ardasavasciogullari/iStock via Getty Images

Signs of a peace deal in the Middle East led to ZIM Integrated Shipping Services Ltd. (NYSE:ZIM) slumping over 10% back to $13. The container shipping stock soared over the last month due to the Yemen Houthi attacks on ships in the Red Sea, which led to soaring shipping rates. My investment thesis remains ultra Bearish on ZIM, with the stock likely to collapse once a peace deal is reached, regardless of whether ZIM reports short-term profits.

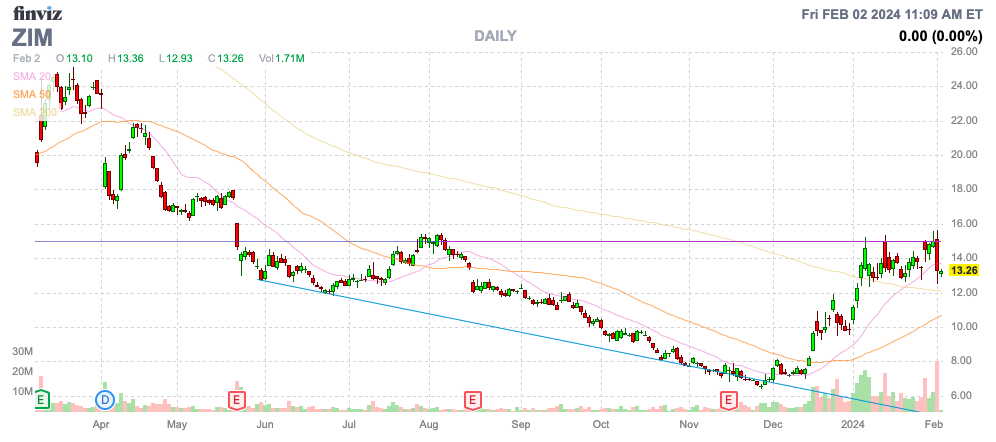

Source: Finviz

Ceasefire Risks

ZIM slumped to $12.50 on February 1, with media reports suggesting a ceasefire on the Israeli incursions into Gaza. With the Yemen Houthi rebels reportedly attacking ships in the Red Sea to support Palestinians, a ceasefire could easily bring an end to the attacks, allowing the shipping market to return to normal again.

The Drewry WCI index for February 1 has jumped to over $3,800 per 40ft container. The rate was below $1,400 back in late November, but the index did fall $140 from the recent peak on January 25.

Source: Drewry Index

The Drewry index didn’t soar until the end of December, so ZIM should still report weak results for the December quarter with an adjusted EBIT loss targeted at ~$100 to $200 million. Earlier this year, the company suggested up to 70% of their business was tied to spot rates, so ZIM should quickly start to benefit from the drastically higher shipping rates in the short term.

The conflict faces further downside risk to shipping prices due to the inability of the Houthi’s militants to actually inflict damage on targeted ships. The group famously hit an oil tanker last week carrying Russian products, yet the resulting fire was contained, and the ship remained seaworthy without any casualties to the crew of 23 Indian and Bangladesh crew members.

Source: NPR

The Central Command continues to detail recent attacks from the Houthis that were repealed. In our opinion, the lack of significant damage to the ships actually hit by the militant group reduces the long-term risks of reopening the shipping routes.

Big Q1 Possible

The shipping company won’t report Q4 until mi-March based on reporting Q4 ’22 numbers on March 13 last year. The focus will clearly set sights on the Q1 and 2024 guidance, with over 40 more days into the ongoing conflict by the time ZIM reports results.

The company guided to a 2023 adjusted EBIT loss of $400 to $600 million. ZIM will definitely report similar numbers, with limited opportunity for new charters to launch on the soaring prices at the very end of December.

Analysts don’t appear to have generally updated 2024 numbers yet. The prior estimates had ZIM losing $3.24 per share this year with a following sizable loss in 2025.

Source: Seeking Alpha

Back when shipping rates were this high following the Covid boost, ZIM reported an operating income of $2.12 billion in Q4’21 alone. The shipping company reported an average freight rate per TEU in that quarter of $3,630.

As S&P Global highlighted, the Red Sea conflict causing ships to be diverted around the Cape of Good Hope of Africa won’t help the container shipping market resolve long-term capacity issues. ZIM alone is set to add 100,000 TEU by the end of 2024, and ships needing to be scrapped will still be sailing due to this conflict. The only way the capacity issue gets resolved is for shipping prices to plunge again.

Heading into this conflict, not all shipping routes had even seen prices normalize to the 2019 and 2020 lows.

Source: S&P Global

If anything, Jefferies highlights the ultimate problem with ZIM. The company will benefit from the spot price surge, but the weakness is being reliant on the spot prices and customers aren’t going to lock in rates at these elevated prices knowing the U.S. Navy operations or a Gaze ceasefire will ultimately eliminate or reduce the Houthi threat.

Even before this conflict, Clarkson Research forecasted a huge oversupply growth in 2024 and 2025 via additional fleet capacity added in 2024 and 2025 beyond forecasted supply growth. If anything, the Red Sea conflict could lead to further imbalance when the conflict ends due to ships delayed from normal scrapping due to the higher shipping rates in the short term.

Source: S&P Global

Takeaway

The key investor takeaway is that ZIM Integrated Shipping Services Ltd. could report some very strong Q1 numbers, but the investment thesis isn’t helped by a short-term profits boost. All signs point towards an eventual ceasefire and container shipping rates collapsing due to overcapacity for the next couple of years.

Investors should continue using the strength in the stock to cash out of ZIM. The stock has failed to top $15 and all signs point towards a quick end to the threat, a threat that hasn’t actually inflicted much damage on ships in the first place. ZIM Integrated Shipping Services Ltd. stock traded around $6 at the prior lows, and the risk is a re-test of those levels.

Q2 2024 Earnings Call Transcript")