yuriz

My first article for Seeking Alpha, back in 2018, was about MGIC (NYSE:MTG), when the stock was $12.55. Back then, with the ’07-’11 housing bust still a painful memory, I argued that another housing meltdown was highly unlikely. That fear of course worsened when COVID hit; my May15, 2020 article on MGIC argued that even in a dire economic scenario the company’s liquidation value was higher than its then $6.70 price. In the recent past I’ve been able to shift my discussions to MGIC’s stability and ability to return the great bulk of its earnings to shareholders. This past Q4 provided more evidence for that view.

The first quarter

MGIC reported Q4 earnings last Wednesday night. Highlights were:

- Cash EPS was $0.63. Reported EPS was $0.66, but I added back $13 million for one-time reinsurance cancellation costs and subtracted off a $23 million decline in MGIC’s non-cash loss reserve. That compares to $0.52 per share of cash earnings a year ago.

- Claim payments on MGIC’s $294 billion of private mortgage insurance in force remain at rock bottom – $13 million in Q4, or 1.8 bp. That compares to 13 bp during Q4 2019.

- Insurance in force declined from a year ago by 1%.

- Operating expenses fell by $19 million from a year ago, to $55 million. Q4 ’22 appeared to have had some unusual pension expenses.

- MGIC paid a $0.115 quarterly dividend, up 12.5% from the prior year. It also bought back 7.0 million shares. The combined cash return to shareholders was $154 million, or $0.55 per share. So MGIC passed on 87% of its cash earnings to shareholders.

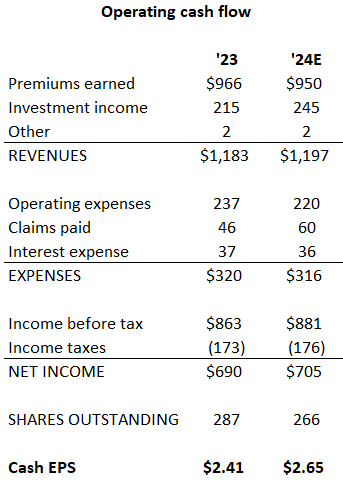

My ’24 cash operating EPS forecast

Here it is:

MGIC financial reports and my forecast

Sources: MGIC financial reports, my forecast

My key assumptions are:

- MGIC’s insurance in force (IIF) and premiums earned on the IIF are roughly flat. Slow home sales means slow growth in home mortgage debt.

- The investment portfolio yield continues to gradually rise.

- Operating expenses come in the middle of MGIC’s guidance in its Q4 earnings call.

- The economy slows over the course of the year, but doesn’t fall into a serious recession.

Despite a run-up, MGIC’s stock remains cheap

MGIC’s stock price rose by 39% over the past year. Yet its P/E ratio, using my ’24 cash EPS forecast, is still only 7.5. And its cash return is 13.4%. Now MGIC is far from a growth story. As I said, its insurance in force actually shrank by 1% last year. Its market – Fannie Mae and Freddie Mac mortgage-backed securities (MBS) – rose by only 1%. Long-term, home mortgage debt should grow in line with nominal GDP growth, or maybe 4%.

In an investment world where revenue growth is more newsworthy than earnings growth, why buy MGIC? Because of that 13.4% cash return. Compare it to bond yields. 13.4% is about what CCC-rated corporate bonds yield. The CCC rating “denotes a very high level of default risk” (Google AI). Yes, the 13.4% yield is far from guaranteed in the future – it will fall materially for several years if the U.S. gets hit with a serious recession. But even in that dire case, earnings won’t fall dramatically because MGIC is spending a lot on reinsurance that will significantly reduce the cost to it of a recession.

Short of that serious recession, I am confident that MGIC’s cash EPS will gradually grow, for 4 key reasons:

- Much more conservative lending standards

- A housing shortage

- Homeowners have tons of equity

- MGIC has substantial excess capital

Reason for optimism #1: Much more conservative lending standards

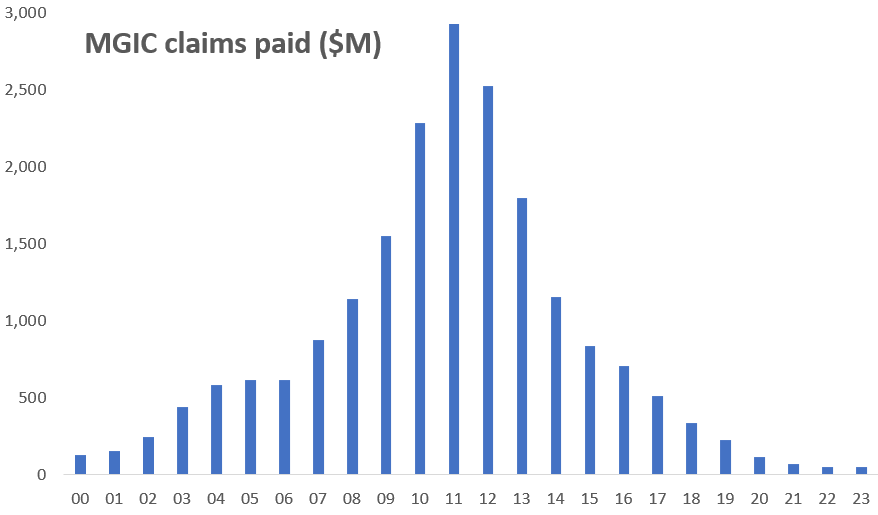

This chart shows a history of MGIC’s claims payments:

MGIC financial reports

Sources: MGIC financial reports

At $46 million, MGIC’s losses last year were the lowest since the 1990’s! Note that the U.S. was in a massive housing bubble during ’04-’06, and average annual losses were still 13 times higher than today. On its IIF added since 2016, MGIC has only been required to make $39 million in claims payments. How is that possible? Because MGIC, and really the entire home mortgage lending industry, maintains much safer lending standards. Specifically, they stopped making subprime and other non-prime home mortgages.

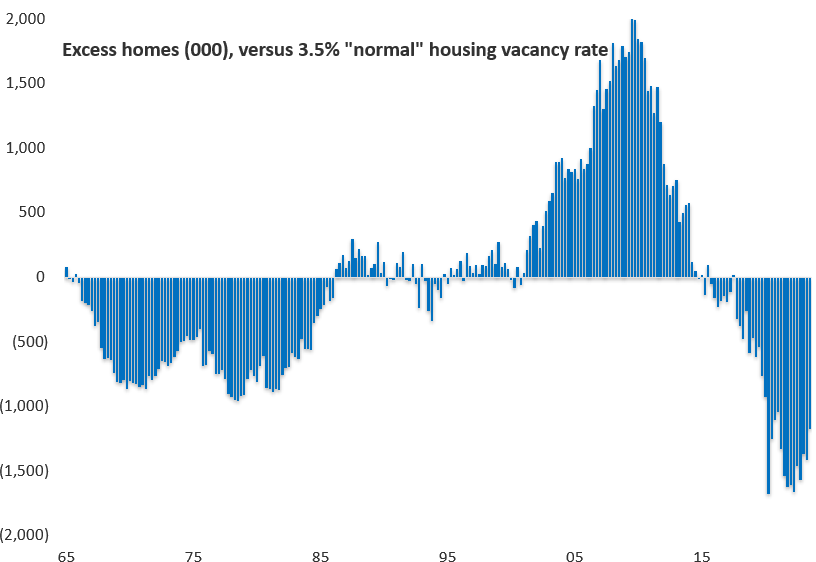

Reason for optimism #2: A housing shortage

The Census Bureau just released its latest quarterly snapshot of U.S. housing supply and demand. We remain seriously short of housing, which is positive for home prices and therefore for mortgage defaults:

Census Bureau

Source: Census Bureau

Clearly many years of over-building will be required to create a housing excess that could lead to higher defaults.

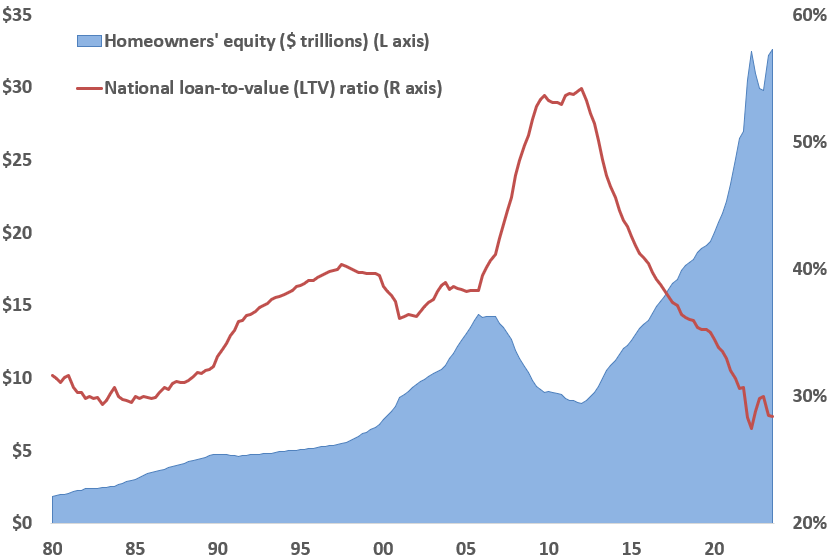

Reason for optimism #3: Homeowners have tons of equity

The current numbers are historically strong:

Federal Reserve

Sources: Federal Reserve

Homeowners collectively have over $30 trillion of equity protecting their mortgage debt. And their debt averages less than 30% of the value of their homes, the lowest ratio in at least 50 years.

Reason for optimism #4: MGIC has substantial excess capital. With lots more piling in

Check out these two measures of capital:

- Regulatory capital. MGIC had $5.8 billion of regulatory capital at the start of this year. It needs only $3.4 billion, in part because the reinsurance it bought is considered to be the equivalent of $2.2 billion of capital. So that leaves $2.4 billion of excess capital.

- Holding company cash. MGIC has $900 million of cash at its holding company (not tied up in an insurance subsidiary). Management says that it wants to retain several years of dividend and interest payments in cash. That comes to maybe $400 million. So the company has $500 million of free cash available to shareholders.

But it gets better. Over the past three years, MGIC paid out an average of $600 million per year of dividends from its insurance subsidiaries to it holding company. My cash earnings forecast suggests that MGIC will add over $650 million of cash to its insurance subsidiaries, so another $600 million dividend to the holding company this year seems quite reasonable.

And since MGIC already has loads of extra holding company cash, that $600 million should largely go investors’ way. About $120 million will be paid as dividends. That leaves $480 million for share repurchases. At the current stock price that means 24 million fewer shares, or 8% less. That’s similar to last year’s 7% reduction. And it’s how in my cash EPS forecast above a 2% dollar increase in earnings turns into a 10% increase in per share earnings.

Unless a serious recession gets in the way, that math will continue – modest dollar earnings increase will turn into 8-10% per share increases.

Summing up. A $27 price target

A 10 P/E – half the market multiple – seems more than reasonable than the current 7.5 ratio for a company with MGIC’s risk and growth profile. That’s a 35% upside. If you don’t want the stock at this price, management is more than happy to buy it.

Q2 2024 Earnings Call Transcript")