Michael Vi

Over the last year or so, the semiconductor industry has been one of the hottest places to invest.

The iShares Semiconductor ETF (SOXX) is up by more than 44% during the past 12 months (more than doubling the S&P 500’s 19.15% performance).

Stocks like Nvidia (NVDA), Broadcom (AVGO), and Advanced Micro Devices (AMD) seem to get most of the publicity here (and for good reason).

Their artificial intelligence prospects have pushed shares of those companies higher by triple digits during the last year.

But they’re not the only semiconductors executing well.

Qualcomm (NASDAQ:QCOM) shares have been flying under the radar (up a measly 6% during the last year). After a tough year (operationally speaking), this company just reported a huge Q1 beat and analysts are calling for double-digit earnings growth this year.

I’ve held this stock for years. There’s been plenty of ups and downs, but ultimately, QCOM has treated me well.

My cost basis is $76.44. That points toward 86% gains. And when you add in all of the dividends I’ve received over the years, my total returns here are well north of 100%.

But what’s in the past is in the past. Yes, QCOM has dominated the mobile chip space throughout the last decade or so. But, can they stay relevant moving ahead as the technology landscape shifts?

I think so. Here’s why.

Qualcomm Continues To Lead In The Handset Space

For years, investors have talked about the handset (cell phone) market maturing, and yet, companies like Apple and Samsung continue to print cash.

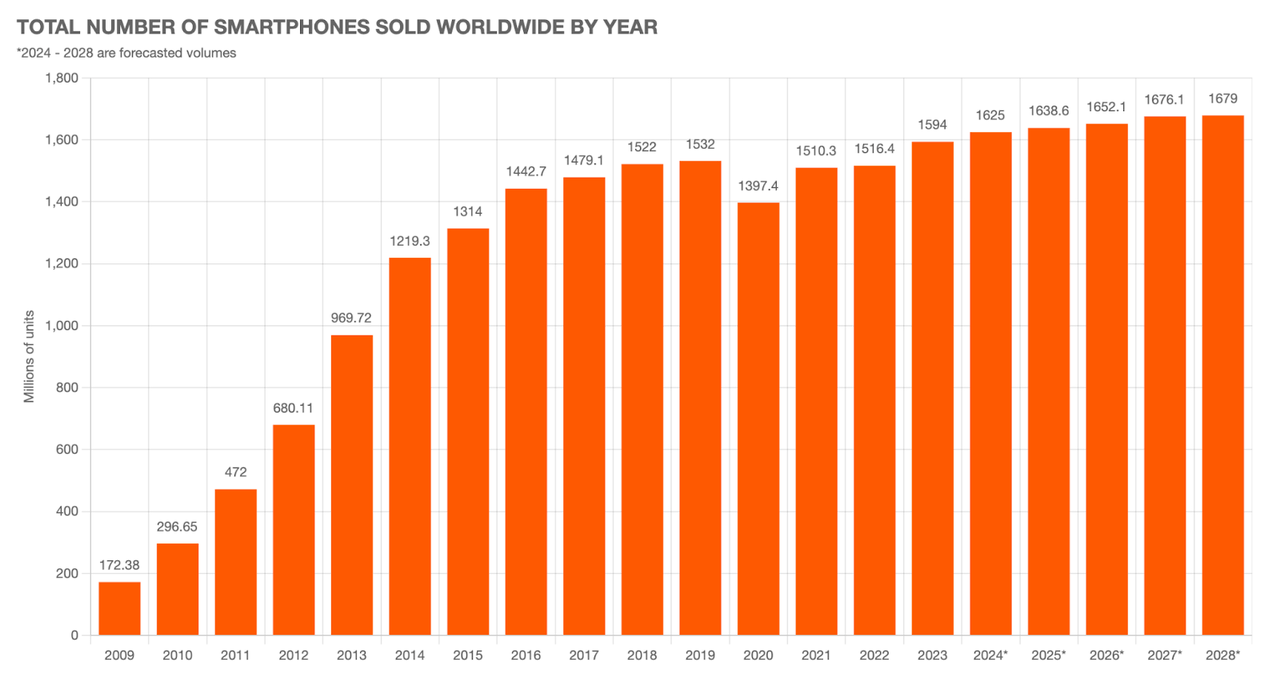

According to SellCell, there were nearly 1.6 billion smartphones sold in 2023.

SellCell

Furthermore, their data suggests that the post-pandemic growth trend isn’t going to end anytime soon.

Yes, tech companies are making progress with wearable and other disruptive tech that could eventually replace the need to carry a cell phone around. However, I don’t think that’s a near-term threat for the industry.

A bigger threat, in my opinion, are the biggest handset companies, such as Apple, moving chip/modem design in-house.

However, for now, at least, it’s widely recognized that QCOM produces the best handset chips and that segment continues to produce.

QCOM’s handset sales grew by 16% during Q1 and the company continues to innovate, resulting in better battery life and CPU/GPU performance metrics, meaning that if the next stage of the handset evolution is centered around AI-enabled smartphones, Qualcomm’s latest generation snapdragon should put the company in a highly competitive position.

Either way, AI or not, having a personal computer in your pocket remains an integral part of modern life and that’s not going to change anytime soon.

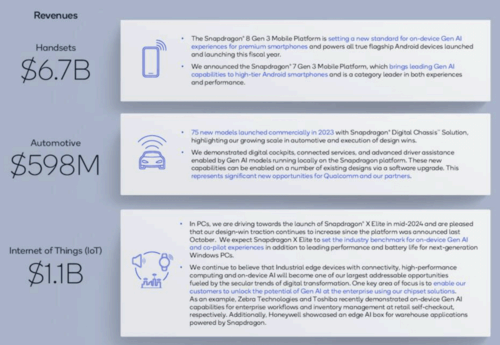

What’s more, QCOM has acknowledged threats of slowing handset growth (and rising competition) by diversifying into other end markets.

Handset chips still made up roughly 79% of its Q1 hardware sales. However, QCOM’s Internet of Things and Automotive segments now both have $1b+ annual run rates.

QCOM Q1 ER Presentation

I like these moves. As we enter into the fifth industrial revolution I expect to see massive demand in both the IoT and automotive industries as essentially all parts of our lives become connected, enabling more and more big-data collection (which will power AI/automation and lead to more efficient, and ideally, simpler/easier lives).

Simply put, it seems that QCOM plans to use its handset cash flows to move into other areas of the tech space with secular growth tailwinds, and that seems like a prudent long-term plan to me.

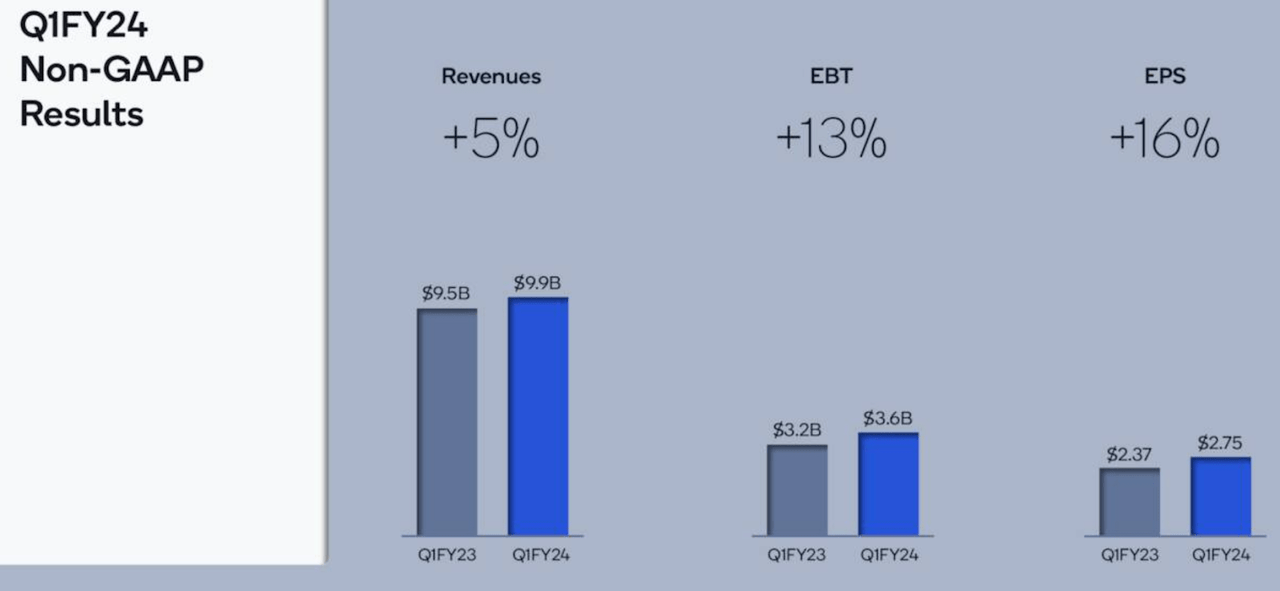

First Quarter Results

QCOM Q1 ER Presentation

QCOM’s bottom line soared in the aftermath of the pandemic because of the combination of strong demand for its products and supply chain issues that resulted in shortages across the semiconductor industry.

In 2021, QCOM’s EPS rose by 104%.

In 2022, it followed that result up with a 47% growth year.

Obviously, that wasn’t sustainable. It actually created comps that the company couldn’t keep up with in 2023, where earnings fell by 33%.

However, analysts were bullish on the company’s bounce-back prospects this year (consensus pointed towards full-year EPS growth of 14%) and QCOM’s Q1 results appear to validate Wall Street’s bullish outlook for 2024.

Coming into the quarter, Wall Street was calling for $2.37/share in earnings, which would have represented flat y/y growth. Well, QCOM soared past that estimate, posting EPS of $2.75, up 16%.

During the Q1 conference call, QCOM’s CEO, Cristiano Amon, mentioned that 2023 was a tough year for QCOM’s Android sales, calling 2023 “a year of correction.”

However, the company was bullish on its Android business moving forward.

Amon said, “We’re also announcing that we extended a multi-year agreement with Samsung relating to Snapdragon platforms for flagship Galaxy smartphone launches starting in 2024. The extended agreement demonstrates the value of Snapdragon 8, our technology leadership and our successful long-term strategic partnership with Samsung.”

Furthermore, Amon noted that QCOM has recently signed agreements with other major handset makers, providing a bit more clarity for its QTL segment over the coming years.

He said, “First, Apple exercised its unilateral option to extend its global patent license agreement for an additional two years, taking the existing agreement through to March 2027; second, we have renewed long-term agreements with two significant Chinese smartphone OEMs.”

QCOM shares are down today, in part because it appears that the company is having trouble gaining share in the Android segment. However, overall, QCOM followed up its big Q1 with solid Q2 guidance, leading me to believe that shares are fairly priced here in the $140 area.

QCOM is calling for EPS of $2.20-$2.40 during Q2 (compared to $2.15 a year ago).

That $2.30/share midpoint represents 7% y/y growth.

And considering that QCOM’s November 2023 guidance for Q1 was $2.25-$2.45, and they ended up posting $2.75 I wouldn’t be surprised if they’re sandbagging a bit here.

$2.50/share in Q2 would represent 16% y/y growth (the same as Q1) and that would be a smaller beat than we just saw.

I’m not here to say that QCOM is lying, but it’s in their best interest to set a low bar and clear it, rather than being overly aggressive and miss.

I’m cautiously optimistic that they can carry the Q1 momentum into the second quarter and produce another beat that sets them up for strong double-digit growth for the full year (remember, Wall Street consensus is calling for 14% EPS growth in 2024 and another 12% in 2025 right now).

Valuation

QCOM shares are down by roughly 5% as I write this, trading for $141.11/share.

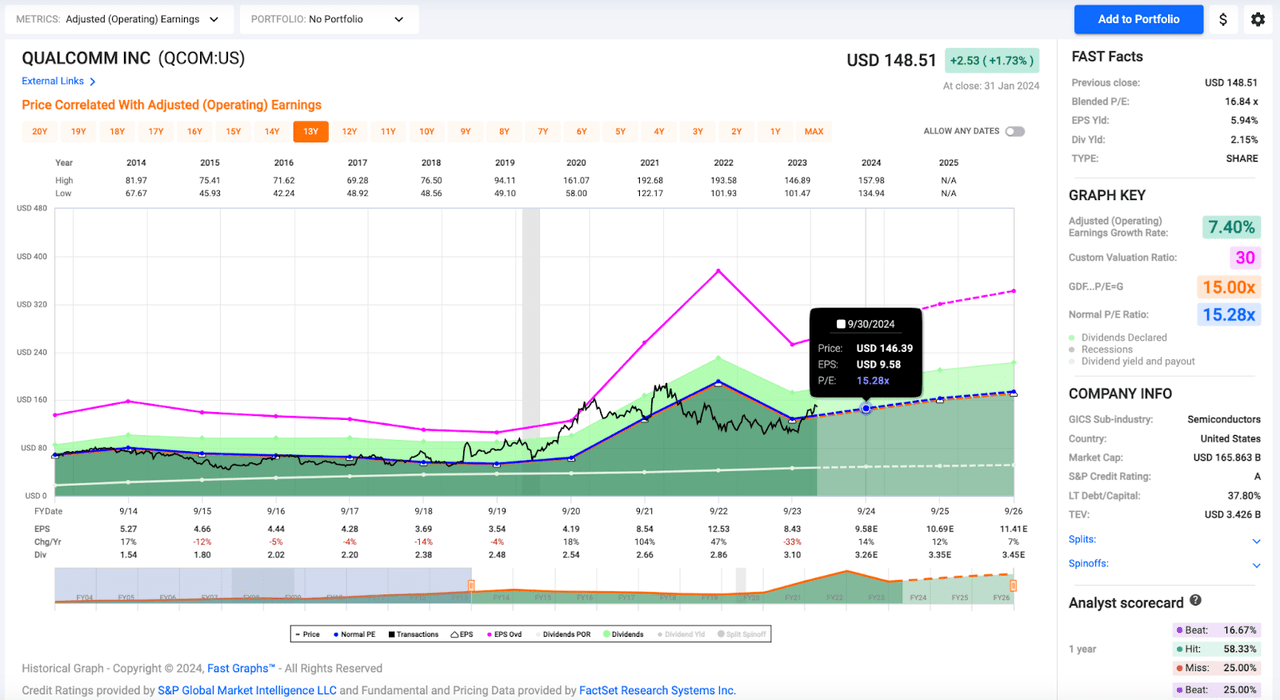

Assuming that QCOM continues along its strong EPS growth trajectory throughout 2024 and hits the analyst consensus of $9.58/share, then this dip has pushed the stock down to a level where it’s trading at a discount to historical fair values on a forward basis.

QCOM’s 20-year average P/E ratio is 20.1x.

Frankly, I think that’s a poor comp because it includes some very high growth years back during the early days of the 3G/4G revolution that QCOM isn’t likely to replicate anytime soon.

QCOM’s 10-year average P/E is 15.3x, which seems like a more reasonable multiple to pay for QCOM shares at this point in its growth cycle.

FAST Graphs

Over the last 10 years, QCOM’s EPS growth has been much more volatile than it was during the prior decade – and the growth has been slower.

From 2013-2023, QCOM’s EPS growth CAGR was 6.5%.

Obviously, the 12%-14% forward growth that analysts are calling for during the next 24 months is better, but due to the risks associated with rising competition in the handset space and the unproven nature of QCOM’s IoT/automotive segments (I don’t believe that QCOM has established itself as a leader in these areas like it has with handsets over the years), I’m not willing to pay a premium for shares.

QCOM’s five-year average P/E is 17.3x. However, I think that’s pricey as well (it’s elevated by the 30x+ multiples that were attached to the stock during 2020).

Remember, it wasn’t long ago that QCOM was trading for just 10x earnings in the $100/share area.

The stock has rallied nicely since its 2023 lows, but it’s clear that the floor here, from an earnings multiple standpoint, is much lower than its peers (who more clearly benefit from secular growth tailwinds).

~15x forward estimates is ~$145.

That’s where my fair value estimate lies.

Therefore, at $141 QCOM offers a slight margin of safety (~3%); however, that’s not enough to entice me to add to my stake.

The Dividend

Even though I’m not interested in adding to my QCOM stake at today’s prices, I’m happy to continue to hold.

Why?

Because QCOM’s 2.15% dividend continues to grow at an acceptable rate.

Qualcomm has been growing its dividend for 20 consecutive years.

Its most recent dividend raise was 6.7%.

QCOM’s five-year dividend growth rate is 5.33%.

With EPS growth accelerating, I think QCOM can sustainably increase its dividend by 6-8% in 2024 and 2025 as well (on a forward basis, the stock’s EPS payout ratio is just 33.3%).

Admittedly, a ~2% yield growing at a mid-to-high single-digit clip isn’t exciting. But, slow and steady growth like this can generate strong results over the long term.

My yield on cost is currently 4.2%.

And assuming we see a rise to the $3.40-$3.50/share annual range when QCOM announces raises its dividend in March, I’ll be looking at a 4.5% YoC.

In another decade, I wouldn’t be surprised to see my YoC approaching double-digit levels, and as someone who plans to live off of the passive income that my portfolio generates throughout my retirement, safe dividends that have steady above-inflation-level growth are assets that are easy for me to hang onto.

Furthermore, QCOM has a long history of returning cash to shareholders via buybacks and effectively using share repurchases to reduce its outstanding share count.

Macrotrends

So, while this isn’t a high-conviction buy for me right now, QCOM remains a generous big-tech name that I sleep well at night owning because of its strong cash flows in the present, its potential to capitalize on secular growth trends moving forward, and its long history of generous shareholder returns.

Conclusion

Overall, Qualcomm’s quarter was solid.

I think that the Q1 numbers, alongside management’s updated Q2 guidance, set this company up for a nice year in 2024.

However, because QCOM faces rising competition in its primary market (with Apple and Samsung both attempting to move chip design in-house) and lacks some of the secular growth tailwinds that its more popular peers are set to benefit from in the coming years (namely AI/data center related hardware), I’m not willing to pay a premium for shares.

I believe that QCOM is trading near fair value in the present; therefore, this stock is a “hold” in my portfolio.

Q2 2024 Earnings Call Transcript")