LIONEL BONAVENTURE/AFP via Getty Images

Shares of Meta Platforms, Inc. (NASDAQ:META) soared 20% on Friday after the digital advertising behemoth submitted a very impressive earnings card for the fourth fiscal quarter. A major takeaway from the earnings card was the Meta is set to become a dividend stock, which creates a pathway for the company to return more of its free cash flow to shareholders in the future. Meta’s revenue surge paints a rosy picture of the state of the digital advertising industry as well, and Alphabet Inc. (GOOG) also reported impressive revenue growth in Google Search and YouTube ads. I believe Meta will use a lot of its free cash flow to turn Meta into a dividend growth stock and rival Apple’s (AAPL) dividend growth!

Previous rating

Since my last coverage of Meta at the end of October 2023 — which resulted in a hold rating — shares of the social media company have soared 60%. I liked Meta’s upside potential related to a recovery in the digital ad business, which accelerated in the last quarter.

While Meta stock clearly is not a bargain, there are reasons to remain invested here. These include strong guidance for Q1 ’24, continual top line momentum in advertising, and, in my opinion, strong prospects for dividend growth.

Meta beats top and bottom-line estimates

Meta easily surpassed consensus estimates with regard to its revenues and earnings due to a roaring comeback of advertising spending on the part of marketers in the fourth quarter, partially aided by the holiday season. Meta reported revenues of $40.1B, which exceeded the consensus prediction by almost $1.0B. Earnings, adjusted for one-off effects, were $5.33 per-share, surpassing the consensus estimate by $0.36 per-share.

Seeking Alpha

Strong long-term earnings outlook for Meta given digital advertising trends

If there was one takeaway from Meta’s impressive Q4 ’23 earnings sheet, it was that the advertising business has made a major comeback, and this comeback has been even stronger than I thought it would be only three months ago. In Q3 ’23, Meta’s revenues soared 23% year-over-year, and they saw 25% top line growth in Q4 ’23, showing a 2 PP revenue acceleration. It was the fastest growth for Meta since FY 2021. Meta’s business performance is driven chiefly by a massive return of advertising dollars to digital marketing platforms, like those operated by Meta or Google, and the company’s first-quarter outlook indicates that this recovery has staying power.

Meta

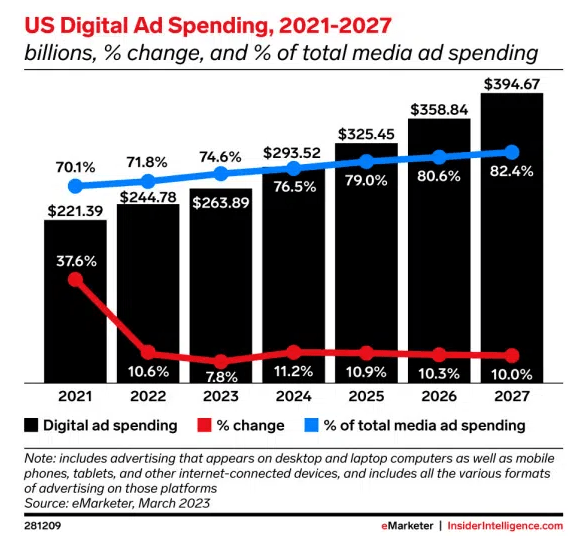

The longer-term outlook for Meta is also extremely positive, in large part because more advertising dollars are expected to shift to the kind of digital marketing channels that Meta runs. The digital ad spending outlook for the U.S. market, submitted by research firm eMarketer, implies an annual growth rate in U.S. digital ad spending of 11% annually. The market size is expected to expand to $394.7B in the next four years, and as one of the largest two digital marketing platforms, Meta is primed to capture a lot of this growth. Additionally, the share of ad budgets going to digital marketing firms is set to increase, from 74.6% in FY 2023 to 82.4% in FY 2027. This shift in ad budgets, in favor of digital marketing channels, should benefit Meta.

eMarketer

According to Meta’s first quarter revenue outlook, the social media platform projects to capture somewhere between $34.5B and $37.0B in revenues. This implies a year-over-year growth rate of 25% at the mid-point. The outlook implies that Meta’s advertising revenue momentum is not expected to be limited to the typically strong Q4. The fourth quarter is usually a very good quarter for digital marketing platforms due to the inclusion of the holidays, resulting in seasonal boost to ad campaign spending.

Daily active user growth supports platform value

One of the major key performance metrics that I pay attention to and monitor is Meta’s daily active user trend, which ultimately reflects the attractiveness of Facebook as a digital advertising platform for marketers. Facebook has been able to consistently expand its user base in the last few years and added 25M of new users to its social media platform just in the fourth quarter. In total, Meta added 110M users to its platform in FY 2023, which compares to a net acquisition figure of 71M in FY 2022.

Meta

Use of free cash flow and changing investment narrative

How profound the recovery in Meta’s core advertising segment has been can be seen in the massive rebound in the company’s free cash flow as well as free cash flow margin expansion. Meta generated $11.5B in free cash flow in the fourth quarter on revenues of $40.1B, which calculates to an impressive free cash flow margin of 28.7%. The advertising rebound has been quite profitable for Meta not only in terms of growing earnings, but the company now also retains a higher share of its free cash flow than last year. Of every dollar generated in revenue in Q4’23, the company retained 28.7 cents in free cash flow. Last year, Meta retained only 16.4 cents for every dollar in sales, showing a FCF margin expansion of 12 PP Y/Y.

|

in mil $ |

Q4’22 |

Q1’23 |

Q2’23 |

Q3’23 |

Q4’23 |

Y/Y Growth |

|

Revenues |

$32,165 |

$28,645 |

$31,999 |

$34,146 |

$40,111 |

24.7% |

|

Operating Cash Flow |

$14,511 |

$13,998 |

$17,309 |

$20,402 |

$19,404 |

33.7% |

|

Purchases of Property/Equipment |

($8,988) |

($6,823) |

($6,134) |

($6,496) |

($7,592) |

-15.5% |

|

Payments on Finance Leases |

($235) |

($264) |

($220) |

($267) |

($307) |

30.6% |

|

Free Cash Flow |

$5,288 |

$6,911 |

$10,955 |

$13,639 |

$11,505 |

117.6% |

|

Free Cash Flow Margin |

16.4% |

24.1% |

34.2% |

39.9% |

28.7% |

74.5% |

(Source: Author.)

Meta is set follow Apple’s dual-pillar capital return strategy

Meta made waves on Thursday after the social media company announced that it will start paying a dividend and upsize its stock buyback authorization by $50B. The first scheduled dividend payment will take place on March 26, 2024, and will amount to $0.50 per-share. At a current share price of $475, Meta is set to yield less than 1%, but the company obviously generates enormous free cash flow from its social media business which indicates that Meta has great potential for dividend growth. And I believe this is a narrative-changing shift for FAANG investors: Meta could funnel a lot of its free cash flow to shareholders via dividends as opposed to stock buybacks in the future now that it creates a more permanent and direct pathway for free cash flow returns.

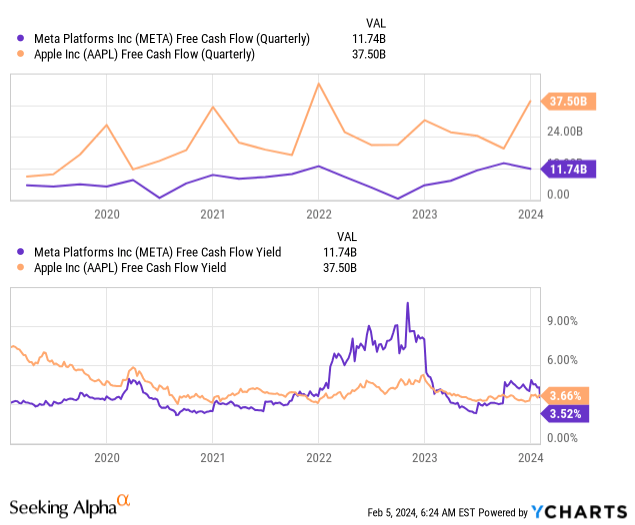

The $0.50 per-share in dividends quarterly will cost Meta about $1.3B per quarter, which is easily covered by free cash flow. Meta earned an average of $10.8B in free cash flow each quarter in FY 2023, so the FCF-based payout ratio here is ~12%. Apple’s free cash flow payout ratio is ~15%, based off of FQ1 ’24 results (Source).

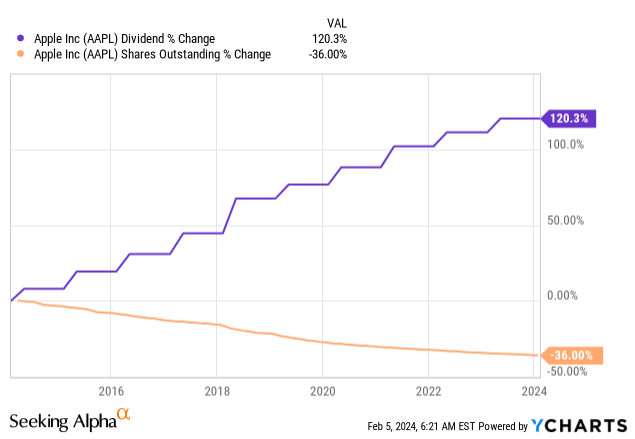

Instead of doing stock buybacks, which have become increasingly expensive (and unattractive) given Meta’s soaring share price, I believe Meta will seek to use its free cash flow to deliver Apple-style dividend growth to shareholders in the future. Apple is the only other FAANG stock that pays shareholders a dividend, and early investors in the company will appreciate it. Apple’ shares also yield less than 1%, but the cash flow for investors has considerably improved in the last ten years: Apple’s dividend is up 120% in the last decade while the company has reduced its outstanding shares by 36%.

Since Apple and Meta are both extremely free cash flow-profitable and have a comparable free cash flow yield, I expect the social media company to follow into the footsteps of Apple and turn META not only into a dividend stock, but specifically a dividend growth stock.

Meta’s valuation

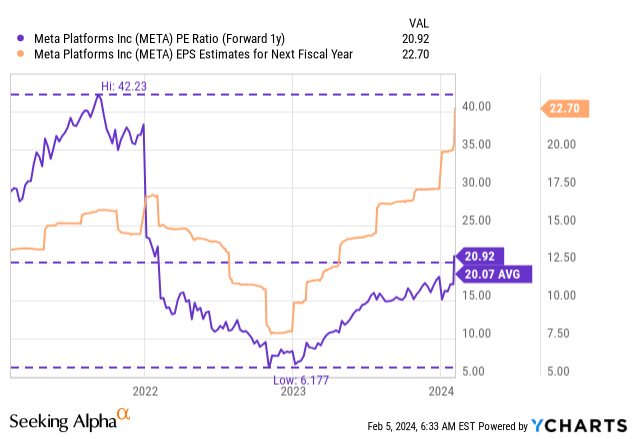

Meta was a bargain during the advertising market correction, but it no longer is. Investors are paying 21X FY 2025 earnings for the company which, in my opinion, makes Meta slightly overvalued. I’d pay a 20X P/E ratio for Meta giving its massive upsurge in earnings, EPS upside revisions and strong free cash flow margins, but I would be uncomfortable jumping on the bandwagon here considering that shares of the social media company soared on Friday.

Meta is consistently profitable, making the use of a P/E ratio sensible, in my opinion. In the last three years, which includes the downturn period in the ad market, Meta traded at an average P/E ratio of 20.1X. With a 20X P/E ratio, shares of Meta have a fair value of $454, so I consider the social media company slightly overvalued (current price is $475). I certainly wouldn’t want to run after the share price here, and given the 20% price jump on Friday, I believe investors may be able to buy Meta at a cheaper price in the near term.

Meta is trading at a higher P/E ratio now than in the immediate past, due to the rebound in advertising and stronger than expected revenue outlook. This valuation increase has resulted in a D- valuation rating from Seeking Alpha. This rating also reflects that Meta’s share price has revalued to the longer-term average, as I just discussed.

Seeking Alpha

Risks with Meta

Meta has set a high bar with its Q4 ’23 earnings release, and while I expect EPS estimate to reset higher, it is unlikely that the online ad business will continue to grow at 25% annualized rates going forward. The biggest risk for Meta, as I see, is a decline in free cash flow margins related to slowing growth in the company’s advertising operations. The biggest commercial risk is a slowdown in the digital advertising industry given the recent upsurge in spending and revenue acceleration. The U.S. economy is growing rapidly right now, but moderating economic growth could negatively affect advertisers’ willingness to grow their ad spend on digital marketing channels.

Final thoughts

Meta Platforms, Inc. submitted a very impressive earnings sheet for the fourth-quarter. The three main take-aways were: 1. The advertising business is in the best shape in years and sees accelerating top line growth, 2. Meta remained extremely free cash flow-profitable and saw a more than 12 PP improvement in its free cash flow margin in Q4’23, and 3. Meta is now not only a dividend stock, but it may be on the brink of becoming a dividend growth stock that could deliver Apple-like dividend growth. Since Meta Platforms, Inc.’s fundamentals are strong, but the valuation is not as appealing as it was last year, a hold rating for META stock remains justified.

Q2 2024 Earnings Call Transcript")