d3sign/Moment via Getty Images

The Company

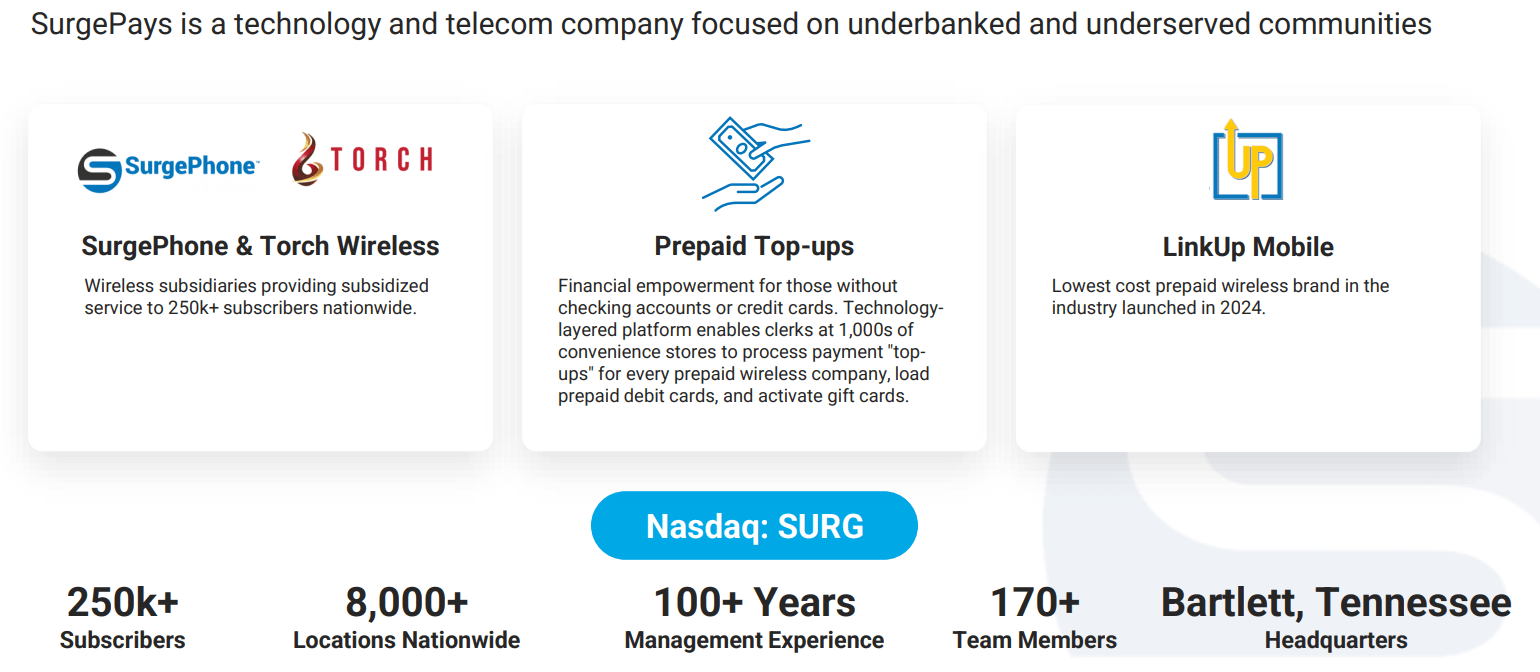

Headquartered in Bartlett, Tennessee, SurgePays, Inc. (NASDAQ:SURG) is a $107 million market cap tech and telecom company offering mobile broadband services. Utilizing a grassroots-level approach, the company specializes in delivering financial and telecom products to underbanked populations through convenience stores. SurgePays operates a technology platform that empowers clerks in thousands of convenience stores to offer prepaid wireless and financial products to lower-income and underbanked consumers. This aligns with the company’s goal of converting these stores into tech hubs for underserved communities.

SURG’s IR materials

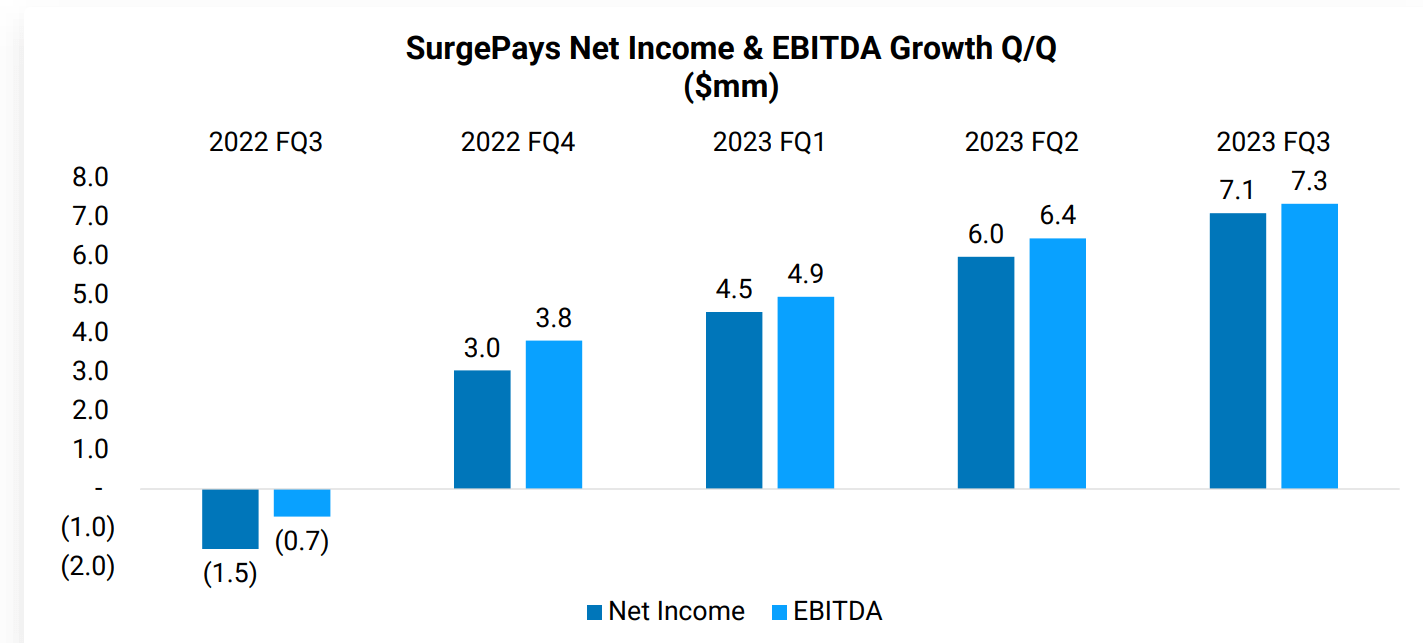

The strategic decisions made by SurgePays, including winding down the legacy mass tort lead gen company, LogicsIQ, and concentrating on its core business, contributed to the record-breaking net income. In Q3 FY2023, SurgePays reported impressive financial results, achieving its highest-ever net income of $7.1 million (compared to a $(1.5) million loss in Q3 2022) and EBITDA of $7.5 million (versus a $(0.8) million loss in Q3 2022).

SURG’s IR materials

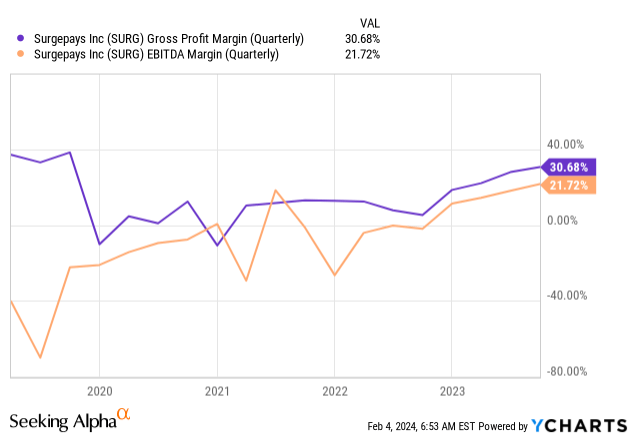

While Q3 2023 revenue slightly decreased to $34.2 million from $36.2 million in Q3 2022, the company achieved a substantial increase in gross profit, reaching $10.5 million, marking an $8.6 million improvement over Q3 2022. The gross profit margin also expanded to 30.7% in Q3 2023 – almost double what we saw at the end of 2022.

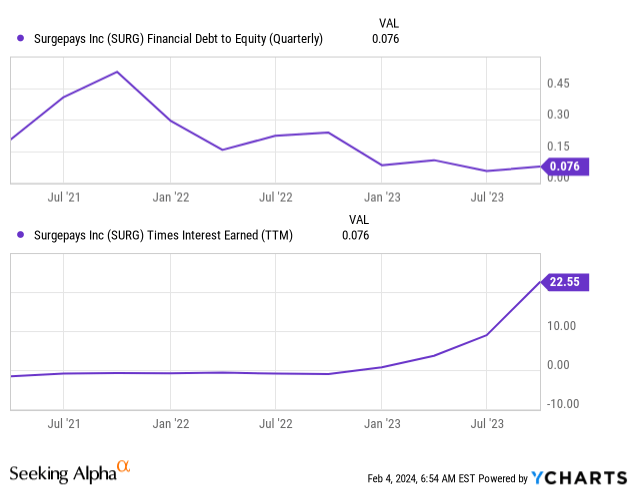

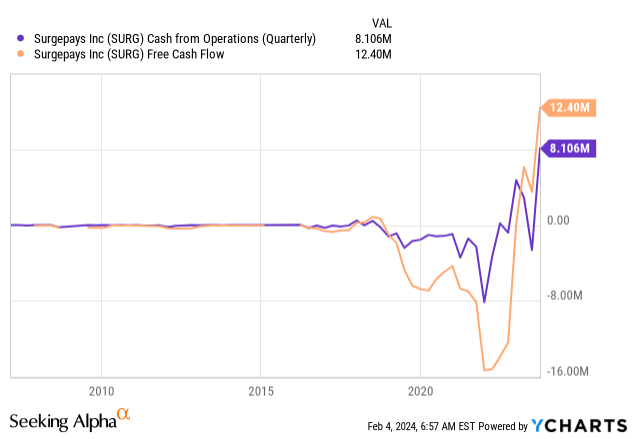

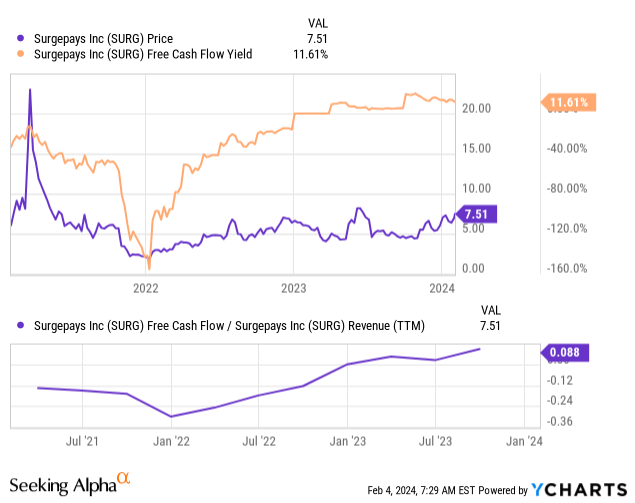

The company’s cash balance has improved to over $12 million, showcasing its sound financial footing with debt-to-equity heading to almost zero and operating profit covering intent payments by more than 22x, based on YCharts data:

SurgePays is now well-positioned to expand its footprint and further penetrate owner-operated convenience stores nationwide. According to the latest management call, SURG plans to transition its ACP sign-up approach to convenience stores, enhancing customer engagement through customer-facing point-of-sale equipment. This move is expected to drive additional revenue through store relationships and create an innovative market leadership position in providing wireless telecom and fintech products to the underbanked.

The company’s focus on managing cash flow and deploying capital for maximum growth reflects its commitment to sustainable profitability and strategic decision-making. Regarding free cash flow and operating cash flow generation, SurgePays is demonstrating significant progress. For instance, the TTM FCF totaling an impressive $12.4 million, represents ~10% of SURG’s market capitalization – this achievement stands out quite bullish amidst the backdrop of expanding profit margins and overall net profit growth mentioned above:

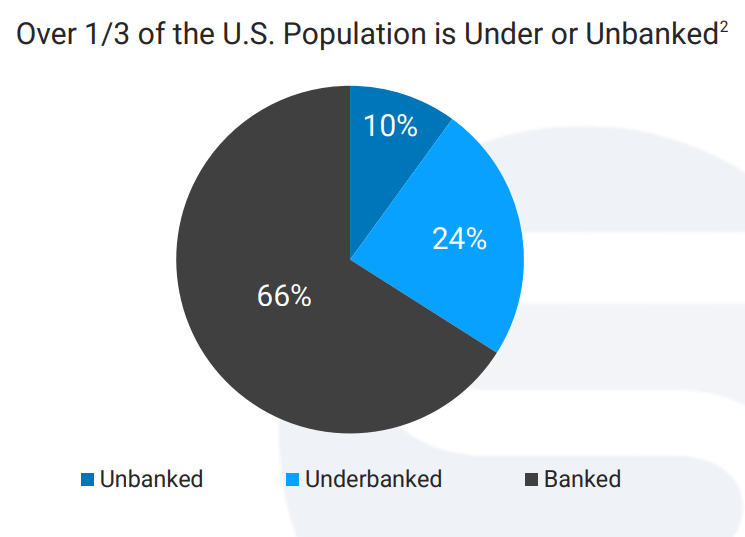

I think SURG has a significant market opportunity in serving the underbanked population, who primarily conduct financial transactions at their local convenience stores. The company leverages these trusted community stores as distribution points, integrating them into its fintech software platform. Through onboarding these stores, SurgePays enables clerks to conduct essential transactions such as prepaid wireless activations, payments, and reloading debit cards. This strategy aims to enhance the daily lives of individuals who lack access to traditional banking services, credit, and checking accounts. SurgePays’ revenue is directly correlated with the number of essential services it provides to this demographic, aligning with its mission to address the financial needs of those who need them the most. With over one-third of the U.S. population classified as underbanked or unbanked, SURG’s top-line growth prospects are clear to me as the firm keeps meeting the financial requirements of this underserved segment.

SURG’s IR materials

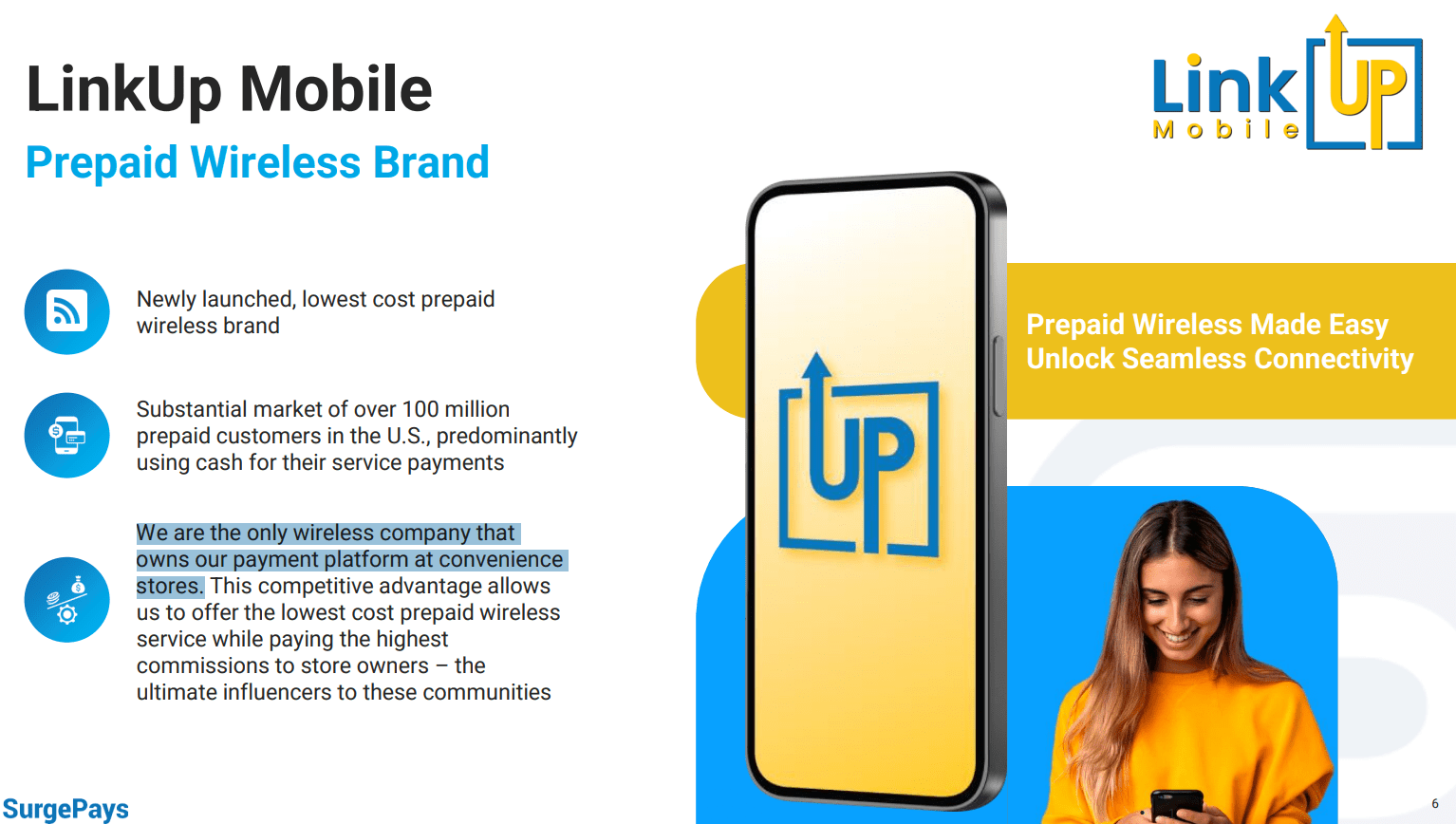

As was mentioned by Geoffrey Seiler in his brilliant article on SURG, the company’s primary opportunity in its end-market lies in its mobile broadband and prepaid businesses, particularly the Affordable Connectivity Program (ACP), where the government subsidizes affordable internet for lower-income households. So the launch of LinkUpMobile, a new prepaid brand, could act as a growth driver, capitalizing on the success of the ACP market. With plans to penetrate a vast market of over 150,000 convenience stores in the U.S., SURG aims not only to sell mobile broadband but also fintech products. The company is introducing LCD screens at registers to promote its offerings and facilitate transactions, eventually integrating loyalty rewards and QR code-driven payments.

SURG’s IR materials, author’s notes

Based on what I see today, I believe SurgePays’ recently published Q3 results and strategic initiatives indicate a positive trajectory for the company’s future growth in its niche telecom market.

But what about the valuation?

The Valuation

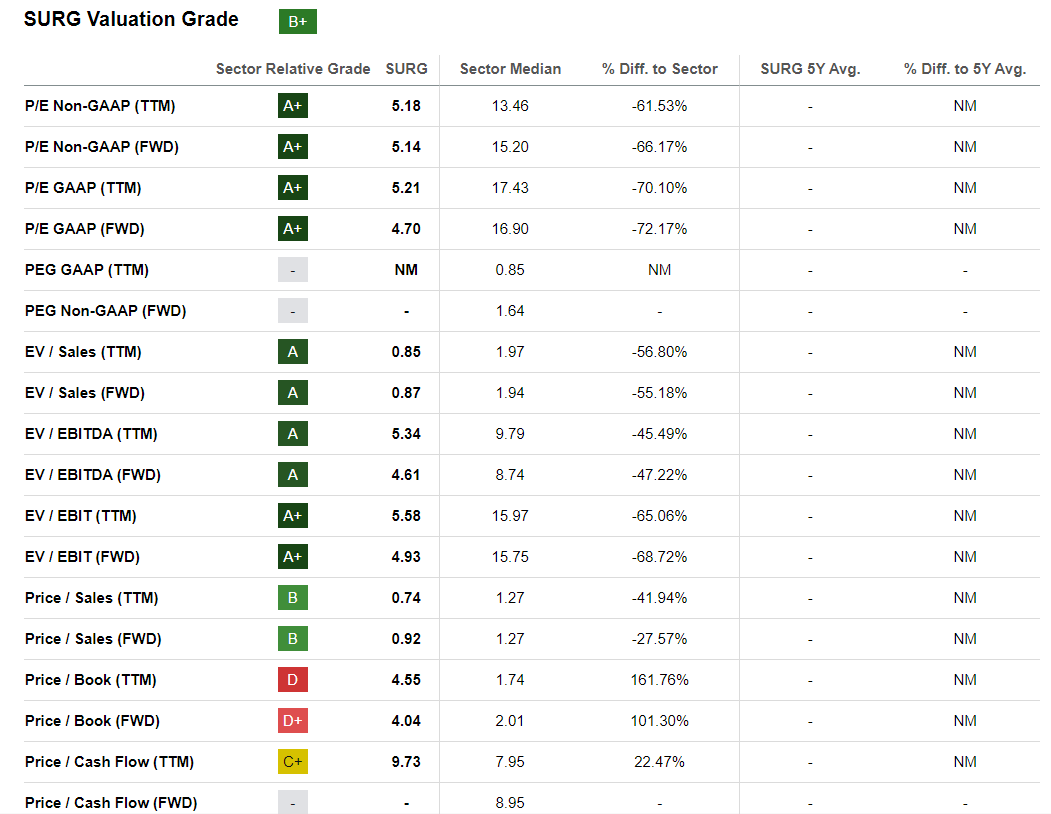

Based on Seeking Alpha’s Quant System, the SurgePays stock currently holds a valuation rating of B+, a notable thing for a rapidly growing enterprise experiencing active margin expansion in recent quarters. If we look in more detail, we’ll find that SURG is trading at just 4.7x of forward earnings and has a next-year EV/EBITDA ratio of 4.61x. Again: In my opinion, this is insanely low amid the expansion of both net profit and unadjusted EBITDA margins from the beginning of FY2023.

Seeking Alpha, SURG

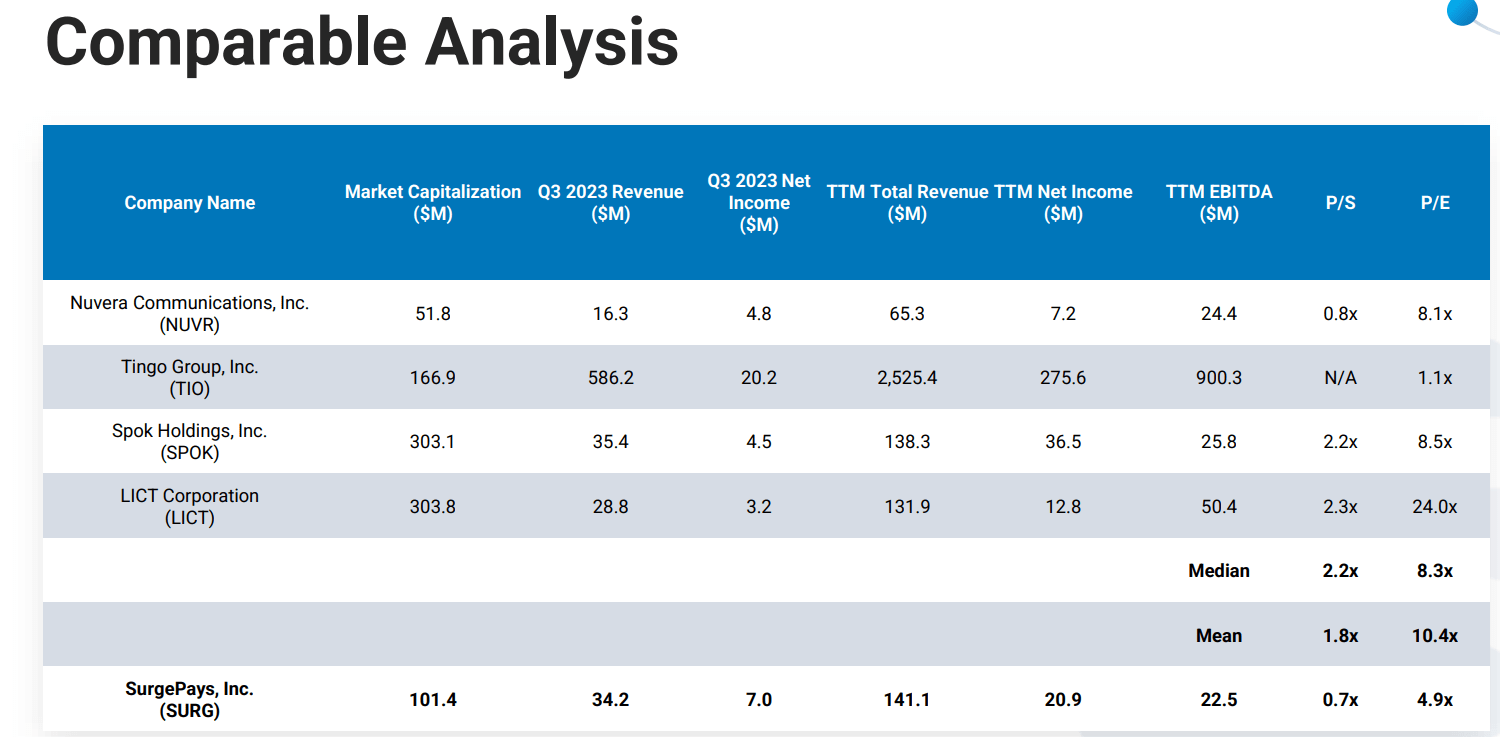

The company management presented a comparative table when discussing the last quarterly results. A careful review of this table shows that the company performs well and trades at one of the lowest multiples in its peer group. At the same time, its market capitalization is lower than some companies with relatively similar sales volumes. In my opinion, this may suggest that SurgePays has a lot of untapped growth potential relative to its peers:

SURG’s IR materials

Additionally, as mentioned earlier, it’s worth noting that the free cash flow as a percentage of market capitalization is quite impressive, ranging from 10% to 11% (depending on how you calculate it). Moreover, the marginality of FCF (as a % of TTM revenue) sits at a substantial 8.8%, which is quite solid for a small-cap business that’s growing as rapidly as SURG is.

Analysts anticipate SurgePays to achieve approximately $145.9 million in revenues for FY2024, as indicated by Seeking Alpha Premium data. Assuming a logical increase in the free cash flow margin to 10%, consistent with recent trends, SurgePays could generate $14.6 million in free cash flow in 2024. If we consider scenarios where the company’s free cash flow yield remains at 10% or decreases to 8%, influenced by the market recognizing SURG’s growth potential and heightened stock demand, the estimated fair value for the company ranges from $146 million to $183.4 million. This, in turn, suggests an upside potential ranging from 36% to 70% by the end of 2024, based on my calculations.

Risks To Consider Before Jumping In

Investing in SURG comes with its share of challenges that prudent investors should carefully consider. Firstly, the company heavily relies on government subsidies provided through the Affordable Connectivity Program. Any alterations or potential discontinuation of this program could introduce regulatory uncertainties, impacting SURG’s revenue streams and overall financial stability.

Furthermore, SURG caters to a market primarily composed of lower-income individuals, making it susceptible to economic fluctuations. During economic downturns, consumer spending on discretionary services such as prepaid wireless and fintech may decline, directly affecting SURG’s profitability. Additionally, in the competitive landscape of mobile internet services, especially through the ACP program, SURG faces challenges with numerous companies offering similar services for free. Effectively differentiating itself is crucial for maintaining and growing market share.

While the company’s expansion into convenience stores is a positive step, it also carries inherent risks. Despite making progress by entering over 8,000 stores, the potential market of more than 150,000 convenience stores in the U.S. underscores the need for successful and strategic expansion.

Investors should maintain a watchful eye on these factors, recognizing that SURG’s success is contingent not only on its operational prowess but also on navigating a dynamic and competitive market landscape.

The Verdict

Despite the myriad of inherent risks, a commonality for many small companies, SurgePays stands out in its niche with a very solid financial condition and market positioning. Given its current market size, I posit that SurgePays holds significant growth potential, especially considering its current financial trends and corporate development initiatives.

The company operates in an attractive end-market, and the launch of LinkUpMobile suggests a great growth opportunity that could likely strengthen SURG’s financials shortly. At least I hope so. My fair value calculations indicate a growth potential ranging from 36% to 70% by year-end, a substantial upside that underscores my confidence in SurgePays, leading me to assign it a ‘Buy’ rating today.

Thank you for reading!

Q2 2024 Earnings Call Transcript")