skynesher/E+ via Getty Images

I’ve always been asked, ‘What is my favorite car?’ and I’ve always said ‘The next one.’” ~ Carroll Shelby.

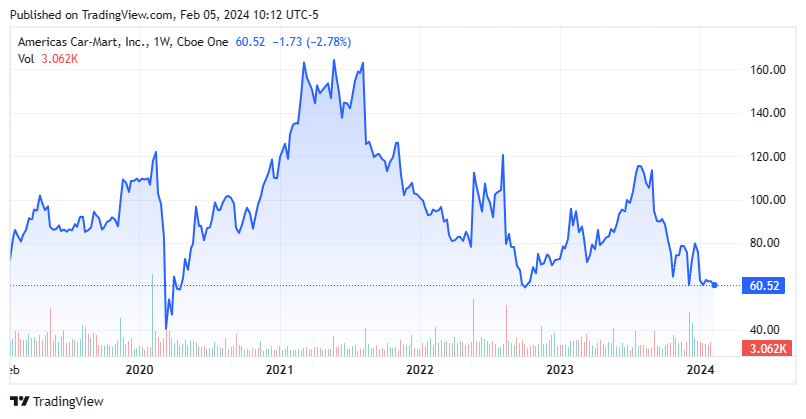

Today, we put America’s Car-Mart, Inc. (NASDAQ:CRMT) in the spotlight. The stock currently trades for around 40% of its levels achieved in the height of the Covid pandemic. The company has been hit recently by worsening credit conditions due to their largely sub-prime customer base. The stock has been cut in half since its recent highs late in 2023. Are the shares in the “buy zone” yet? An analysis follows below.

Seeking Alpha

Company Overview:

This automotive retailer is headquartered in Rogers, AR. The company primarily sells older model used vehicles. It also provides financing for its customers. America’s Car-Mart largest publicly held automotive retailers in the United States. It operates just over 150 stores nationwide. America’s Car-Mart core customer is made up largely of individual that are challenged getting financing from traditional lenders due to their poor credit histories. Currently, the stock trades for around sixty dollars a share and sports an approximate market capitalization of $400 million. The company’s fiscal year begins on April 1st.

Second Quarter Results:

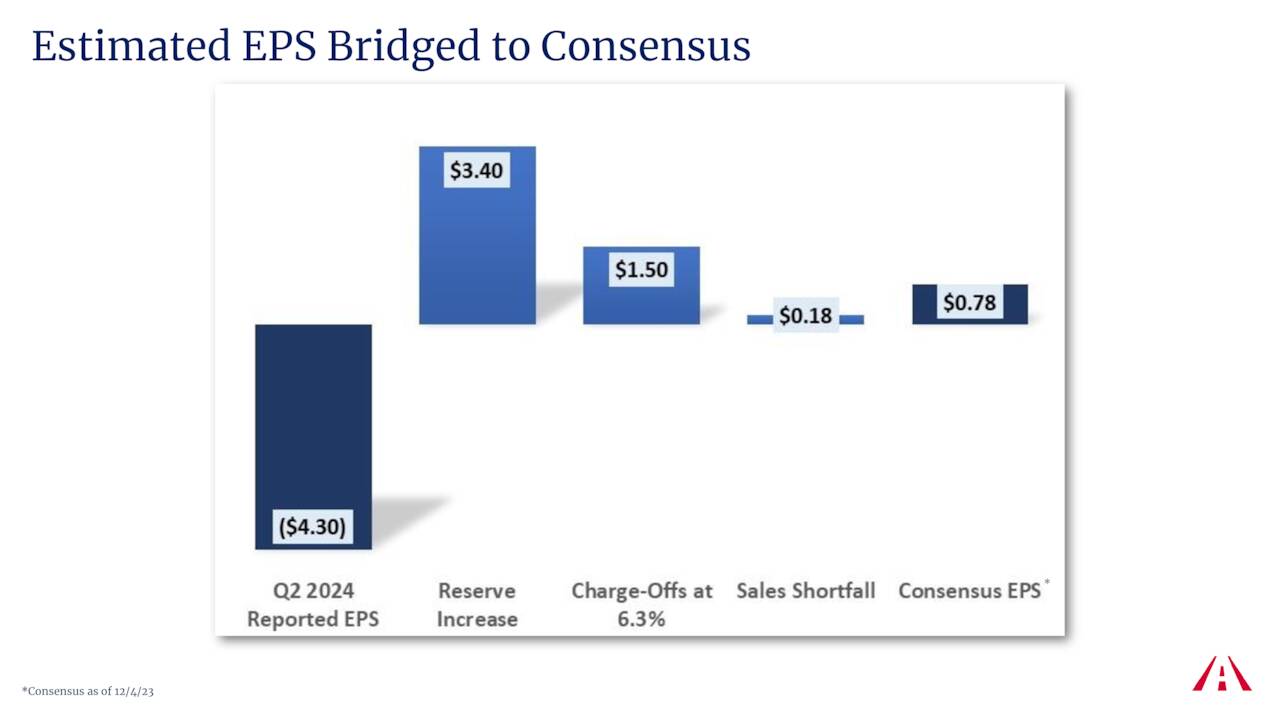

America’s Car-Mart posted its Q2 2024 numbers on December 5th. The company posted a loss of $4.30 a share, compared to expectations for a 77 cent a share profit. Results were crushed by a deterioration of consumer credit. Net charge-offs as a % of the company’s average finance receivables rose 7.2% versus 5.8% in 2Q2023. Management also took its allowance for credit loss all the way up to 26.04%, up from 23.91% previously. This resulted in $3.40 of the quarterly loss America’s Car-Mart delivered for the quarter. Charge-offs rose to 6.3% in the quarter and accounted for a $1.50 a share loss.

December Company Presentation

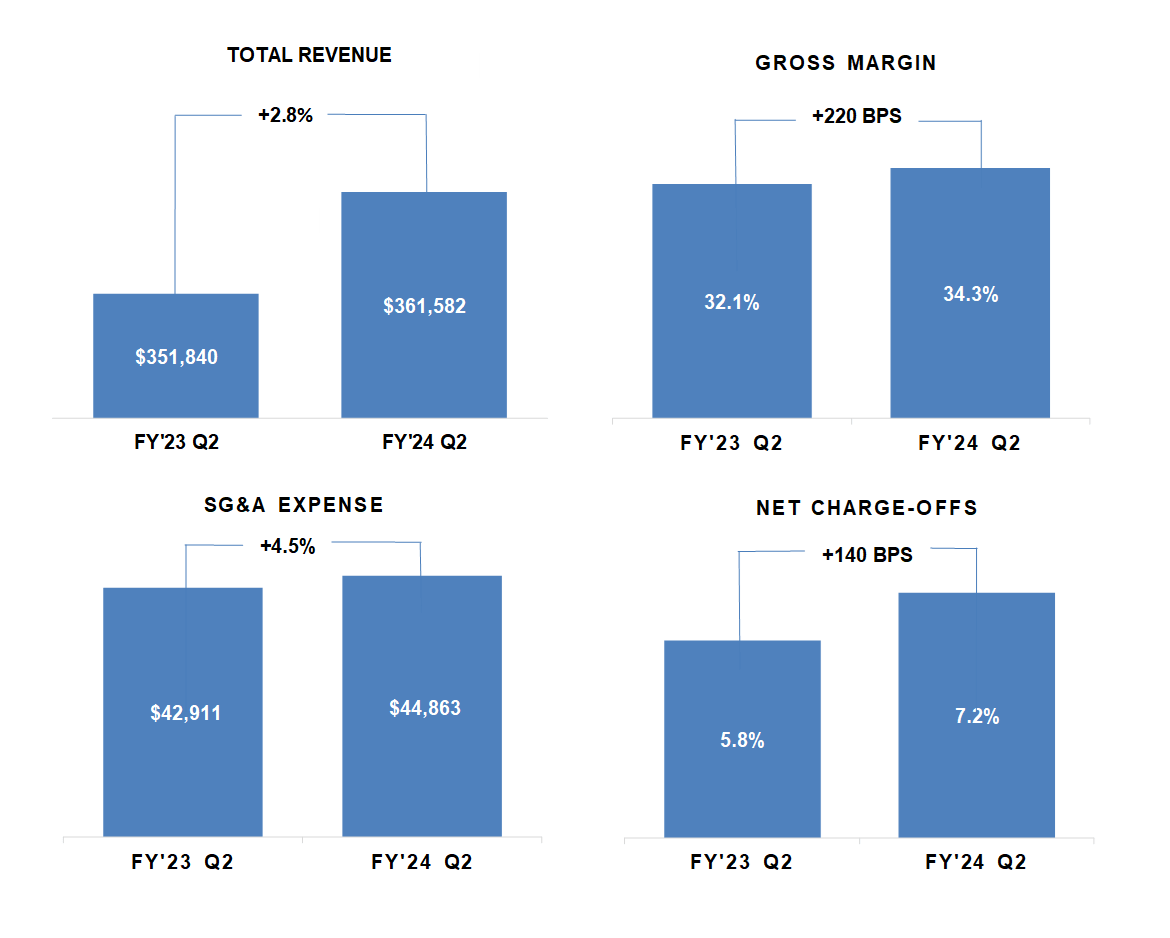

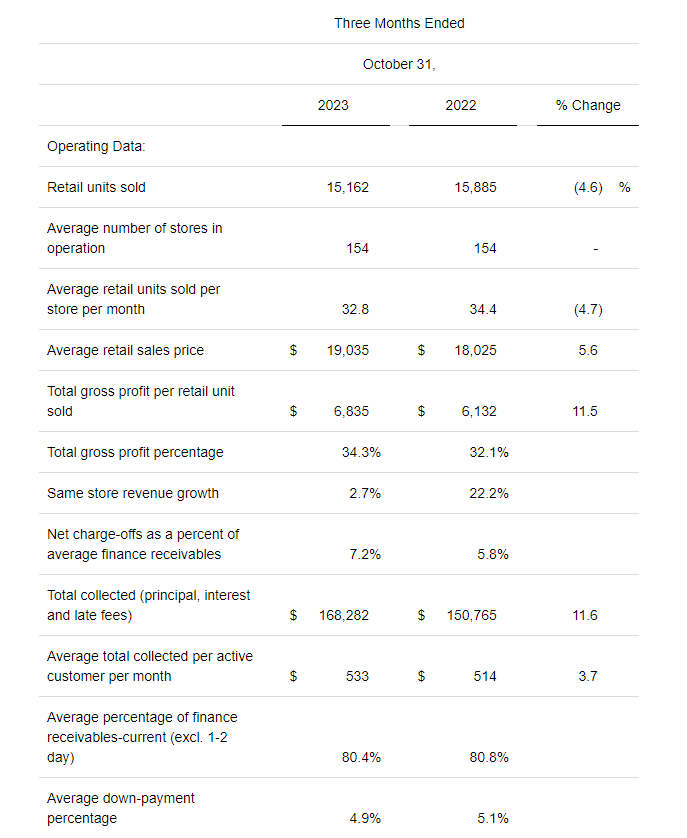

Revenues rose nearly three percent on a year-over-year basis to $361.6 million, some $14 million below the consensus. Unit sales were down by 4.6% while gross margins improved to 34.3% from 32.1% in the same period a year ago. The rise in revenue was primarily due to increased interest income (a 23% rise) and a 5.6% increase to average sales price of a vehicle.

Fourth Quarter Press Release

The company has reduced its workforce by approximately 10% since quarter end to pare costs and improve margins.

Seeking Alpha

Analyst Commentary & Balance Sheet:

Since quarterly results were posted in early December, Bank of America has reissued its Sell rating on the stock with a $55 price target. Stephens also downgraded the shares to Equal Weight from Overweight.

Approximately 20% of the stock’s outstanding float is currently held short. A beneficial owner disposed of just over $3 million of their stake in the firm in early August of last year. That was the last insider activity in this equity.

According to the 10-Q filed for the quarter, America’s Car-Mart had nearly $95 million in cash and marketable securities on its balance sheet, which includes restricted cash. It also had nearly $580 million of net non-recourse notes payable, as well $165 million outstanding on a revolving credit facility. Interest expense jumped to just over $16.5 million in the quarter from just under $8.4 million in 2Q2023.

December Company Presentation

Verdict:

The company made $3.11 a share on $1.41 billion in revenues in FY2023. The current analyst consensus has America’s Car-Mart, Inc. losing just over three bucks a share in FY2024 on sales of $1.46 billion. They do project a big rebound in earnings to just over five bucks a share in FY2025 on sales growth of four percent.

The stock currently trades a bit under 12 times FY2025E EPS. However, I would take 2025’s projected rebound in earnings with a large grain of salt. Management believes the current headwinds regarding credit loss are “shorter-term in nature.” I am a skeptic on that view. Recent surveys that show just over 60% of Americans are living paycheck to paycheck and only 24% believe the country is heading in the right direction. Delinquency and default rates on credit card balances and consumer loans continue to rise, and auto-loan defaults are at their highest levels in the 21st century.

Therefore, I am aligned with the two analyst firms that have provided ratings since a large quarterly loss was announced in December, and agree that America’s Car-Mart, Inc. stock is one to avoid at this moment.

Straight roads are for fast cars, turns are for fast drivers.” ~ Colin McRae.

Q2 2024 Earnings Call Transcript")