photovs

Waste Management (NYSE:WM) is poised for slow, yet consistent and sustainable long term growth due to their recession resilient characteristics, annuity like revenue streams, and strategic capital allocation.

Waste Management, the North American titan of trash collection and disposal, isn’t the flashiest company on the block. But beneath the unassuming surface lies a hidden gem: a recession-proof business model generating consistently growing free cash flow, fueling dividend growth for nearly two decades.

This article delves deep into WM’s investment thesis, analyzes its valuation, and reveals why it should be on the radar of every long-term dividend investor.

Weathering Any Storm: A Recession-Resilient Business Model

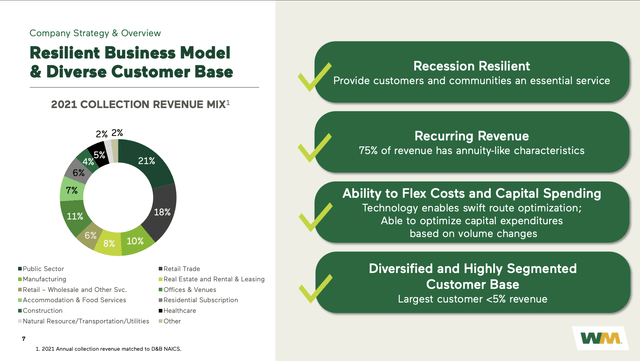

WM’s strength lies in its near-monopoly grip on the essential service of waste disposal. Unlike cyclical industries that crumble during economic downturns, WM’s bread and butter remains untouched. People, regardless of economic conditions, still need their garbage collected. This translates into a remarkably stable revenue stream, with 75% boasting annuity-like characteristics.

WM Business Model (WM Investors Presentation)

I would argue this is one of the biggest selling points of owning Waste Management. Investors love stability and predictability, and that’s exactly what WM provides. But WM isn’t simply content with collecting our refuse. They’re constantly innovating, utilizing technology and automation to minimize their “cost to serve” and enhance the customer experience.

The management team made it clear in a recent presentation that lowering cost to serve through technology and automation is one of the key strategic focuses of the business. This relentless pursuit of efficiency not only strengthens their bottom line but also positions them for continued free cash flow growth.

Fueling Investor Joy: A Capital Allocation Plan that Rewards Shareholders

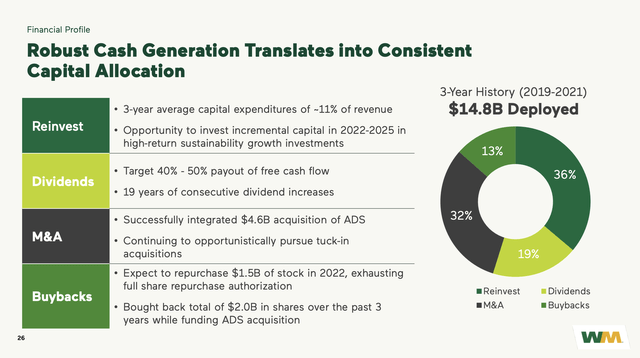

The strength of WM falls on management’s ability to consistently reward shareholders with a strategic capital allocation plan. The company targets to payout 40% to 50% of their free cash flow in the form of dividends. This allows them to use the other 50% of their free cash flow to pursue share buybacks, mergers and acquisitions, and reinvest back into the business.

WM Capital Allocation (WM Investors Presentation)

This capital allocation plan has been advantageous for shareholders, as it’s helped WM grow free cash flow per share from $2.53 in 2013 to $4.11 for the trailing 12 months. The byproduct of this has been 19 consecutive years of dividend growth. While the starting yield for the company is currently sitting at around 1.51%, they also have a 3 year dividend growth rate of 8.70%.

And while growth rate projections for the dividend aren’t in double-digit territory, investors can feel confident that that will be a company that they can rely on to steadily grow their dividend payments year after year for a very long time. With WM, you can rest assured that your dividend stream is in safe hands. With all this being said there are two key factors that I believe could greatly contribute to WM’s ability to reward shareholders in the future.

Hidden Gem #1:

The global conversation around waste management is shifting rapidly. Landfills are overflowing, sustainability regulations are tightening, and the circular economy – aiming to minimize waste and maximize resource recovery – is gaining momentum. WM isn’t just watching; they’re actively shaping this narrative.

Their acquisition of Advanced Disposal Services (ADS) in 2020, a leader in recycling and landfill gas-to-energy, sends a clear message. This isn’t just a bolt-on acquisition; it’s a strategic leap into the circular economy revolution. The company aims to expand its recycling capabilities by diversifying beyond traditional recyclables and capturing valuable materials currently lost in landfills.

Additionally, it plans to develop renewable energy by converting landfill gas into clean energy, thereby reducing environmental impact and potentially creating new revenue streams. Furthermore, the company seeks to become a champion of the circular economy by positioning itself as a leader in sustainable waste management solutions. This strategic approach aims to attract eco-conscious customers and investors, furthering the company’s commitment to sustainability and innovation.

This move isn’t just about ticking sustainability boxes; it’s about unlocking significant growth potential. The global recycling market is projected to reach $531.8 billion by 2025, and WM is strategically positioned to grab a significant share.

Hidden Gem #2:

While WM’s core business might seem low-tech, they’re quietly embracing automation and data analytics to become a leaner, meaner trash machine. Their investments in:

-

Autonomous trucks: Piloting self-driving garbage trucks, potentially reducing costs and improving safety.

-

Smart containers: Deploying sensors that optimize collection routes and predict waste volume, leading to efficiency gains.

-

Data-driven insights: Utilizing data to personalize customer service, identify cost-saving opportunities, and optimize pricing strategies.

These initiatives might seem incremental, but their cumulative impact could be substantial. Imagine a future where your trash can talks to the truck, optimizing collection routes and minimizing fuel consumption. That’s the kind of efficiency WM is striving for, and it translates to higher margins and improved profitability. As their business size grows, increasing profit margins could be one of the keys to WM long term success.

Valuation

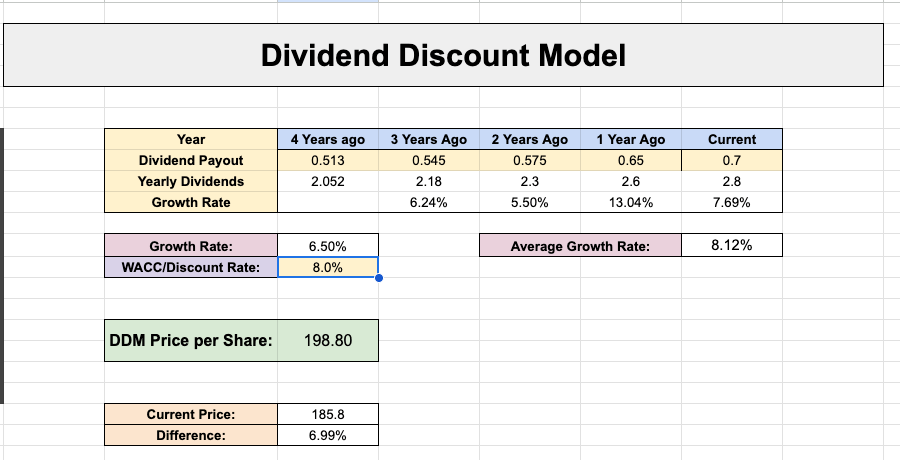

The first valuation we’ll utilize is the dividend discount model. In this scenario, we’re projecting:

– 6.50% dividend growth

– 8% discount rate

Dividend Discount Model WM (Dividendology Patreon)

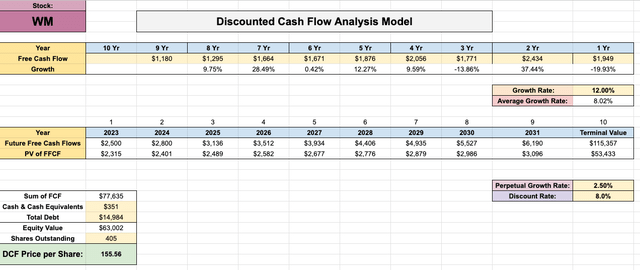

This gives us a fair value of $198.80. The next valuation model we’ll use is the discounted cash flow analysis. This values a company based on how much free cash flow they are expected to produce in the future.

Discounted cash flow analysis WM (Dividendology Patreon)

This gives us a fair value of $155.56.

WM currently trades at the high P/E of 31.07, but if there’s anything I’ve learned over the past decade of investing, it’s that investors are willing to pay a premium for predictability and reliability. But when we look at the P/E ratio of other comparable companies, we can see this high valuation seems to be the standard across the board.

WM price to earnings vs peers (Seeking Alpha)

At its current prices, you do have to pay a premium to be a shareholder. I originally added this company to my portfolio at around $152 a share.

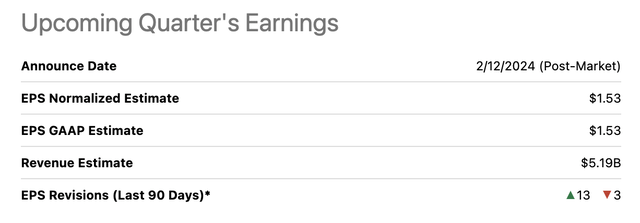

Latest Quarter’s Earnings

WM saw a slight beat on the bottom line and a slight miss on top line earnings in the latest quarter. Analysts seem to be more bullish on the next earnings report to be released on 2/12/24, with WM receiving 13 bullish EPS revisions in the last 90 days.

WM price to earnings vs peers (Seeking Alpha)

Risks

The best place to analyze the risk of any publicly traded company is by analyzing their form 10-k. According to WM management, here are some of the current top risks of the company:

-

WM may be unsuccessful in implementing their technology-led automation and optimization strategy and other improvements to operational efficiency and such efforts may not yield the intended result.

-

Acquisitions, investments and/or new service offerings or lines of business may not increase WM’s earnings in the timeframe anticipated

-

Disruptions or delays in the supply chain may adversely affect the schedule for implementing the proposed expansion of recycling and renewable energy ventures.

Every investment has risk that needs to be addressed. WM is no different. However, I personally believe that the risks involved in holding WM are quite lower than the majority of other stocks in the S&P 500.

A Long-Term Vision: Beyond Short-Term Gains

Investing in WM isn’t a get-rich-quick scheme. Its true value lies in its long-term potential. Its recession-proof nature, focus on efficiency, and commitment to responsible capital allocation make it a cornerstone for any dividend-focused portfolio. While short-term gains are exciting, it’s the future dividend stream that should truly entice investors.

WM’s future is bright. Growing urban populations, stricter environmental regulations, and increasing emphasis on waste recycling all play into its favor. The company is well-positioned to capitalize on these trends, further propelling its growth and securing its place as a dividend staple.

The Final Verdict: A Worthy Addition to Your Dividend Arsenal

Waste Management may not be a flashy tech startup or a high-growth disruptor, but its unassuming strength lies in its unwavering commitment to its core business: efficiently managing our waste.

This stability, coupled with its robust free cash flow generation and consistent dividend growth, makes WM a compelling investment for any long-term dividend investor (at the right valuation) seeking reliable returns and recession-proof resilience.

Q2 2024 Earnings Call Transcript")