z1b

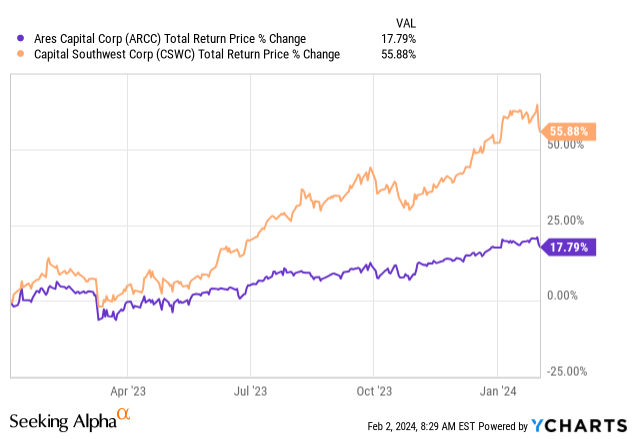

A little over a year ago, I compared two blue-chip Business Development Companies (BIZD) in Ares Capital Corp stock (NASDAQ:ARCC) and Capital Southwest stock (NASDAQ:CSWC). In that analysis, we rated both stocks as Buys. Since then, our bullishness has been rewarded, as both (and CSWC in particular) have delivered very strong total returns for shareholders:

However, a lot has changed since then, as interest rates now appear to have reached their peak, the economy continues to sustain growth while numerous recession indicators are flashing red, and ARCC and CSWC’s fundamentals and valuation multiples have both changed. In this article, we provide an updated analysis of each stock and share whether or not we think they are still buys.

Ares Capital Stock Vs. Capital Southwest Stock: Investment Portfolios

Both ARCC and CSWC are primarily focused on lending to middle market companies. ARCC has 43.1% exposure to first lien loans, 21.8% exposure to second lien loans, 6.1% exposure to unsecured/subordinated loans, 9.9% exposure to preferred equity, and 18.9% exposure to equity investments. CSWC meanwhile, has 84% exposure to first lien loans, 2.5% exposure to second lien loans, 0.1% exposure to unsecured/subordinated loans, 4.5% exposure to preferred equity, 8.1% exposure to equity investments, and 0.8% exposure to warrants and options. With 86.5% overall exposure to senior secured debt compared to ARCC’s 64.9% overall exposure to senior secured debt, CSWC’s portfolio appears to be much more defensively positioned.

Overall, non-accruals are fairly low in both portfolios, with CSWC’s sitting at 2.2% and a weighted average internal rating of its investments of 1.91 (meaning that on average its investments are outperforming initial expectations when the loans were underwritten).

Meanwhile, ARCC’s non-accruals have not been updated since Q3, but sat at just 0.6% at the time, whereas CSWC’s were at 2.0% at the end of Q3. Translating ARCC’s internal rating of its investments to CSWC’s, ARCC’s weighted average rating was 1.87, slightly better than CSWC’s.

Overall, while CSWC’s portfolio appears better positioned to weather a meaningful economic downturn given its more defensive posture, ARCC’s is actually slightly outperforming it during the current lower growth, higher interest rate environment.

ARCC Stock Vs. CSWC Stock: Balance Sheets

Both ARCC and CSWC have investment grade credit ratings and solid balance sheets overall. CSWC’s leverage ratio is just 0.77x, making it one of the lowest in the BDC sector. Meanwhile, ARCC’s is a bit higher at 1.03x as of the end of Q3.

CSWC’s liquidity is also substantial, with over $1.1 billion in cash and undrawn leverage commitments. ARCC’s liquidity is also quite large, with ~$5.3 billion in total liquidity as of the end of Q3, and management recently raised $1 billion in notes maturing 2029 in order to pay off certain outstanding indebtedness on its credit facilities. CSWC’s liquidity is even more remarkable when viewed relative to its enterprise value of $1.7 billion, whereas ARCC’s liquidity is less impressive – though still far more than sufficient – when compared to its $22.5 billion enterprise value.

CSWC’s conservative approach to its balance sheet is prudent given the current uncertainty about where interest rates and the economy as a whole are headed. As management stated on its latest earnings call:

We continue to maintain a conservative mindset to both balance sheet liquidity and BDC leverage, managing the company with a full economic cycle mentality. While this starts with our underwriting of new investment opportunities, it also applies to how we manage the BDC’s capitalization and liquidity, managing leverage to the lower end of our target range, while ensuring strong balance sheet liquidity, affords us the ability to invest in new platform companies even in periods of volatile capital markets, when risk-adjusted returns can be particularly attractive. Additionally, it allows us to support our portfolio companies while also opportunistically repurchasing our stock if it were to trade meaningfully below NAV.

Ares Capital Stock Vs. Capital Southwest Stock: Risks

Both ARCC and CSWC are quite economically sensitive given that they invest in middle market companies that often have quite a bit of leverage on their balance sheets and tend to suffer more than large businesses during economic downturns.

That being said, ARCC benefits from the scale and experience of ARES’ underwriting and recoveries teams and CSWC also has considerable experience with handling challenging macroeconomic environments. Moreover, as we previously noted, CSWC’s portfolio is quite defensively positioned with the vast majority of its investments being in 1st lien loans.

It is also worth noting that neither stock cut its dividend during 2020 when COVID-19 uncertainty was at its peak and both have consistently created shareholder value over the long-term, which further mitigates recession concerns for these two stocks.

Another risk to keep in mind is that both invest heavily in floating rate loans. Yes, they also have significant floating rate debt exposure on the liabilities side of their balance sheets, but overall, their net investment income will likely decline some in the wake of Federal Reserve interest rate cuts. An ideal scenario for both – and ARCC in particular – is that the economy will avoid recession and the Federal Reserve will be able to only gradually reduce interest rates over the next several years, thereby keeping non-accruals and defaults low on ARCC’s and CSWC’s investments while still keeping net interest income at elevated levels.

However, a scenario in which the economy falls into a recession would be detrimental to both companies, as non-accruals and defaults would likely rise sharply due to weak economic conditions while net investment income would take an additional hit due to the Fed likely feeling compelled to slash rates fairly aggressively in an effort to prop up the economy.

ARCC Stock Vs. CSWC Stock: Valuations

On a Price to NAV basis, CSWC is far more expensive than ARCC is given its 44.96% premium to NAV vs ARCC’s much smaller 5.74% premium to NAV. Meanwhile, their other metrics are much more comparable:

- CSWC’s NTM P/E ratio is 9.22x, whereas ARCC’s is 8.53x.

- CSWC’s NTM dividend yield is 9.9%, whereas ARCC’s is 9.7%.

How can ARCC’s earnings yield be only ~7.5% less than CSWC’s and CSWC’s NTM dividend yield actually be higher than ARCC’s despite ARCC trading at such a cheaper valuation relative to its NAV? A big reason behind this is that CSWC’s expense ratio is so much lower than ARCC’s. As per, cefdata.com, CSWC’s non-leveraged expense ratio is 5.02% and its leveraged expense ratio is 12.02%. In contrast, ARCC’s non-leveraged expense ratio is 8.68% and its leveraged expense ratio is 14.37%. As a result, ARCC is a much less efficient operator than CSWC is as more of ARCC shareholder’s earnings go to pay management fees than they do with CSWC.

A big reason for this difference is that CSWC is internally managed, meaning that it benefits from economies of scale in terms of its management expenses and management is more fully aligned with maximizing shareholder value. In contrast, ARCC is externally managed by Ares Management Corporation (ARES), which means that management is incentivized to grow the company’s enterprise value as much as possible in order to maximize the fees that ARES earns from managing the fund. Of course, ARCC has a tremendous long-term track record of delivering market-crushing total returns and ARES’ team is clearly skilled at underwriting and managing ARCC’s investment portfolio, so investors cannot really complain about the higher expense ratio. Still, this key difference is important to grasp when determining why CSWC can offer comparable dividend and earnings yields to ARCC while trading at such a higher premium to NAV.

ARCC Stock Vs. CSWC Stock: Investor Takeaway

Overall, both BDCs remain quality BDCs and have some of the very best track records in the sector. However, after their strong recent runs – and especially given the uncertainty of the macroeconomic environment – neither looks like a Buy at the moment. CSWC looks very attractive due to its conservative portfolio setup, high yield, and strong balance sheet, but its premium to NAV is significant and well above its 10-year average of 1.05x. Keep in mind that during the 2020 crash, its P/NAV briefly dropped below 0.5x. At a current premium of 45% to its NAV, it could potentially lose ~2/3 of its value without its NAV changing at all if its stock price were to repeat that same movement in the event of a future sharp market crash.

ARCC, meanwhile, is not nearly as well prepared for a recession as CSWC is given its more aggressive portfolio posture and higher leverage ratio. Moreover, while its P/NAV is not unreasonably high, it is not discounted either, as its 10-year average is 1.00x.

As a result, we are neutral on both of these stocks at this point, though we would favor CSWC for more conservative and defensive investors and ARCC for more aggressive investors with a more bullish outlook on the economy.

Q2 2024 Earnings Call Transcript")