BalkansCat

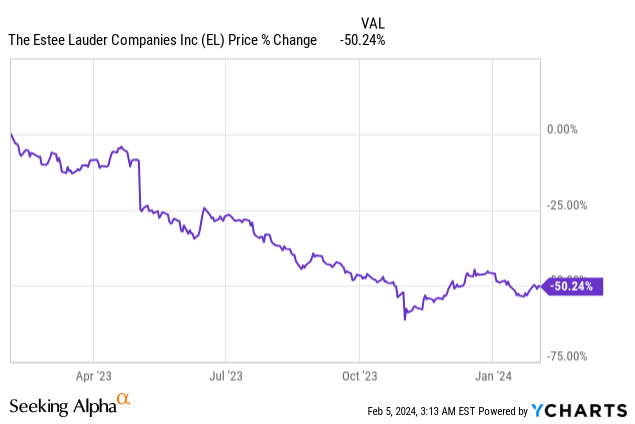

Estee Lauder (NYSE:EL) has had a rough past year with the stock down about 50% on struggling APAC travel retail, most notably due to a decline in the Chinese outbound travel market. In FY23, EPS (year-end: June 30) declined 52% y/y while sales in the same period fell 10% y/y. In FY2Q24, the company reported sales of $4.28B and non-GAAP EPS of $0.88, both of which were strong beats. We think the company’s announcement of a new restructuring plan, which entails a 3%-5% workforce reduction to generate a $350M-$500M incremental benefit, to be a main driver of the positive price action post-earnings release. We do, however, caution that the stock still faces significant fundamental headwinds while its valuation is certainly not cheap.

Strong beat in earnings

Reported sales of $4.28B imply a 7.4% y/y decline with organic sales growth down 8% y/y. This figure was better than what the company guided previously and ahead of market expectations by about 1%. Non-GAAP EPS of $0.88 was significantly better than expectations of about $0.56. This was mainly driven by higher than expected gross margin and lower operating expenses.

Looking at the segments, Skincare/Makeup/Fragrance/Haircare organic sales growth changed by -10%/-8%/flat/-6% y/y. By geography, Americas/EMEA/APAC organic sales growth moved by -1%/-14%/-7% y/y.

The company’s Asia travel retail business remains weak as retailer inventory levels have yet to completely reset while demand in China for overall prestige beauty has been lethargic, evidenced by lower global sales during the 11/11 shopping festival.

Even though Estee Lauder’s net sales improved by double digits in the Americas, overall sales in the region actually declined 1% y/y.

…but guidance is strangely cut again

EL downgraded FY24 guidance yet again. They now expect non-GAAP EPS of $2.08-$2.23 (vs. prior $2.17-$2.42), organic sales growth of +/- 1% y/y (vs. prior -1% to 2% y/y) and net sales +/- 1% y/y (vs. prior -1% to 2% y/y).

As for the next quarter, they anticipate organic sales growth to be 4%-6% y/y, net sales growth to be 3%-5% y/y and non-GAAP EPS to be $0.36-$0.46 which is below market consensus of $0.82.

We are quite perplexed as to why EL continues to guide lower than what the current trend may suggest. Granted, FX movements and disruptions in the Middle East may be difficult to predict and has thus weighed into these forecasts. However, the market will look at the actual reported figures and in FY2Q24, those handily beat expectations. Company guided numbers may not be so relevant in the end.

Rejoicing in the new restructuring plan

Investors are focusing on the restructuring plan which aims to reduce workforce by 3%-5% and deliver $350M-$500M in gross benefits to be reinvested into consumer facing areas. This is expected to help bring improvements to operating profit by $1.1B to $1.4B through the Profit Recovery Plan, up from $800M to $1.0B which was previously communicated. These benefits are anticipated to be realized no later than FY26E with more than half of the benefits to be realized in FY25E. To put this into perspective, this update implies an additional ~20% growth in net income annually during FY25E-FY26E.

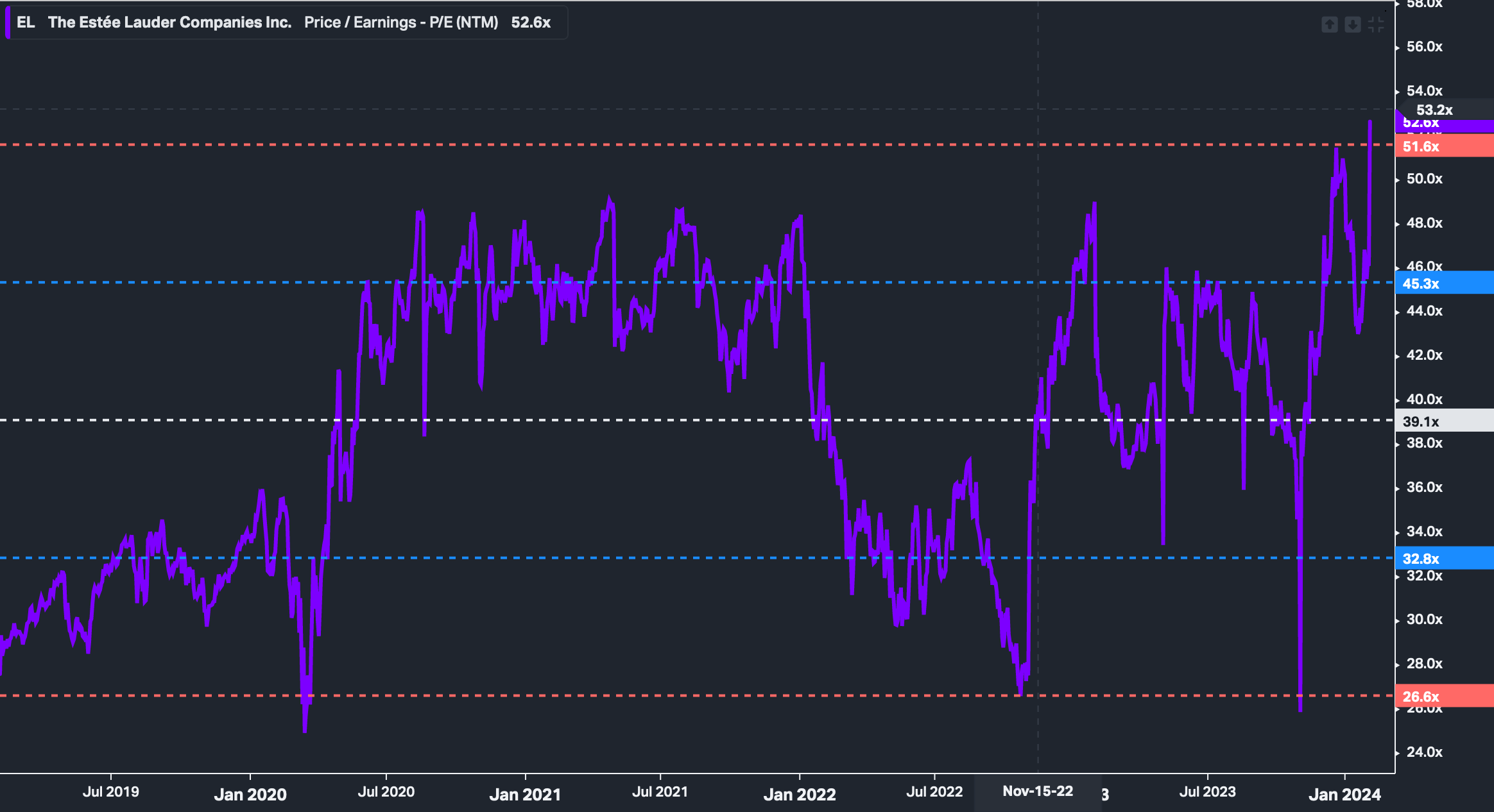

Valuation: Lots of optimism already priced in

EL is trading at nearly 52 times forward earnings which is significantly above its 5-year average of about 39x. The market estimates EL to earn $4.1 in adjusted EPS in FY25E which should be attainable given the ongoing restructuring plan and a potential rebound in the Asia travel business. However, lifting earnings by cost-cutting is considered low quality while net sales are still declining y/y in FY24E with a potential recovery in the mid to high single digits in FY25E. We expect softness in the Chinese consumer to continue to weigh on domestic and travel demand. We believe the risk to reward on holding EL may not be worth it given the recent surge and the headwinds it still faces despite being an under-performer in the past year.

Himalayas Research, Koyfin

Q2 2024 Earnings Call Transcript")