sommaiphoto

Investment Introduction

Just looking at the price chart of EnerSys (NYSE:ENS) it seems they are quite volatile when the earnings reports are being released. In late May, the company posted their quarterly results and the stock price shot up nearly 20% in the span of a few days. Now as we approach the next earnings report by the company, expected to be released on February 8 after the market close, I am wondering if the same qualities and improved operational performance can be read in this report, just like their Q4 report on May 24. I am leaning towards that a decent beat is possible for ENS once again. The fourth quarter saw EPS beat by $0.44 and come in at $1.82. Historically, the company has been inconsistent in meeting some earnings estimates, but I think it’s being unfairly to some degree baked in with the current stock price. The stock is valued at a discount and offers investors a solid buying opportunity ahead of coming earnings.

Company Introduction

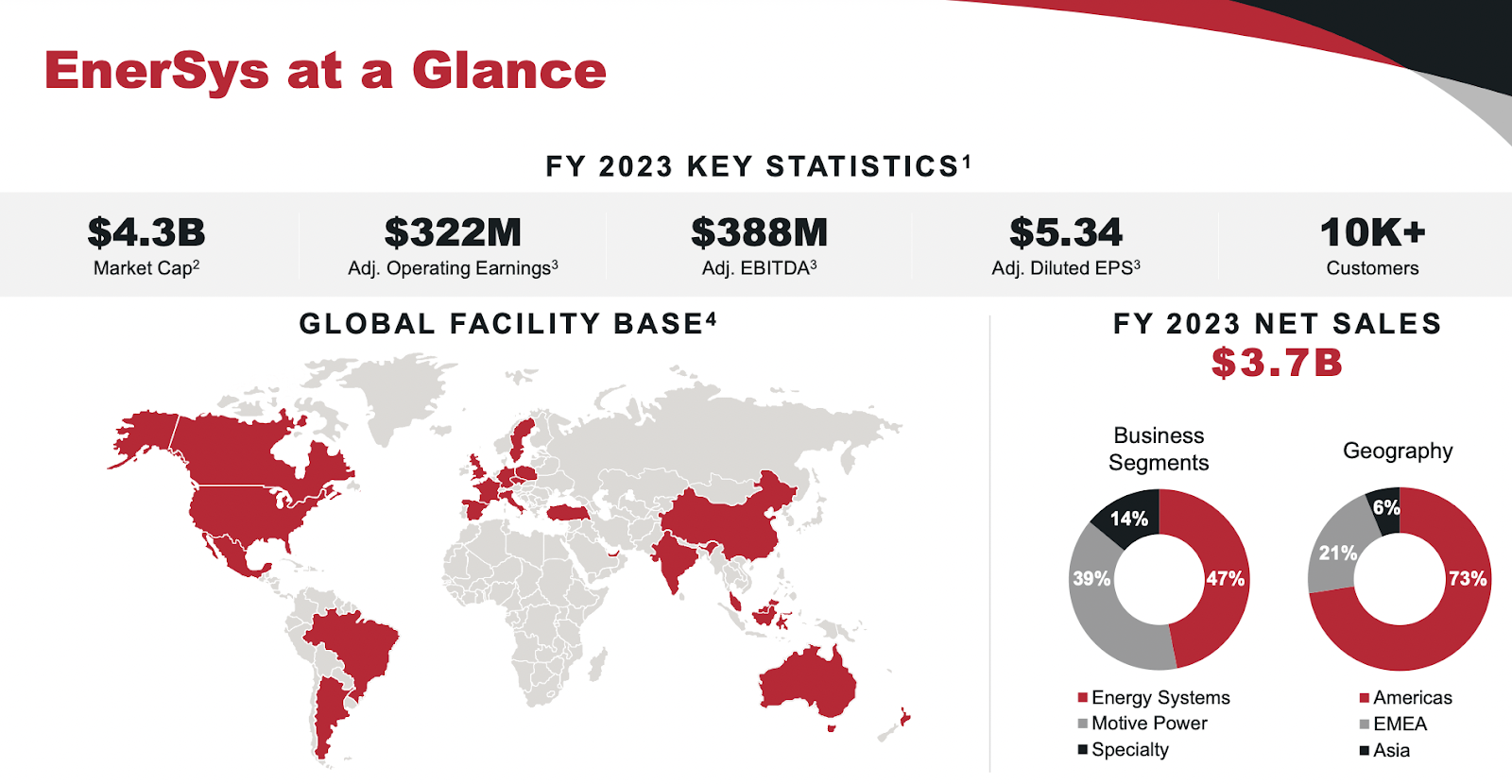

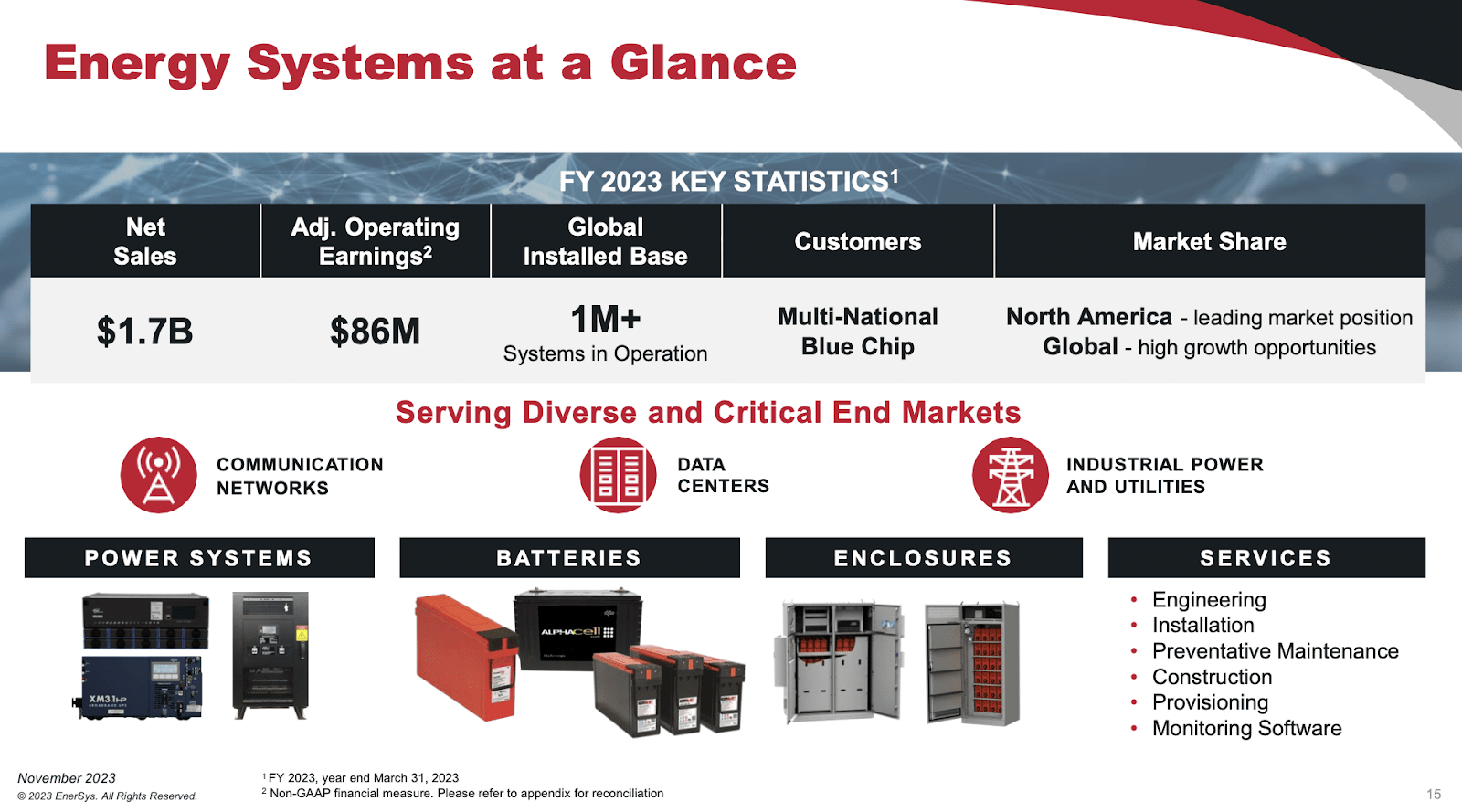

ENS holds a significant position in making industrial battery manufacturers, as operations span globally. The company operates across three main sectors: Motive Power, focusing on electric vehicles like forklifts; Energy Systems, focusing on telecommunications and uninterruptible power supplies; and Specialty, which includes aerospace and defense applications. The company has expanded its portfolio through strategic acquisitions like the Alpha Technologies Group, enhancing its offerings in DC power and energy storage systems. Apart from being a significant battery manufacturer, ENS also has various chargers and energy systems in their product lineup.

Operational Overview (Investor Material)

The agreement to acquire Alpha Technologies came in late 2018 and looking at how the revenues have been impacted they have been trending upwards very well since 2018 ENS has averaged a revenue CAGR of 6.83%, now at nearly $4 billion in annual revenues. The acquisition was valued at $750 million in total and resulted in a strong addition of power supply solutions to ENS. What I think was very beneficial for shareholders of ENS since then is that the deal didn’t necessarily overleverage the balance sheet, and ENS seems to have paid a good price as well. With annual revenues of $600 million for Alpha before the acquisition, ENS only paid a sales premium of 1.25. Quite low for acquisition targets, at least these days, I think.

Market Opportunity (Investor Material)

ENS paints itself as a company that can capture market demand. Although one shouldn’t base an investment thesis on previous results as they are no indication of future results, in the case of ENS, they have captured much of the momentum its addressable markets have shown. ENS estimates they have a $30 billion serviceable addressable market and plenty of room to grow within this, as FY23 net sales were $3.7 billion. The primary markets that I am looking at for ENS are data centers and industrial power which are driven by tailwinds such as energy transition and energy security. Deglobalization has hit some markets as countries aim to bring manufacturing back home within their borders. It would be true to say this is a risk to some companies and industries, but in the case of ENS, I think it’s very limited. They come from a different angle, that is to power up and enable increased production and manufacturing capabilities with their batteries and energy solutions. This approach will position them as a winner over the long term.

Valuation

Company Glance (Investor Material)

ENS serves as a medium to high-growth company in the industrial sector right now, I think. If we look at the valuation and attribute a more sector-similar valuation, the upside would suggest a lot of growth here, but more on that below. In terms of growth for the top and bottom line, it will be fueled by high growth opportunities globally and be supported by a leading position that ENS holds in the US in regards to its power systems and batteries produced.

The Value You Get

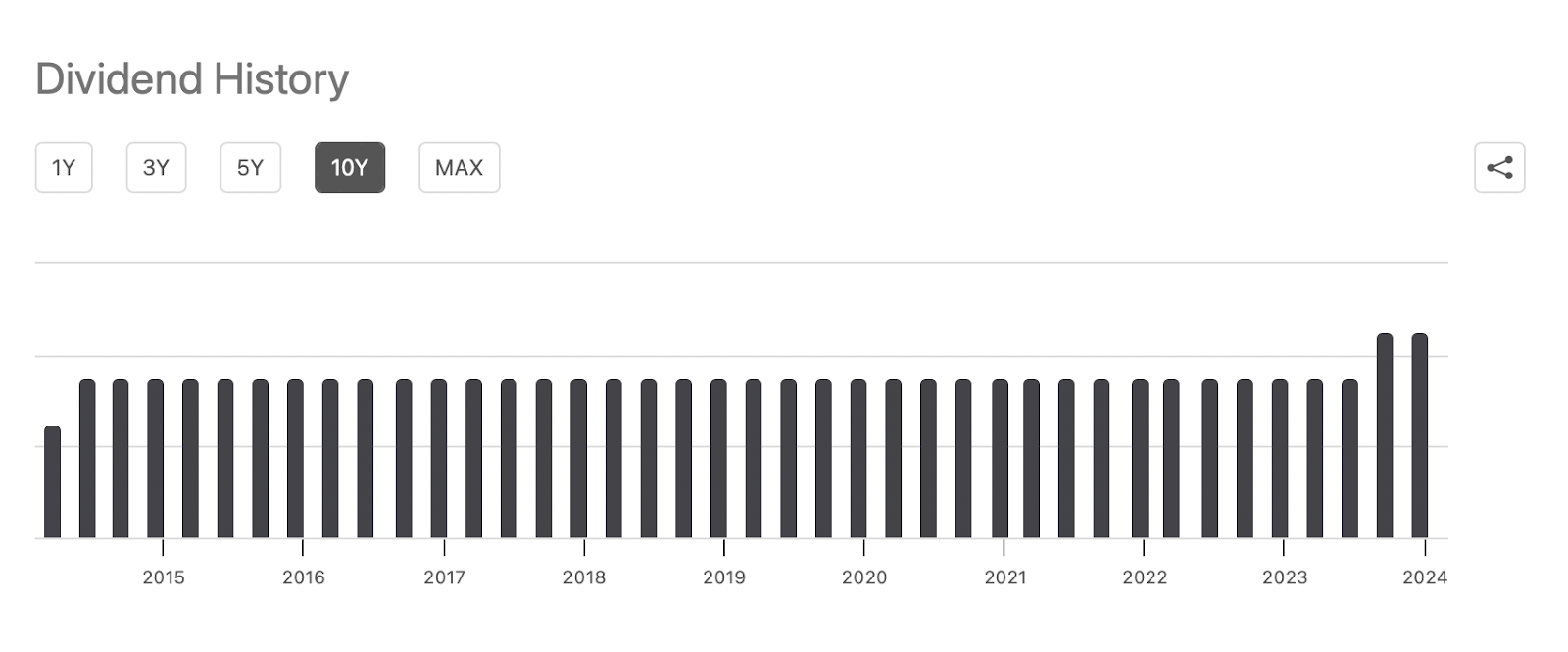

What I define as the value that you get would be if a company has an established dividend program or buying back shares frequently is a broad practice. In the case of ENS, you are getting a dividend yield of 0.94% but no real scheme for buying back shares, unfortunately. Dividend raises are also quite a new phenomenon for ENS as well. It was only in the past 2 quarters that a higher dividend was distributed. Previously it had remained the same going back to the middle of June 2014. Perhaps partly the result of a stronger financial position, but also the fact the market outlook remains positive and even filled with higher demand.

Dividend History (Seeking Alpha)

In the last report, the company bought back shares totaling $47.3 million, which is more than double the amount the company did in the first six months of 2022. Could this be a switch in the company’s approach to delivering value for shareholders? Not necessarily, but I do think it indicates that ENS believes its share price is significantly undervalued in comparison to what it could be generating in terms of revenues and earnings in the next few years.

Price Target

Valuation (Seeking Alpha)

When looking at the valuation of ENS, I first look at the P/E. ENS is at a pretty significant discount right now, as I have mentioned throughout the article already. The discount could come from margin worries and that the recent improvements are not something that can last. On top of this, the company has some debt due in the next few years that would take out a chunk of the cash position most likely, limiting future growth potential, or at least investment potential. I don’t think this should all result in a discount of 35.21% for earnings and 24.94% on sales. I think that given the volatility of margins previously, a 15% discount to the sector would do the thesis justice here. With that in mind, the P/E should be 15.6 for ENS, and I think an EPS estimate of $7.2 is within reason here given increased demand and what could be resilient margins. This gets me a price target of $112 for ENS, indicating an upside of 15.7%. This is a worthwhile amount to buy into and should the report deliver surprisingly strong margin improvements I think this price target might be reached quite quickly.

The Bear Thesis

Margin Graph (Seeking Alpha)

The primary risk to ENS and the bear thesis I think is based on poor margin development. It can’t be left unsaid that ENS has had trouble in keeping consistently growing and strong margins over a long period. The past 5 years have been a rollercoaster, resulting in an average gross margin of 24.07% and 4.74% NI margin. What I think has also to be accounted for is the significant amount of volatility the markets have experienced during this period. A discount to the valuation for ENS seems justified, seeing as they have lacked resilience during this period. However, the discount still wouldn’t put ENS in a spot where a sell or a hold would be justified, as I see it. My thesis would be disproven if the current margin improvement trend reverses and ENS finds itself with higher expenses like material shipping costs. For reference, ENS managed to raise gross profits by $44.7 million YoY while revenues just grew by 0.2% YoY.

State Of The Company

Income Statement (Earnings Report)

A shift in the past few quarters has certainly been the increased profitability of the company. As the gross profits accelerate past the growth of net sales by a wide margin, I think that ENS is shaping up very well for the coming report. ENS has remained quite conservative in taking on more debt, and this seems to have proven to be the right direction in the past 12 months as interest rates have climbed higher. Just as the gross profits climbed rapidly, so did the net earnings too now at $65.2 million for the quarter, up from $34.5 million. All in all, a solid YoY improvement for ENS and something I think they can build on and carry with them in 2024 too.

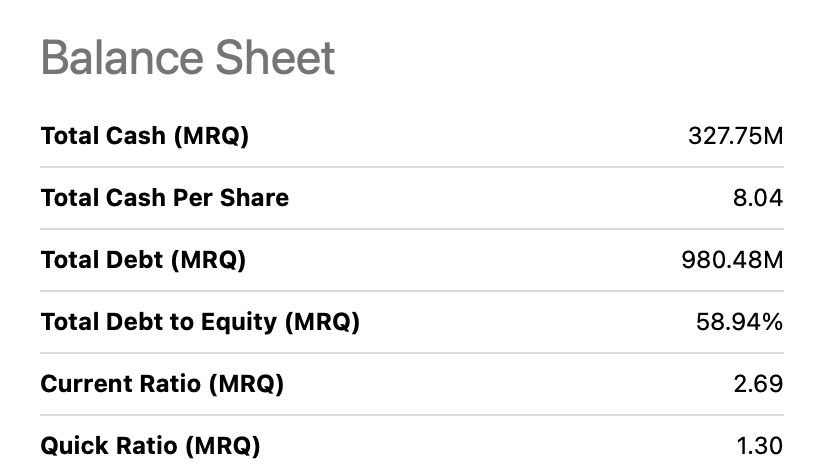

Balance Sheet Highlights (Seeking Alpha)

A quick look at the balance sheet highlights reveals what I think is a rather stable business, with a lot of cash at hand and a manageable amount of debt as well. Cash is $327 million and total debt is $980 million. The debt is manageable like I said, but I don’t think ENS is in a place where they should be raising more to fund expansion before paying down a bigger chunk, the debt-to-equity ratio is nearing 60% and this is a place where I think I would become more worried as an investors and possible hold back increasing a position. The last 10Q from ENS reveals the majority of the debts, around $600 million, seem to be due in FY2026. This still leaves ENS with the opportunity to build up a larger cash position as demand is picking. The state of the company I would therefore say is quite solid and doesn’t necessarily showcase any risks that would outweigh the buy thesis I have currently.

Investment Conclusion

ENS operates in reliable markets where it has carved out a space for itself as a leader in the US but is still presented with a lot of growth prospects globally. The current valuation suggests a pretty steep discount, which I think seems unwarranted. Worries relate to incitement margins the past few years, but I think that will over time balance out. The state of the company is positive and with the value presented in the form of a steady dividend, I land at a buy here for ENS.

Q2 2024 Earnings Call Transcript")