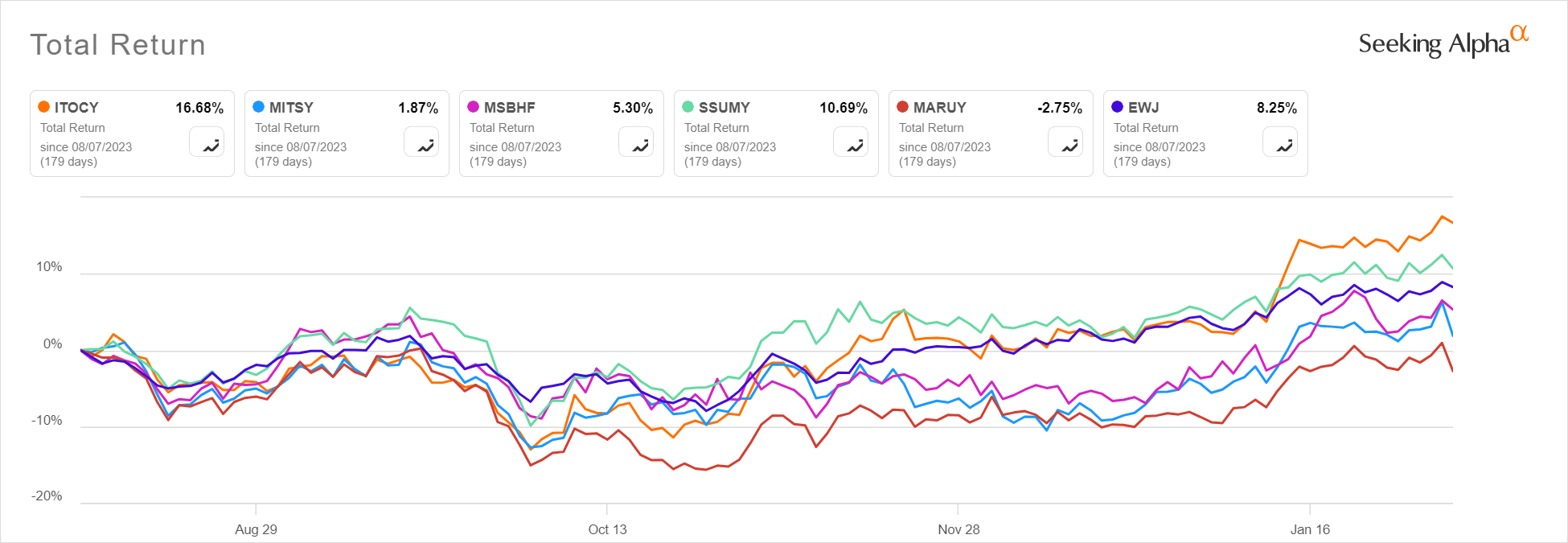

In the six months since I last covered ITOCHU Corporation (OTCPK:ITOCY, OTCPK:ITOCF), the stock has been the highest performing of the five major Japanese trading companies. This included a 10% jump in three days on January 10-12 on no significant news.

Seeking Alpha

This outperformance is hard to justify based on the lack of changes in company fundamentals since then. I even skipped a quarterly update in November as there was only a minimal change in the profit forecast for the year, from ¥780 billion to ¥800 billion and no change in the ¥160 per share dividend forecast. There was even less movement in the 3Q results, where both the profit and dividend forecasts were unchanged from the previous quarter.

Itochu Corp.

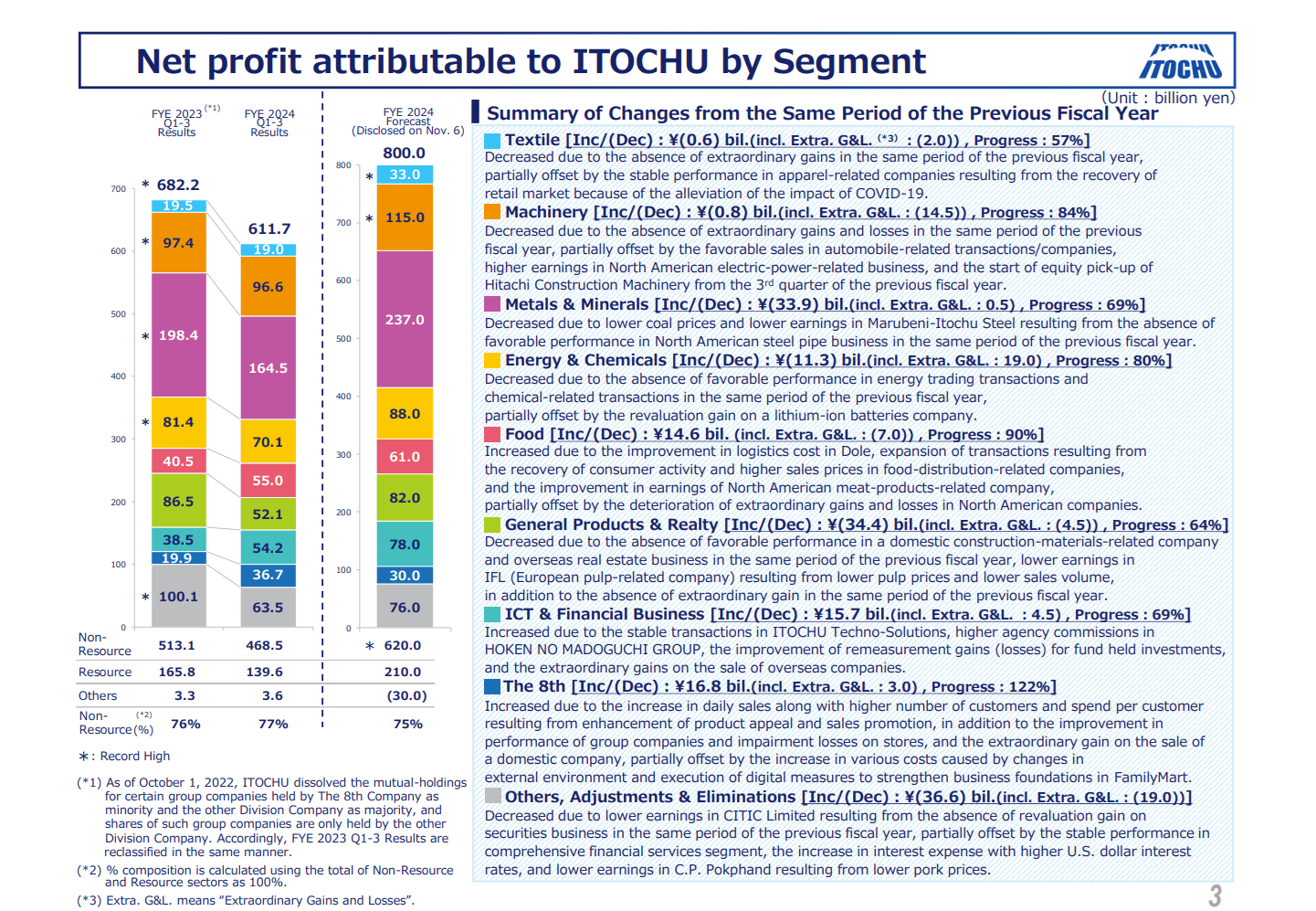

Still, the small changes that have been made since August reinforce the importance of the non-commodity businesses at Itochu, in contrast to the other trading companies.

The Machinery segment profit forecast is ¥10 billion higher than the original plan, and the segment has already delivered 84% of the updated plan for the full year. This was due to continued good performance in the automotive and North American power businesses.

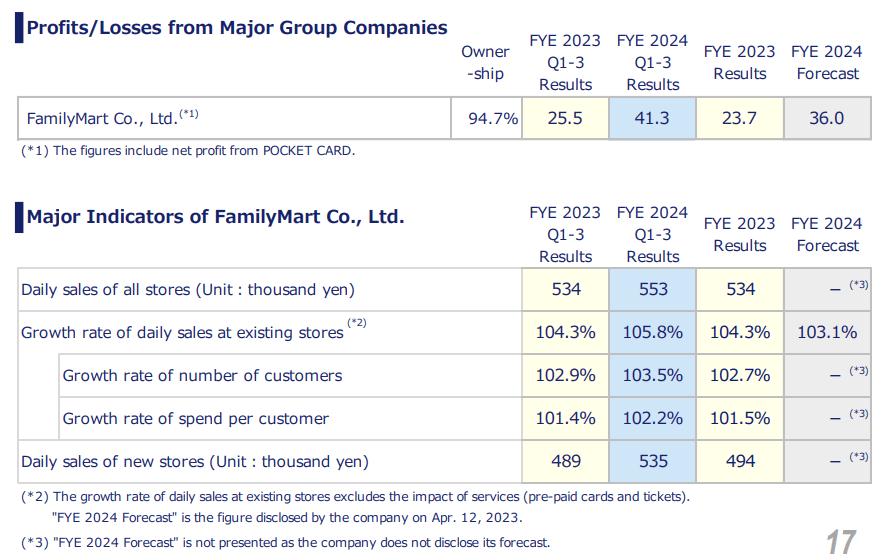

The profit forecast for the 8th Company is now ¥9 billion above the original plan, driven by further improvement at the FamilyMart convenience store chain, now expected to earn ¥36 billion, compared to the ¥26 billion forecasted in August. The 8th Company has already delivered 122% of its plan for the year.

Itochu Corp.

Offsetting these positives is an ¥8 billion decline in the forecast for General Products & Realty due to worsening performance of Itochu Fiber Limited, a European pulp business. The segment has delivered just 64% of its full year plan after three quarters.

Finally, the Others, Adjustments, and Eliminations category has improved by ¥9 billion, but this is mainly because the “loss buffer” corporate overview used to make the forecast more conservative has decreased by ¥20 billion, offset by actual performance declines of ¥11 billion in other corporate areas.

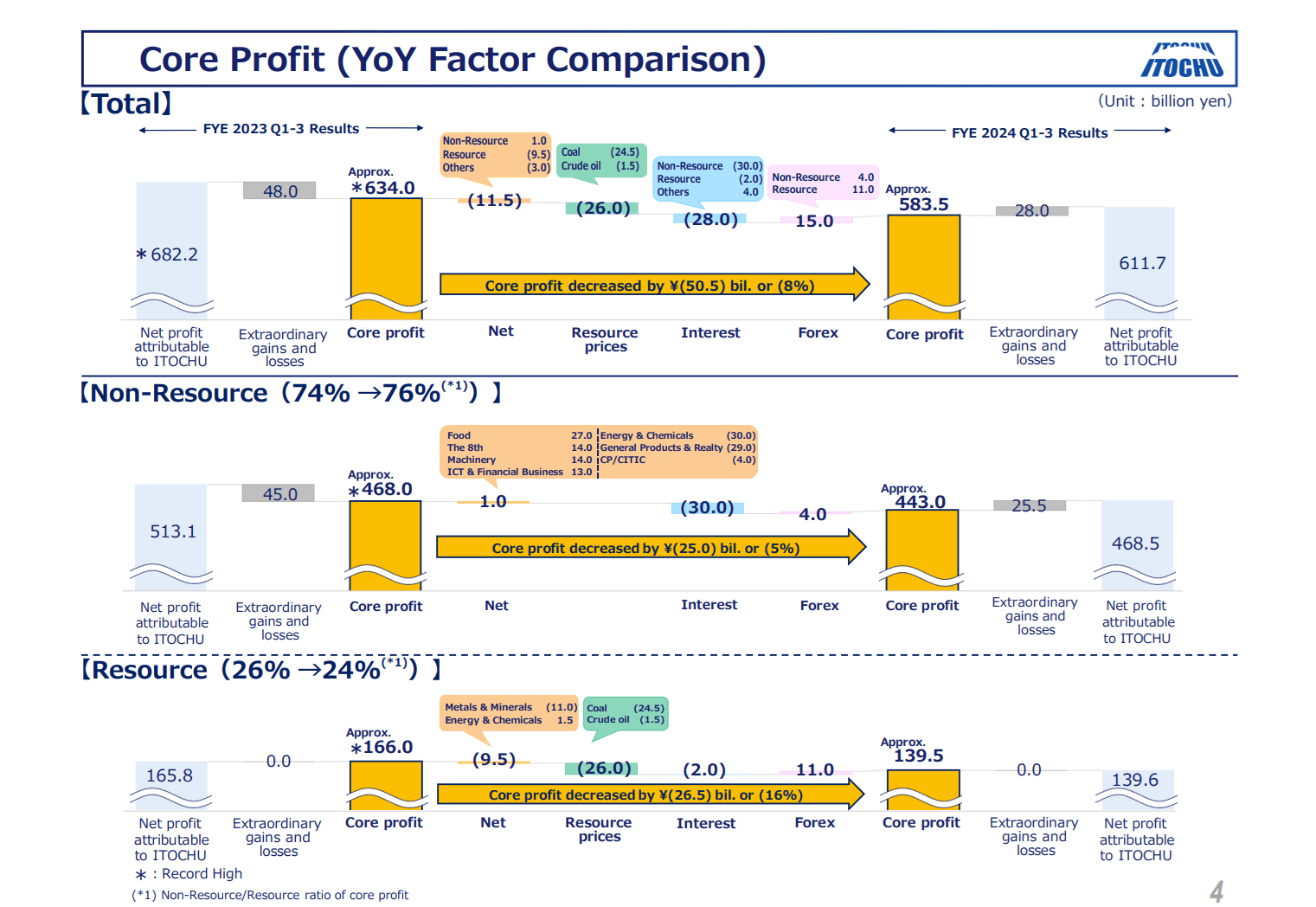

Looking at the company overall, compared to the first 9 months of fiscal 2023, we see that lower coal prices have been a major headwind, along with higher interest rates, partially offset by the benefits of a weaker yen. Outside of these environmental factors, performance within the company’s control (seen as the “Net” Core Profit bar on the chart below) was basically unchanged from last year in the non-resource businesses and down about 6% in the resource businesses. Lower energy and chemical trading performance appears to be driving this shortfall.

Itochu Corp.

Outlook

Looking at Itochu’s chance of hitting the current plan for FY 2024 with one quarter left, it appears that the overperformance in Machinery, the 8th Company, and Food can make up for shortfalls in Textile, General Products & Realty, and ICT & Financial. Although Metals & Minerals is only at 69% of the full-year plan through three quarters, iron ore prices have stabilized above where they were at the start of the fiscal year, and coal so far does not seem to be getting any worse. There also remains the -¥30 billion loss buffer which provides some cushion for the company if any of the segments fall short. Overall, I am comfortable with the ¥800 billion full year profit plan, but I do not see the company exceeding it by more than ¥20 billion (2.5%). This could allow for at most a ¥5 per share bump in the year-end dividend, but I would not count on that.

Looking forward to the company’s FY 2025, which starts in April, Itochu will not release their annual plan until the Q4 and year-end results are announced in May. For my first estimate, I am going with an assumption that commodity prices remain stable as I did in my recent article on Mitsui & Co., Ltd. (OTCPK:MITSY, OTCPK:MITSF). Itochu makes forecasting more difficult than Mitsui by not including a medium-term commodity volume forecast in their earnings supplement, but we can see that iron ore production was up about 9% and oil and gas down about 11% in FY 2024 compared to 2023. On this basis, I am forecasting the profit for the resource businesses to be unchanged in FY 2025, while the non-resource businesses will have growth around nominal Japanese GDP. The most recent economic outlook from the Bank of Japan forecasts real GDP growth of 1.1% and a CPI increase of 2.35%. Applying the 3.45% increase to the non-resource businesses, my prediction for Itochu’s profits in FY 2025 is ¥820 billion.

Valuation

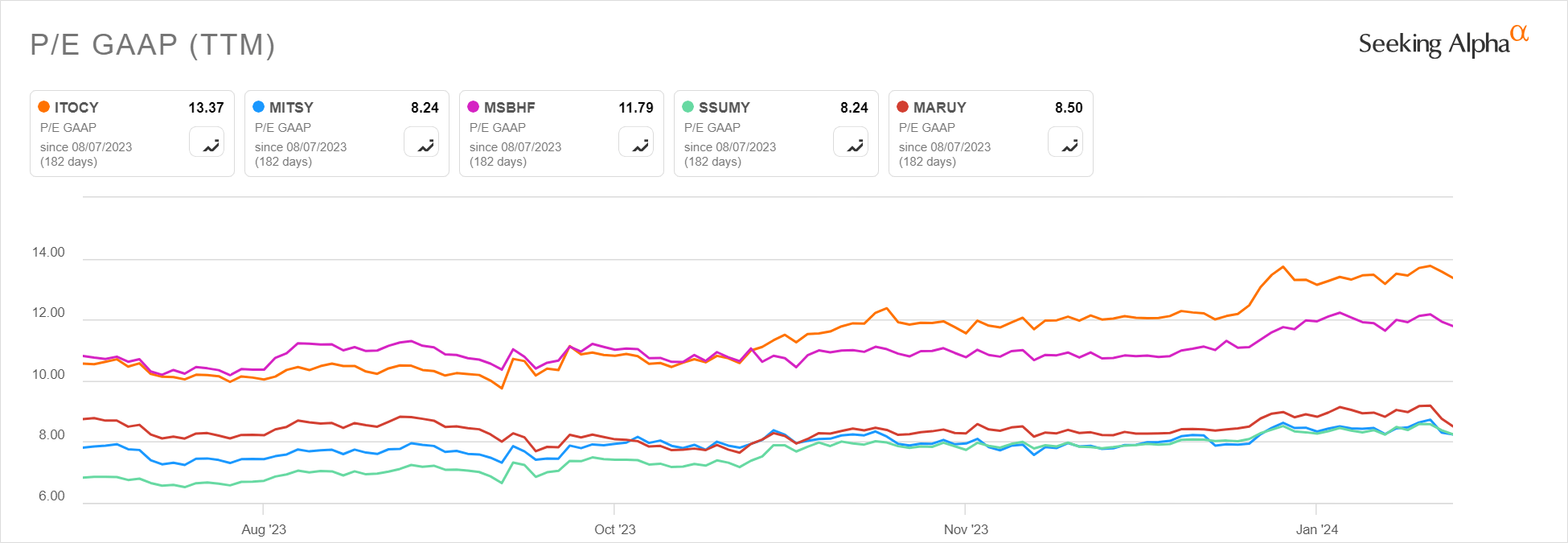

Since my last article, Itochu regained its status as the highest-valued trading company by P/E, outpacing Mitsubishi Corporation (OTCPK:MSBHF).

Seeking Alpha

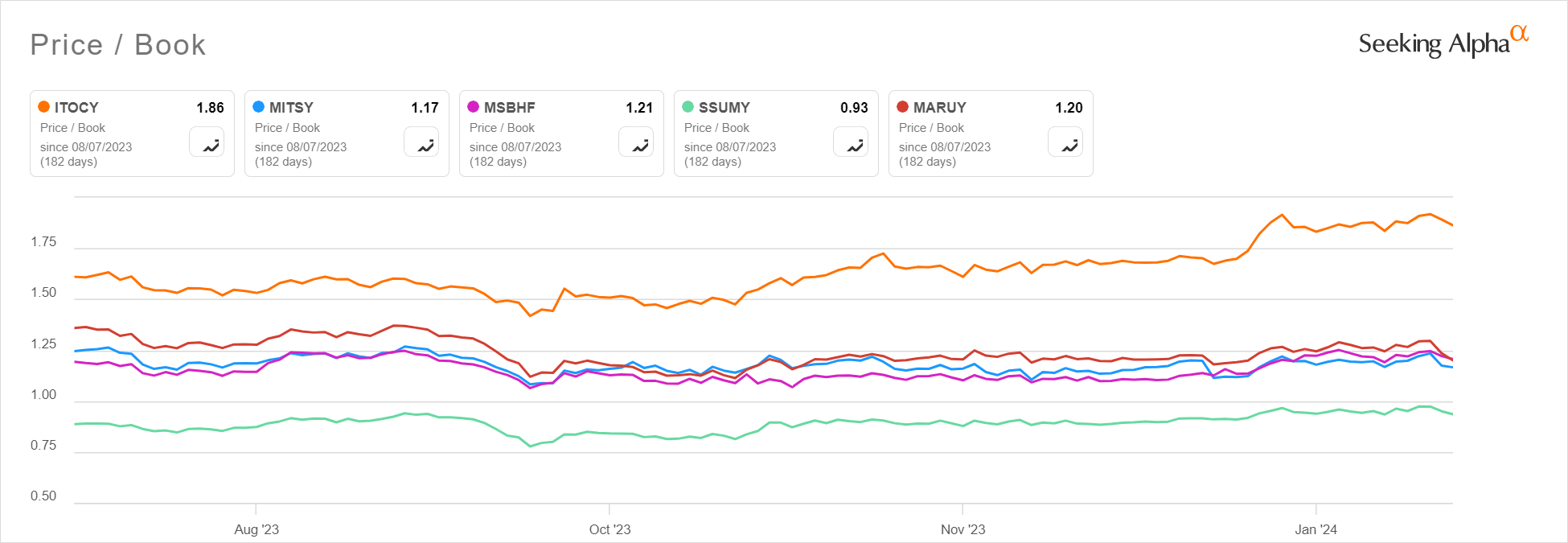

Itochu also further widened its premium price/book ratio over its peers.

Seeking Alpha

Itochu continues to have the highest return on equity, based on the 2024 profit forecast, at 15.65%, but this is now only slightly above Marubeni Corporation (OTCPK:MARUF, OTCPK:MARUY) which has a lower valuation, in the middle of the pack on both P/E and P/B. The run in the share price also gives Itochu the lowest dividend yield at 2.4%.

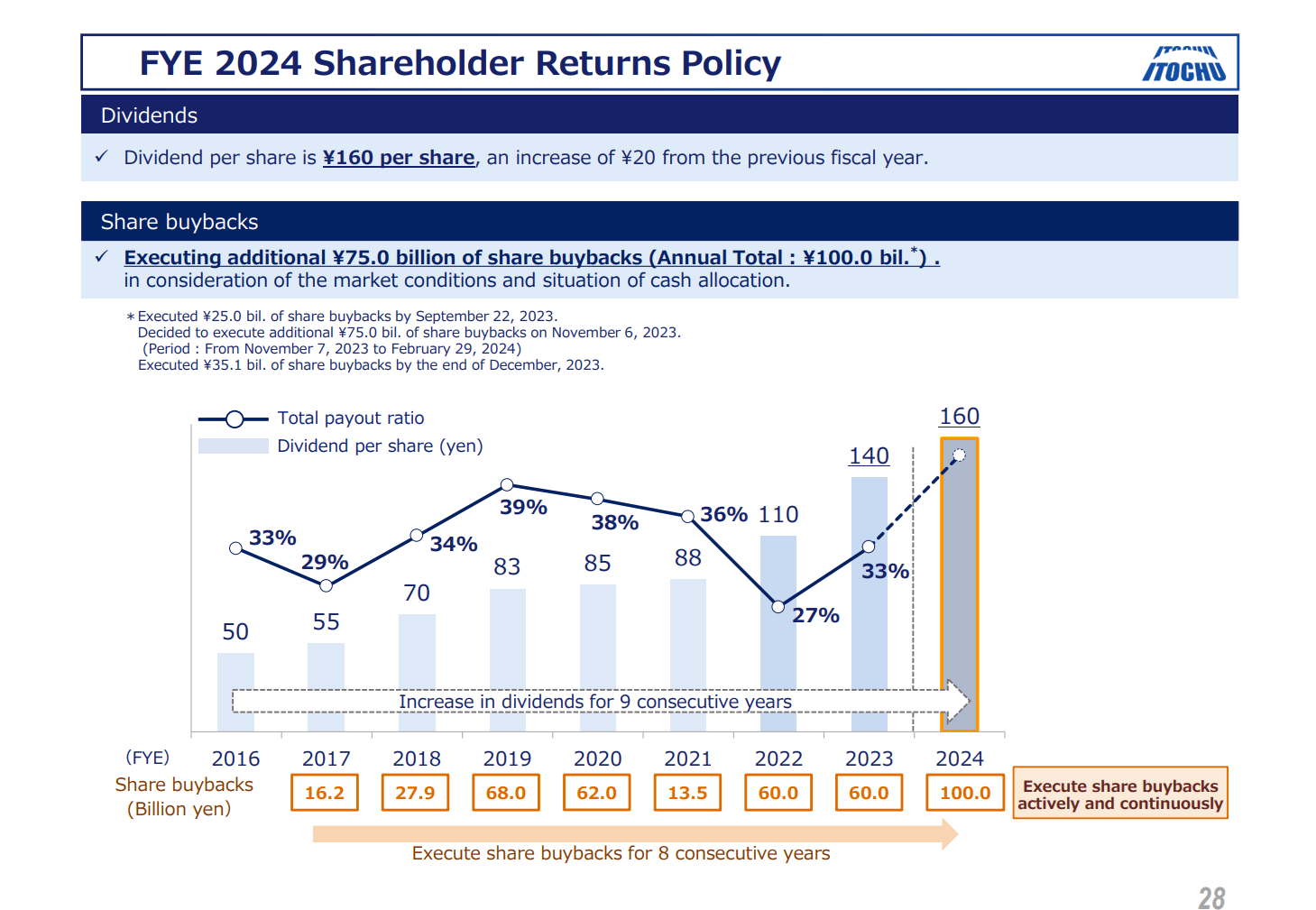

Capital Management

Itochu had a core free cash flow of ¥196 billion in fiscal YTD, down from ¥305 billion in the same period last year. The full year dividend forecast of ¥160 per share would use ¥232.4 billion. Itochu has also completed share buybacks of ¥60 billion so far this year, with plans to purchase ¥40 billion more in fiscal Q4. With a total capital return plan of ¥332.4 billion in FY 2024, Itochu needs to generate ¥136.4 billion of free cash flow in Q4 to fully cover dividends and buybacks. This would be above ratable delivery from the first three quarters, so it appears aggressive unless there is a planned asset sale or working capital release.

The ¥332.4 billion total capital return represents a payout ratio of 41.6% of plan net income this year. Noticeably different this quarter was the deletion from the shareholder returns slide of a reference to a 40% payout ratio target and possible upward revision in the profit forecast this year.

Itochu Corp.

With the currently planned shareholder returns now above the 40% payout ratio target, I now put a low probability of a significant dividend increase from Itochu Corporation above the ¥160 per share forecast for the fiscal year. I think a small bump is possible, but only if the loss buffer is not used and the final profit result is above ¥830 billion.

Conclusion

The Itochu Corporation share price has increased significantly in the past 6 months, further extending its premium valuation on P/E and P/B over the other Japanese trading companies. This is despite only a small increase in the company’s profit forecast. The planned record level of buybacks does not leave any room for dividend increases based on a total capital return target of 40% of profits. I now see minimal upside to the FY 2024 profit forecast of ¥800 billion, probably only the release of the ¥30 billion loss buffer at year-end.

For FY 2025, I expect flat commodity prices and only modest growth in the non-resource businesses in line with the Japanese GDP. The recent run-up in the Itochu Corporation share price has outpaced the improvement in company fundamentals, making Itochu a Hold.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")