La_Corivo/iStock via Getty Images

Overview

GoGold (OTCQX:GLGDF) is a precious metals mining company in Mexico. The company has a smaller producing asset in Parral together with the two development projects Los Ricos South and Los Ricos North. This is a company I have covered frequently over the years and those articles can be found here.

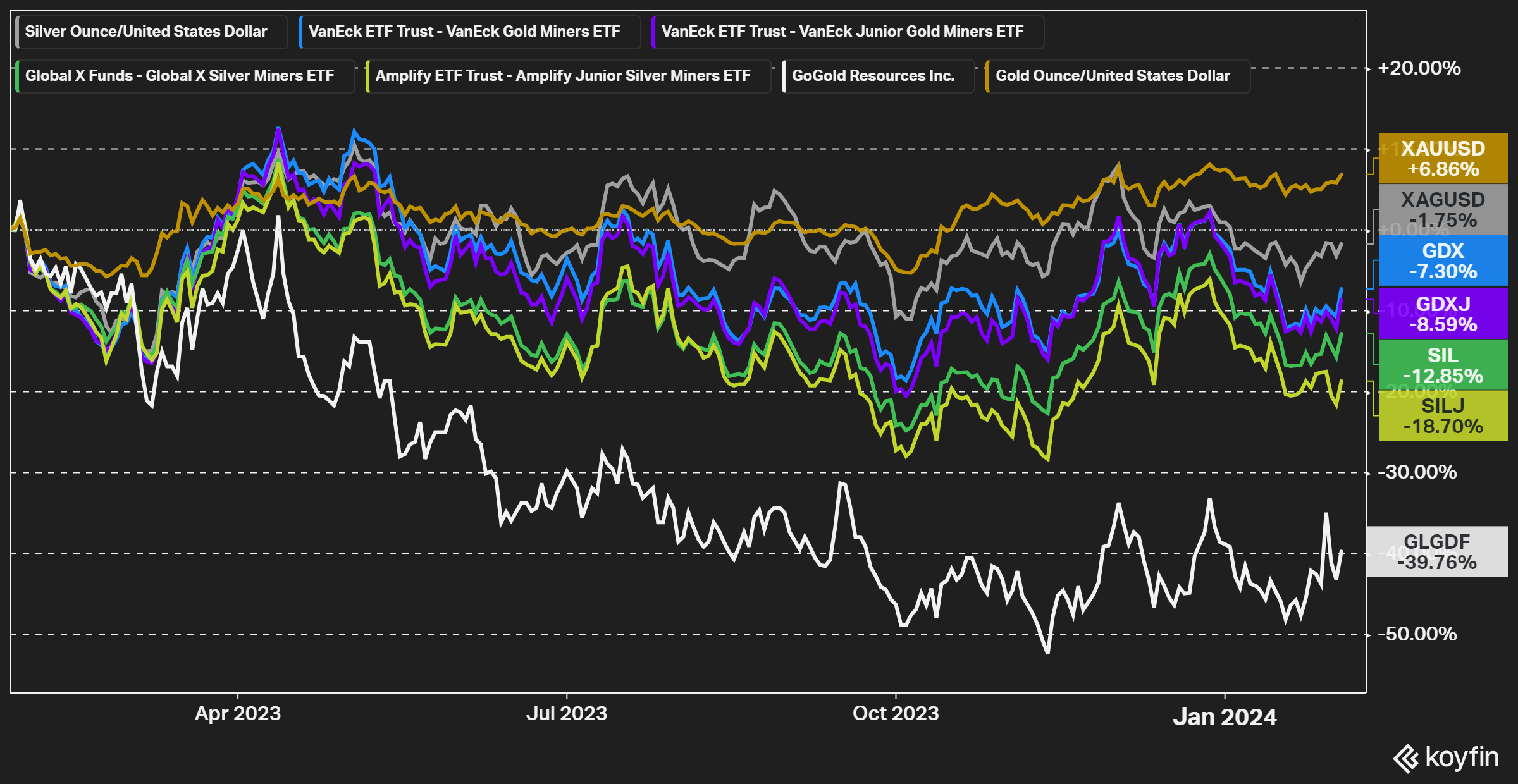

Figure 1 – Source: Koyfin

The stock price performance of GoGold has been poor over the last year, underperforming the metals and the more common precious metals mining ETFs substantially.

Part of the negative performance is likely due to developers having performed poorly in general, but I do think it is fair to say GoGold has had some challenges and disappointments over the last year, which I didn’t foresee a year ago, and that might explain some of the underperformance at least.

- The strong Mexican Peso has been a headwind on costs for all producing mining companies operating in Mexico.

- Both the Preliminary Economic Assessment (“PEA”) on Los Ricos North and the updated PEA of Los Ricos South didn’t quite meet the high expectations that I and some brokers had, even if both projects are still relatively impressive.

- Production at Parral has been low, and costs have spiked over the last year, due to the focus on re-handling old material to defer some capital investments.

With that said, GoGold is at this point attractively priced, has a few important catalysts for the coming year, and Parral should bounce back now that new material is once again being stacked on the leach pads.

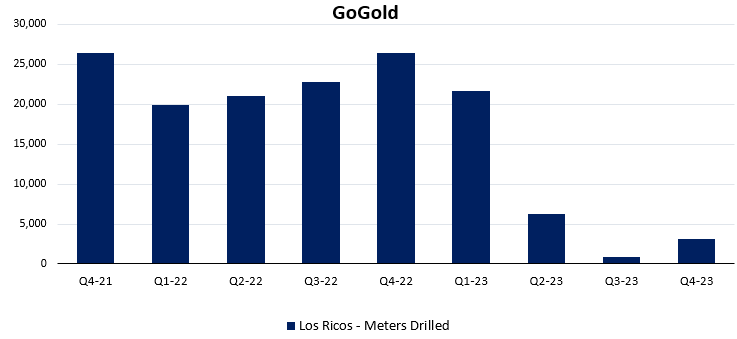

Another potential reason for the lack of interest in GoGold lately could be because the drill activity has declined substantially. The company has been more focused on technical studies and progressing Los Ricos South towards a construction decision.

Figure 2 – Source: GoGold Q4-23 MDA

Parral

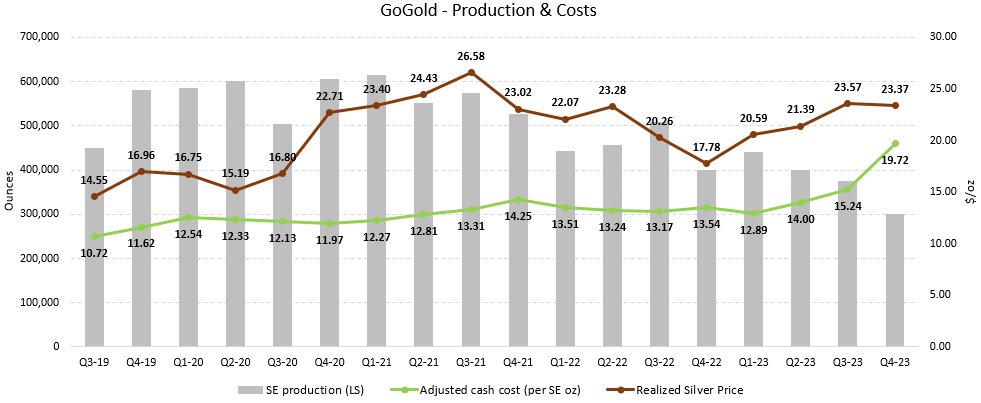

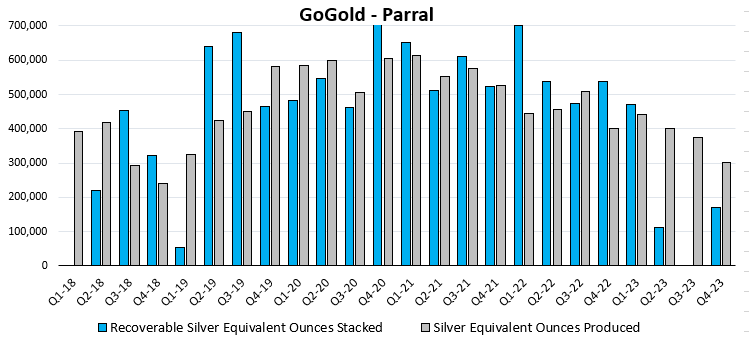

Figure 3 – Source: Quarterly Reports

We can in the chart above see that the production volume at Parral has been declining quite a bit over the last year, while costs spiked substantially over the last few quarters. The adjusted cash cost at Parral was almost $20/oz in Q4-23 and the silver equivalent production was only about 300Koz.

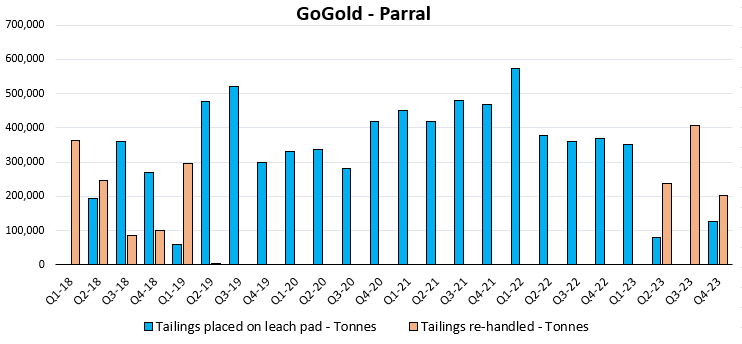

This has no doubt deterred some investors, but I am not overly concerned by the recent trend. GoGold has been re-handling some old material to defer capital investment for leach pad expansions. So, much fewer ounces have consequently been placed on the leach pad. The re-handling work concluded in August of last year, so I do expect we will see a very nice rebound of the production volume in the first calendar quarter of 2024.

Figure 4 – Source: Quarterly Reports

Figure 5 – Source: Quarterly Reports

GoGold announced in December that the completion of the zinc circuit, which has been a small construction project at Parral designed to produce zinc, and recycle more cyanide. This new circuit should be a tailwind for Parral in 2024. The company is expecting Parral to produce around 2M AgEq ounces per year, with a cash cost of about $14-15/oz.

Los Ricos

GoGold hasn’t released much new information on Los Ricos South since my last update on the company back in September of last year, where a deeper dive into the Los Ricos South updated PEA can be read here. I also published an article focused on the Los Ricos North PEA in May of last year, which can be read here.

The company is presently working on a feasibility study (“FS”) on Los Ricos South and trying to get the permit as well. This was initially planned to be a pre-feasibility study (“PFS”), but that changed to a FS recently. I like this change and I am more comfortable with a construction project based on an FS compared to a PFS. Both the FS and the permit are expected during the summer, which has the potential to be a substantial catalyst for the company.

The permit for Los Ricos South is the primary risk for the company, where GoGold is only applying for a permit on the underground portion of Los Ricos South at this point. That should make the permit more achievable, but we have over the last few years seen several permits be denied or delayed in Mexico, so this is certainly a risk to be aware of for anyone investing in GoGold.

Valuation & Conclusion

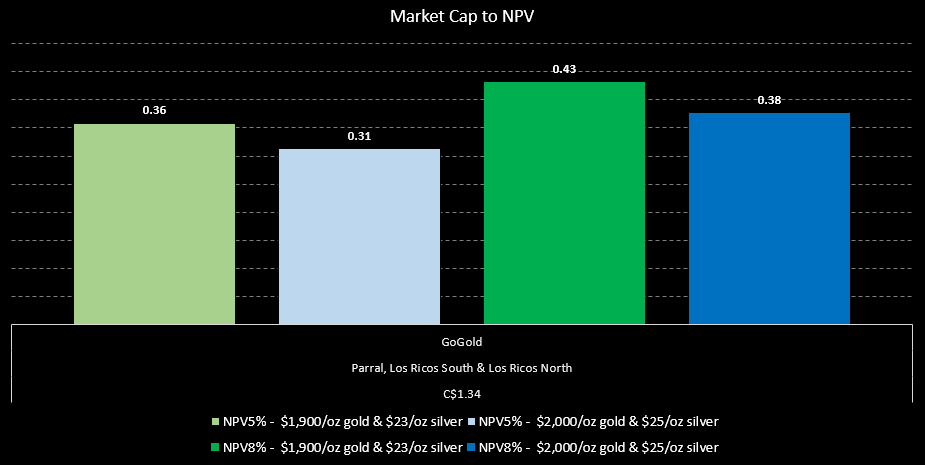

The below chart illustrates my valuation for GoGold, using a couple of different metal price assumptions, together with both a 5% and an 8% discount rate.

Figure 6 – Source: My Estimates

Here we can see that GoGold is trading with market cap to net present value around 0.31-0.43. That is not expensive for a company with one asset in production and another which could be producing in as little as two years away. I would also point out that my assumptions for Los Ricos North have been very conservative, given the open pit nature of that project.

GoGold has no debt and $95M in cash as of the latest quarterly report, so I expect the company can quite easily debt finance the remaining portion of the construction capital for Los Ricos South, which is around $150M, once the permit and feasibility study are in place.

If things go according to plan for GoGold. The company could produce a FS on Los Ricos South, get a permit for the same mine, announce a potential financing and construction decision later in 2024. I also feel very confident that Parral will rebound towards historical production and costs levels in 2024.

With that said, everything rarely goes according to plan in the mining industry, where I think delays in either the FS or the permit could keep the stock price somewhat muted in the near term. However, given how extremely well-capitalized GoGold is for a junior mining company and that Parral is producing cash flows, any delays should likely impact the sentiment more than the fundamentals of the company. So, for anyone with a 2-3-year horizon, I consider GoGold a very attractive stock here.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")