marrio31

Welcome to another installment of our BDC Market Weekly Review, where we discuss market activity in the Business Development Company (“BDC”) sector from both the bottom-up – highlighting individual news and events – as well as the top-down – providing an overview of the broader market.

We also try to add some historical context as well as relevant themes that look to be driving the market or that investors ought to be mindful of. This update covers the period through the fourth week of January.

Market Action

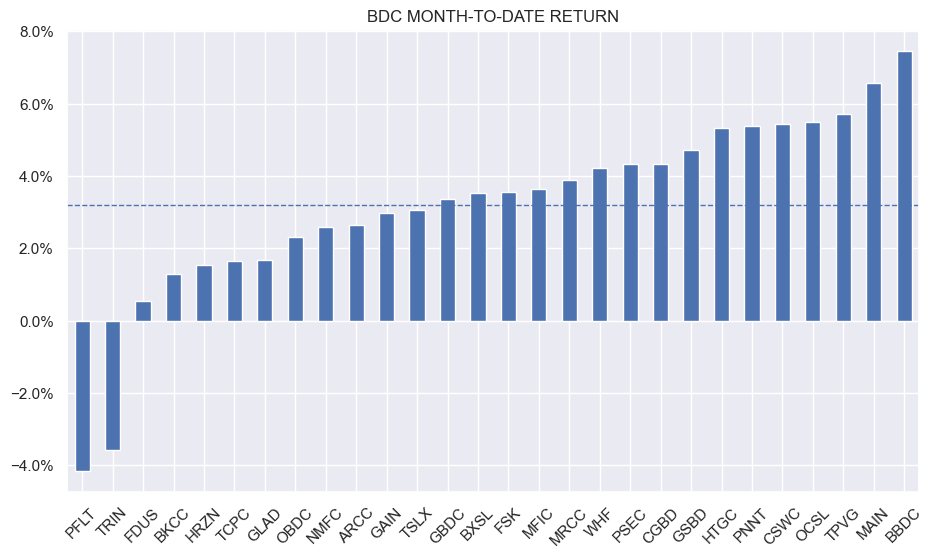

BDCs had another good week with a 1.5% total return. Month-to-date, only two BDCs in our coverage are in the red.

Systematic Income

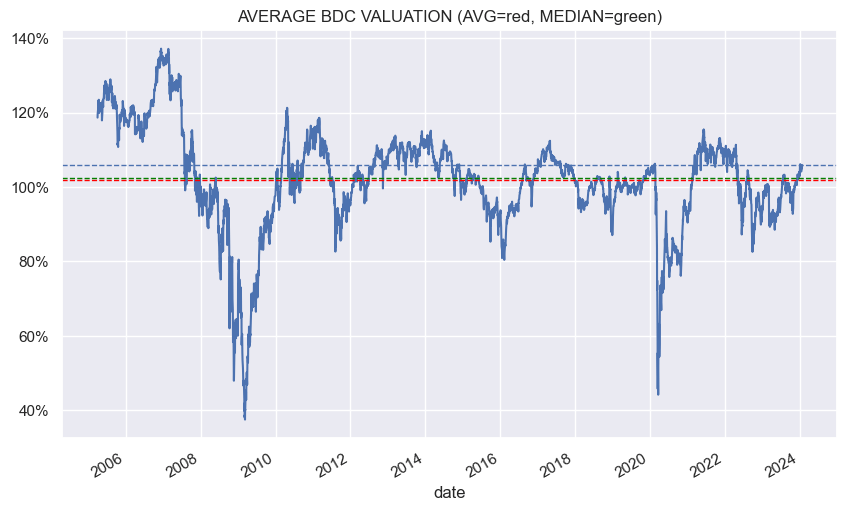

Aggregate BDC valuations remain above their historic average. The sector has been supported by an unwinding of some expected Fed cuts as well as a delay in the likely first cut.

Systematic Income

Market Themes

GBDC is merging with its private BDC – GBDC 3 – with GBDC carrying on as the surviving entity. Recall GBDC also merged with Golub Capital Investment Corp in 2019. GBDC is not the only BDC merging with its private sister BDCs. The Oaktree Specialty Lending Corp (OCSL) merged with OCSI in 2020 and OSI II last year.

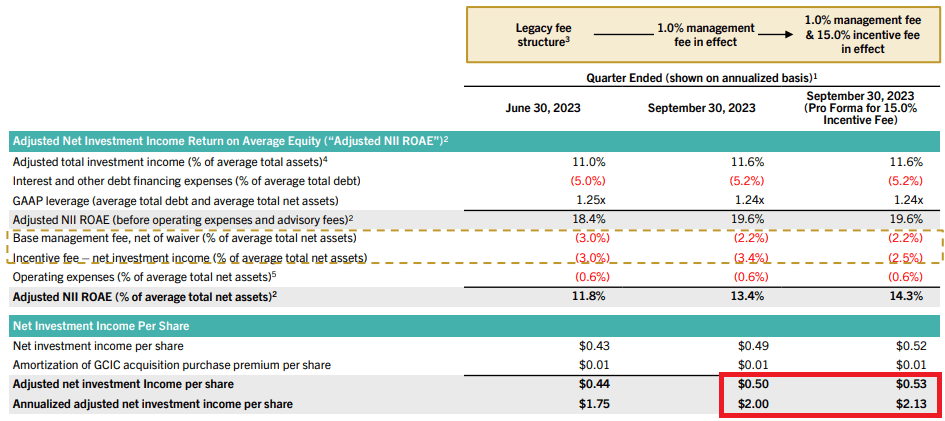

There are the usual benefits of a larger BDC such as improved liquidity, lower fixed costs, possibly better pricing on debt issuance. As far as more concrete benefits, as a sweetener, the GBDC incentive fee is falling from 20% to 15% – the lowest in our coverage. The reduction is effective 1-Jan but will be made permanent on completion of the merger. It is expected to add $0.03-0.04 to adjusted net income per quarter.

GBDC

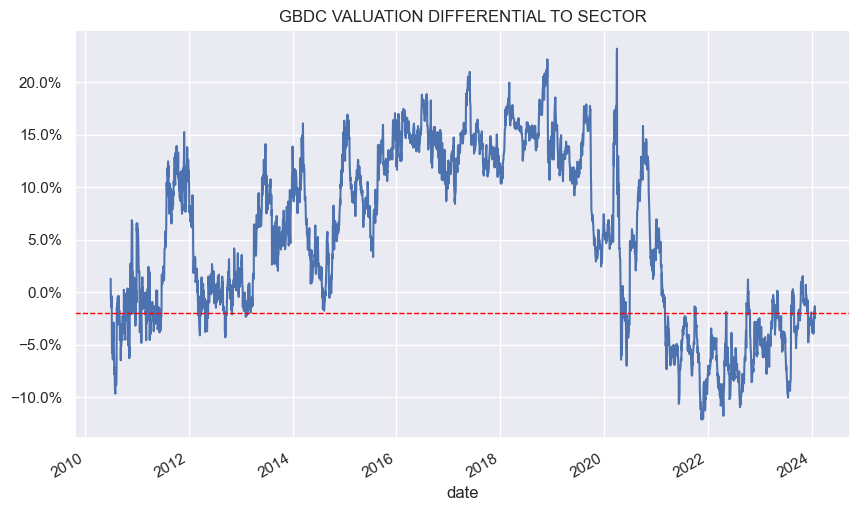

The combination of the recent base management fee cut as well as this cut in the incentive fee means GBDC is now good value not when it trades at a discount to the sector but when it trades at the sector valuation – about where it is now. Any drop below the sector valuation would be a great opportunity to add the stock.

Market Commentary

Ares Capital Corp (ARCC) announced a $1bn offering of 2029 5.875% notes. Recall that we had a number of other BDCs, including MAIN and TSLX, issue bonds already this year. BDCs are clearly taking advantage of the recent drop in longer-term Treasury yields (10Y yield falling from 5% towards 4%).

This new bond looks to be a refinancing of the 2024 4.2% bond so the net result is that interest expense will rise marginally for the company. With short-term rates having flatlined for a while now, refinancings will cause net income to descend slightly in the sector which should then accelerate somewhat once the Fed actually cuts rates.

Stance And Takeaways

The cuts in both management and incentive fees means GBDC net income has risen by a pro-forma 20% in a short span of time, all else equal. This means that the company’s valuation should rerate higher given its sustainably higher level of forward net income.

In practical terms, the company should continue to raise its base dividend. On a pro-forma basis, its base dividend coverage is 136% which gives it additional room to hike even if the Fed makes a series of rate cuts. We will be looking to add to our GBDC position on any dips relative to the sector.

Systematic Income

Check out Systematic Income and explore our Income Portfolios, engineered with both yield and risk management considerations.

Use our powerful Interactive Investor Tools to navigate the BDC, CEF, OEF, preferred and baby bond markets.

Read our Investor Guides: to CEFs, Preferreds and PIMCO CEFs.

Check us out on a no-risk basis – sign up for a 2-week free trial!

Q2 2024 Earnings Call Transcript")