Justin Sullivan

We all know about the classic “beat and raise” during earnings season, where a company beats estimates and raises guidance for the next quarter or year. And the market typically rewards the stock. Meta Platforms, Inc. (NASDAQ:META) took this to a new level last night, to the extent that I am struggling for superlatives. In such cases, I keep it simple.

- EPS Beat – Check

- Revenue Beat – Check

- Increased Guidance – Check

- Surprise Dividend – Check

- Surprise Buyback – Check.

The market is going gaga over the results, and META stock is up a staggering 17% pre-market. It is hard to blame the reaction, especially after the market’s sudden reversal from Wednesday’s Fed-induced selloff. There are plenty of things to focus on in Meta’s Q4 report, but I’d like to focus on the surprise dividend in this article. I wrote this article on Meta Platforms a little more than a year ago, imagining Meta Platforms as a dividend champion, comparing it to two established, dividend-paying technology stocks. Let’s call that article the “prediction” article for ease hereon. Never did I imagine, just one year later, that Meta would already set the ball rolling on its dividend.

Before we get into the meat of this article, my most recent coverage on Meta was in August 2023 when I rated the stock a “Hold,” backed by 5 reasons. Since then (hiding myself), the stock has gone up an astounding 60%, including the pre-market run today. But to be fair to myself, I literally called the bottom on Meta Platforms back in November 2022 when the stock was at around $96, and since then, the stock has nearly quintupled. You win some, you draw some.

Back to the meat of this article, the newly-minted dividend, and can Meta Platforms actually become a dividend champion? Let’s go deeper, while referencing the prediction article.

- Meta’s current total shares outstanding: 2.629 billion, a hair lower than the 2.658 billion at the time of the prediction article.

- Meta’s Free Cash Flow [FCF] in FY 2023: $43.01 billion (page 1), while the trailing twelve months [TTM] FCF was $26.406 billion at the time of the prediction article. Hmm, wow!

- New dividend that Meta Platforms has declared is $2/share annually. Dividend I had forecasted in the prediction article (using Apple, Inc.’s (AAPL) FCF-based payout ratio at that time) was $1.29, which was based on 13% of the-then FCF. Interestingly, the newly-minted annual dividend of $2 also represents ~13% of the TTM FCF as shown below.

- Annual FCF that Meta Platforms now needs to commit to meet its new dividend: $5.258 billion (that is, 2.629 billion times $2 annual dividend). This gives Meta a TTM FCF-based payout ratio of 12.22%. That is, $5.258 needed in FCF to pay $2 dividend per share divided by TTM FCF of $43.01 billion.

- Meta Platforms’ current yield 0.43%. Forecasted yield I had come up in the prediction article: 1.075%. However, the stock price was $124 at the time of the prediction article and is now at $462 pre-market.

- All in all, I am surprised a little that Meta Platforms indeed declared a dividend that closely resembles (in terms of payout ratio) what I had predicted in the article. Perhaps, Meta is indeed trying to follow the Apple-footprint when it comes to rewarding shareholders.

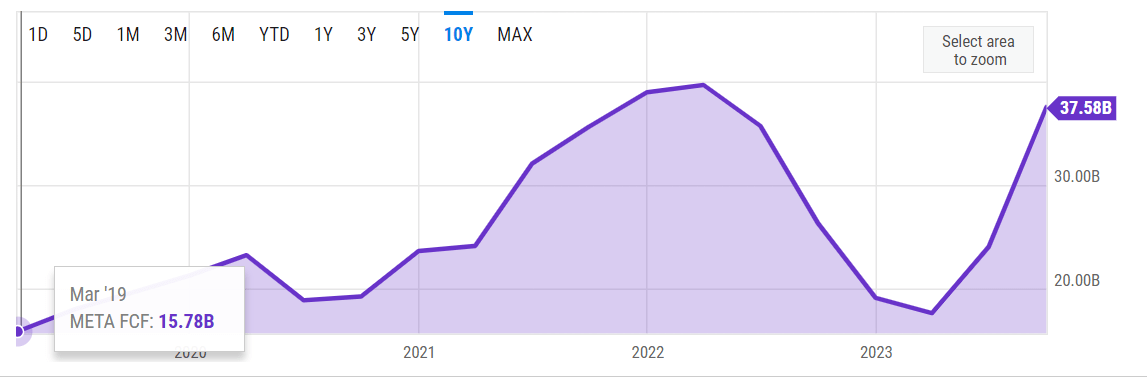

Can the company first keep affording and, then, increasing dividends here on? While that sounds like a ridiculous question right now given how optimistic everything looks, let’s not forget how dire things looked for the company in November 2022. How healthy will Meta’s new dividend look, if the company’s FCF falls to its worst levels in the last 5 years? Well, good news for investors on that front as well. Meta’s lowest TTM FCF in the last 5 years was $15.78 billion, which would mean a payout ratio of 33% using the lowest possible number in the last 5 years. We need to go back to September 2014 to find a TTM period where the FCF was less than the $5.258 needed to cover the current dividend. In short, I don’t foresee a situation where Meta cannot afford its current dividend.

Meta FCF (YCharts.com)

Next, can the company afford dividend increases? Since I used Apple’s numbers in my prediction article, why not look back at Apple’s dividend growth history? Specifically, let’s look at Apple’s dividend growth rate the first years after it re-instated quarterly dividends in 2012 at (adjusted for two splits) 9.45 cents/share:

- 2013 dividend increase: 10.89 cents/share or 15% increase

- 2014 dividend increase: 11.75 cents/share or 7.89% increase

- 2015 dividend increase: 13 cents/share or 10.63% increase

- 2016 dividend increase: 14.25 cents/share or 9.61% increase

- 2017 dividend increase: 15.75 cents/share or 10.52% increase

- For an average increase of 10.73%/yr over the first five years.

That may sound a bit disappointing, but Apple has always been a more cautious company than Meta Platforms. I mean, when was the last time Apple came to the market and said it was betting its fortunes on Wild Wild West and was going to rename itself to align with these efforts? I am a very cautious investor and analyst, erring on the side of caution and preferring to be surprised to the upside. Hence, I feel just about comfortable to use a 15% dividend growth rate/yr. below, compared to Apple’s ~10%.

Laugh all you may want at the near 1% Yield on Cost [YOC] for someone buying the stock here, but I’ve time and again made a case for strong dividend growth rates over high-yield, especially when the underlying company is deeply-baked into our every day lives the way Meta Platforms is. The forecasted 2029 dividend of ~$4/share would mean Meta would need about $10 billion in FCF (assuming similar shares count) to cover its dividend. We need to go back to March 2016 when the company last reported TTM FCF of < $10 billion. In short, Meta Platforms can easily afford to maintain and satisfactorily (to me) increase its dividends for the foreseeable future.

Meta 5 years (Author)

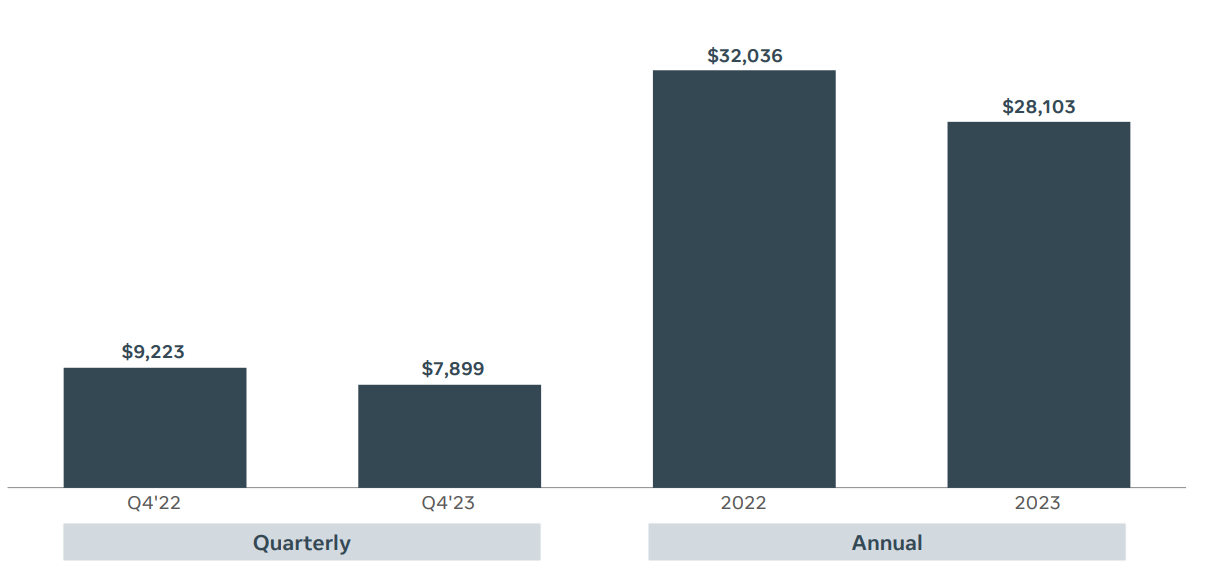

In the prediction article, I had also argued that declaring a dividend is likely to make Meta Platforms more fiscally responsible towards shareholders. Investors do not take kindly to dividend cuts, and it looks like Meta Platforms is already ahead of the game here. The company not only reduced its FY 2023 capital expenditures by nearly $4 billion (12% YoY) but has also authorized a $50 billion buyback program.

Meta CAPEX (investor.fb.com)

Let’s dive a bit deeper into what the buyback program may mean for investors. The $50 billion is good to retire about 108 million shares at the pre-market price of $462. We need to acknowledge here that Meta Platforms uses stock-based compensation (aka, dilution) to attract talent, and it is impossible that the entire $50 billion will go towards actually retiring existing shares. However, it will still offset dilution and will reduce shares outstanding. Either way, the buyback authorization is likely to save the company about $200 million/yr. in annual dividend payments, and increase earnings per share by about 4% simply by retiring these shares. Again, a win-win for investors.

Despite all these accolades, I am sticking with my “Hold” rating, as I am never a fan of chasing stocks after a monstrous post-earnings run. The market loves everything from Q4 and guidance, no doubt, but it doesn’t mean we need to chase the stock today. To conclude, Meta Platforms has surprised the market with an unexpected but always-welcome dividend initiation. Now that the company has put itself in the spotlight with dividend investors and funds, there is likely no turning back without retaliation.

I expect Meta Platforms, Inc. will continue blossoming as a dividend-paying technology stock, and I look forward to reviewing the company’s dividend progress and strength after each (expected) increase. Who knows, in 2034, I may publish a 10-year look-back article like I did with Apple last year.

Q2 2024 Earnings Call Transcript")