PATRICK T. FALLON/AFP via Getty Images![]()

Despite being in business for over twenty years, Palantir Technologies Inc. (NYSE:PLTR) is just getting started in many ways. Palantir was widely regarded as a secretive government contractor for many years. It was so mysterious that many market participants had no idea what Palantir did. However, now that Palantir is hitting the mainstream, its commercial business is booming.

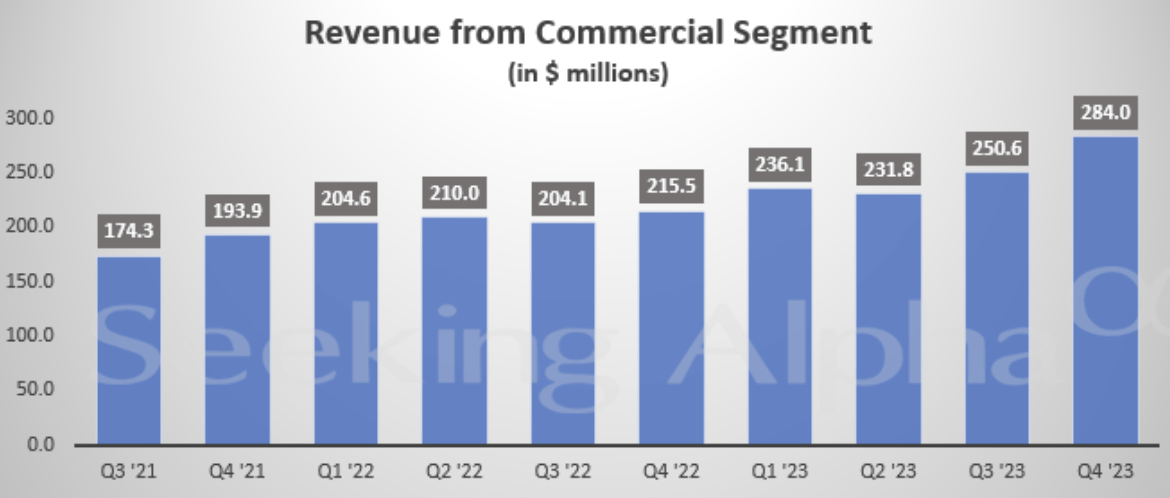

Palantir commercial revenues (SeekingAlpha.com)

Moreover, with its dominant market-leading position in AI software and services, Palantir could experience exponential growth and increased profitability for years. While Palantir’s stock is up by over 100% over the last year, its “Nvidia moment” hasn’t arrived yet. Nonetheless, it’s coming, in my view, and the stock should go considerably higher in the intermediate and long term.

Technically – The Breakout Is Likely Coming

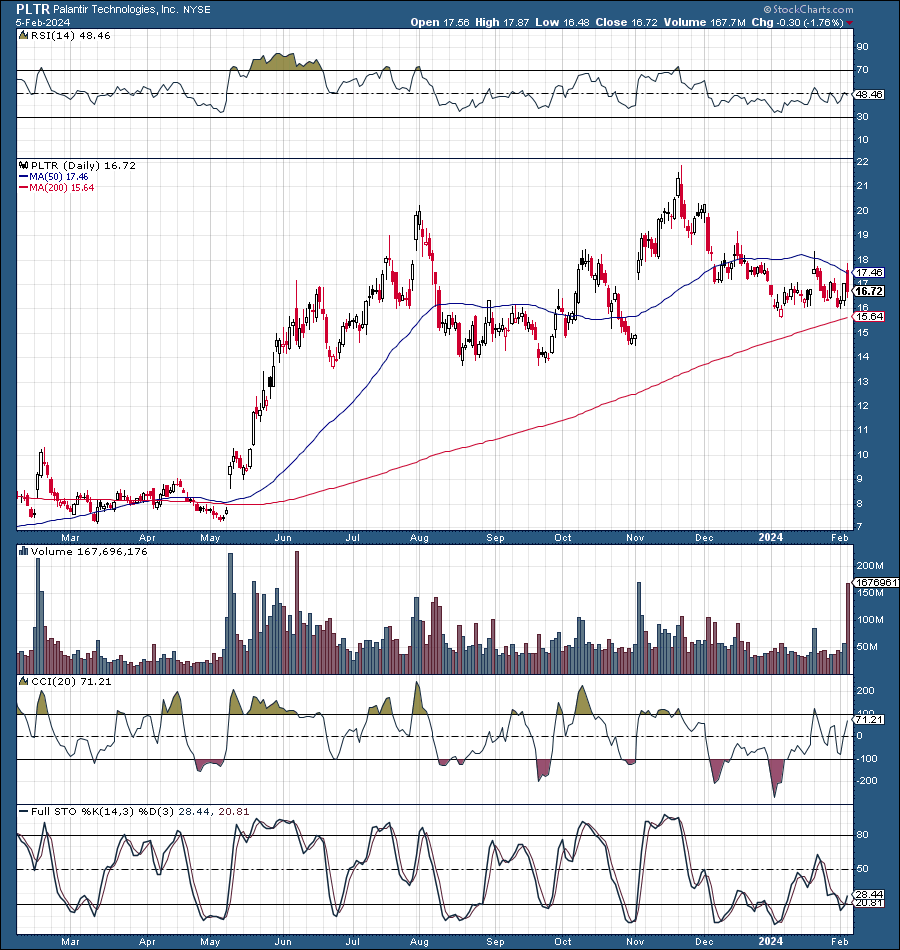

PLTR (StockCharts.com)

Palantir had an excellent earnings report last quarter (Q3 2023), and we’re seeing more of the same in Q4. Palantir’s stock surged in early November after it reported Q3 earnings but failed to break out above the $20-$22 resistance range. As a result, Palantir came back down to the $15-$16 range, filling the gap and creating an excellent long-term buying opportunity.

Yesterday (2/5/24), Palantir provided another solid earnings announcement, and its stock opened above $20 today (up over 21%). Therefore, it’s highly probable that Palantir will retest the all-important $20-$22 resistance range. However, this time, we may see a breakout to $25 or higher, as Palantir’s stock has consolidated for around eight months and has many constructive technical and fundamental tailwinds.

The CCI, RSI, full stochastic, and other technical gauges are turning upward, implying that a shift to a more bullish momentum is approaching and could propel the stock considerably higher. Also, Palantir’s stock has made a series of higher highs and higher lows, suggesting the stock is looking for a breakout to higher trading levels. Palantir’s stock is also between the 50 and 200-day MAs, illustrating that it is no longer overbought technically, providing a solid setup to move higher.

The Nvidia Moment Approaches

What is the Nvidia Moment?

The NVIDIA Corporation (NVDA) moment is when a company guides to significantly better-than-expected sales and profitability due to stronger-than-anticipated demand for AI-related products and services. Nearly a year ago, Nvidia guided to much better than expected revenue and profitability for its fiscal Q2 2024 quarter. The company announced its revenues would be about 50% above the consensus estimates due to increasing demand for AI solutions services and other factors. Nvidia’s stock has more than tripled over the last year.

More recently, Super Micro Computer, Inc. (SMCI) had its Nvidia moment, pre-announcing much better than anticipated guidance, enabling its stock to surge by over 100% in just weeks. Palantir is a market leader in AI-enhanced optimization software platforms and services, and its commercial customer count and revenues are growing substantially. While Palantir’s recent earnings were impressive, and the stock surged by around 18% after hours, its Nvidia moment is still to come.

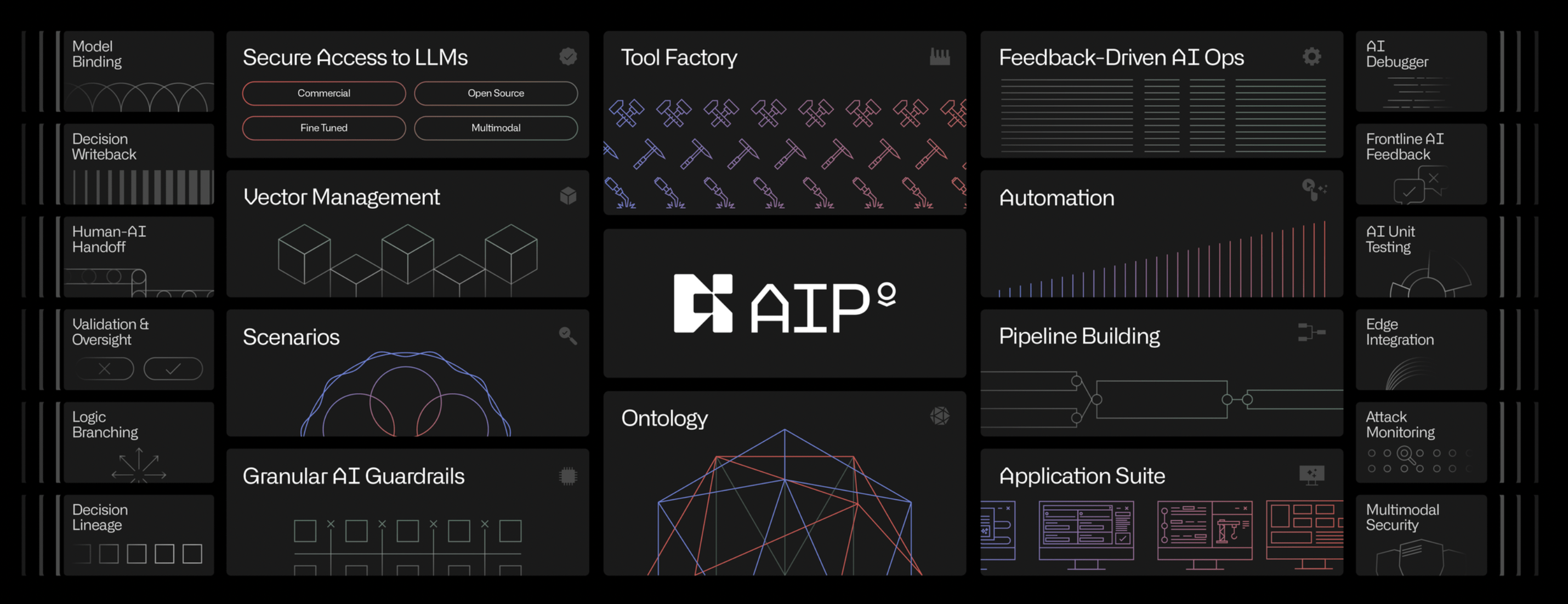

Palantir’s AIP Platform

Palantir’s Artificial Intelligence Platform “AIP” is a full-spectrum AI platform that drives enterprise operations.

AIP (Palantir.com)

Palantir offers AIP boot camps to get customers from zero to use cases in days, enabling enterprises to solve real business problems immediately. AIP is powered by Ontology, a decision-centric system at the heart of AIP that integrates AI with enterprise data, logic, and action. From secure LLM access to end-user applications, AIP provides an integrated architecture that brings full spectrum AI to life, optimizing the everyday decision-making process.

AIP Solutions and Services Include:

- Semantic Data Layer.

- Dynamic Logic Layer.

- Kinetic Action Layer.

- Granular AI Guardrails.

- AIP Logic.

- AIP Scenarios.

- AIP Automate.

- Vector Management.

- AIP Tool Factory.

- Feedback-Driven AI Ops.

- AIP Application Suite.

- APIs, SDKs, & More.

Every organization, government, and commercial, domestic and foreign, can benefit from Palantir’s comprehensive solutions and services. Palantir has an enormous market share to acquire in future years, making its stock one of the best buy-and-hold candidates for the next decade.

The Results Continue Getting Better

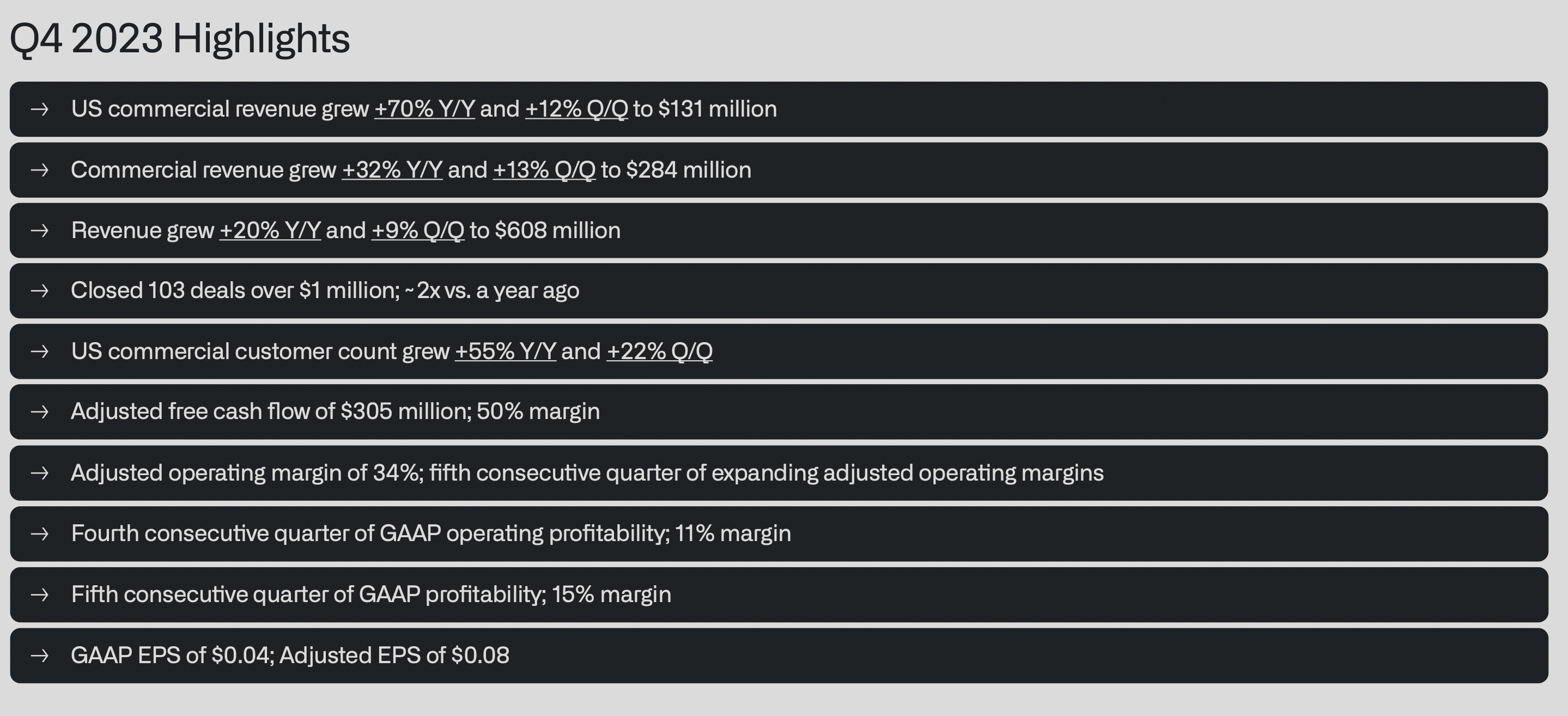

For Q4, Palantir reported non-GAAP EPS of eight cents (in line with estimates) and revenues of $608.35 million, beating by $5.55 million.

Palantir also provided excellent guidance for 2024:

- Revenues between $2.652-$2.668 billion.

- US commercial revenue in excess of $640 million, representing a growth rate of at least 40%.

- Adjusted income from operations of $834-$850 million.

- Adjusted free cash flow of $800 million-$1 billion.

- GAAP operating income in each quarter of this year.

- GAAP net income in each quarter of this year.

Q4 Highlights (Stock Market Analysis & Tools for Investors)

Here’s a staggering fact. Palantir’s U.S. commercial revenues skyrocketed by 70% YoY last quarter. Overall commercial revenues increased by 32% YoY. This dynamic suggests that U.S. companies are ahead of the curve in utilizing Palantir’s solutions relative to their European and foreign counterparts. We should continue seeing robust commercial growth, with international commercial growth likely increasing in future quarters.

In Q4, Palantir closed 103 $1M+ deals, about a 100% increase over last year’s Q4. U.S. commercial customer count expanded by 55% YoY and 22% QoQ. U.S. commercial count has now grown 13x in the previous three years. Palantir also reported its fifth consecutive quarter of adjusted operating margins and its fifth consecutive quarter of GAAP profitability.

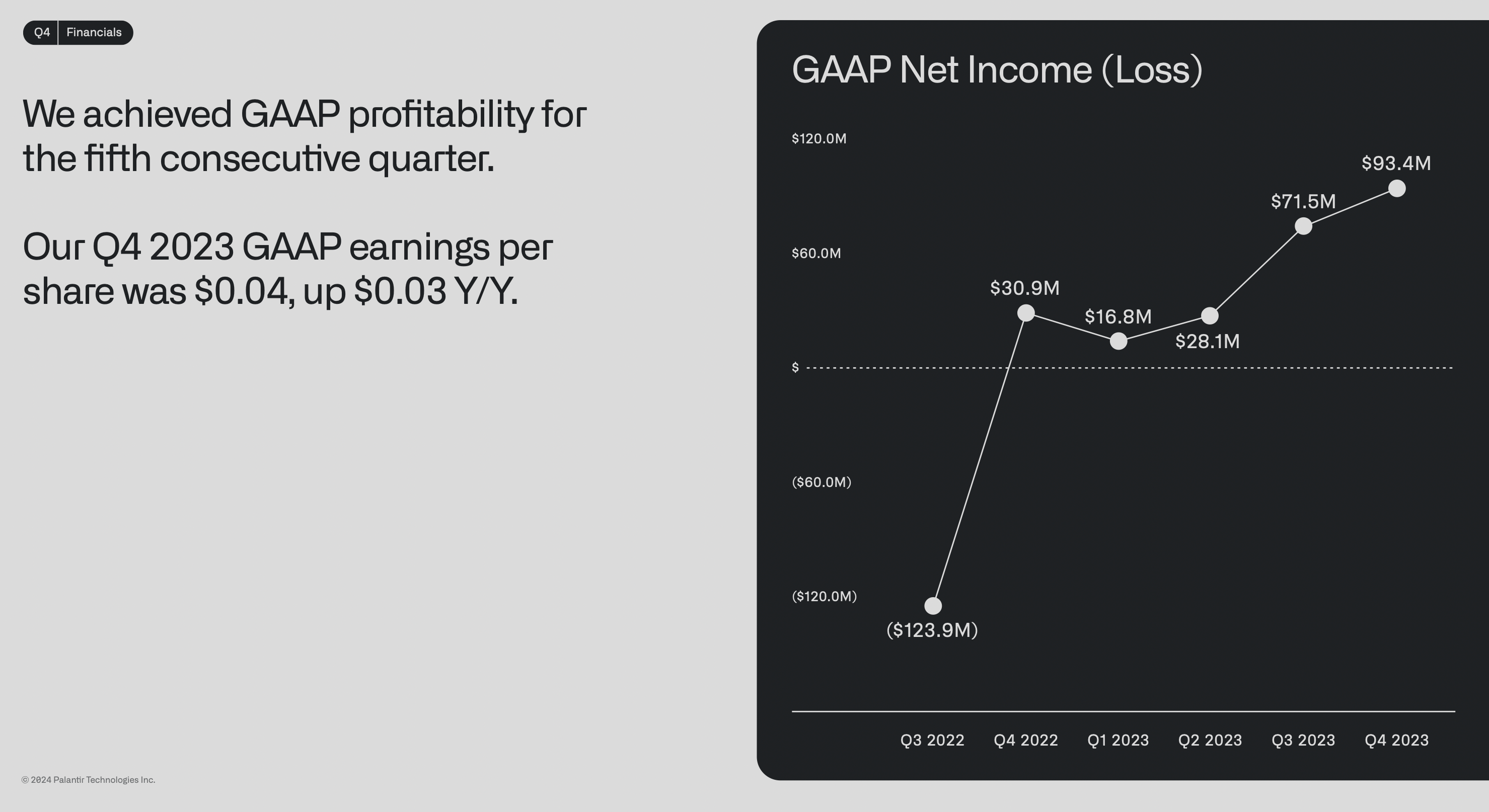

Palantir is Becoming More Profitable

Earnings expanding (Stock Market Analysis & Tools for Investors)

Palantir’s net income has surged from a loss of $124 million in Q3 2022 to a gain of $93.4 million last quarter. Also, Palantir’s stellar gains have occurred in a relatively slow economic atmosphere, compounded by the challenges posed by a high-interest rate environment. Still, so many firms are turning to Palantir to optimize their businesses. Palantir’s growth could accelerate as economic growth improves, and the Fed enables a more accessible monetary atmosphere.

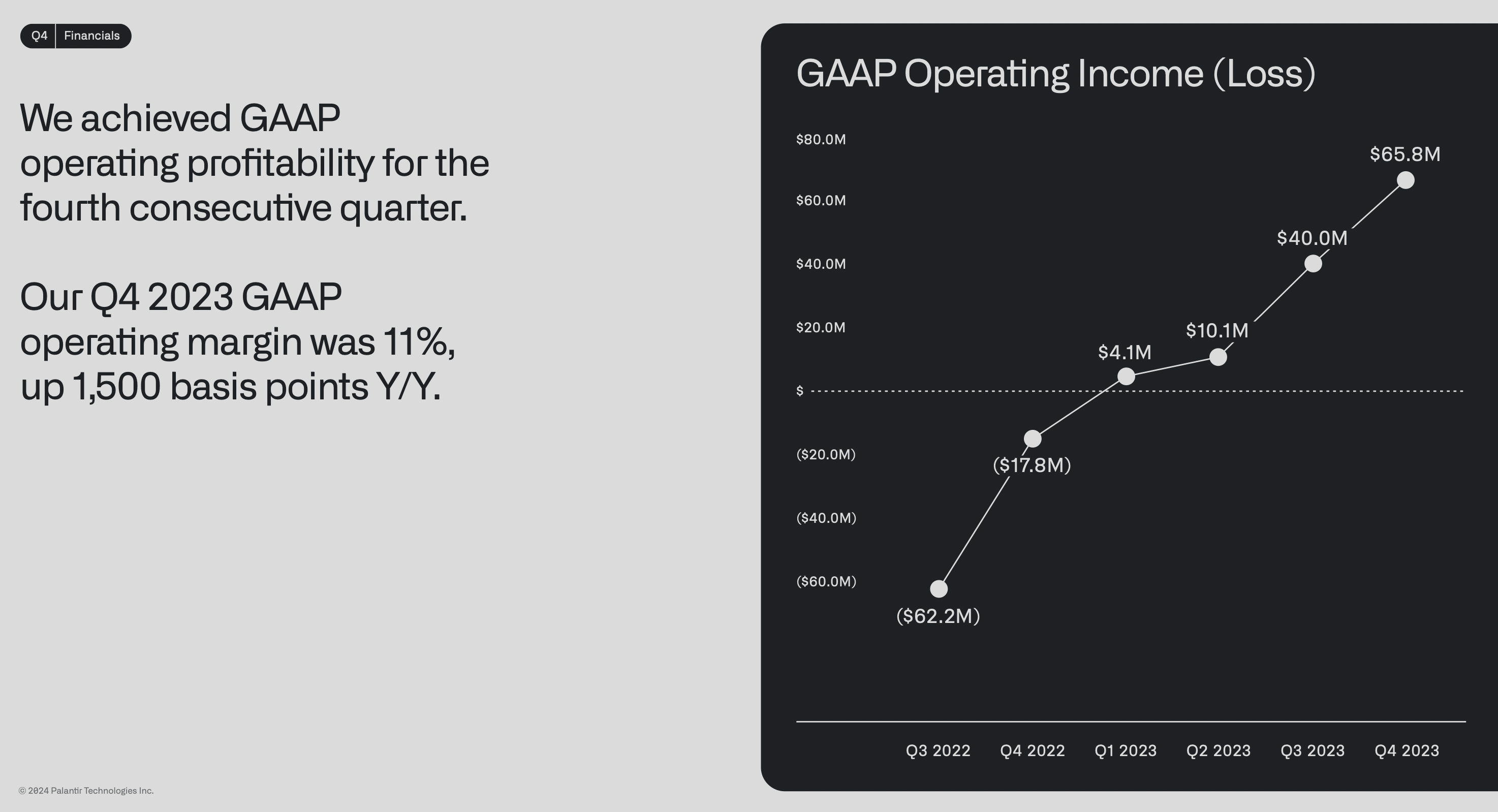

Operating Margin is Surging

Operating income (Stock Market Analysis & Tools for Investors)

Palantir’s GAAP operating income surged to $65.8 million last quarter, illustrating a GAAP operating margin of 11%, up 1,500 Bps YoY. This dynamic indicates that Palantir is growing increasingly profitable with scale and should continue increasing profitability in future quarters. Palantir’s gross margin came in at 84% last quarter, rising over the 82% gross margin QoQ and YoY. This improvement further highlights Palantir’s remarkably high profitability potential and improving profitability with scale.

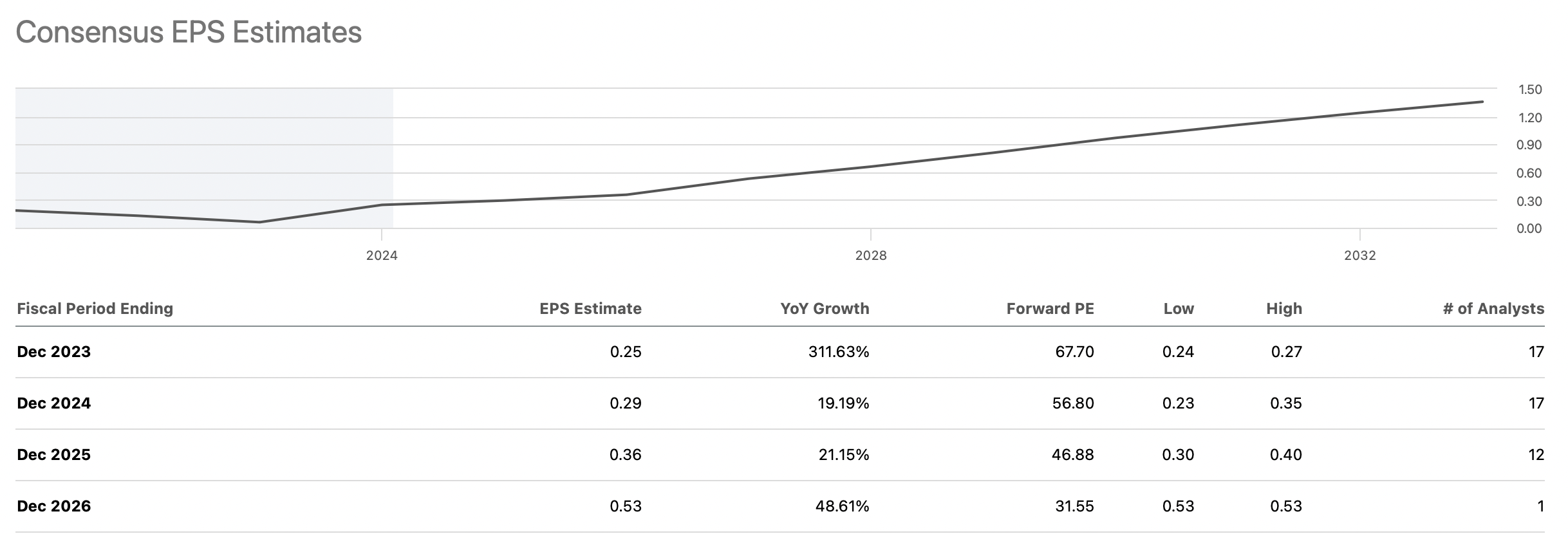

Profitability Could Increase More Than Expected

EPS forecasts (SeekingAlpha.com)

Palantir’s EPS surged by over 300% last year. I must highlight that this stellar performance was achieved during a high interest rate and relatively slow economic environment. Despite Palantir’s surging commercial business growth and rapidly expanding profitability, the consensus estimate is only 19% EPS growth this year.

The $0.29 consensus EPS estimate appears highly depressed, and Palantir can achieve much greater profitability this year, enabling upward earnings revisions for future quarters. In my view, Palantir can earn at least $0.35 in EPS this year, in line with higher-end estimates.

This estimate implies an EPS growth rate of 40% this year, leading to my 35% EPS growth estimate for 2025, suggesting we see around $0.47 in EPS next year. This dynamic illustrates that Palantir may be trading around a 40-forward P/E ratio here, which is cheap for a dominant market-leading company in Palantir’s advantageous position.

Where Palantir’s stock could be in the future:

| Year | 2024 | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 |

| Revenue Bs | $2.87 | $3.64 | $4.6 | $5.7 | $7.1 | $8.8 | $10.7 |

| Revenue growth | 29% | 27% | 26% | 25% | 24% | 23% | 22% |

| EPS | $0.35 | $0.47 | $0.61 | $0.78 | $0.99 | $1.24 | $1.55 |

| EPS growth | 40% | 35% | 30% | 28% | 27% | 25% | 25% |

| Forward P/E | 60 | 58 | 56 | 55 | 54 | 52 | 50 |

| Stock price | $28 | $35 | $44 | $54 | $67 | $81 | $99 |

Source: The Financial Prophet

I’m implementing relatively modest estimates provided Palantir’s market-leading position and potential in AI. Therefore, we could see higher revenue and EPS growth, leading to a more significant multiple expansion and a higher stock price in future years. Still, under this “base-case” scenario forecast, we can see Palantir’s stock price appreciate by about fivefold over the next several years (by 2030), in my view.

Risks to Palantir

Despite my bullish assessment, Palantir faces risks. There is the risk of a slower-than-expected economy and higher rates for longer. There is also the risk of lower-than-expected demand for Palantir’s services, especially from foreign companies and the government side. Palantir’s government segment has slowed considerably, and continued declines could impact the stock. There is also the risk of competition, as other companies are keen to cut into Palantir’s space. Palantir’s profitability could be worse than projected, leading to slower share appreciation. Investors should examine these and other risks before investing in Palantir.

Q2 2024 Earnings Call Transcript")