Wirestock

Holding Steady In A Tougher Environment

Since 2020, BP p.l.c. (NYSE:BP) has been pursuing a strategy to transform from an “international oil company” to an “integrated energy company” in their words. With the world not going green as fast as BP’s management originally thought, the company pivoted slightly one year ago to be less aggressive in ramping down oil and gas production while still planning to grow renewable energy capacity. It’s been six months since I last covered BP, rating it a Buy. At that time, the company had just announced a mid-year dividend increase for the second year in a row, indicating confidence in its ability to deliver its strategic plan.

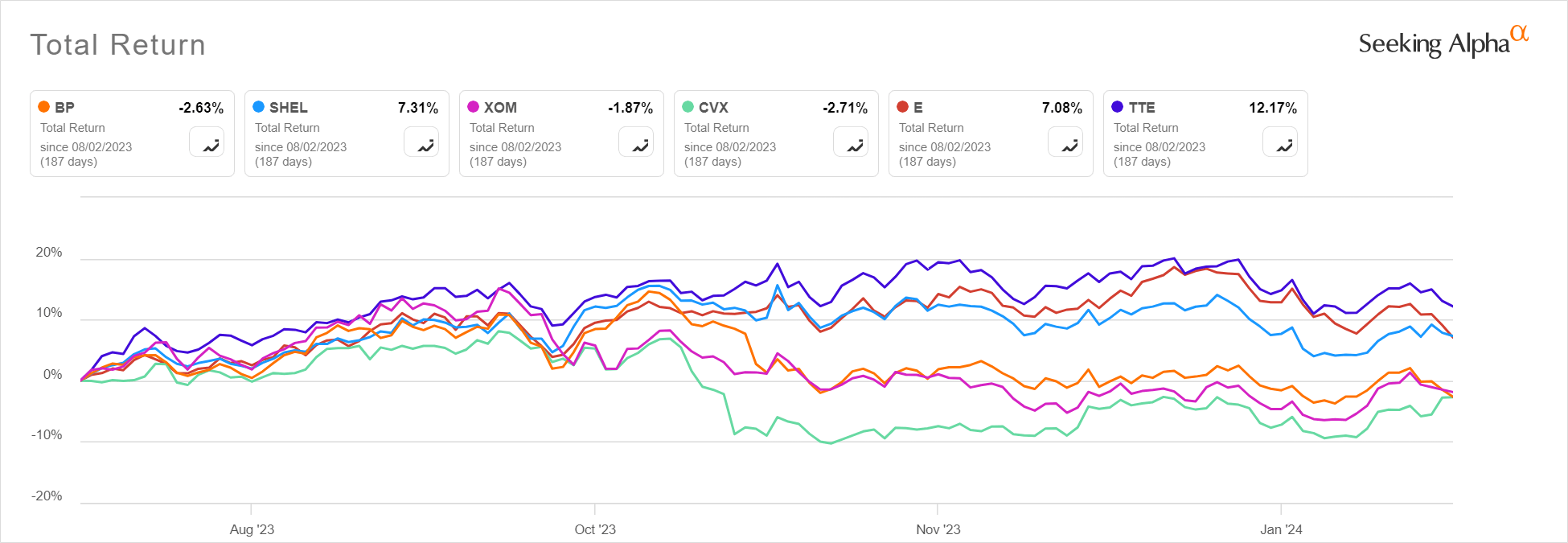

Since that article, the stock has gone basically nowhere, with a total return of -2.6% prior to the release of 4Q and full-year 2023 earnings. This is right in line with BP’s two biggest US peers, Exxon Mobil Corporation (XOM) and Chevron Corporation (CVX). Perhaps surprisingly, BP’s European peers have done better over that time frame. BP closed the gap with the Europeans and moved ahead of the US majors with a 6% rally on the day of the earnings release, not yet shown on the chart.

Seeking Alpha

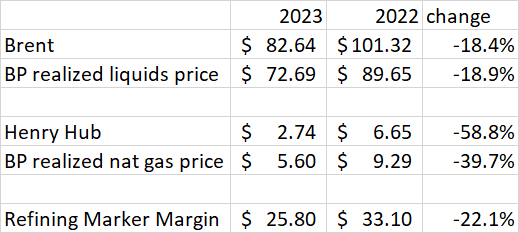

Even a flat stock performance is a decent result considering the decline in the commodity pricing environment and BP’s results in 2023 compared to 2022. BP’s underlying replacement cost operating profit was down by almost exactly half in FY 2023, to $13.84 billion from $27.65 billion in 2022. Commodity market prices and BP realized prices were also down:

Author Spreadsheet

One key development at BP was the appointment of Murray Auchincloss, the former CFO, as the new CEO, replacing Bernard Looney. Any investors looking for a bigger pivot away from renewables under the new boss will probably be disappointed. The theme of the earnings call was “steady as she goes”. The new CEO has no plans to curtail renewables investments. Nevertheless, BP continues to invest to sustain its oil and gas production at least through 2025 and dropped hints that it is open to slowing the planned decline between 2025 and 2030. Within renewables, the investment plan has not changed, but the focus remains on profitability and simplification.

On the financial side, BP continues to bring down its net debt. The one new development in the capital return plan is that free cash flow after dividends will now be allocated 80% towards buybacks and 20% towards debt reduction. Previously, this split was 60/40. Although no dividend raise was announced today, BP has now committed to $14 billion of buybacks over the next two years, or almost 14% of the current market cap.

While the strategy has not shifted much, I now see the potential for a 15.3% annualized total return for BP through 2030, assuming a similar commodity price environment, up from 13% in my last article. The core of these returns is still driven by oil and gas. The risk of overdoing the green agenda seems incorrectly overemphasized by the market, making the stock a Buy.

Delivering The Strategy

bp

Oil And Gas

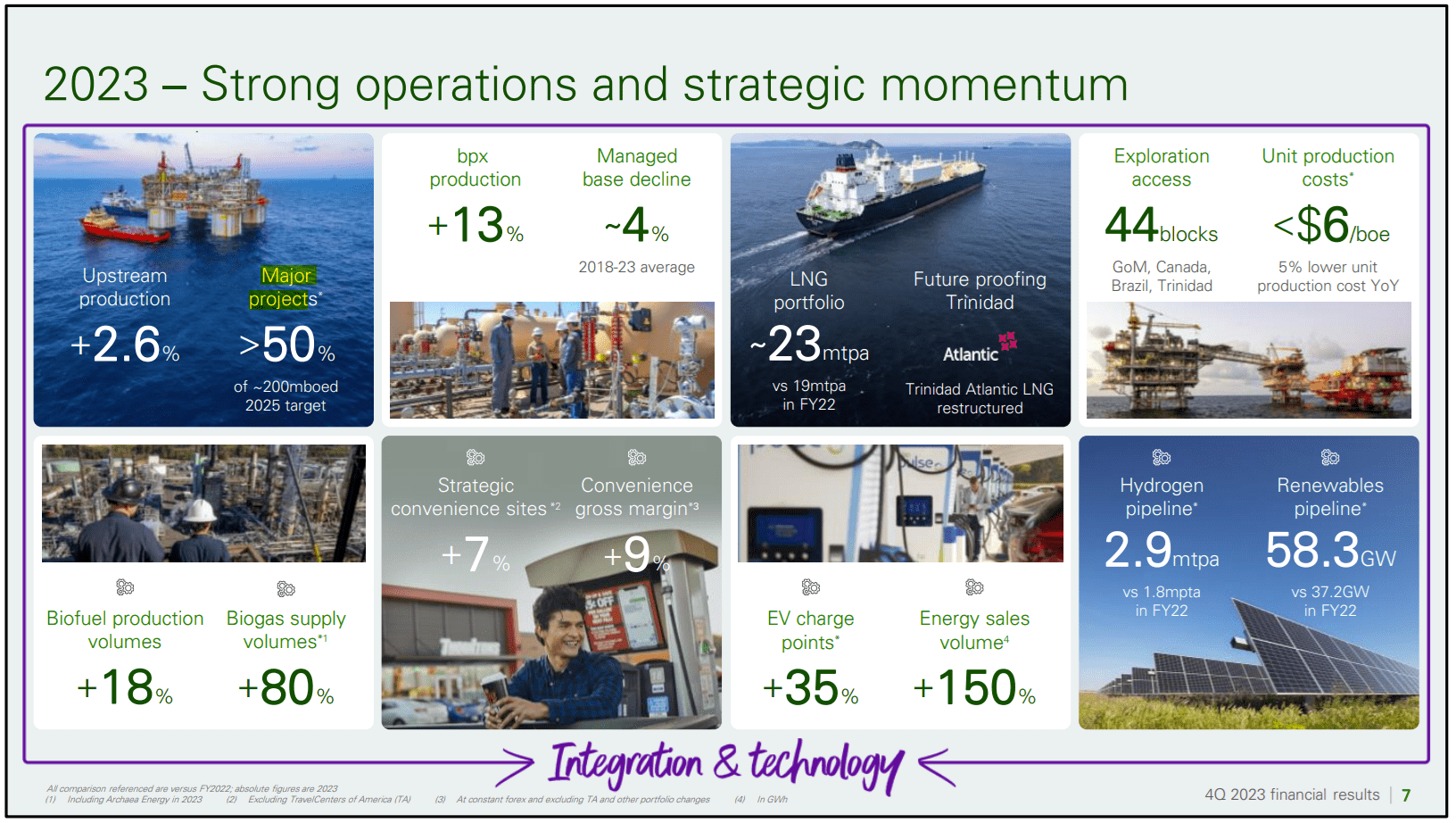

BP grew its total upstream production by 2.6% in 2023, to 2,313 mboe/d. Regardless of the green talk, this growth was mostly in oil, offsetting flatter natural gas production growth. Looking forward to 2024, guidance is for more of the same. The company started up four major projects in 2023 and is planning to have six more online by 2025. Compared to other oil majors, BP’s activity in onshore US areas like the Permian is often overlooked due to the size and global scope of the company. Still, bpx, as the onshore US business is called, could be its own mid-major company. The division produced 400 mboe/d in 4Q, a growth of 13%. Looking ahead, bpx is starting up two central processing facilities by 2025 to handle this growing volume. Further out, in the second half of the decade, the CEO reminded analysts on the call that BP has the capacity to actually grow oil production by 2%-3% per year at least through 2027.

So what we told everybody in Denver is that we see the capacity to grow our oil production, so to speak, by 2% to 3% through 2027. As we look ahead over the next 2 years, we have some big decisions on sanctions as well that will determine what happens beyond that, Os. So you have Cabo Frio in Brazil. You’ve got Kaskida, Tiber, and Gila in the Gulf of Mexico and the Paleogene [indiscernible] Northern Canada, you have clear expansion. You have Abu Dhabi expansion. I’m probably missing some that I can’t think of off the top of my head, but you have these massive projects, some of which are held 100%. I think Paleogene 9 billion barrels 100%.

While the current plan shows flat production through 2025 and a gradual decline through 2030, these barrels are available if they are economical to produce and BP decides to go after them. As Murray said on the call,

Our reserve replacement ratio has been a bit low in the past. It’s going to get back much more competitive now, as we look at these 12% to 16% sanctions across the next 2 years.

What the volume outcome from that will be? Hard to predict. We’ve given you 2 million a day by the end of the decade, 2% to 3% growth through ’27 on oil, but I think the sanctions will really determine that. So as we get through ’24 and ’25 and decide those, then we’ll update you in due course about what 2030 really looks like based on all those sanctions. So I have a bias for returns. I don’t necessarily have a bias for volume or oil gas on returns by ourselves.

Renewables

BP made a step change in its biofuels business by acquiring biogas producer Archaea Energy. Archaea is already delivering production and will add about 50 mboe/d by 2030 on top of the 100 mboe/d that were in the model at the time of my last article.

BP took a step forward in its retail business by acquiring TravelCenters of America in 2023. While providing another outlet for its traditional diesel and gasoline sales, TA can also be used to deliver biofuel and EV charging. Speaking of EV charging, BP has narrowed its focus since the 2020 strategy rollout and is now concentrating on four countries – the UK, Germany, the US, and China. Two of these countries are now profitable with the overall charging business expected to be EBITDA positive by 2025.

Simplification is a theme in other renewable businesses as well. BP has agreed to acquire the portion of solar JV Lightsource BP that it does not already own. On the wind side, BP is ending its partnership with Equinor ASA (EQNR) on the US east coast, with BP taking full ownership of the Beacon project in Long Island Sound, and Equinor taking the Empire project to the southeast of Long Island.

BP seems to be investing in renewables in a measured and smart way, with EBITDA from low-carbon energy increasing from just 1.3% of group EBITDA in 2025 to 4.2% in 2030.

BP Stock: Financial Model Update

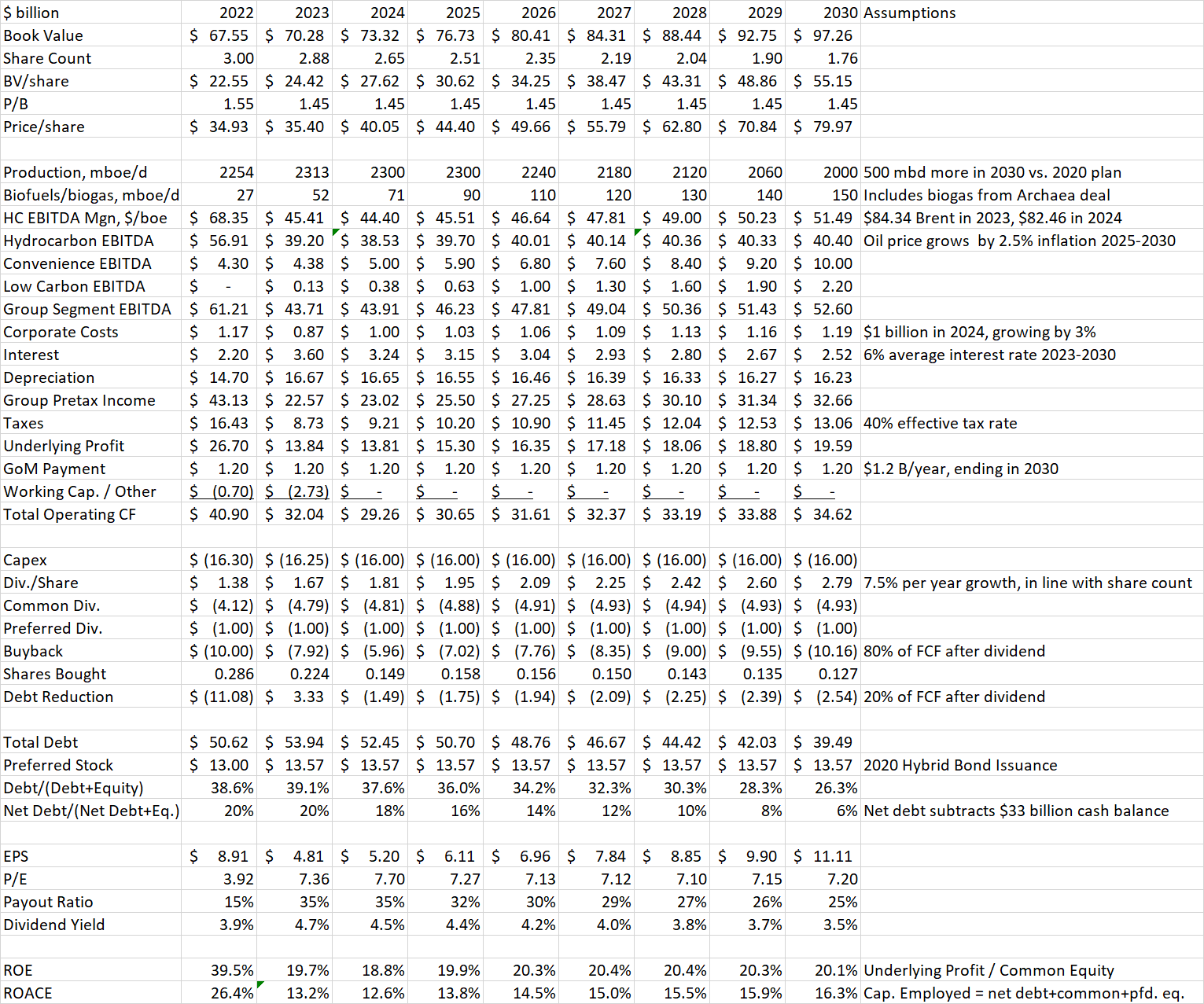

I have updated some assumptions in the model used in my last article. Traditional oil and gas production rates have not changed, but I added the planned biogas production from Archaea. For hydrocarbon margins, I am now using a real 2021 Brent price of $70, in line with company planning assumptions. With inflation, a $70 real Brent price in 2021 equates to $82.46 in 2024, not far off current conditions. I increase this by 2.5% per year through 2030. Natural gas prices and refining margins are assumed to move similarly.

Corporate costs have been reduced to $1 billion per year in 2024, down from $1.2 billion based on company guidance. I raise these by 3% per year going forward for inflation. I now assume 6% interest on debt, up from 5.5% last time, and a 40% effective tax rate.

On the capital management side, I use a capex plan of $16 billion per year through the end of the decade. BP promises only a 4% per year dividend increase to ensure that the dividend is sustainable at Brent prices as low as $40. In practice, however, they have raised it faster with 2023’s payout of more than 20% over 2022. Going forward, I assume a 7.4% per year dividend increase, in line with share count reduction. I am using the new 80/20 split between buybacks and debt reduction that BP announced. Gearing (Net debt/(net debt + equity)) is down to about 20%, its lowest level in a decade. Even with the increase in buybacks, gearing still reaches single-digit percentages by the end of the decade, probably further than BP really needs to go to maintain their A debt rating. The company has room for even higher dividend increases, more capex, or cushion in the event of lower commodity prices. For my share price estimation, I assume a constant price/book at the current value of 1.45.

Author Spreadsheet

The model shows that BP’s stock price reaches about $80/ADS in 2030. Dividends grow at 7.5% per year, reaching $2.79/year in 2030. Total return comes out to 15.3% per year annualized. This is based on a 2024 starting share price of $35.40 and a 7-year period through the end of 2030.

Valuation And Peer Comparison

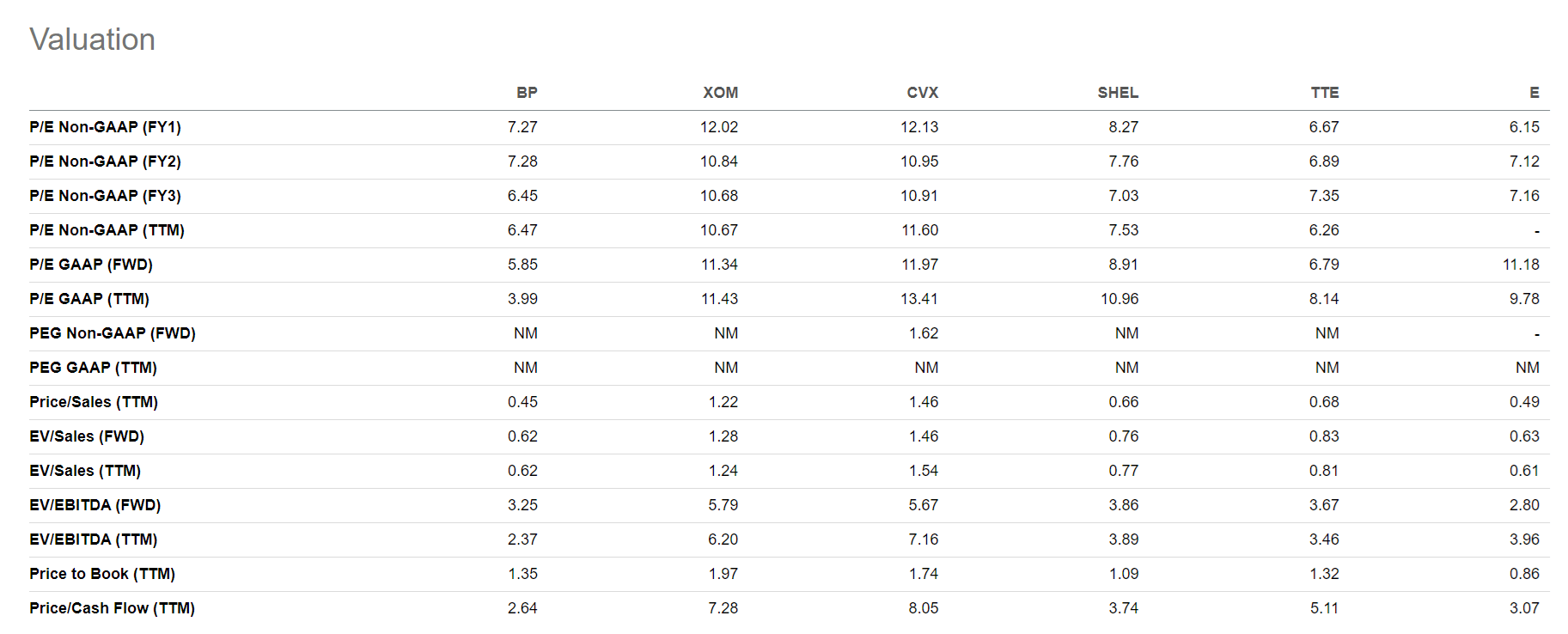

BP is valued cheaper on 2024 earnings than either US major or Shell, but slightly more expensive than TotalEnergies SE (TTE) or Eni S.p.A. (E). Using analyst consensus of 2026 earnings, BP is the cheapest of the entire group. Note that the analyst consensus of $4.85 in 2026 is below my estimate of $6.96.

BP Peer Comparison Tool (Seeking Alpha)

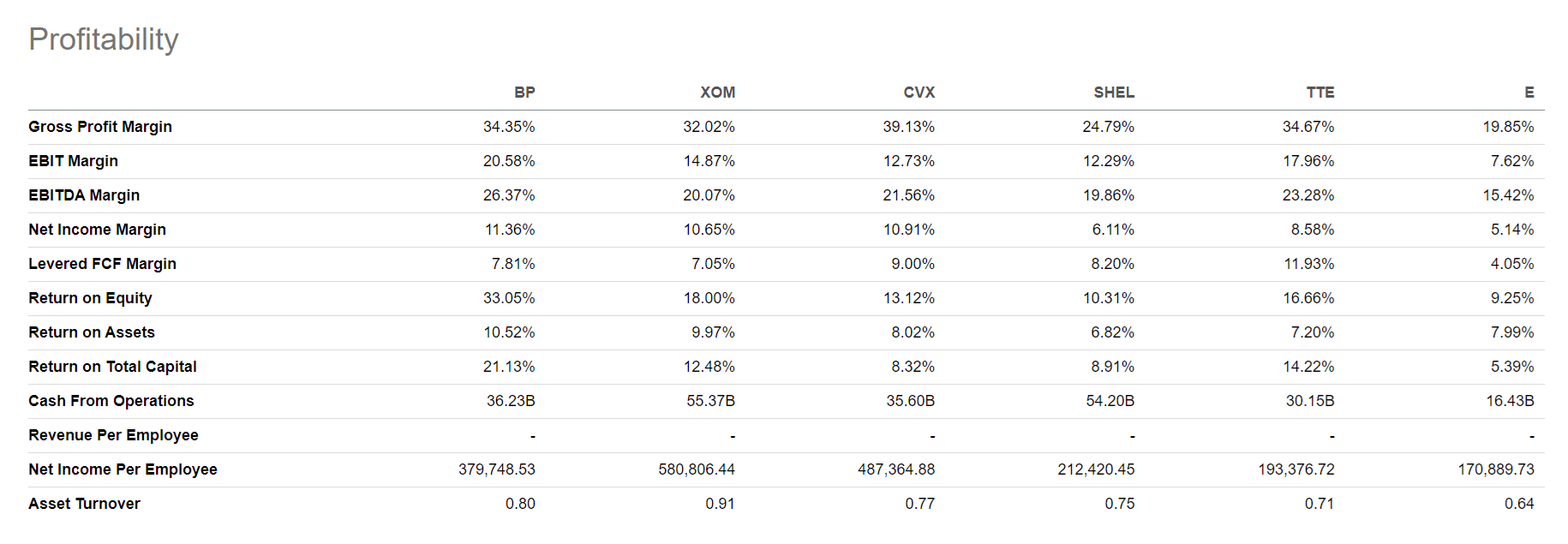

BP has one of the lower P/E valuations despite ranking at the top on most profitability metrics like returns on equity, assets, and total capital.

Peer Comparison Tool (Seeking Alpha)

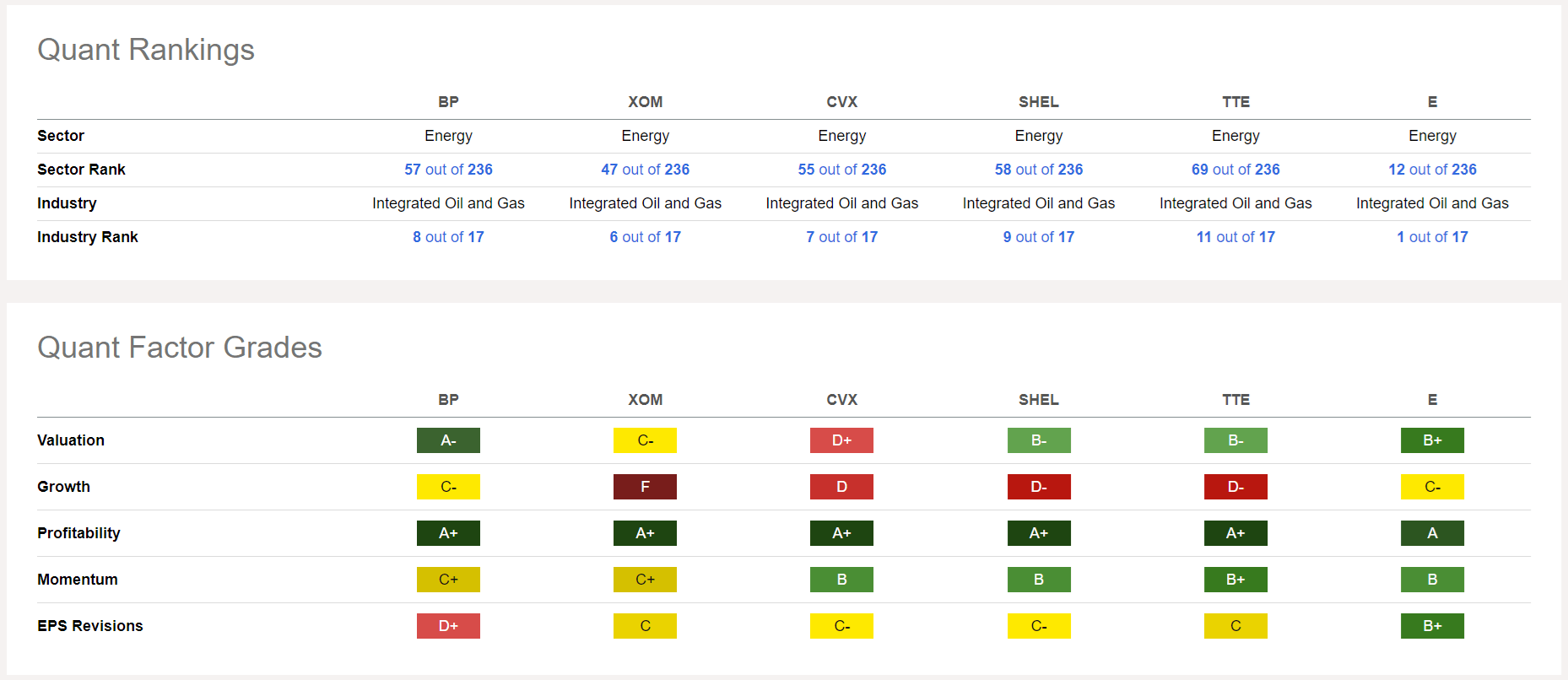

Looking at Seeking Alpha’s Quant Factor grades, BP is rated best or tied for the best on Valuation, Growth, and Profitability. I expect the lower Momentum grade to improve following the share price rise after the earnings release. EPS Revisions can improve as well if the company delivers the results used in my model. Although currently ranked 8th of 17 Integrated Oil and Gas companies, BP has the potential to move up.

Peer Comparison Tool (Seeking Alpha)

Conclusion

BP is maintaining a steady course under its new CEO. While the company is not dialing back its investments in renewables, oil and gas production has resumed growing with projects in the hopper to grow further if the company decides to pursue them. Even within renewables, biofuels are taking off, EV charging is headed for profitability in 2025, and wind and solar businesses are becoming more simplified.

My latest financial model update now estimates a 15.3% annual return through 2030 including a 7.5% per year dividend increase. The company has pared its debt and can continue doing so in the current commodity price environment, even with its massive buyback program. BP looks cheap compared to peers and remains a Buy.

Q2 2024 Earnings Call Transcript")