RiverNorthPhotography

Investment Thesis

T. Rowe Price (NASDAQ:TROW) is going to report its Q4 earnings on the 8th of February, pre-market. I wanted to have a look at the company’s financials and how they have developed over the last three quarters and give some info on the upcoming report and what I would like to see from the company going forward. I still believe the company is a buy at these levels, and any substantial drop in price would be a good time to start a position or build into a full position over time.

Briefly on Most Recent Financials

As of Q3 ´23, the company had over $5B in liquidity split in half between Cash and short-term investments against around $26m in long-term debt, according to Seeking Alpha. The company’s financial position is as strong as ever. Let’s look at how the company’s margins have developed over the last three quarters.

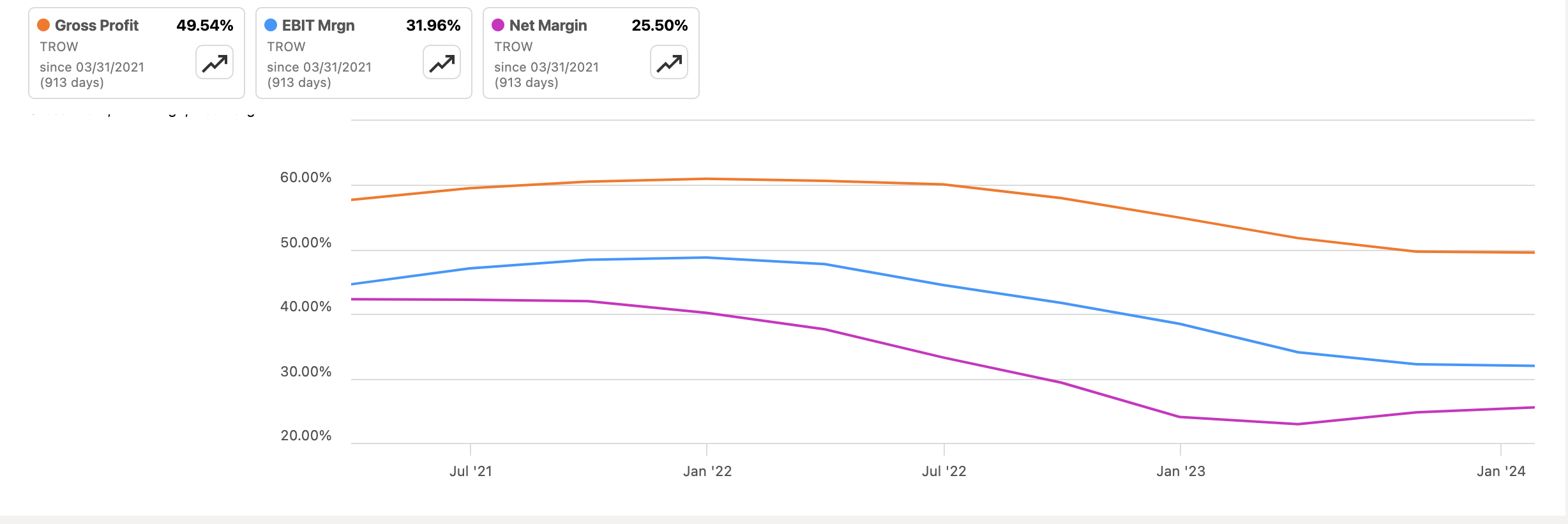

We can see that the gross and EBIT margins have been coming down over the last 3 quarters, as it has been the running theme over the last few years, which is not a good direction to go in, however, we can observe a trough forming. Is this the end of efficiency and profitability problems? Too early to tell, but it is a good sign.

Progress of Margins (SA)

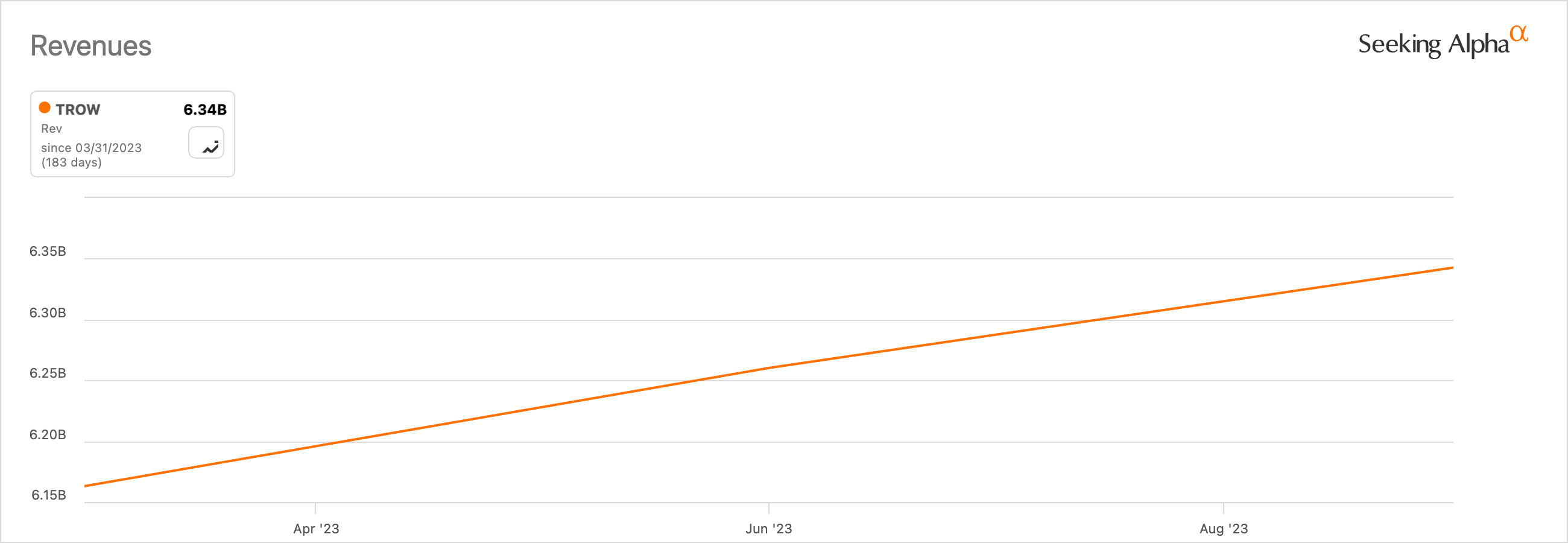

Revenues, however, have been trending upward this past year, which is a good sign. Even as assets under management, or AUM, have been coming down. The company managed to improve its top line in a very tough market, and that is commendable. There was very little the company could have done to stop the AUM bleeding when the economy was so uncertain regarding high-interest rates and high inflation. Investors get skittish and leave for high-yielding bonds.

Revenue progress (SA)

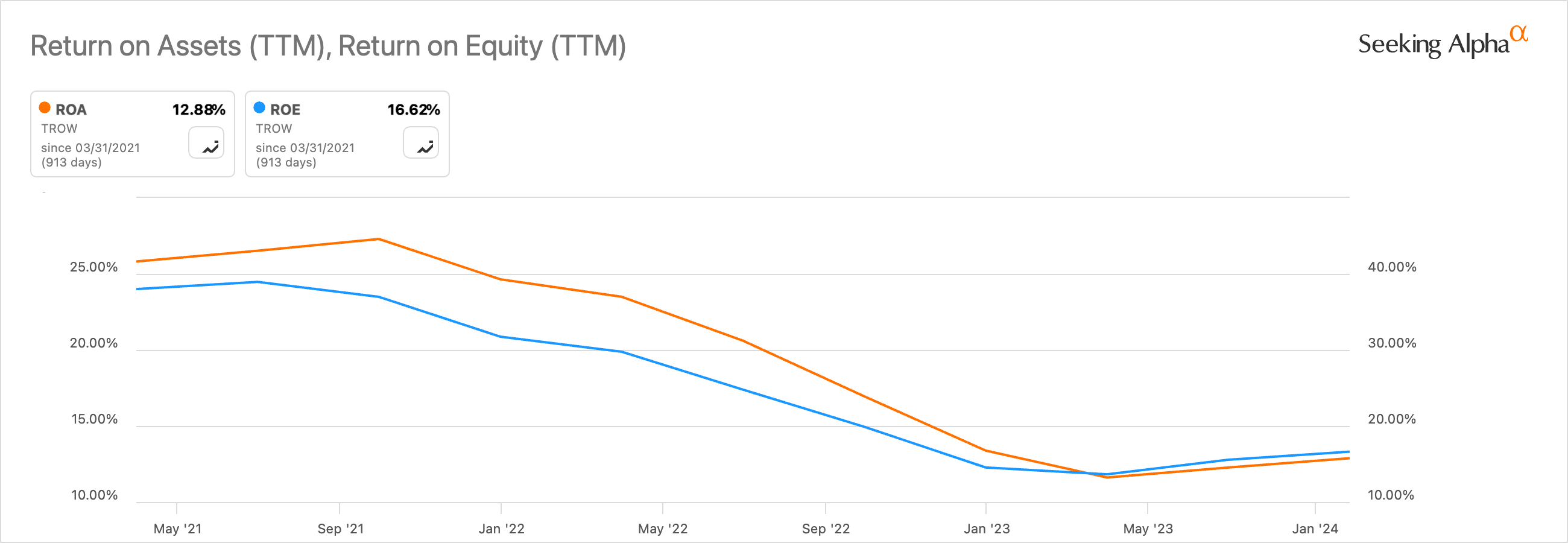

In terms of efficiency and profitability, it seems that the bottom has been set over the past couple of quarters, and we may see an improvement going forward in ROA and ROE, which have plummeted over the last 3 years as profitability evaporated.

ROA and ROE (SA)

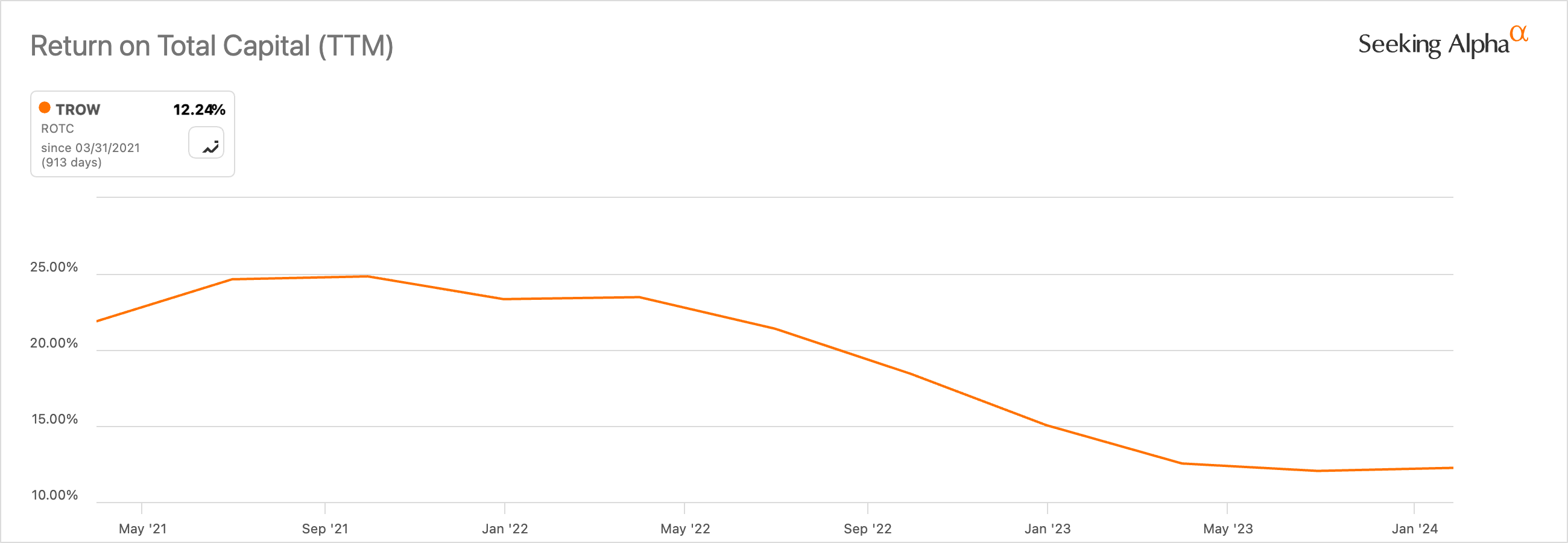

A similar situation can be observed in the company’s return on total capital, or ROTC, which measures how efficiently the company is using its total capital to generate profit. This also tells us if the company has a competitive edge and a moat. If we look at the last 3 years of performance, we can see a deterioration in the company’s moat and edge, however, a trough can be observed also.

ROTC (SA)

Overall, as I mentioned, we can see a bottom forming for the company. That may not necessarily mean it has formed as I would like to see a couple of quarters of improvements here, however, it does look positive. Revenues have been seeing a y/y increase in all of the quarters in 2023 except for Q1, which is a positive development.

What to Expect from Earnings

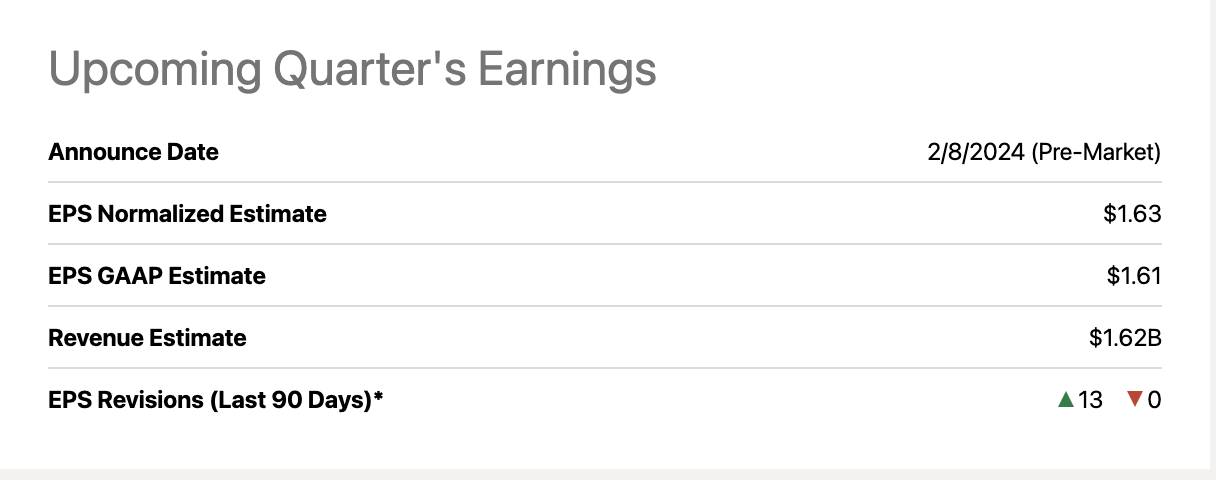

Analysts are expecting $1.63 and $1.61 adjusted and GAAP EPS, respectively, on around $1.62B in revenue. The management did not provide any numbers for Q4, however, Robert Sharps, the CEO of TROW did mention that “fourth quarter flows to be worse than recent trends with further weakness concentrated in November and December.” This is not a very positive news. The bleeding of AUM is continuing and that will deter many investors from starting a position, and I don’t blame them. As you can see below, the company’s EPS has seen 13 upward revisions in the last 90 days.

Earnings estimates (SA)

In terms of expenses, the company sees an increase of 2% to 4% over the comparable 2022 quarter, and that excludes any expenses related to compensation. The company expects many expense categories to be higher due to seasonality, where marketing and stock-based compensation usually end up being higher in Q4 compared to the rest of the quarters.

So, the top line should see around a 6% increase y/y, and expenses if we take everything into account unadjusted would probably come in at around the same, which is not curbing costs very efficiently, but I’ll give them the benefit of the doubt and will take the management’s comments at face value that seasonality is the reason expenses are higher. The next couple of quarters will dictate how well the company is handling expenses.

What I Would Like to See

I don’t think we will see a miss in upcoming earnings. I think the company is set up to beat the estimates quite nicely, and a miss would send the company’s share price down closer to $100 or even below.

In terms of margins, I would like to see expenses be contained, which we know is not going to be the case in the upcoming quarters, however, I would like to see an upward trend in efficiency and profitability in the later quarters continuing, to solidify that we have seen the trough here, and it’s only up from now on. In Q2, the management mentioned that they are focused on managing expense growth, however, it is a bit too early to tell if these cost-cutting measures have yielded results, however, I do like that the company is going to embrace a hybrid working environment, which means that from now on, the management will be reviewing its real estate costs, and if possible close some of these offices and consolidate for further savings. We can already see this happening with a consolidation of Owings Mills campuses into 4 buildings instead of 6 and are looking to reduce occupancy in their Colorado Springs buildings by the end of 23.

What I would like to see going forward in terms of AUM is obviously the bleeding of it to stop. With the preliminary reports, we can see that November saw a 6.1% increase in AUM and a 3.7% climb in December. Now, this is a given because the global markets saw a nice rally in the last 3 months, however, this tells us nothing about the net cash flows, which are predicted to be negative and worse than in the last couple of quarters even as markets rallied.

Q4 Rally of Major indices (SA)

A lot of the time, the big movements in share price on the day of earnings come from the guidance the management provides. I have a feeling that it is not going to be very positive, and I expect cash outflows to dominate in the upcoming quarter, however, I do hope that Q1 ´24 will not be as bad as Q4 outflows.

Risks

The macroeconomic environment is far from being certain and with the most recent FOMC meeting gone by where the FED chair J Power diminished all the hopes of having cut rates commencing in March, the volatility is alive and well in the global markets, which will affect TROW share price significantly if we are not going to get any more clarity on what is going to happen going forward, which will lead to further fears of investors and further outflows.

The management needs to show us that they are capable of curbing costs effectively. It may seem that margins have bottomed how, however, we may see further downside here if the cost-cutting measures are not good enough, which will no doubt bring further downside in the price of the shares.

The company overall needs to do better at retaining clients’ funds. It seems like the company is not offering enough value to retain clients’ cash and so are seeing consistent outflows. It may all be due to the macro uncertainties, but I can’t blame only that as I believe the company needs to do a better job at marketing its funds better, to show that it is better to stay invested during the turbulent times if you are focused on the long-term. If the company is not going to improve on that, outflows may continue, and we will see more risks to the downside.

Closing Comments

Overall, I still believe the company is a great long-term play, and once we are going to see certainty in the macroenvironment, investors will start to see value in the company and will start to buy up. I do think there will be more hurdles ahead, however, with such a strong financial position, I don’t doubt the company’s ability to remain resilient until everything starts to turn around. I am maintaining my long-term buy recommendation, and for any further substantial weakness in price, I would consider it to be an opportunity to accumulate into a full position over time.

I would like to see the cost-cutting measures bearing fruit over the next couple of quarters to make sure we did hit the bottom already, but in the long run, the low margins should just be a blip, that should be fixed in no time if cost-cutting initiatives are effective.

Q2 2024 Earnings Call Transcript")