Back in November 2023, I reiterated a neutral view on Palantir Technologies Inc. (NYSE:PLTR) citing an unwarranted valuation premium and overstretched technical charts:

Palantir’s improving business fundamentals do not quite justify its significant valuation premium. While I believe in Palantir’s AI growth story, the long-term risk/reward for PLTR stock [based on pretty aggressive valuation model assumptions] is unattractive at current levels.

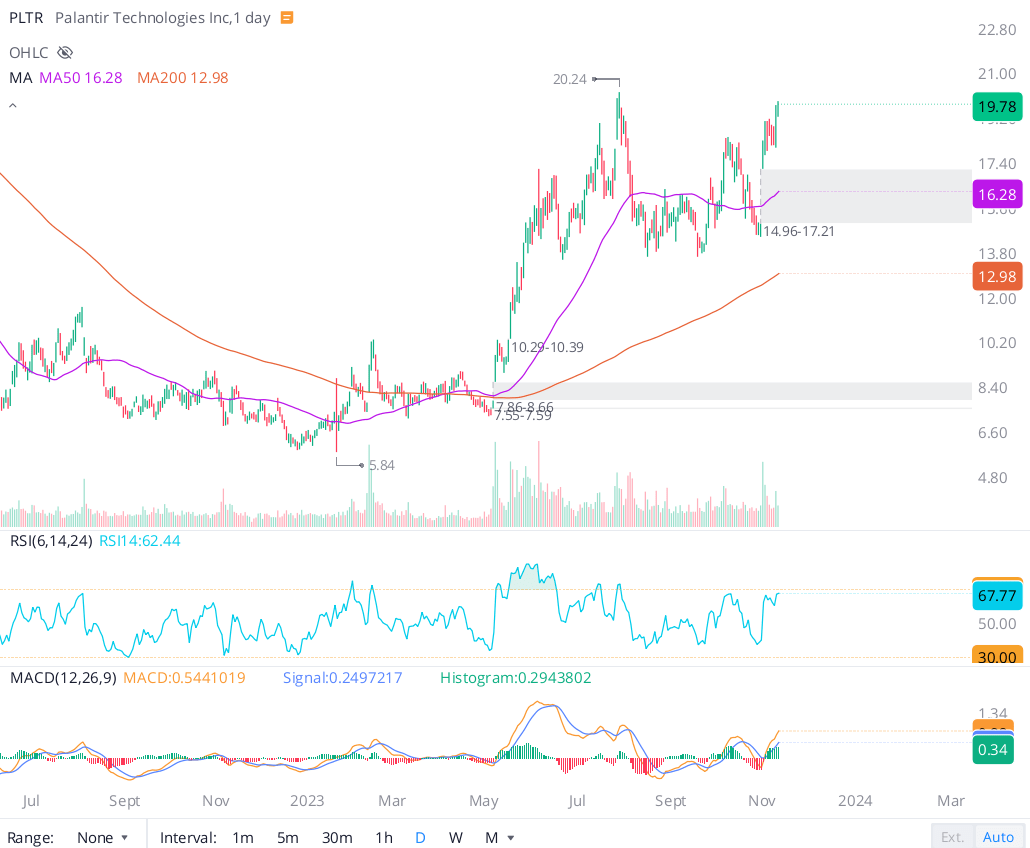

From a technical perspective, Palantir is showing strong momentum as evidenced by its “Momentum” quant factor grade of “A+”. That said, Palantir is getting close to “Overbought” territory (Daily RSI > 70), and a technical pullback is very much on the table. While not all technical gaps get filled, most of them do. And, as you can see below, Palantir’s chart has two big technical gaps at ~$15 and ~$7.5 that look ripe to be filled.

Palantir PLTR Stock Chart (WeBull Desktop)

At my investing group, we own a ~2.8% position in Palantir (cost-basis: $7.34 per share) within our moonshot growth portfolio. For now, we are not buyers in Palantir; however, if the stock pulls back down to 200-DMA levels at ~$12-13 per share, we will resume accumulation, i.e., slow, staggered buying.

Key Takeaway: Due to unfavorable long-term risk/reward, I rate PLTR stock a “Hold/Neutral/Avoid” at $19.67 per share.

Source: “Palantir Stock: The Retail Army Is Winning, But Is It Too Late To Join The Party?”

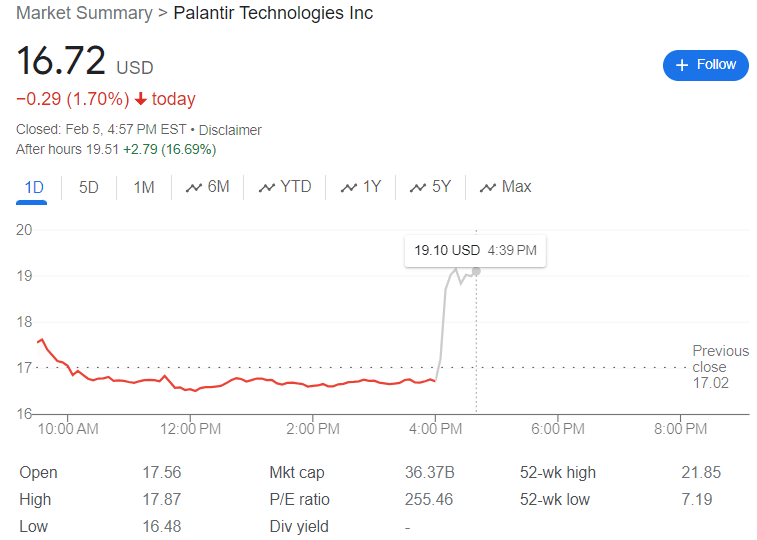

Going into today’s Q4 earnings report, Palantir stock was down ~16% from the publication of my previous update. However, in light of the release of Palantir’s Q4 report, PLTR stock has quickly popped up by ~17% to ~$19.5 per share.

GoogleFinance

In today’s note, we will briefly review Palantir’s Q4 2023 report and then reevaluate PLTR’s fair value & expected returns to see if Palantir is an attractive investment right now. Let’s crunch some numbers!

Brief Review Of Palantir’s Q4 2023 Report

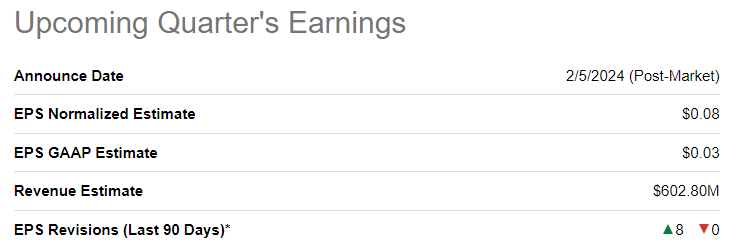

Heading into its Q4 2023 report, Palantir was projected to deliver revenues and EPS of $602.8M and $0.08, respectively.

SeekingAlpha

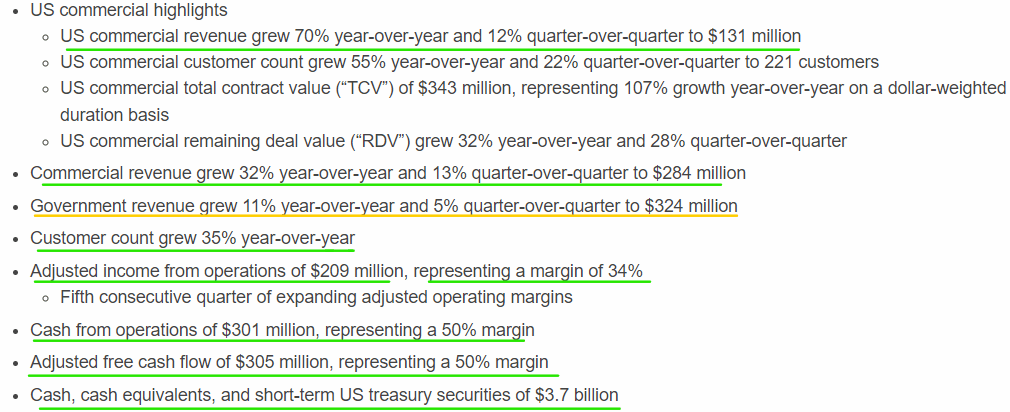

As you may have guessed from the pop in PLTR stock, Palantir’s Q4 numbers beat consensus expectations, with revenues coming in at $608M (+20% y/y, +9% q/q) driven by robust growth in commercial revenues (+32% y/y [US commercial revenues +70% y/y]),

Palantir Q4 2023 Earnings Release

While its adj. EPS of $0.08 was in line with estimates, Palantir generated $305M in adj. free cash flow at a margin of 50% – increasing its cash balance from $3.3B in Q3 2023 to $3.7B in Q4 2023.

According to Palantir’s CEO, Alex Karp, Palantir AIP [artificial intelligence platform] was the primary driver of the stronger-than-expected showing in their commercial business (emphasis added):

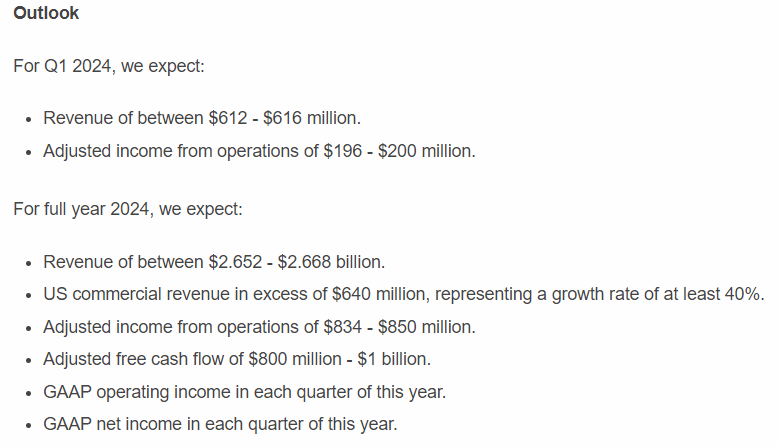

Our U.S. commercial business continues to be a significant driver of our growth, a trend that we expect to continue. In the U.S. commercial market, our revenue increased 70% year-over-year to $131 million in Q4 2023 from $77 million the year before, bringing our total U.S. commercial revenue for 2023 to $457 million. We now anticipate that our U.S. commercial revenue will exceed $640 million in 2024, which would represent a growth rate of at least 40% from last year. The demand for large language models from commercial institutions in the United States continues to be unrelenting. Every part of our organization is focused on the rollout of our Artificial Intelligence Platform (AIP), which has gone from a prototype to a product in months. And our momentumwith AIP is now significantly contributing to new revenue and new customers.

As I said in my previous note, Palantir has real AI substance, and AIP’s rapid scale-up is ample proof. For 2024, Palantir’s management is guiding for total revenues of $2.652-2.668B (+20% y/y growth at the midpoint of guidance range), with U.S. commercial revenues expected to exceed $640M (growth of more than 40%).

Palantir Q4 2023 Earnings Release

While this guidance could be sandbagged (considering Palantir’s guidance history) and 20%+ y/y growth is nothing to scoff at, Palantir investors may just be getting overly excited once again with this after-hours pop. Let’s re-run Palantir through our Valuation Model to see if this is the case!

Palantir’s Fair Value And Expected Returns

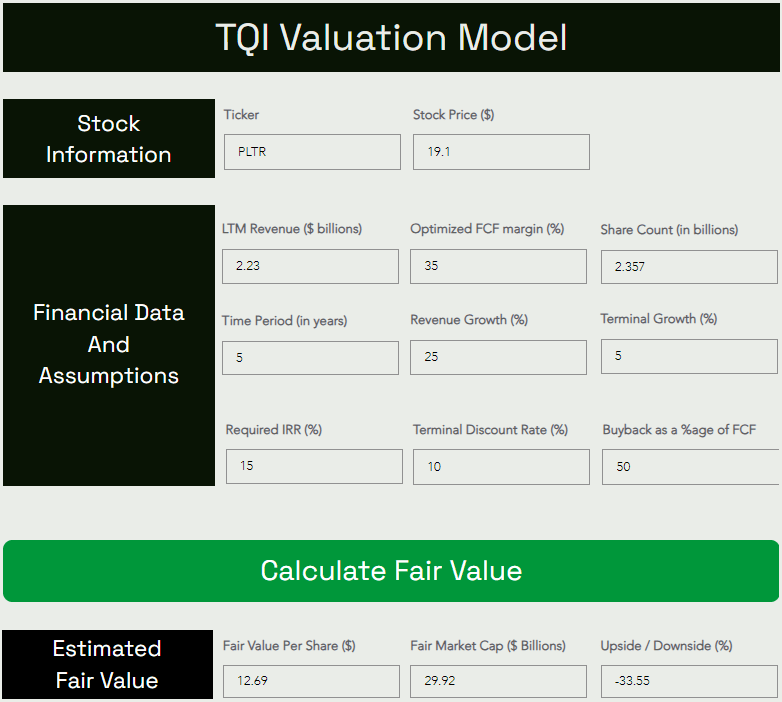

For today’s valuation exercise, I am maintaining my long-term sales growth and optimized free cash flow, or FCF, margin assumptions at 25% and 35%, respectively. These assumptions were explained in our previous update, linked above.

All other assumptions are straightforward and self-explanatory, but if you have any questions, please share them in the comments section below.

Here’s my updated valuation for PLTR stock:

TQI Valuation Model (TQIG.org)

From an absolute valuation standpoint, Palantir remains significantly overvalued, with PLTR stock having a potential downside of -33% to fair value [$12.7 per share]. Now, I wouldn’t dismiss the idea of investing in Palantir solely due to its premium valuation, as history shows that winning stocks can be overvalued for long periods [e.g., Amazon.com, Inc. (AMZN), Tesla, Inc. (TSLA), NVIDIA Corporation (NVDA), etc.].

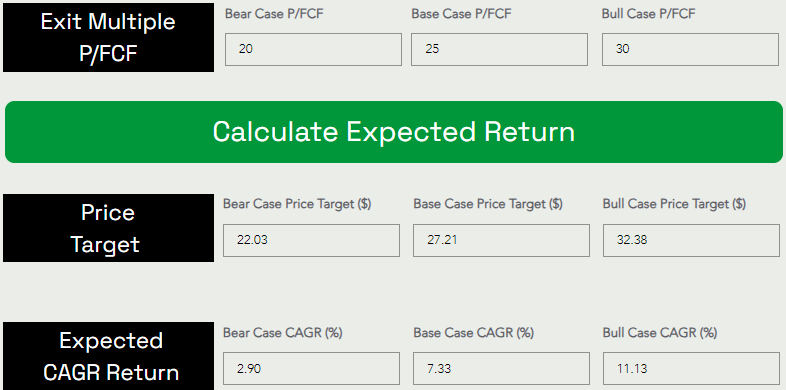

Let’s take a look at Palantir’s long-term risk/reward to make an informed decision:

Assuming an aggressive exit multiple of 25x P/FCF, Palantir stock could rise from $19.1 to $27.2 at a CAGR rate of 7.33% by 2028-29.

TQI Valuation Model (TQIG.org)

While Palantir’s expected 5-yr CAGR return has improved slightly since mid-November, PLTR fails to beat our minimum investment hurdle rate of 15%. Henceforth, I am still not a buyer at current levels.

Concluding Thoughts

As of Q4, Palantir has a cash balance of $3.7B and no debt, which is a solid financial foundation to support its AI ambitions. Overall, business momentum is building at Palantir, with the company delivering a solid mix of revenue growth and profitability. That said, Palantir’s better-than-expected outlook for 20% y/y growth in 2024 is not exceptional, and as of now, Palantir is not showing AI-powered hypergrowth!

As a long-term investor, I am pleased with Palantir Technologies Inc.’s improving business fundamentals; however, in the absence of AI-driven hypergrowth, I think PLTR’s significant valuation premium remains unjustified. To clarify, I am long on Palantir, and I’m a firm believer in Palantir’s AI growth story, but the long-term risk/reward for PLTR stock [based on pretty aggressive valuation model assumptions] is unattractive at current levels.

Hence, I wouldn’t be surprised if this after-hours pop in Palantir were to be faded by the market in the near term. Palantir is a battleground stock – adored by millions of retail investors and frowned upon by certain institutional money managers. Today, the retail army is winning, but the near term upside looks capped due to valuation.

At my investing group, we own a ~2.4% position in Palantir [cost-basis: $7.34 per share] within our moonshot growth portfolio. In light of Palantir’s Q4 report, we will continue to refrain from further accumulation. To resume buying, I would want to see a price or time correction that boosts PLTR’s 5-year expected CAGR to 15%+.

Key Takeaway: Due to unfavorable long-term risk/reward, I continue to rate Palantir Technologies Inc. stock a “Hold/Neutral/Avoid” at $19.5 per share.

Thanks for reading, and happy investing. Please share your thoughts, concerns, and/or questions in the comments section below.

Q2 2024 Earnings Call Transcript")