Thos Robinson

Billionaire Stephen A. Schwarzman recently attended the Davos World Economic Forum, where he made some very interesting remarks about what he thinks are great investment opportunities at the moment.

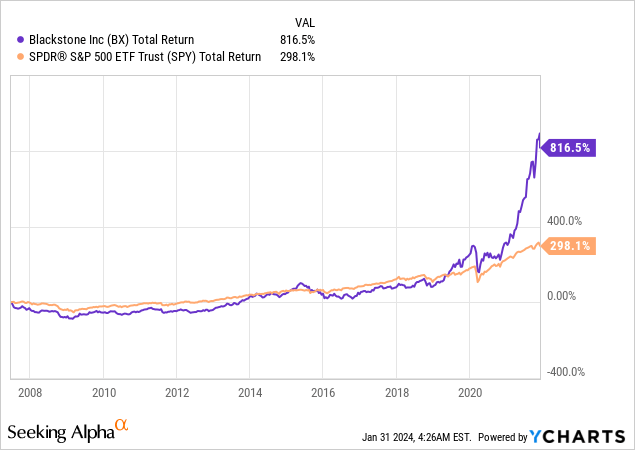

In case you are not familiar with Steve Schwarzman, he is the co-founder and CEO of Blackstone Inc. (BX), which is the biggest private equity group in the world. It controls today over $1 trillion worth of investments, and its track record is among the best in the entire world:

So when Schwarzman talks, we listen, and here are the main takeaways for me:

There Will be Many More REIT Buyouts in 2024

Blackstone has been very heavily investing in real estate investment trusts, or REITs, in recent years.

In 2022 alone, they acquired 4 major REITs for about $30 billion:

- American Campus Communities

- PS Business Parks

- Preferred Apartment Communities

- Resource REIT

Then in 2023, they took a bit of a break as it was a tougher fundraising environment and the world was very uncertain, so they closed only one acquisition

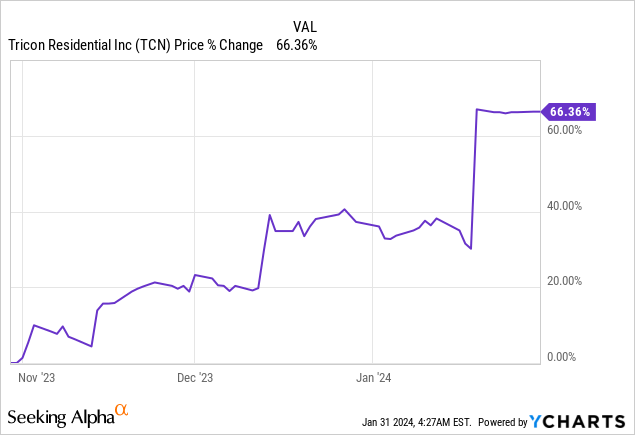

But now as we end the first month of 2024, they have already announced their first acquisition of the year with Tricon Residential (TCN), and Steve Schwarzman is telling us that they are going to be a lot more active this year:

“So as we look forward to 2024, we think we’re going to be a lot more active than we have been.”

On their Q4 conference call, he reiterated this point (emphasis added):

“We are, of course, not waiting for the all-clear sign and believe the best investments are made during times of uncertainty. We announced three major real estate transactions in the past few months, the $3.5 billion take-private of Tricon Residential, a partnership with Digital Realty (DLR) to develop $7 billion of data centers, and a joint venture with the FDIC to acquire a 20% stake in a $17 billion first mortgage portfolio from the former Signature Bank. We think this is just the start as Blackstone Real Estate has $65 billion of dry powder to invest into this dislocated market.”

They are investing in REITs because valuations are low.

REITs crashed in 2022 even as property prices remained more or less stable, and as a result, a lot of REITs are today priced at large discounts relative to the fair value of their properties.

When asked if he sees opportunities in the real estate market in the U.S., Steve Schwarzman answers that the best opportunities are today in the public market [in REITs] (emphasis added):

“We’re starting to see other interesting things to buy. Some of the public companies [referring to REITs] have struggled a bit in the US [referring to the low share prices]. So as we look forward to 2024, we think we’re going to be a lot more active in 2024 than we have been.”

He said that right as they announced the multi-billion-dollar acquisition of Tricon Residential, a major single-family rental landlord, at a 30% premium to its latest share price.

This is good evidence that REIT valuations remain opportunistic.

Remember that Blackstone is famous for buying real estate at a discount to its fair value. They are the biggest landlords globally and have better market intelligence than anyone else.

If they can afford to pay a 30% premium and still get a discount relative to what they think this is worth, then it is a pretty strong sign that REITs remain undervalued.

The reason why they seem to be doubling down now on their REIT investments is because interest rates are expected to drop lower later this year and this should create a “better market environment” according to Steve Schwarzman.

REITs dropped due to rising interest rates… and therefore, a drop in interest rates should have the opposite effect. Importantly, it will reset the narrative because it is ‘all about the direction’ of interest rates according to him.

Today, many REITs remain heavily discounted, but the window of opportunity could be closing and this appears to be why they expect to be a lot more active in 2024.

What Are Some Likely Buyout Candidates?

Steve Schwarzman makes it clear that they are only interested in a few specific things.

Firstly, he seems very interested in European real estate. This may seem surprising to some of you, given that Russia is still at war with Ukraine, but valuations are low and there’s a lot of distress due to overleverage. Here is what he said:

“European real estate is very interesting… But what’s happening is that interest rates were negative so people could borrow money very cheaply and now their cost of money now is 500 or 600 basis points higher. So people who use debt to own their portfolios are struggling and they have to pay down debt so they have to sell assets. We’re one of the few people in the world who have a lot of money and like to buy things.”

Just to give you a taste of how low valuations have become, consider the case of Branicks Group (BRNK / OTCPK:DDCCF), which is a major industrial and office landlord in Germany. Its latest NAV per share is €21.40, but its share price is just €2, representing a 90% discount. They are so cheap because they have major debt maturities coming in 2024, and they may not survive to see the recovery.

Steve Schwarzman is ready to pick up the pieces at low prices.

We agree with Steve, and also think that the European REITs are very opportunistic today. We own 6 European REITs and plan to accumulate more of them in 2024. One of our largest holdings is Vonovia (VNA / OTCPK:VONOY), which owns ~500k apartment units in Germany, Austria, and Sweden:

Vonovia

Secondly, Steve Schwarzman makes it clear that they are especially interested in industrial and residential real estate:

“People approach us w/ portfolios to buy and we say thank you for the opportunity. But we’re actually only interested in buying a few types of real estate. We really want to buy more warehouses, more student loans, one or two other classes. So if you could take this pile of stuff back and just give us what we’d like, we’ll buy it all. And so what tends to happen is they go back and they find all of the stuff of the type we’ll buy and they come to sell it and they often bring their best stuff. So we’re able to buy wonderful pieces of real estate at prices that work for us and they get liquidity. This is the start of distressed cycle for those owners.”

In another interview, he also said that they like other residential properties and data centers.

Here are potential buyout candidates that come to my mind after reading this:

Mid-America Apartment Communities (MAA): Blackstone has previously invested in the shares of MAA, which tells me that they know their assets very well and would be interested in owning the whole company. Today, the sunbelt apartment REIT is today priced at an estimated 30% discount on its net asset value, a historically low valuation. The one challenge here is that MAA is very big. Its market cap is $15 billion, but as we noted earlier, Blackstone bought $30 billion worth of REITs in 2022 alone. MAA would really move the needle for them, and they could pull it off.

Mid-America Apartment Communities

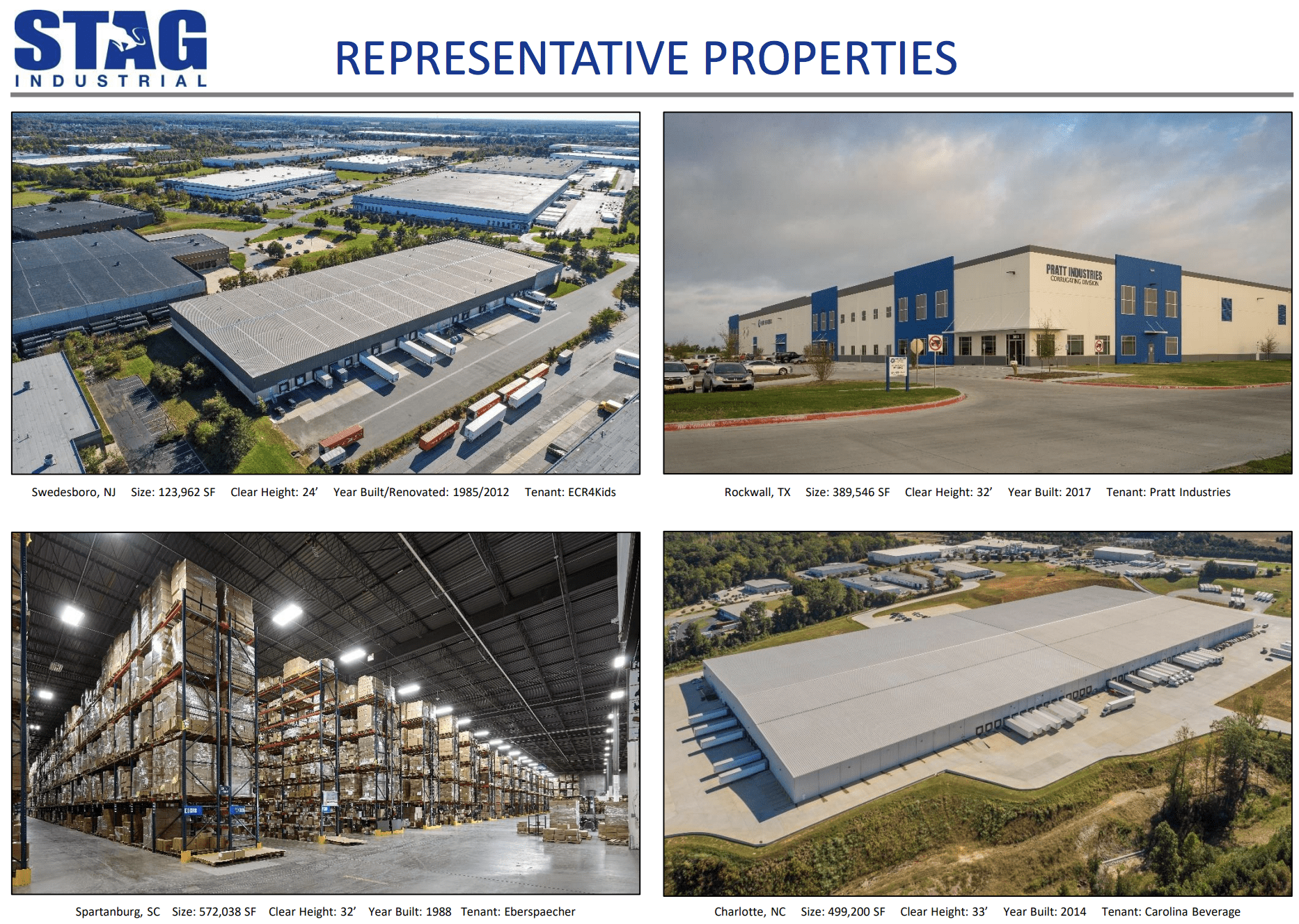

STAG Industrial (STAG): Blackstone likes industrial properties, and acquiring STAG could give them new capabilities that they are today missing. STAG follows a unique approach, focusing mainly on value-add deals in secondary markets. These markets are particularly well positioned to benefit from the growing trend of onshoring and will be less impacted by all the new supply hitting the industrial market. Today, STAG seems to trade at a reasonable valuation of 16x FFO, but this ignores the fact that its rents are deeply below market. The public REIT market is not giving much value to that since most investors only care about the next quarter, but Blackstone could see value in capitalizing on the mark-to-market opportunity.

STAG Industrial

Closing Note

If Steve Schwarzman is buying REITs and is willing to pay a large premium for them, it tells me that I am doing something right.

Valuations remain historically low and opportunities are abundant.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")