Sundry Photography

Overview

Seeking Alpha analysts have rated ARM (NASDAQ:ARM) stock as a Sell, citing concerns over its valuation despite recognizing its strong business model and dominance in the semiconductor market. In this article, I will challenge this perspective by introducing the Dominance Company Method, a modified version of the traditional discounted cash flow approach. Through this method, I aim to demonstrate that ARM may not be as overvalued as commonly perceived by analysts. I encourage you to explore this methodology with me, as it may reveal an opportunity that is being overlooked.

ARM’s business model revolves around licensing intellectual property (IP) for chip design and collecting royalties from chip manufacturers. Renowned for its substantial investment in research and development, ARM has solidified its dominant position in the smartphone market and is expanding its dominance into other sectors such as cloud computing, PCs, electric and autonomous vehicles, robotics, IoT, and VR headsets.

Traditional Valuation

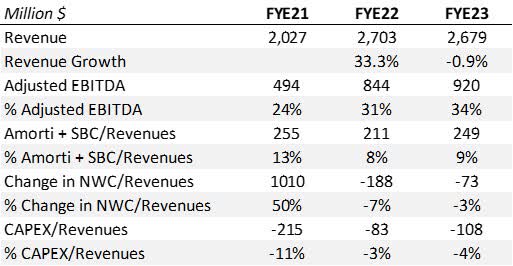

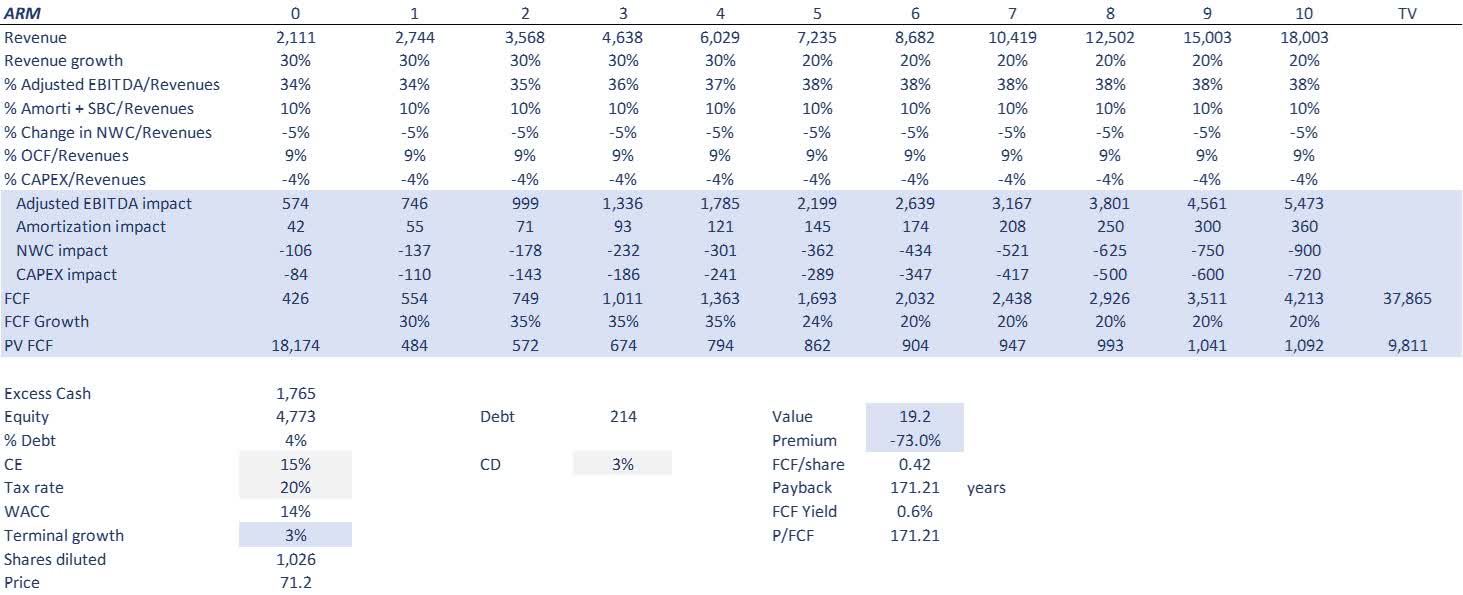

In fiscal year 2023, revenue remained relatively flat compared to 2022 as you can see in Figure 2. However, in the second quarter of 2024, revenue reaches a record high of $800 million, marking a 28% increase year over year. To forecast future growth, I conservatively assign a growth rate of 30% for the first five years and 20% from year six until ten. This projection may even underestimate the company’s potential given its presence in high-growth industries such as PC AI, IoT, cloud computing, automotive, and robotics. Additionally, factors like increased revenue per SOC (System on Chip) due to greater complexity and a business model that fosters significant network effects contribute to this optimistic outlook.

Margins, represented by Adjusted EBITDA (which includes stock-based compensation), currently stand at 34% of revenues, showing steady growth from 24% and expected to reach 38% after five years. This trend is supported by economies of scale in research and development and strengthening network effects as the company expands its business. Other key value drivers, including Amortization, Stock-Based Compensation, Change in Net Working Capital, and Capex, are estimated to remain proportional to revenues over the ten-year period, with changes of 10%, -5%, and -4%, respectively.

Figure 2: Author based on ARM financials

Free cash flow is discounted at a weighted cost of capital (WACC) of 14%. Following a traditional valuation method, I project free cash flow for the next 10 years. Additionally, I calculate a terminal value using the same WACC and a perpetual growth rate of 3%. This approach assumes that beyond year 10, the company will grow at the same rate as the economy.

Figure 2: Author based on ARM financials

Using this methodology, I value the company at $19 per share, compared to the current market price of $76 per share. This translates to a price-to-free cash flow ratio of 182 and a free cash flow yield of 0.5%. Given this valuation, the stock appears to be significantly overpriced, aligning with the common sentiment that it is ‘priced for perfection.’ Therefore, a clear recommendation would be to sell.

New perspective in valuation: the Dominance Company Method

In the previous section, I assumed a 30% growth rate until year 5 and 20% until year 10, followed by a long-term growth rate of 3%, which is a common practice in free cash flow valuation. However, it’s important to delve deeper into these assumptions. Firstly, there’s a significant shift between year 10 and year 11, transitioning from 20% growth to a terminal growth rate of 3%. This assumption inherently results in a loss of value, as the typical progression is towards a gradual decline to 3% over many years.

Secondly, industry competition may limit business growth to match GDP growth, typically around 3%. This assumption reflects the idea that businesses cannot outpace overall economic growth. That is not always the case.

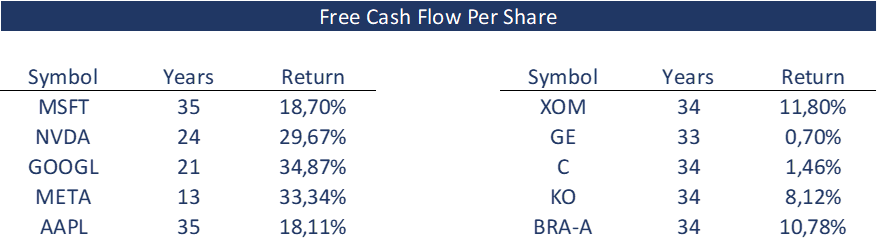

Now, let’s challenge these assumptions. Consider the possibility that a business’s growth rate remains unchanged indefinitely due to its exceptional performance. While this scenario may seem improbable, historical data provides insight. Figures from the past 34 years reveal consistent and extraordinary growth rates for companies like Microsoft (MSFT), Apple (AAPL), Nvidia (NVDA), and Meta (META), with compounded annual returns ranging from 18% to 33%.

Analyzing this data, I establish that an exceptional business can sustain a compounded growth rate of 18% in its free cash flows for 35 years. Applying this growth rate to ARM for 35 years, followed by a gradual decline of 1 percentage point each year until reaching 3%, yields a valuation of ARM stock at $82 per share.

Figure 3: Author

To contrast between great and good businesses, consider the table on the right, showcasing businesses that are good but not exceptional. For instance, General Electric demonstrates an overall growth rate of 0.7%, while Citigroup exhibits 1.46%. In comparison, renowned companies like Coca-Cola or Berkshire Hathaway maintain a growth rate around 10%. My thesis posits that an 18% growth rate over 35 years is only viable for exceptional businesses. This highlights a common pitfall among value investors who apply traditional hypotheses to unprecedented businesses, potentially missing out on significant opportunities, as Warren Buffett and Charles Munger have acknowledged, not investing in Google. Therefore, I propose this valuation method to be called the Dominance Company Method (DCM).

My conclusion, considering ARM’s potential as a great business, I quantitatively ascertain that the stock is undervalued and represents a clear buying opportunity. However, the question remains: Is ARM truly a great business? Let’s explore further.

ARM Business Model

Historically, semiconductor companies took on an integrated model, managing the entire process from design to production and sales. ARM’s strategic edge lies in its specialization, excelling particularly in microprocessor designs. By focusing solely on design, ARM fosters collaboration with semiconductor manufacturers, supplying them with ready-made designs and benefiting from the collective insights of a diverse client base.

ARM’s expertise enables semiconductor manufacturers to skip the initial stages of processor design. Their designs are enriched by insights from various industries, backed by ARM’s substantial investment in research and development ((R&D)) and economies of scale. This robust foundation solidifies ARM’s leadership in microprocessor design.

The network effects within ARM’s ecosystem further bolster its market position. As more software developers adopt ARM processors, semiconductor companies are incentivized to follow suit to ensure compatibility and expand their market reach and the other way around, as more electronic devices adopt ARM more software developers wil write code in ARM. The significant barriers to entry, including ARM’s years of design experience and substantial R&D investment, deter potential competitors. Moreover, once a client adopts ARM’s platform, switching costs become substantial due to the integration of operating systems and applications tailored to ARM architecture.

ARM’s collaborative ecosystem, comprising original equipment manufacturers ((OEMs)), semiconductor manufacturers, electronic design automation (ADE) software providers, and software application developers, amplifies its dominance in microprocessor design. This strategic focus, along with its energy efficiency and streamlined coding structure, positions ARM to shape the future of computing.

In the mobile-phone chips industry, ARM commands over a 99% market share, with expectations of significant growth in data-center and PC chips in the coming years. Major PC vendors are also poised to enter the Arm-based CPU market, diversifying the sector and intensifying competition. The involvement of AMD and Nvidia in Arm-based PC chips, along with Nvidia’s expertise in high-end gaming GPUs, signals a robust entry into the premium PC space.

Considering ARM’s transformative potential, I believe it justifies a valuation based on the Dominance Company Method.

ARM faces some risks

While my use of the Dominance Company Method has revealed ARM to be undervalued, traditional valuation methods employed by the market perceive the company as expensive. Consequently, the stock is highly sensitive to news, leading to periods of volatility and potential price declines. However, I assure you that such fluctuations will likely be temporary.

One significant risk facing ARM is the challenge of maintaining its dominance in the PC and server markets while expanding into AI. Intel (INTC), a long-standing leader in the PC market since the 1980s, recently launched a new generation of AI chips with potential better performance improvements and power-saving features. Intel’s ability to adapt to evolving requirements should not be underestimated, as an effective response from Intel could impede ARM’s growth trajectory and adversely affect the stock price.

Another risk to consider is the potential emergence of new competitors facilitated by AI tools in chip design software such as those developed by Cadence Design Systems and Synopsis, which streamline chip design processes akin to ARM’s characteristics. While these competitors may arise from niche segments of the market, the overall impact may be limited.

Conclusion

I have introduced you a new method based on the traditional discounted cash flow method but adding more years at a high growth rate because that has been the behaviour of the dominants players, specially in Tech.

Even the prominent perception of the market is that ARM is expensive, based in the Dominance Company Method, I consider it cheap or fairly valued. I think ARM is going to dominate the chip market. So I recommend to buy the stock and keep track of the evolution of the semiconductor market.

Q2 2024 Earnings Call Transcript")