Svetlana Sultanaeva/iStock via Getty Images

The U.S. financial system has plenty of money to support itself.

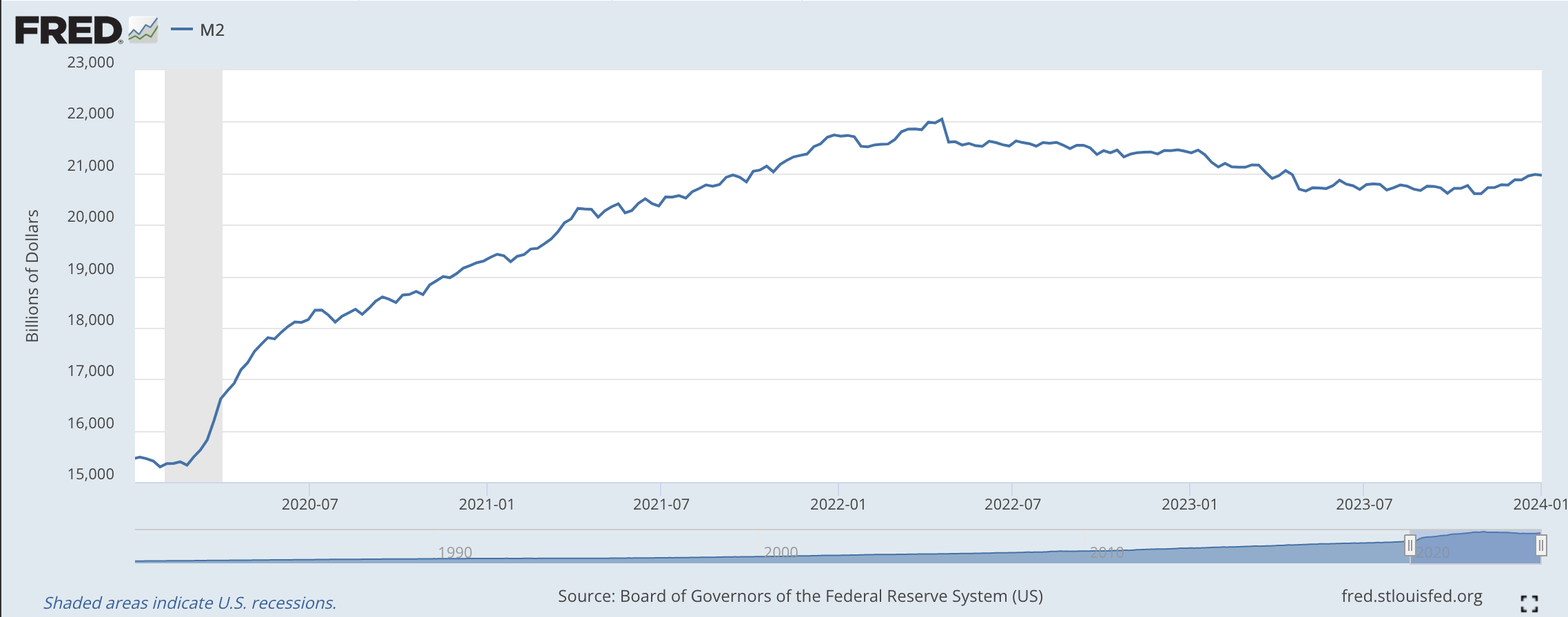

Take a look at the M2 stock of money in the economy.

M2 Money Stock (Federal Reserve)

Yes, the M2 money stock has declined a bit since early 2022, but it is still up an enormous amount since early in 2020.

This is what I have been trying to emphasize over the past few months.

The Federal Reserve is steadily reducing the size of its securities portfolio.

We can see this from the following chart,

Securities Held Outright (Federal Reserve)

In fact, the amount of securities held outright by the Federal Reserve has declined by almost $1.4 trillion since the middle of March 2022.

This decline is a very large number, but the Fed still has over $7.1 trillion in securities held outright on its balance sheet.

One can see from the first chart above that the Fed was busy injecting reserves into the banking system from early 2020 through to the middle of March 2022.

So, the banking system still has an enormous amount of funds floating around the financial system.

And, this is the narrative I have been trying to talk about in posts like the one I wrote yesterday, “where are interest rates going?”

And, this is the situation that Jerome Powell and the Federal Reserve are trying to work their way out of.

The Federal Reserve responded to a financial crisis as the Covid-19 pandemic sped through the U.S. economy and the world. In combating this situation, the Fed worked to err on the side of channeling too much liquidity into the banking system. The Fed did not want to be accused of doing too little to keep the financial system together.

And, it seems as if the Fed did its job and prevented the U.S. economy and financial system from falling apart.

But, there is now the “other side of the coin to deal with.” Now, the financial system now has lots and lots and lots of money, sitting on balance sheets that could be used to go on a spending spree. This could generate excessive inflation again.

But, the Federal Reserve has responded with its policy of quantitative tightening, and this effort seems to be containing inflation while not jerking the economy around with an overly tight monetary policy.

The Federal Reserve has been reducing the size of its securities portfolio in a consistent, steady fashion. The Fed has been reducing the size of its securities portfolio for over twenty months, and has seemingly convinced the investment community that it will continue to do so for a much longer time.

The business and investment communities have responded by not pumping up prices again. The Federal Reserve has apparently convinced these individuals that it will continue to keep on with quantitative tightening as long as it appears that it is needed.

What does this do?

The Federal Reserve is reducing the excess liquidity that is in the U.S. financial system. It seems to be doing the reducing at a fast enough speed that the economy has pulled back from taking advantage of all the liquidity and “making money” by generating more and more inflation.

The economy currently seems to be using the money to acquire assets, financial and physical, much in the way it acquired assets during the period of economic expansion following the Great Recession in the 2010s.

One place where funds have been used has been in the stock market. This is what happened in the 2010s, and I wrote and referred to the activity that was going on as “credit inflation.”

The economy expanded, although modestly, price inflation remained low, and stock prices and other asset prices rose consistently.

It seems as if investors and business people are now acting much as they did in this period of credit inflation.

Why, just last week, the Standard & Poor’s Stock Index hit a new historical high. Furthermore, it seems as if investors have positioned themselves to move more heavily into stocks. This movement seems warranted to me.

In fact, this seems to be the right narrative for investors to move forward with.

There is plenty of money available in the U.S. financial system.

These monies are “out there” because of the Fed’s past efforts to fight the effects of the Covid-19 pandemic. These monies will not be used for consumer price inflation as we move forward because the Federal Reserve will continue its policy to reduce the size of its securities portfolio through quantitative tightening.

This will keep consumer price inflation down in the U.S. economy.

The “excess cash” that is around will be used for purchasing stocks and other assets that investors believe are attractive. It should be a pretty good time for investors.

The economy will continue to grow, but the growth rate will not be excessive. But, unemployment should not become a problem in the near future.

As I argued in my post of yesterday, in this environment, I do not see short-term interest rates coming down to any degree. Any further economic growth coming from further monetary stimulus would be only of minor benefit.

And, it could stir inflationary expectations once again. We don’t want to do that.

If this picture works out, investors should be working in a very nice environment for the near future.

Q2 2024 Earnings Call Transcript")